Accounting for Business Exam: Financial Analysis and Budgeting

VerifiedAdded on 2023/06/18

|5

|998

|246

Homework Assignment

AI Summary

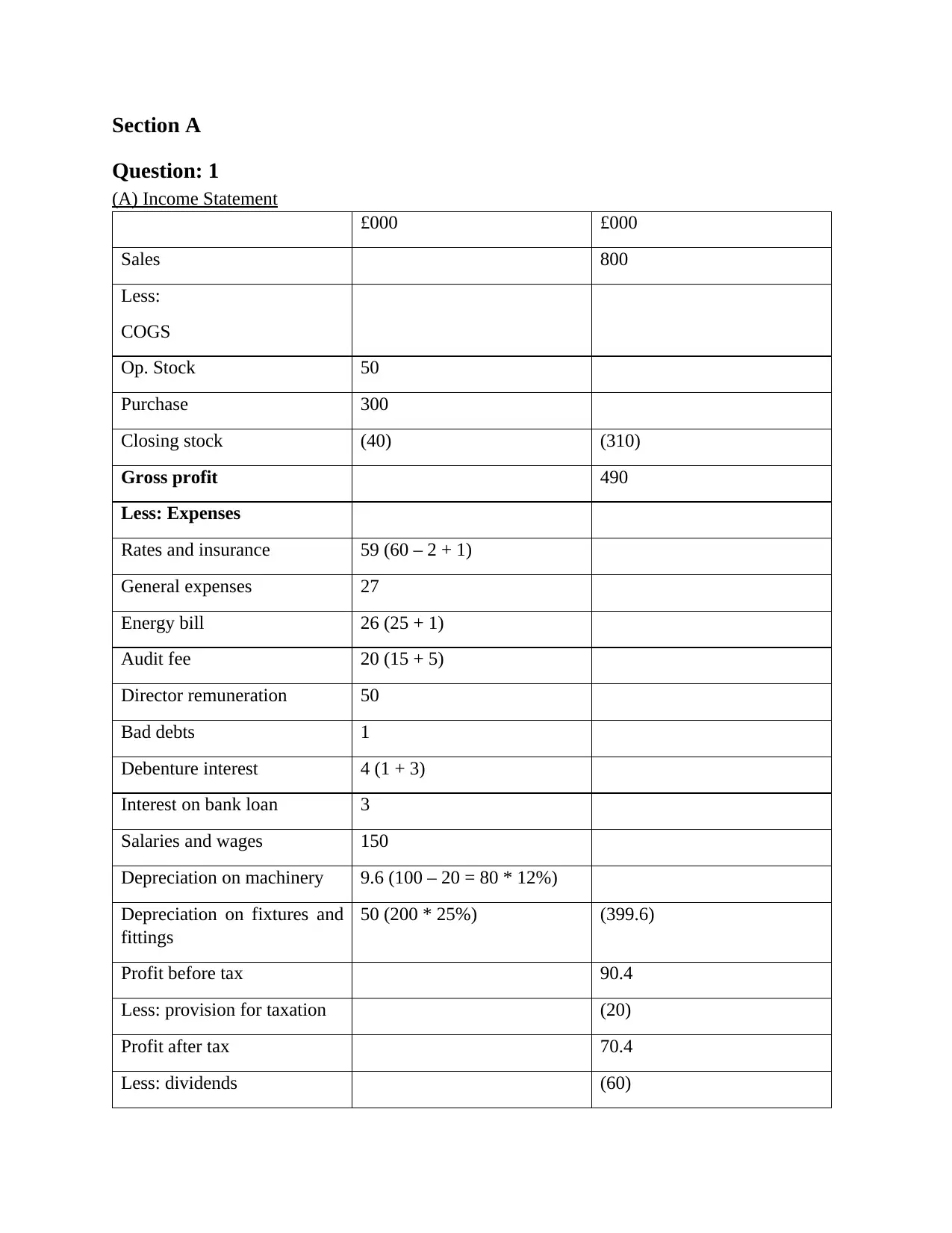

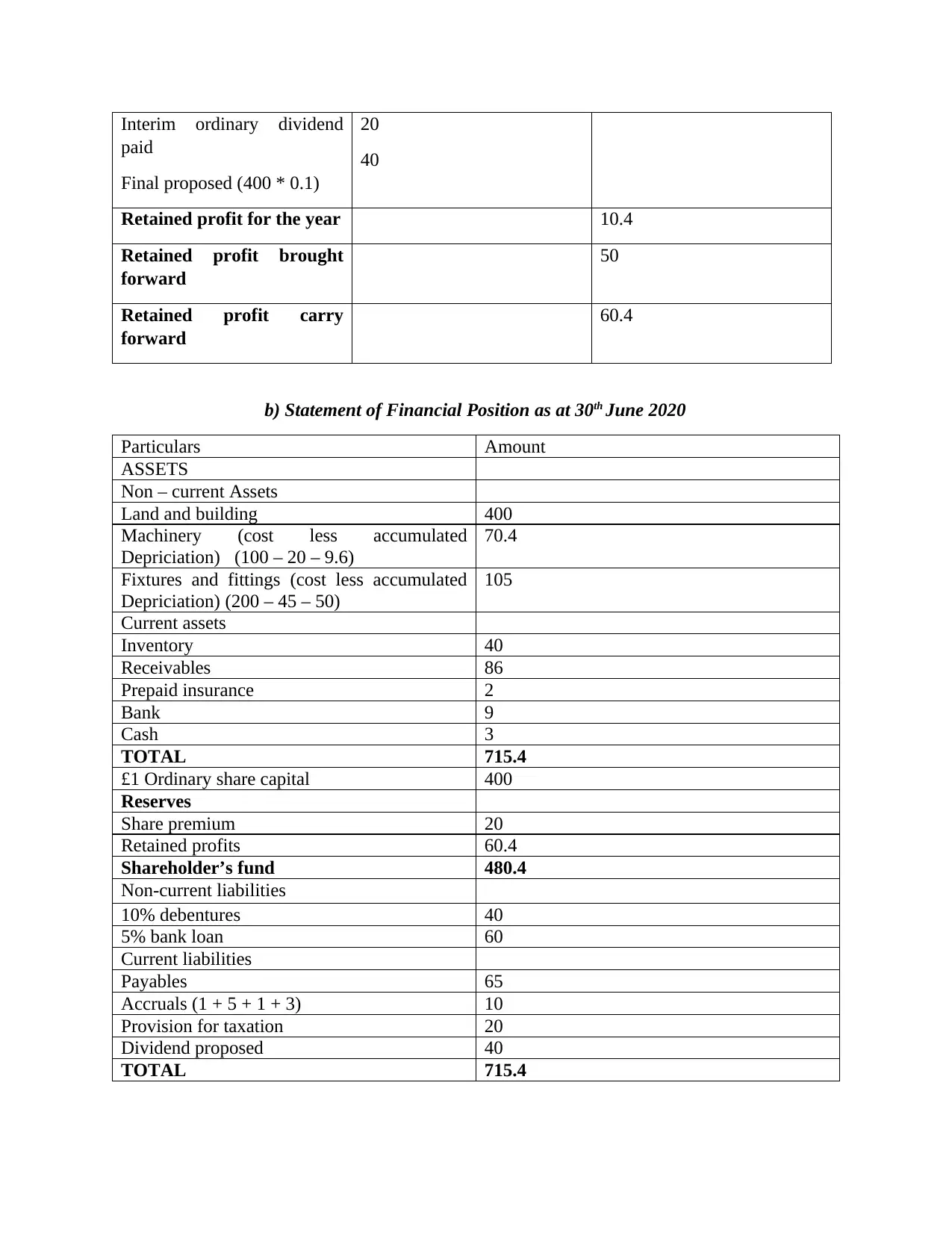

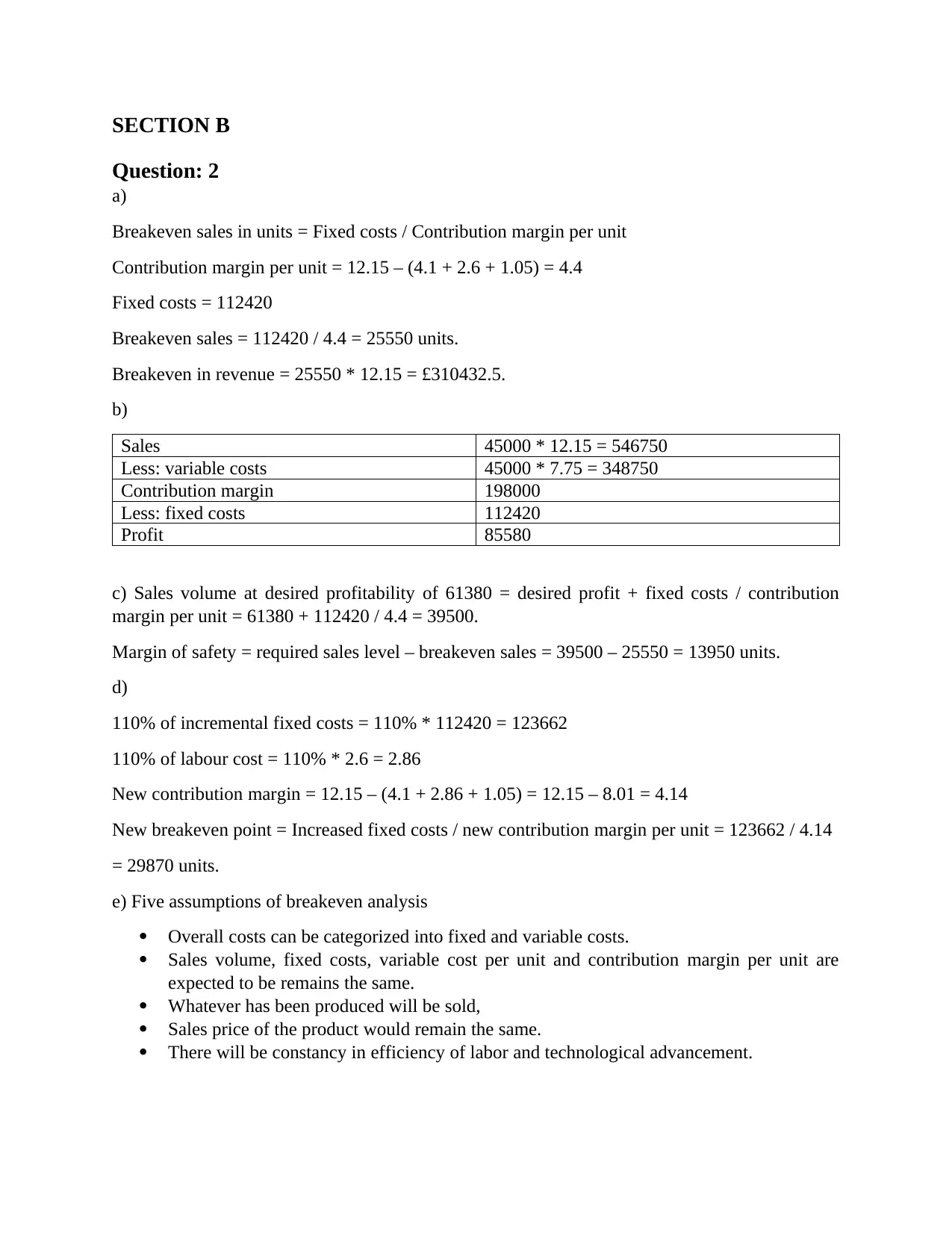

This document presents a comprehensive solution to an accounting for business exam, covering key areas of financial accounting and management accounting. Section A focuses on the preparation of financial statements, including the income statement and statement of financial position, with detailed calculations and adjustments for items such as depreciation, bad debts, and taxation. Section B delves into breakeven analysis, calculating breakeven points in units and revenue, analyzing sales volume for desired profitability, and examining the impact of increased fixed costs and labor costs on the breakeven point. The solution also outlines the key assumptions underlying breakeven analysis. Finally, the document discusses the benefits and limitations of budgeting, the role of budgets in controlling business performance, and the uses of the statement of cash flows in providing insights into a company's financial health and future financing needs. Desklib provides a platform for students to access similar solved assignments and past papers.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.