Financial Ratios and Business Valuation: Accounting for Business

VerifiedAdded on 2022/11/26

|7

|2010

|403

Homework Assignment

AI Summary

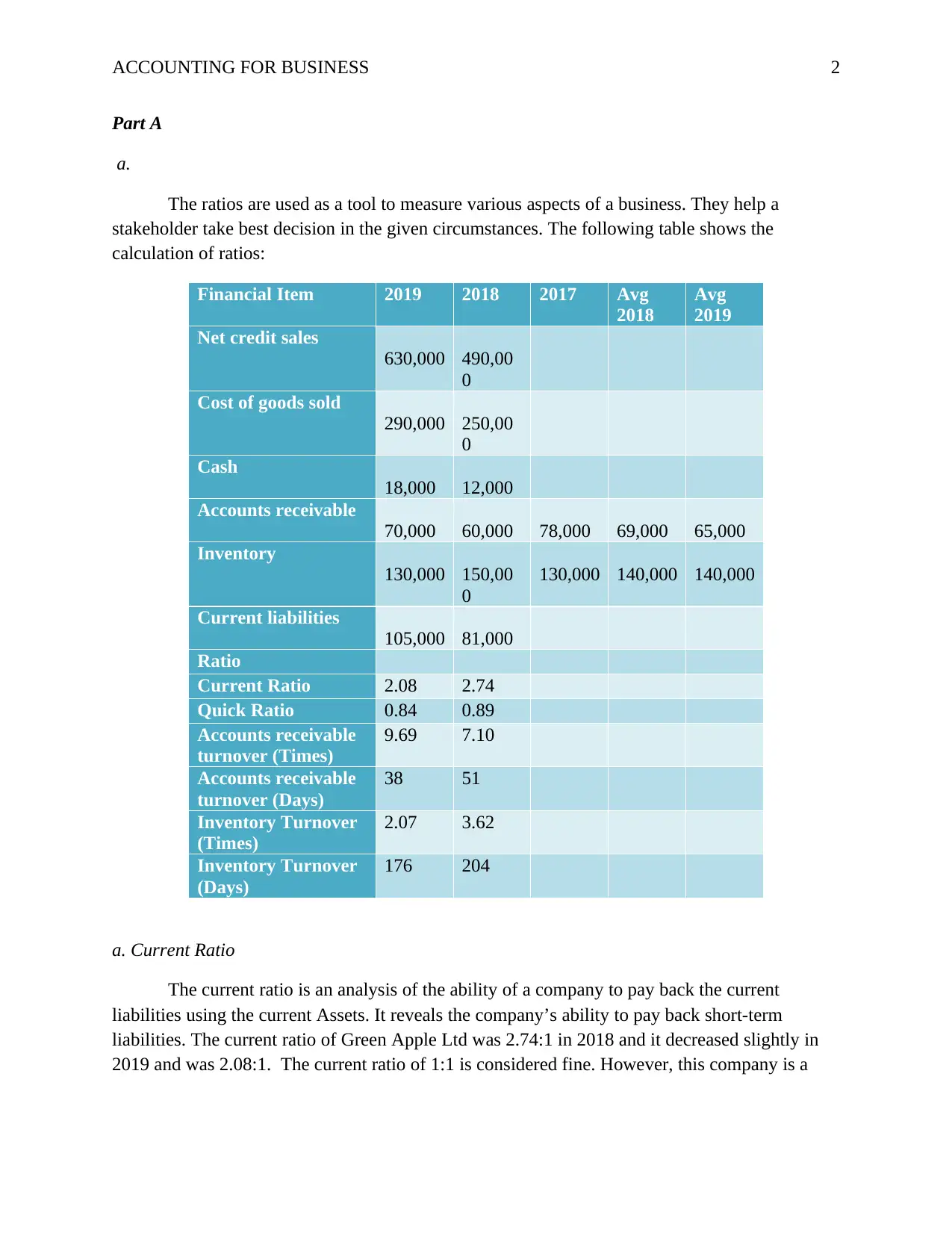

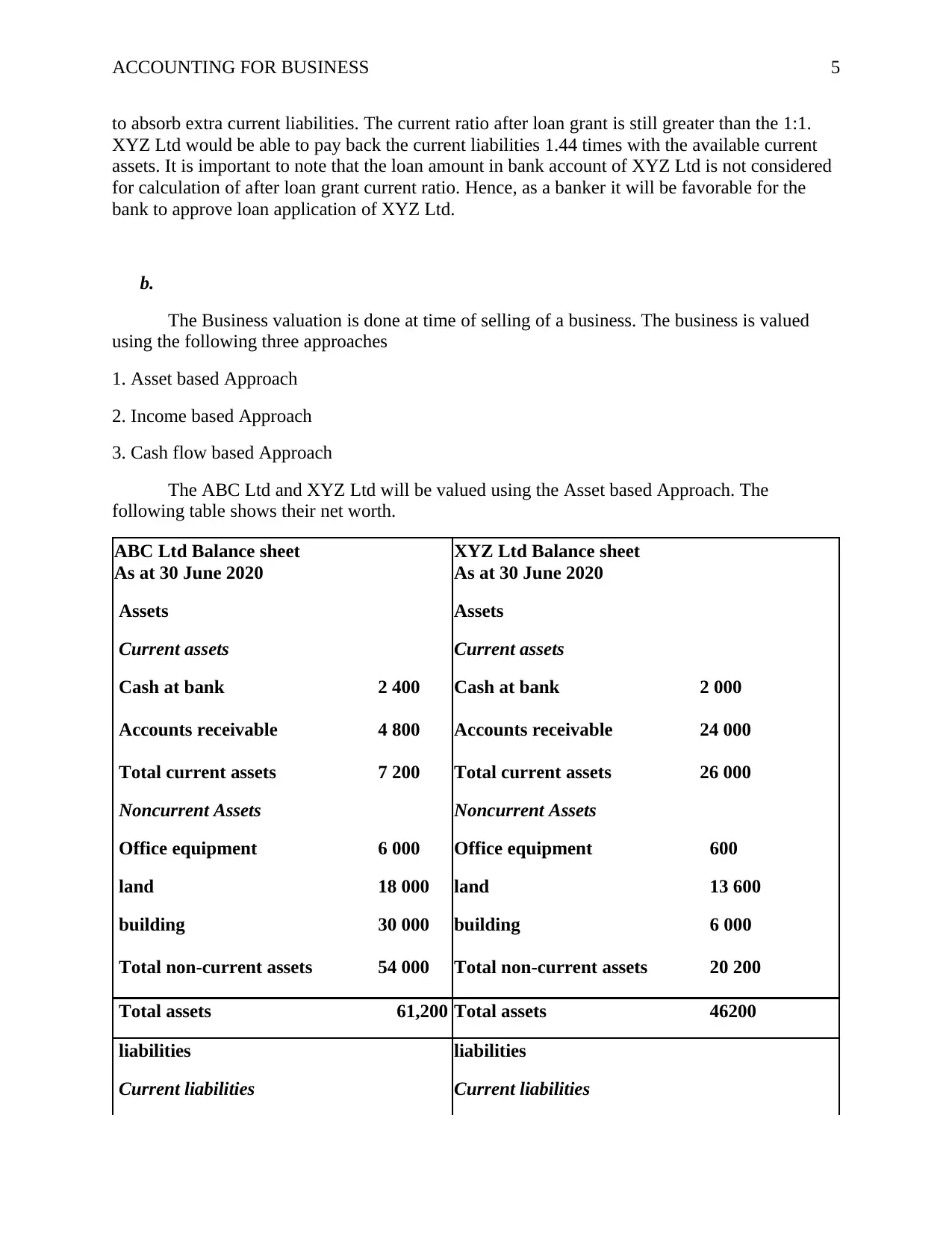

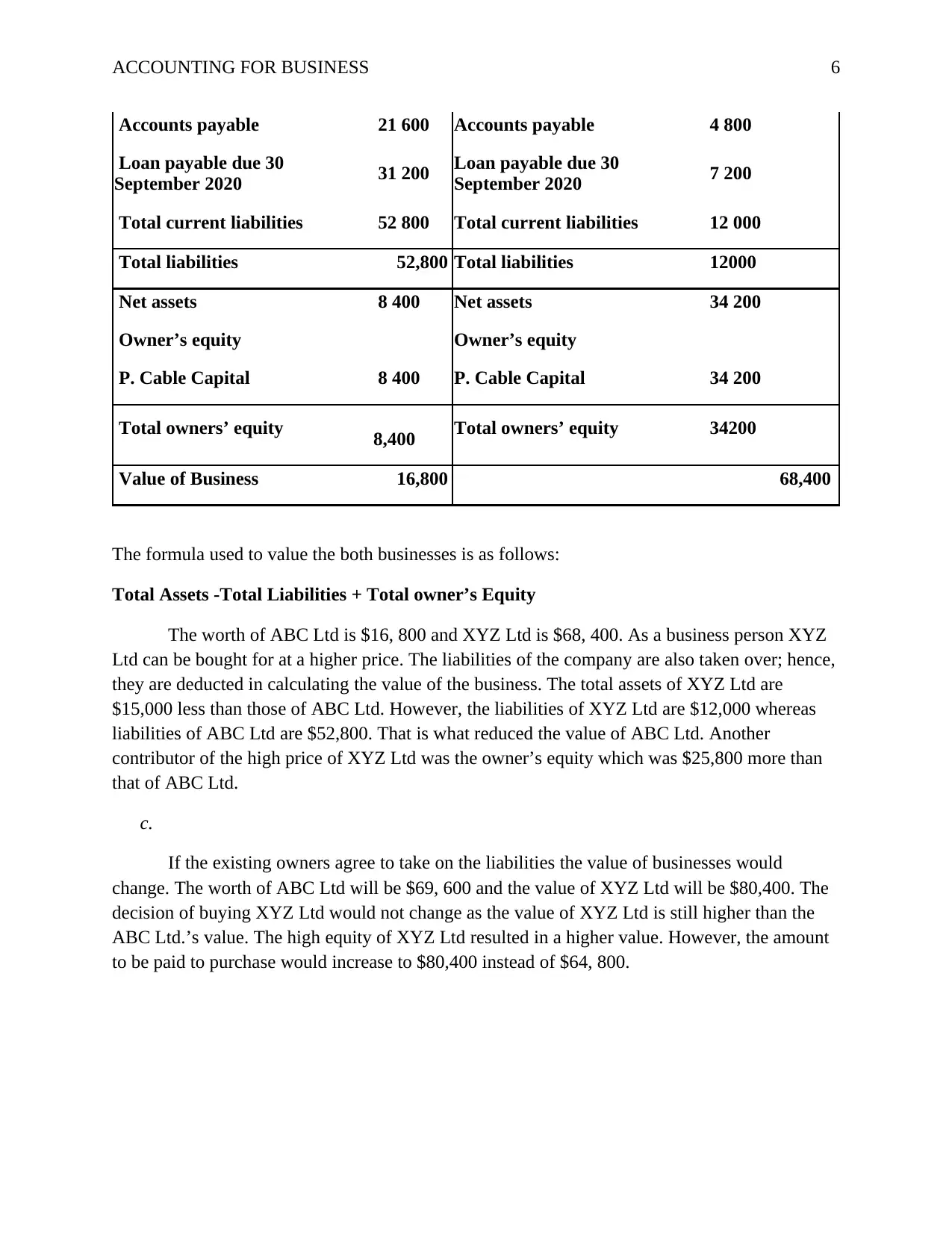

This assignment delves into the core concepts of accounting for business, focusing on financial statement analysis and business valuation. Part A involves a comprehensive examination of financial ratios, including current ratio, quick ratio, accounts receivable turnover, and inventory turnover, using provided financial data from 2017 to 2019. It assesses the short-term solvency and efficiency of a business. Part B focuses on identifying and classifying revenue and income items based on their definitions. Part C applies accounting knowledge to real-world scenarios, evaluating the liquidity of two companies for loan approval and valuing businesses using the asset-based approach. The assignment utilizes financial statements, balance sheets, and ratio calculations to provide insights into the financial health and performance of the companies involved, along with references to academic sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.