HI5001: Accounting for Business Decisions - Tutorial Questions

VerifiedAdded on 2023/01/10

|12

|2457

|75

Homework Assignment

AI Summary

This assignment delves into key aspects of accounting for business decisions, addressing various tutorial questions. It begins by outlining the process of recording transactions in different accounting books and journals, covering topics like purchases, sales, and payments. The solution includes calculations for cash receipts and payments, along with the preparation of cash at bank ledger accounts and bank reconciliation statements. Furthermore, the assignment explores journal entries, particularly for sales, discounts, and uncollectible accounts, along with their reflection in the balance sheet. The assignment then presents inventory valuation using the FIFO method, accompanied by an income statement analysis. Finally, it demonstrates the calculation of depreciation using straight-line, diminishing balance, and units of production methods, including journal entries and balance sheet presentation for the diminishing balance method. The report concludes by summarizing the importance of accurate accounting for informed business decisions.

Accounting for

business decisions

business decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Week 6.........................................................................................................................................1

Week 7.........................................................................................................................................2

Week 8.........................................................................................................................................4

Week 9.........................................................................................................................................5

Week 10.......................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Week 6.........................................................................................................................................1

Week 7.........................................................................................................................................2

Week 8.........................................................................................................................................4

Week 9.........................................................................................................................................5

Week 10.......................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Accounting can be defined as the process of recording information of business

transactions in different books so that it could be determined that all the operations are carried

out systematically or not. while planning to reach the long-term business goals it is very

important for all the companies to make sure that they are able to formulate effective decisions

related to accounting (Carenys and Moya, 2016). If the professional who are responsible to

generate records of the company are not having proper knowledge of accounting then it will be

very difficult for them to generate accurate records. Therefore, it is very important for all the

accounting professional to have proper knowledge of it so that effective decisions for business

could be taken. Present report is based upon, analysis of various aspects of accounting such as

depreciation, cash book, journals, income statement etc. Different topics that are covered in this

assignment are details regarding the accounts in which transactions are recorded, calculation of

dep, reflection of different elements in balance sheet as well as income statement etc.

MAIN BODY

Week 6

There are various types of accounts and books that are generated by business entities for

the purpose of recording details regarding accounting transactions. Some of the specific

transactions along with the accounts or books in which they will be recorded are discussed

below:

Purchased inventories on credit: When Fiona Sporty will buy inventory on credit then

it will be recorded in purchase journal and general journal so that when the amount of it

will be paid then balance total could be matched (Christ and Burritt, 2017).

Sales of inventory on credit: If Fiona Sporty will sale the inventory on credit then it will

be recorded in two journals. First one is sales journal and another one is general journal

as it is required to recorded each transaction in two accounts to maintain accuracy.

Received payment of a customer’s account: While receiving payment from a

customer’s account then its value will be recorded in the cash receipt journals and the

journals which s specifically made for the customer. Apart form this it will also be

recorded in the general journals to close the account which was made at the time of credit

sales.

1

Accounting can be defined as the process of recording information of business

transactions in different books so that it could be determined that all the operations are carried

out systematically or not. while planning to reach the long-term business goals it is very

important for all the companies to make sure that they are able to formulate effective decisions

related to accounting (Carenys and Moya, 2016). If the professional who are responsible to

generate records of the company are not having proper knowledge of accounting then it will be

very difficult for them to generate accurate records. Therefore, it is very important for all the

accounting professional to have proper knowledge of it so that effective decisions for business

could be taken. Present report is based upon, analysis of various aspects of accounting such as

depreciation, cash book, journals, income statement etc. Different topics that are covered in this

assignment are details regarding the accounts in which transactions are recorded, calculation of

dep, reflection of different elements in balance sheet as well as income statement etc.

MAIN BODY

Week 6

There are various types of accounts and books that are generated by business entities for

the purpose of recording details regarding accounting transactions. Some of the specific

transactions along with the accounts or books in which they will be recorded are discussed

below:

Purchased inventories on credit: When Fiona Sporty will buy inventory on credit then

it will be recorded in purchase journal and general journal so that when the amount of it

will be paid then balance total could be matched (Christ and Burritt, 2017).

Sales of inventory on credit: If Fiona Sporty will sale the inventory on credit then it will

be recorded in two journals. First one is sales journal and another one is general journal

as it is required to recorded each transaction in two accounts to maintain accuracy.

Received payment of a customer’s account: While receiving payment from a

customer’s account then its value will be recorded in the cash receipt journals and the

journals which s specifically made for the customer. Apart form this it will also be

recorded in the general journals to close the account which was made at the time of credit

sales.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

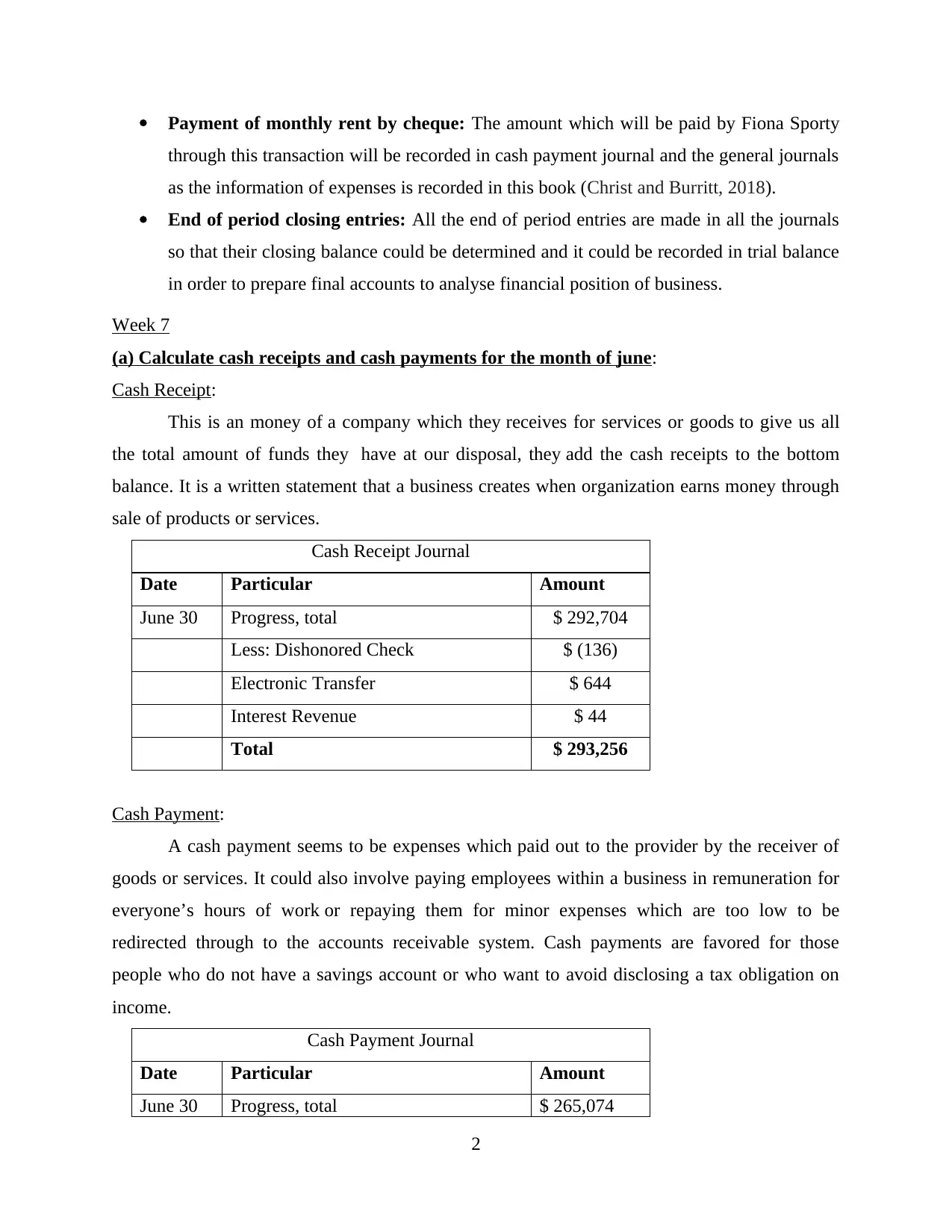

Payment of monthly rent by cheque: The amount which will be paid by Fiona Sporty

through this transaction will be recorded in cash payment journal and the general journals

as the information of expenses is recorded in this book (Christ and Burritt, 2018).

End of period closing entries: All the end of period entries are made in all the journals

so that their closing balance could be determined and it could be recorded in trial balance

in order to prepare final accounts to analyse financial position of business.

Week 7

(a) Calculate cash receipts and cash payments for the month of june:

Cash Receipt:

This is an money of a company which they receives for services or goods to give us all

the total amount of funds they have at our disposal, they add the cash receipts to the bottom

balance. It is a written statement that a business creates when organization earns money through

sale of products or services.

Cash Receipt Journal

Date Particular Amount

June 30 Progress, total $ 292,704

Less: Dishonored Check $ (136)

Electronic Transfer $ 644

Interest Revenue $ 44

Total $ 293,256

Cash Payment:

A cash payment seems to be expenses which paid out to the provider by the receiver of

goods or services. It could also involve paying employees within a business in remuneration for

everyone’s hours of work or repaying them for minor expenses which are too low to be

redirected through to the accounts receivable system. Cash payments are favored for those

people who do not have a savings account or who want to avoid disclosing a tax obligation on

income.

Cash Payment Journal

Date Particular Amount

June 30 Progress, total $ 265,074

2

through this transaction will be recorded in cash payment journal and the general journals

as the information of expenses is recorded in this book (Christ and Burritt, 2018).

End of period closing entries: All the end of period entries are made in all the journals

so that their closing balance could be determined and it could be recorded in trial balance

in order to prepare final accounts to analyse financial position of business.

Week 7

(a) Calculate cash receipts and cash payments for the month of june:

Cash Receipt:

This is an money of a company which they receives for services or goods to give us all

the total amount of funds they have at our disposal, they add the cash receipts to the bottom

balance. It is a written statement that a business creates when organization earns money through

sale of products or services.

Cash Receipt Journal

Date Particular Amount

June 30 Progress, total $ 292,704

Less: Dishonored Check $ (136)

Electronic Transfer $ 644

Interest Revenue $ 44

Total $ 293,256

Cash Payment:

A cash payment seems to be expenses which paid out to the provider by the receiver of

goods or services. It could also involve paying employees within a business in remuneration for

everyone’s hours of work or repaying them for minor expenses which are too low to be

redirected through to the accounts receivable system. Cash payments are favored for those

people who do not have a savings account or who want to avoid disclosing a tax obligation on

income.

Cash Payment Journal

Date Particular Amount

June 30 Progress, total $ 265,074

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

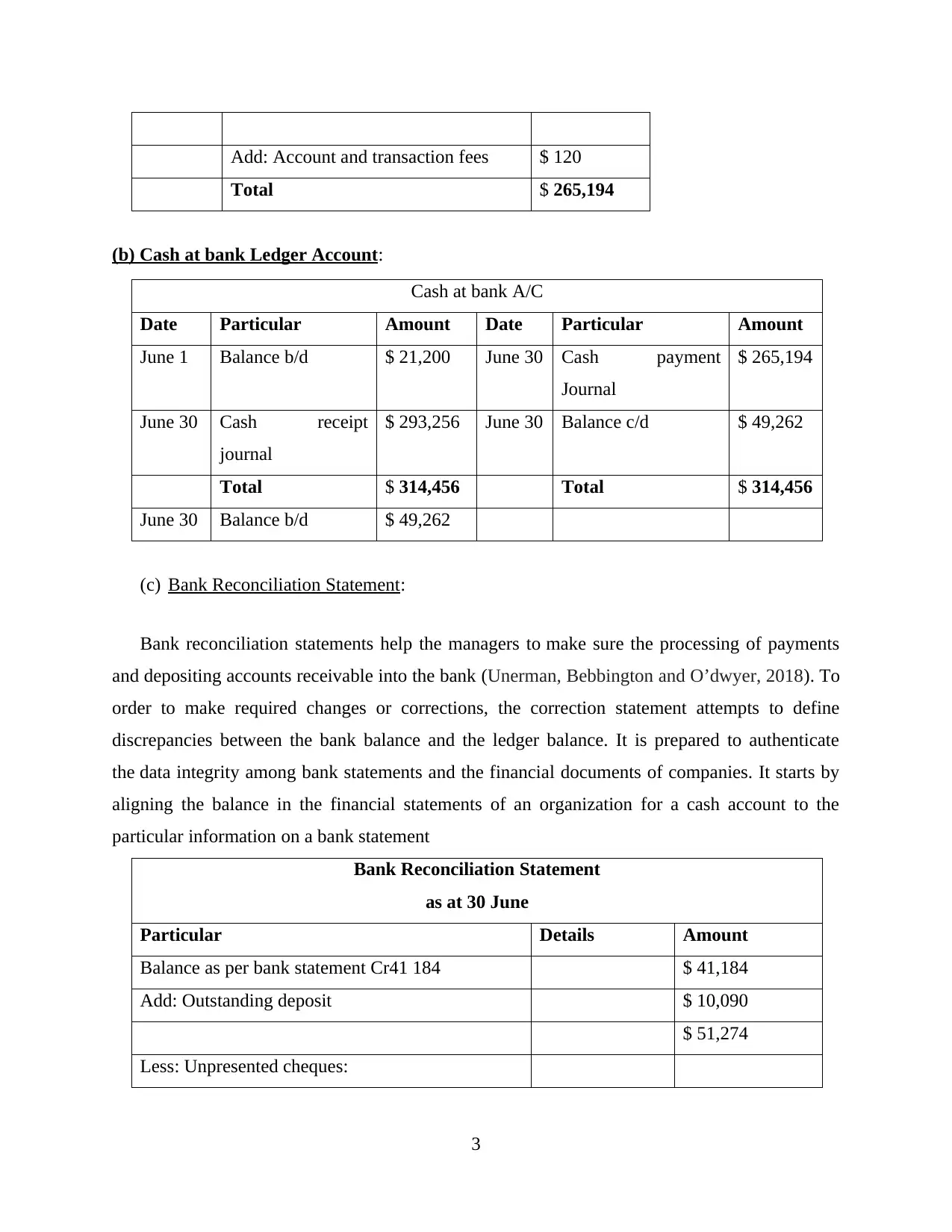

Add: Account and transaction fees $ 120

Total $ 265,194

(b) Cash at bank Ledger Account:

Cash at bank A/C

Date Particular Amount Date Particular Amount

June 1 Balance b/d $ 21,200 June 30 Cash payment

Journal

$ 265,194

June 30 Cash receipt

journal

$ 293,256 June 30 Balance c/d $ 49,262

Total $ 314,456 Total $ 314,456

June 30 Balance b/d $ 49,262

(c) Bank Reconciliation Statement:

Bank reconciliation statements help the managers to make sure the processing of payments

and depositing accounts receivable into the bank (Unerman, Bebbington and O’dwyer, 2018). To

order to make required changes or corrections, the correction statement attempts to define

discrepancies between the bank balance and the ledger balance. It is prepared to authenticate

the data integrity among bank statements and the financial documents of companies. It starts by

aligning the balance in the financial statements of an organization for a cash account to the

particular information on a bank statement

Bank Reconciliation Statement

as at 30 June

Particular Details Amount

Balance as per bank statement Cr41 184 $ 41,184

Add: Outstanding deposit $ 10,090

$ 51,274

Less: Unpresented cheques:

3

Total $ 265,194

(b) Cash at bank Ledger Account:

Cash at bank A/C

Date Particular Amount Date Particular Amount

June 1 Balance b/d $ 21,200 June 30 Cash payment

Journal

$ 265,194

June 30 Cash receipt

journal

$ 293,256 June 30 Balance c/d $ 49,262

Total $ 314,456 Total $ 314,456

June 30 Balance b/d $ 49,262

(c) Bank Reconciliation Statement:

Bank reconciliation statements help the managers to make sure the processing of payments

and depositing accounts receivable into the bank (Unerman, Bebbington and O’dwyer, 2018). To

order to make required changes or corrections, the correction statement attempts to define

discrepancies between the bank balance and the ledger balance. It is prepared to authenticate

the data integrity among bank statements and the financial documents of companies. It starts by

aligning the balance in the financial statements of an organization for a cash account to the

particular information on a bank statement

Bank Reconciliation Statement

as at 30 June

Particular Details Amount

Balance as per bank statement Cr41 184 $ 41,184

Add: Outstanding deposit $ 10,090

$ 51,274

Less: Unpresented cheques:

3

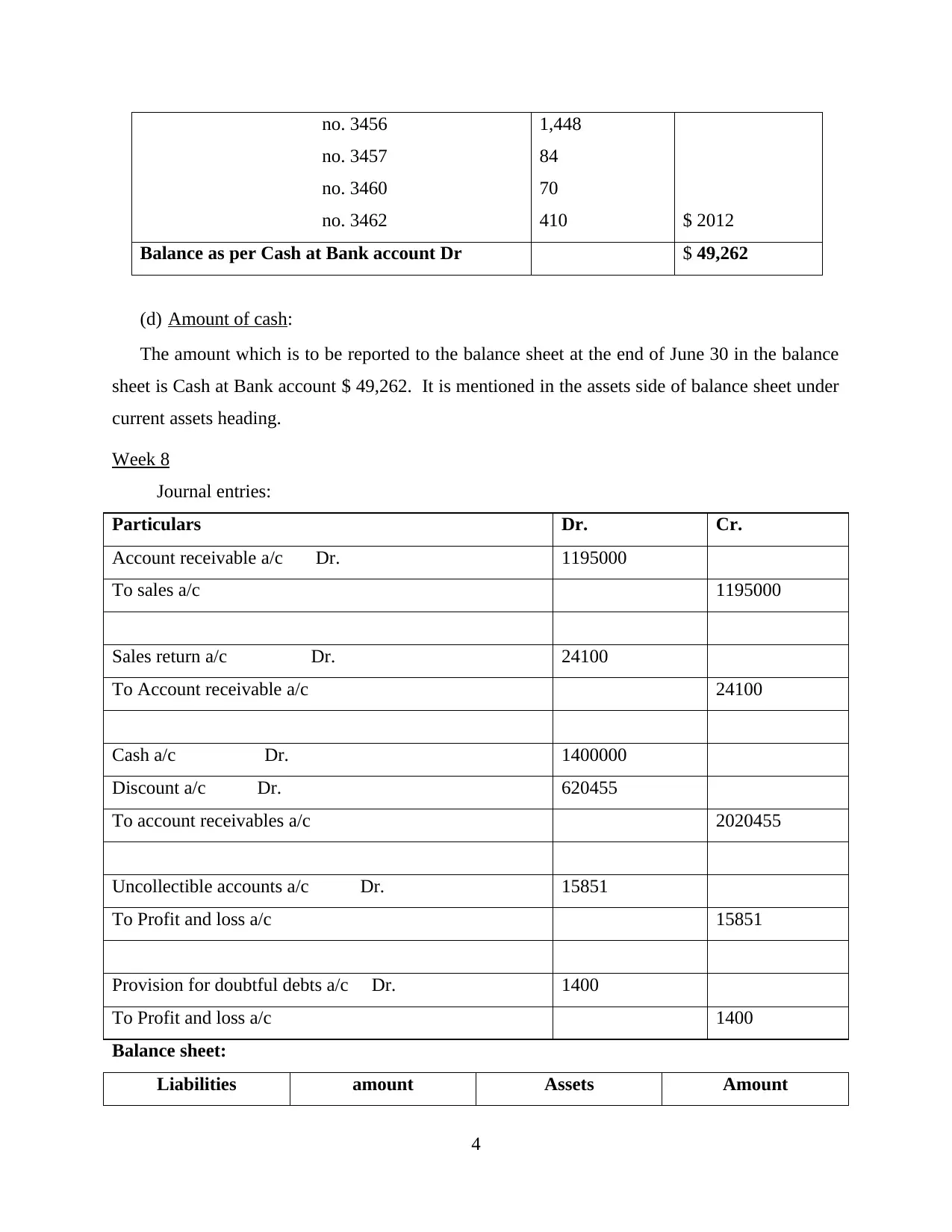

no. 3456

no. 3457

no. 3460

no. 3462

1,448

84

70

410 $ 2012

Balance as per Cash at Bank account Dr $ 49,262

(d) Amount of cash:

The amount which is to be reported to the balance sheet at the end of June 30 in the balance

sheet is Cash at Bank account $ 49,262. It is mentioned in the assets side of balance sheet under

current assets heading.

Week 8

Journal entries:

Particulars Dr. Cr.

Account receivable a/c Dr. 1195000

To sales a/c 1195000

Sales return a/c Dr. 24100

To Account receivable a/c 24100

Cash a/c Dr. 1400000

Discount a/c Dr. 620455

To account receivables a/c 2020455

Uncollectible accounts a/c Dr. 15851

To Profit and loss a/c 15851

Provision for doubtful debts a/c Dr. 1400

To Profit and loss a/c 1400

Balance sheet:

Liabilities amount Assets Amount

4

no. 3457

no. 3460

no. 3462

1,448

84

70

410 $ 2012

Balance as per Cash at Bank account Dr $ 49,262

(d) Amount of cash:

The amount which is to be reported to the balance sheet at the end of June 30 in the balance

sheet is Cash at Bank account $ 49,262. It is mentioned in the assets side of balance sheet under

current assets heading.

Week 8

Journal entries:

Particulars Dr. Cr.

Account receivable a/c Dr. 1195000

To sales a/c 1195000

Sales return a/c Dr. 24100

To Account receivable a/c 24100

Cash a/c Dr. 1400000

Discount a/c Dr. 620455

To account receivables a/c 2020455

Uncollectible accounts a/c Dr. 15851

To Profit and loss a/c 15851

Provision for doubtful debts a/c Dr. 1400

To Profit and loss a/c 1400

Balance sheet:

Liabilities amount Assets Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current liabilities: Current assets:

Provision for doubtful

debts

13500 Account receivables 2020455

Journal entry:

Particulars Dr. Cr.

Uncollectible receivables a/c Dr. 2400

To Kim Ltd a/c 2400

Cash a/c Dr. 2400

To uncollectible receivables recovered a/c 2400

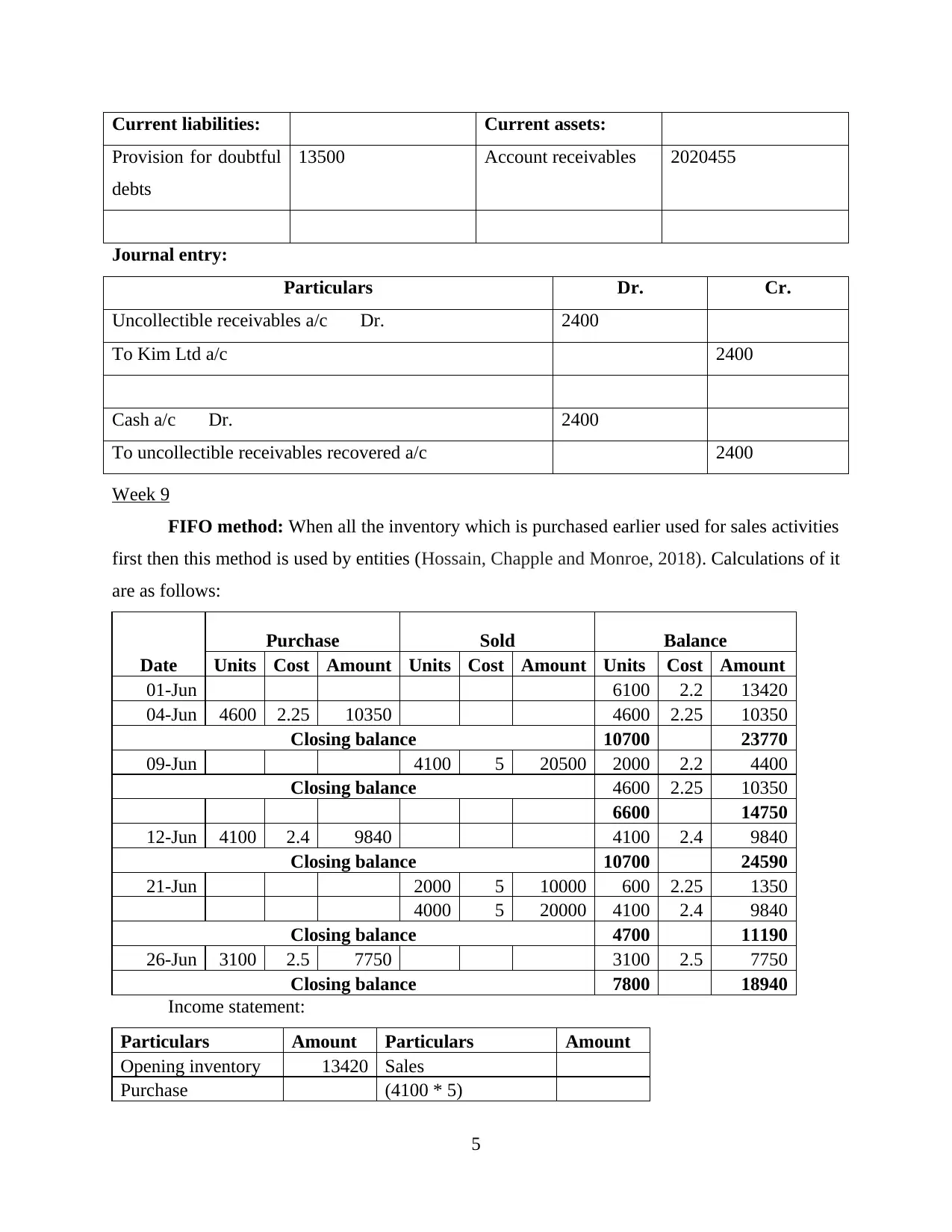

Week 9

FIFO method: When all the inventory which is purchased earlier used for sales activities

first then this method is used by entities (Hossain, Chapple and Monroe, 2018). Calculations of it

are as follows:

Date

Purchase Sold Balance

Units Cost Amount Units Cost Amount Units Cost Amount

01-Jun 6100 2.2 13420

04-Jun 4600 2.25 10350 4600 2.25 10350

Closing balance 10700 23770

09-Jun 4100 5 20500 2000 2.2 4400

Closing balance 4600 2.25 10350

6600 14750

12-Jun 4100 2.4 9840 4100 2.4 9840

Closing balance 10700 24590

21-Jun 2000 5 10000 600 2.25 1350

4000 5 20000 4100 2.4 9840

Closing balance 4700 11190

26-Jun 3100 2.5 7750 3100 2.5 7750

Closing balance 7800 18940

Income statement:

Particulars Amount Particulars Amount

Opening inventory 13420 Sales

Purchase (4100 * 5)

5

Provision for doubtful

debts

13500 Account receivables 2020455

Journal entry:

Particulars Dr. Cr.

Uncollectible receivables a/c Dr. 2400

To Kim Ltd a/c 2400

Cash a/c Dr. 2400

To uncollectible receivables recovered a/c 2400

Week 9

FIFO method: When all the inventory which is purchased earlier used for sales activities

first then this method is used by entities (Hossain, Chapple and Monroe, 2018). Calculations of it

are as follows:

Date

Purchase Sold Balance

Units Cost Amount Units Cost Amount Units Cost Amount

01-Jun 6100 2.2 13420

04-Jun 4600 2.25 10350 4600 2.25 10350

Closing balance 10700 23770

09-Jun 4100 5 20500 2000 2.2 4400

Closing balance 4600 2.25 10350

6600 14750

12-Jun 4100 2.4 9840 4100 2.4 9840

Closing balance 10700 24590

21-Jun 2000 5 10000 600 2.25 1350

4000 5 20000 4100 2.4 9840

Closing balance 4700 11190

26-Jun 3100 2.5 7750 3100 2.5 7750

Closing balance 7800 18940

Income statement:

Particulars Amount Particulars Amount

Opening inventory 13420 Sales

Purchase (4100 * 5)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

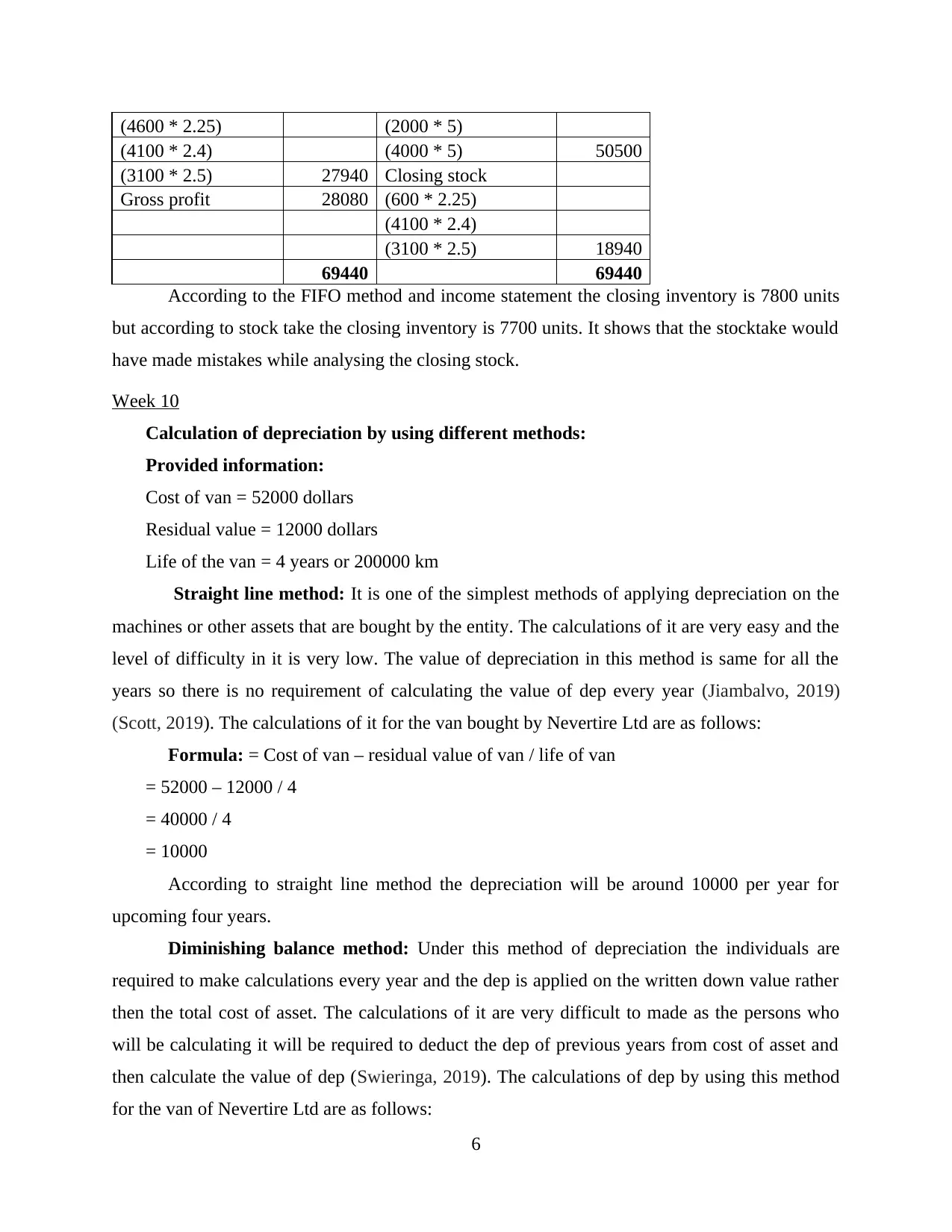

(4600 * 2.25) (2000 * 5)

(4100 * 2.4) (4000 * 5) 50500

(3100 * 2.5) 27940 Closing stock

Gross profit 28080 (600 * 2.25)

(4100 * 2.4)

(3100 * 2.5) 18940

69440 69440

According to the FIFO method and income statement the closing inventory is 7800 units

but according to stock take the closing inventory is 7700 units. It shows that the stocktake would

have made mistakes while analysing the closing stock.

Week 10

Calculation of depreciation by using different methods:

Provided information:

Cost of van = 52000 dollars

Residual value = 12000 dollars

Life of the van = 4 years or 200000 km

Straight line method: It is one of the simplest methods of applying depreciation on the

machines or other assets that are bought by the entity. The calculations of it are very easy and the

level of difficulty in it is very low. The value of depreciation in this method is same for all the

years so there is no requirement of calculating the value of dep every year (Jiambalvo, 2019)

(Scott, 2019). The calculations of it for the van bought by Nevertire Ltd are as follows:

Formula: = Cost of van – residual value of van / life of van

= 52000 – 12000 / 4

= 40000 / 4

= 10000

According to straight line method the depreciation will be around 10000 per year for

upcoming four years.

Diminishing balance method: Under this method of depreciation the individuals are

required to make calculations every year and the dep is applied on the written down value rather

then the total cost of asset. The calculations of it are very difficult to made as the persons who

will be calculating it will be required to deduct the dep of previous years from cost of asset and

then calculate the value of dep (Swieringa, 2019). The calculations of dep by using this method

for the van of Nevertire Ltd are as follows:

6

(4100 * 2.4) (4000 * 5) 50500

(3100 * 2.5) 27940 Closing stock

Gross profit 28080 (600 * 2.25)

(4100 * 2.4)

(3100 * 2.5) 18940

69440 69440

According to the FIFO method and income statement the closing inventory is 7800 units

but according to stock take the closing inventory is 7700 units. It shows that the stocktake would

have made mistakes while analysing the closing stock.

Week 10

Calculation of depreciation by using different methods:

Provided information:

Cost of van = 52000 dollars

Residual value = 12000 dollars

Life of the van = 4 years or 200000 km

Straight line method: It is one of the simplest methods of applying depreciation on the

machines or other assets that are bought by the entity. The calculations of it are very easy and the

level of difficulty in it is very low. The value of depreciation in this method is same for all the

years so there is no requirement of calculating the value of dep every year (Jiambalvo, 2019)

(Scott, 2019). The calculations of it for the van bought by Nevertire Ltd are as follows:

Formula: = Cost of van – residual value of van / life of van

= 52000 – 12000 / 4

= 40000 / 4

= 10000

According to straight line method the depreciation will be around 10000 per year for

upcoming four years.

Diminishing balance method: Under this method of depreciation the individuals are

required to make calculations every year and the dep is applied on the written down value rather

then the total cost of asset. The calculations of it are very difficult to made as the persons who

will be calculating it will be required to deduct the dep of previous years from cost of asset and

then calculate the value of dep (Swieringa, 2019). The calculations of dep by using this method

for the van of Nevertire Ltd are as follows:

6

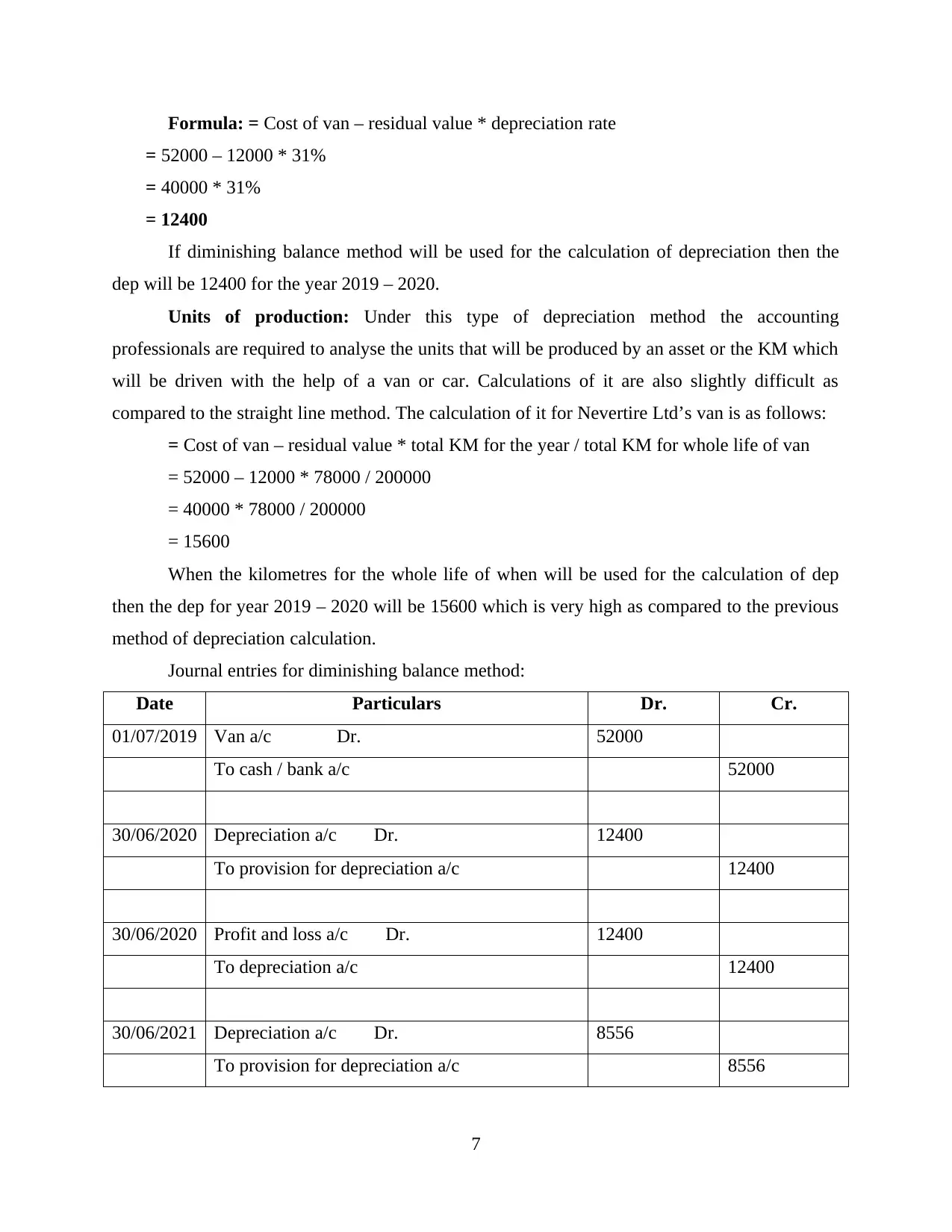

Formula: = Cost of van – residual value * depreciation rate

= 52000 – 12000 * 31%

= 40000 * 31%

= 12400

If diminishing balance method will be used for the calculation of depreciation then the

dep will be 12400 for the year 2019 – 2020.

Units of production: Under this type of depreciation method the accounting

professionals are required to analyse the units that will be produced by an asset or the KM which

will be driven with the help of a van or car. Calculations of it are also slightly difficult as

compared to the straight line method. The calculation of it for Nevertire Ltd’s van is as follows:

= Cost of van – residual value * total KM for the year / total KM for whole life of van

= 52000 – 12000 * 78000 / 200000

= 40000 * 78000 / 200000

= 15600

When the kilometres for the whole life of when will be used for the calculation of dep

then the dep for year 2019 – 2020 will be 15600 which is very high as compared to the previous

method of depreciation calculation.

Journal entries for diminishing balance method:

Date Particulars Dr. Cr.

01/07/2019 Van a/c Dr. 52000

To cash / bank a/c 52000

30/06/2020 Depreciation a/c Dr. 12400

To provision for depreciation a/c 12400

30/06/2020 Profit and loss a/c Dr. 12400

To depreciation a/c 12400

30/06/2021 Depreciation a/c Dr. 8556

To provision for depreciation a/c 8556

7

= 52000 – 12000 * 31%

= 40000 * 31%

= 12400

If diminishing balance method will be used for the calculation of depreciation then the

dep will be 12400 for the year 2019 – 2020.

Units of production: Under this type of depreciation method the accounting

professionals are required to analyse the units that will be produced by an asset or the KM which

will be driven with the help of a van or car. Calculations of it are also slightly difficult as

compared to the straight line method. The calculation of it for Nevertire Ltd’s van is as follows:

= Cost of van – residual value * total KM for the year / total KM for whole life of van

= 52000 – 12000 * 78000 / 200000

= 40000 * 78000 / 200000

= 15600

When the kilometres for the whole life of when will be used for the calculation of dep

then the dep for year 2019 – 2020 will be 15600 which is very high as compared to the previous

method of depreciation calculation.

Journal entries for diminishing balance method:

Date Particulars Dr. Cr.

01/07/2019 Van a/c Dr. 52000

To cash / bank a/c 52000

30/06/2020 Depreciation a/c Dr. 12400

To provision for depreciation a/c 12400

30/06/2020 Profit and loss a/c Dr. 12400

To depreciation a/c 12400

30/06/2021 Depreciation a/c Dr. 8556

To provision for depreciation a/c 8556

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

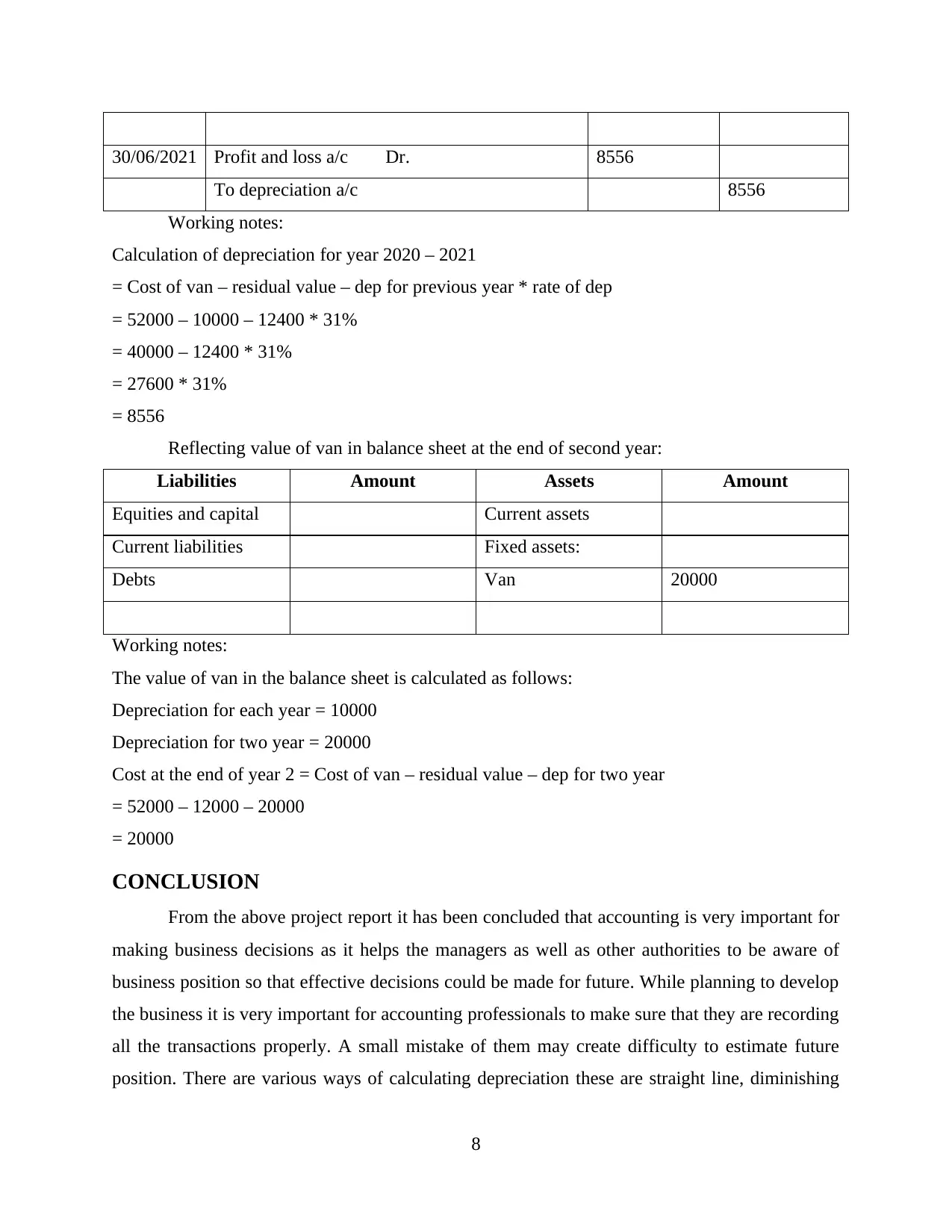

30/06/2021 Profit and loss a/c Dr. 8556

To depreciation a/c 8556

Working notes:

Calculation of depreciation for year 2020 – 2021

= Cost of van – residual value – dep for previous year * rate of dep

= 52000 – 10000 – 12400 * 31%

= 40000 – 12400 * 31%

= 27600 * 31%

= 8556

Reflecting value of van in balance sheet at the end of second year:

Liabilities Amount Assets Amount

Equities and capital Current assets

Current liabilities Fixed assets:

Debts Van 20000

Working notes:

The value of van in the balance sheet is calculated as follows:

Depreciation for each year = 10000

Depreciation for two year = 20000

Cost at the end of year 2 = Cost of van – residual value – dep for two year

= 52000 – 12000 – 20000

= 20000

CONCLUSION

From the above project report it has been concluded that accounting is very important for

making business decisions as it helps the managers as well as other authorities to be aware of

business position so that effective decisions could be made for future. While planning to develop

the business it is very important for accounting professionals to make sure that they are recording

all the transactions properly. A small mistake of them may create difficulty to estimate future

position. There are various ways of calculating depreciation these are straight line, diminishing

8

To depreciation a/c 8556

Working notes:

Calculation of depreciation for year 2020 – 2021

= Cost of van – residual value – dep for previous year * rate of dep

= 52000 – 10000 – 12400 * 31%

= 40000 – 12400 * 31%

= 27600 * 31%

= 8556

Reflecting value of van in balance sheet at the end of second year:

Liabilities Amount Assets Amount

Equities and capital Current assets

Current liabilities Fixed assets:

Debts Van 20000

Working notes:

The value of van in the balance sheet is calculated as follows:

Depreciation for each year = 10000

Depreciation for two year = 20000

Cost at the end of year 2 = Cost of van – residual value – dep for two year

= 52000 – 12000 – 20000

= 20000

CONCLUSION

From the above project report it has been concluded that accounting is very important for

making business decisions as it helps the managers as well as other authorities to be aware of

business position so that effective decisions could be made for future. While planning to develop

the business it is very important for accounting professionals to make sure that they are recording

all the transactions properly. A small mistake of them may create difficulty to estimate future

position. There are various ways of calculating depreciation these are straight line, diminishing

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

balance and units of production method. Any one of them could be used by entities according to

their choice. In order to record the details of stock transactions different methods such as LIFO,

FIFO, Average cost method etc. could be used.

9

their choice. In order to record the details of stock transactions different methods such as LIFO,

FIFO, Average cost method etc. could be used.

9

REFERENCES

Books and journals:

Carenys, J. and Moya, S., 2016. Digital game-based learning in accounting and business

education. Accounting Education. 25(6). pp.598-651.

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for corporate

practice. Journal of Cleaner Production. 152. pp.379-386.

Christ, K. L. and Burritt, R. L., 2018. The role for transdisciplinarity in water accounting by

business: reflections and opportunities. Australasian Journal of Environmental

Management. 25(3). pp.302-320.

Hossain, S., Chapple, L. and Monroe, G. S., 2018. Does auditor gender affect issuing going‐

concern decisions for financially distressed clients?. Accounting & Finance. 58(4).

pp.1027-1061.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Scott, P., 2019. Accounting for business. Oxford University Press, USA.

Swieringa, R. J., 2019. Building connections between accounting research and

practice. Accounting Horizons. 33(2). pp.3-10.

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and business research. 48(5). pp.497-522.

10

Books and journals:

Carenys, J. and Moya, S., 2016. Digital game-based learning in accounting and business

education. Accounting Education. 25(6). pp.598-651.

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for corporate

practice. Journal of Cleaner Production. 152. pp.379-386.

Christ, K. L. and Burritt, R. L., 2018. The role for transdisciplinarity in water accounting by

business: reflections and opportunities. Australasian Journal of Environmental

Management. 25(3). pp.302-320.

Hossain, S., Chapple, L. and Monroe, G. S., 2018. Does auditor gender affect issuing going‐

concern decisions for financially distressed clients?. Accounting & Finance. 58(4).

pp.1027-1061.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Scott, P., 2019. Accounting for business. Oxford University Press, USA.

Swieringa, R. J., 2019. Building connections between accounting research and

practice. Accounting Horizons. 33(2). pp.3-10.

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and business research. 48(5). pp.497-522.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.