Holmes Institute - Accounting for Business Assignment T1 2019

VerifiedAdded on 2022/11/26

|6

|1184

|234

Homework Assignment

AI Summary

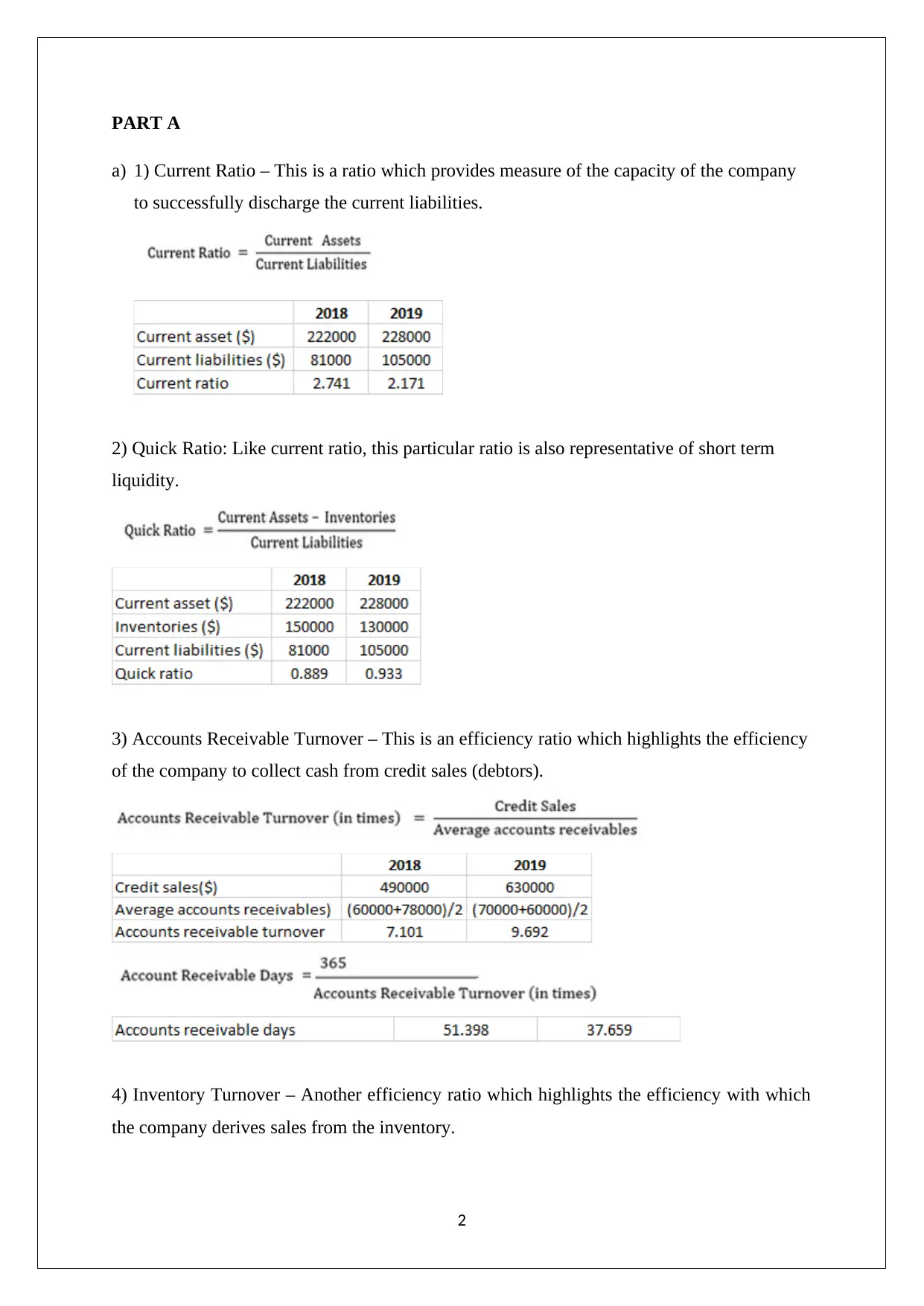

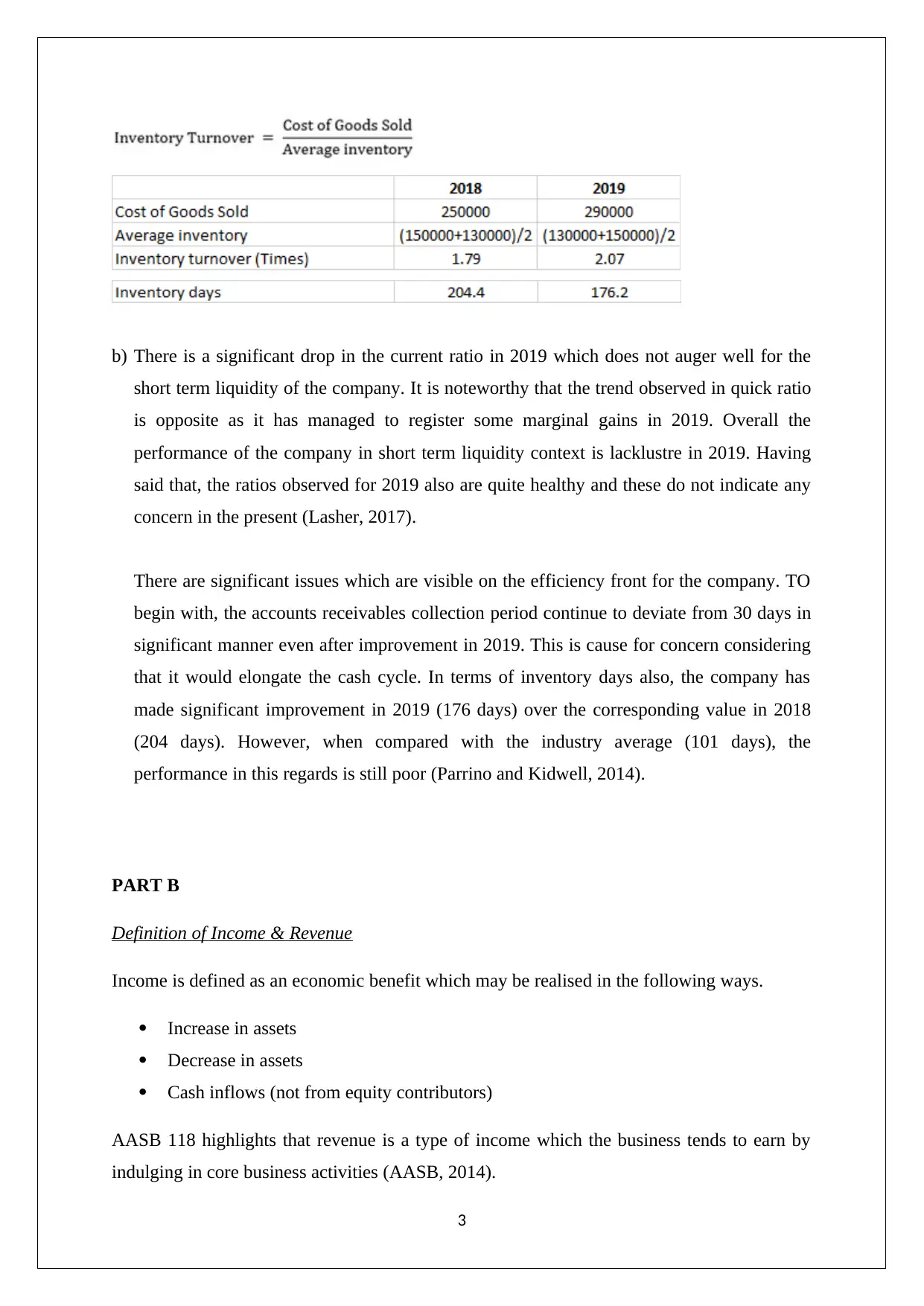

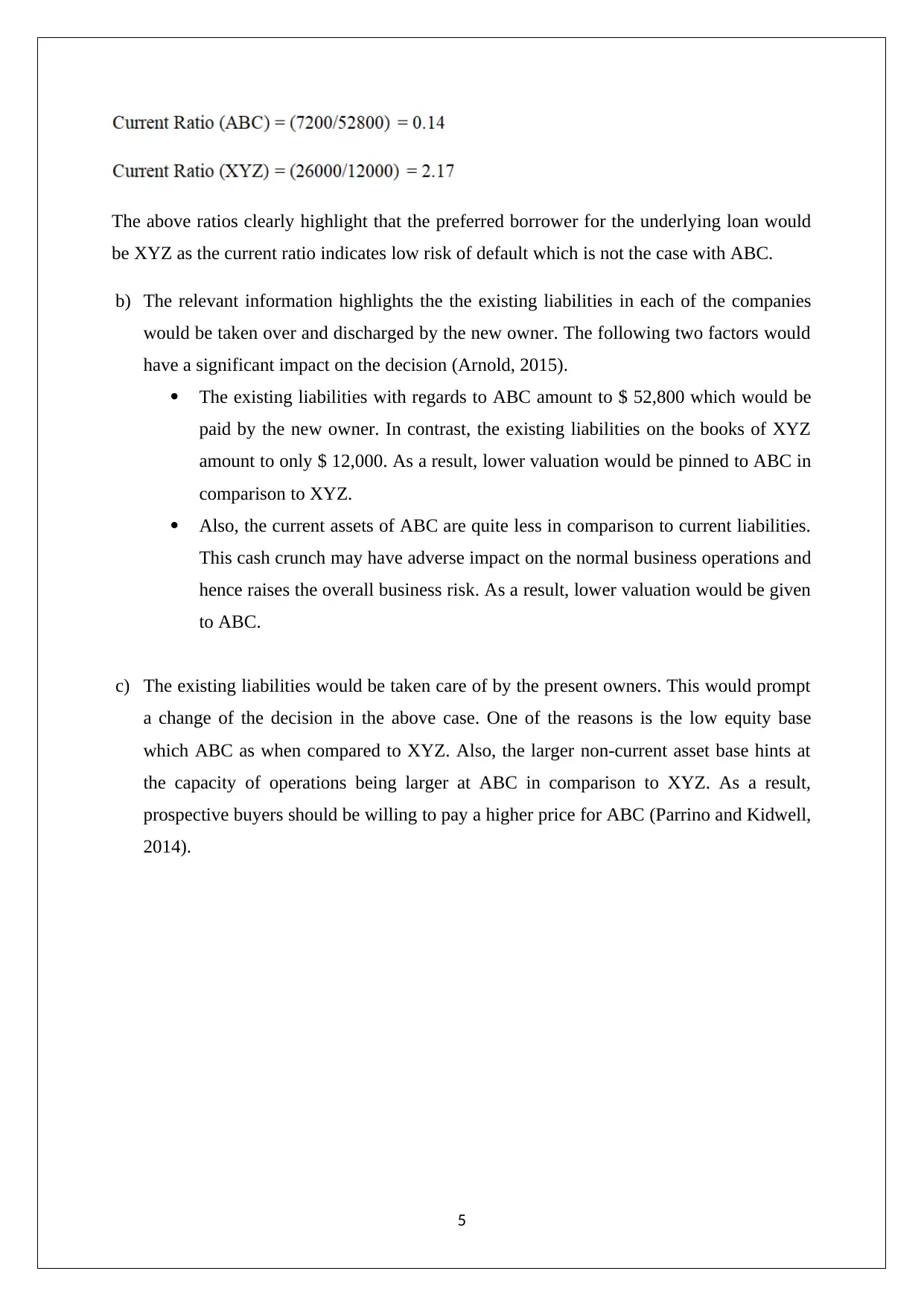

This assignment provides a comprehensive analysis of financial statements, focusing on key accounting ratios and their implications. Part A delves into the calculation and interpretation of current ratio, quick ratio, accounts receivable turnover, and inventory turnover, examining their trends and significance for short-term liquidity and efficiency. Part B defines income and revenue, differentiating between the two and applying these concepts to specific financial items of a software company, clarifying which transactions constitute revenue. Part C presents a case study involving a short-term loan, comparing the financial health of two potential borrowers, XYZ and ABC, based on current ratios and other financial considerations, including the impact of liabilities and asset bases on loan decisions. The assignment incorporates relevant accounting standards and references to support its analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.