HC1010: Financial Statement Analysis - Accounting for Business

VerifiedAdded on 2023/03/23

|6

|1206

|37

Homework Assignment

AI Summary

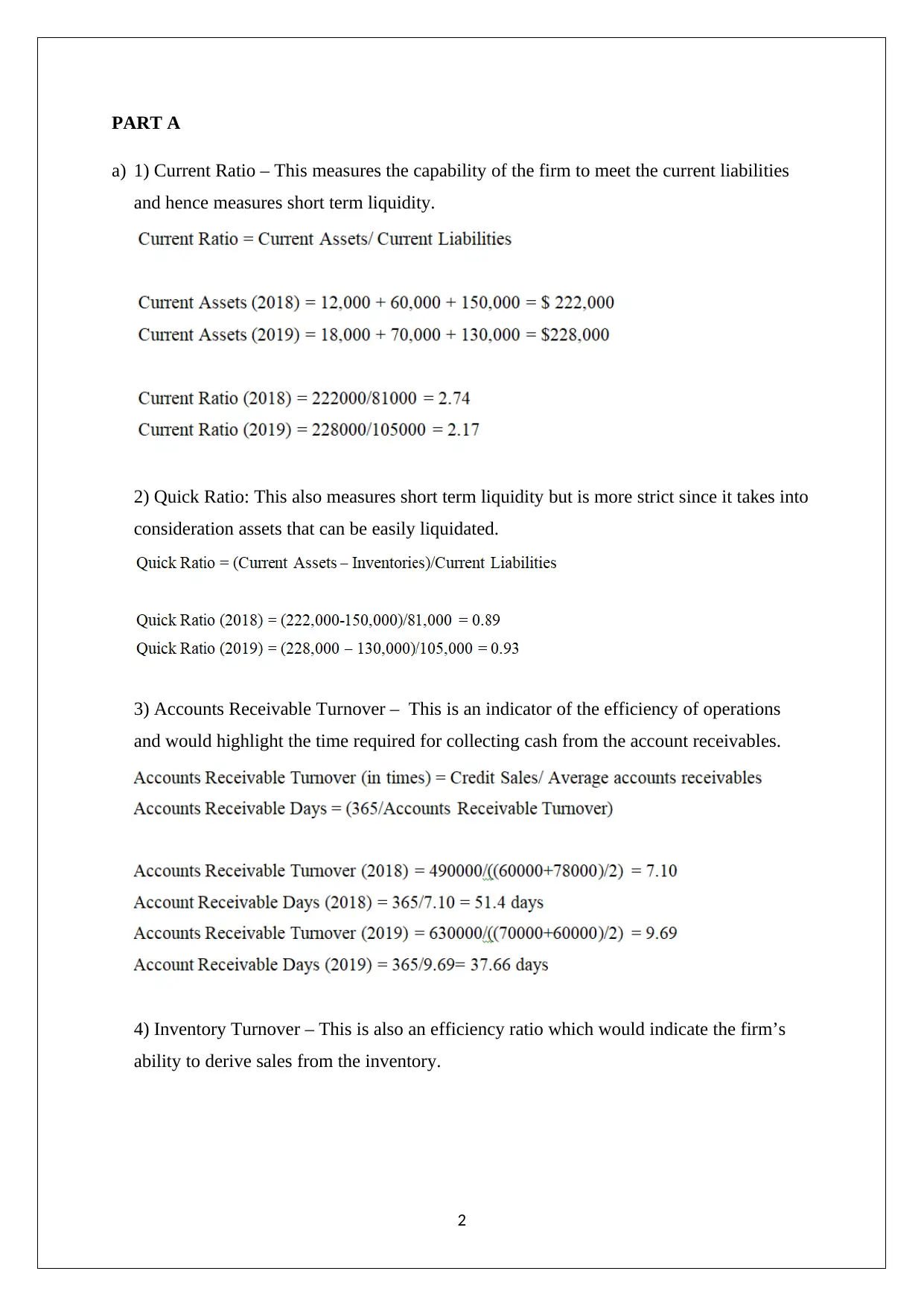

This assignment solution for an Accounting for Business course (HC1010) provides a detailed analysis of financial statements, focusing on ratio analysis, liquidity, and operational efficiency. It evaluates a company's ability to meet short-term liabilities using current and quick ratios, and assesses operational efficiency through accounts receivable and inventory turnover. The solution also addresses revenue recognition in accordance with AASB 118, categorizing various cash inflows for Green Apple Ltd. Furthermore, it compares two companies (ABC and XYZ) based on their financial health, capital structure, and debt liabilities to determine investment preferences. Desklib offers a wide range of study resources, including past papers and solved assignments, to support students in their academic endeavors.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.