Financial Analysis and Accounting Assignment - Holmes Institute

VerifiedAdded on 2022/11/26

|7

|1323

|145

Homework Assignment

AI Summary

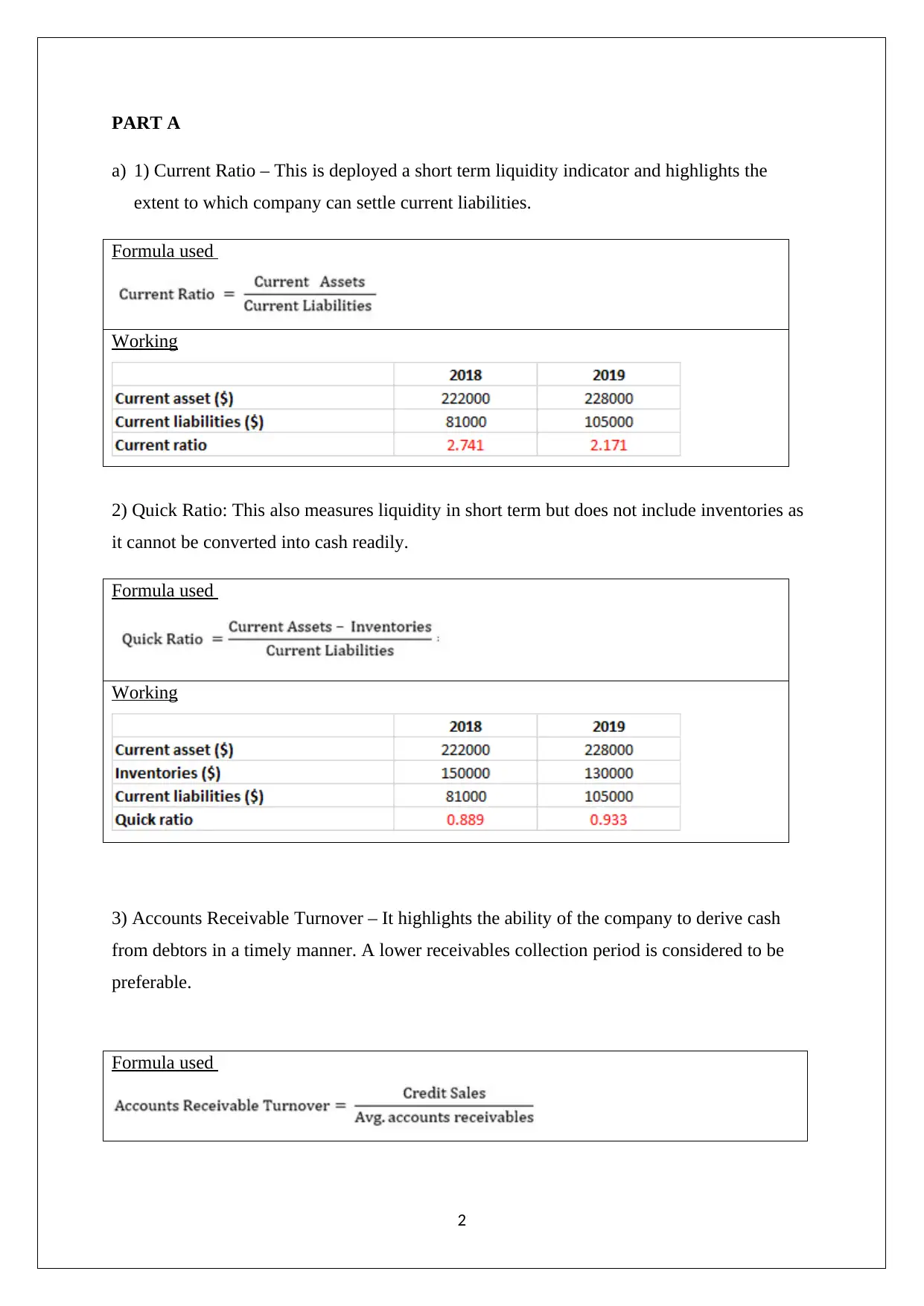

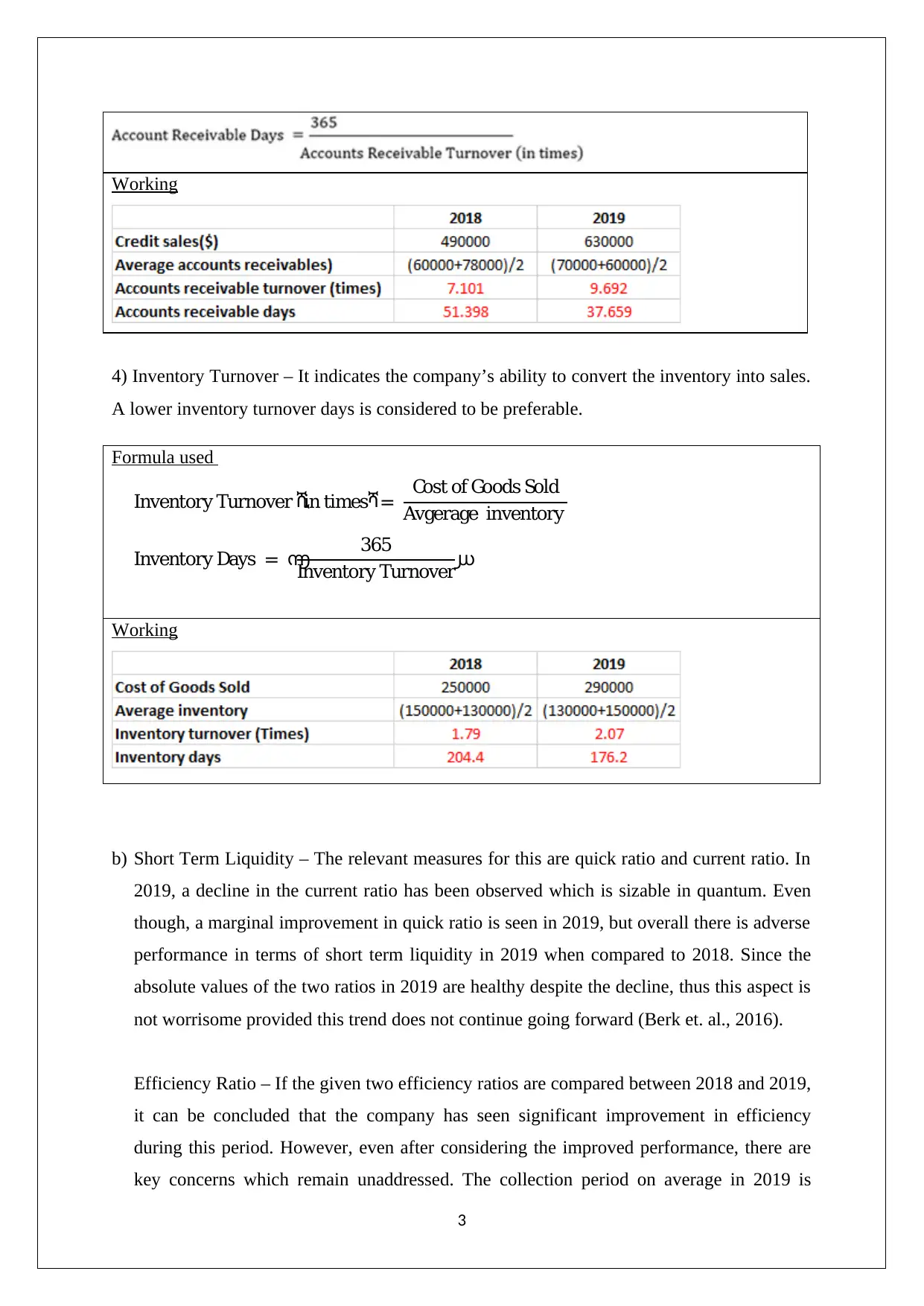

This assignment solution for the Accounting for Business course (HC1010) involves a detailed analysis of financial statements and key financial ratios. Part A focuses on calculating and interpreting ratios such as the current ratio, quick ratio, accounts receivable turnover, and inventory turnover to assess short-term liquidity and efficiency. The analysis compares financial performance between 2018 and 2019, highlighting improvements and areas of concern. Part B delves into the definitions of income and revenue, classifying various financial items (software sales, interest, discounts, share issues) correctly. Part C applies financial analysis to a loan scenario, comparing ABC and XYZ companies based on their current ratios and liabilities to determine which company is a better candidate for a loan, and assessing the valuation of the two companies based on their liabilities and asset base. The solution references several accounting and finance textbooks and standards like AASB.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.