Accounting for Business: Financial Analysis and Decision Making

VerifiedAdded on 2022/11/26

|6

|1264

|465

Homework Assignment

AI Summary

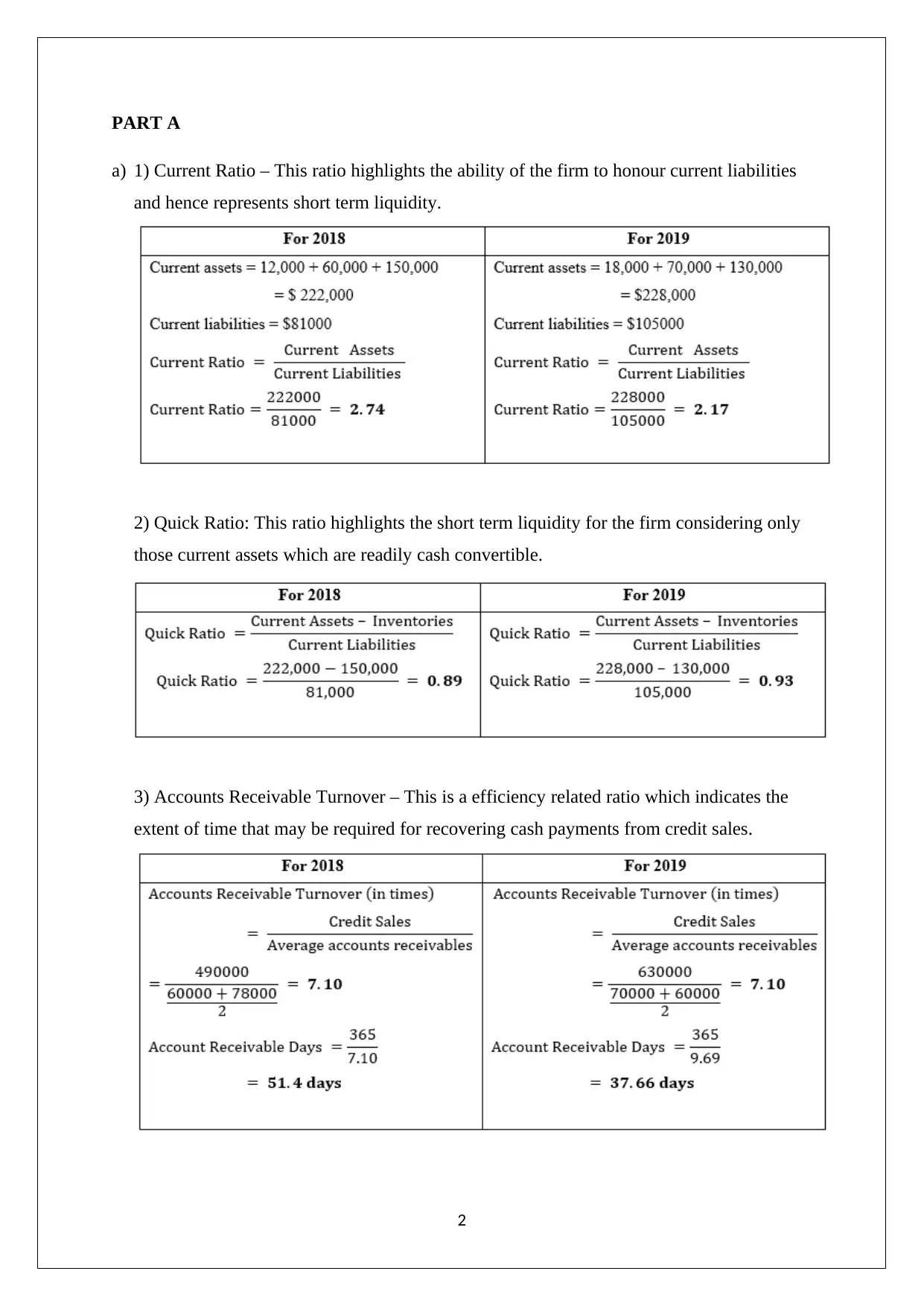

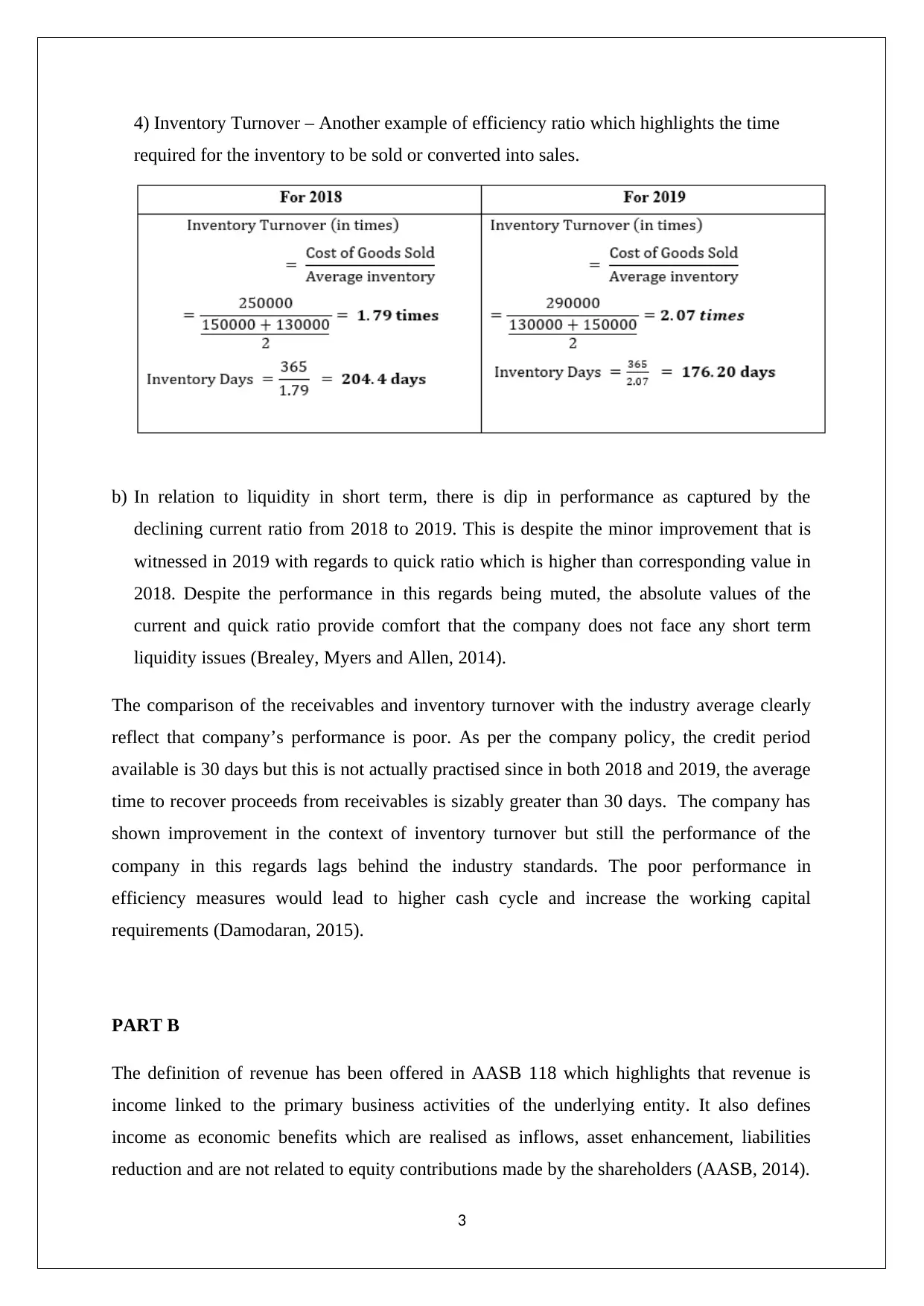

This assignment solution delves into key financial concepts, including ratio analysis, revenue recognition, and short-term loan decisions. Part A focuses on evaluating a company's liquidity and efficiency using ratios like current, quick, accounts receivable turnover, and inventory turnover. The analysis compares performance over two years and against industry averages, highlighting the impact of efficiency measures on working capital. Part B addresses the application of AASB 118 to determine revenue recognition for various financial items, distinguishing between revenue and other income sources. Part C provides a comparative analysis of two companies (XYZ and ABC) to determine the most suitable candidate for a short-term loan and a higher company valuation, considering liquidity, capital structure, and existing liabilities. The solution is supported by references to relevant accounting and finance literature.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.