Accounting for Business: Financial Statement Analysis Homework

VerifiedAdded on 2022/11/14

|7

|1353

|174

Homework Assignment

AI Summary

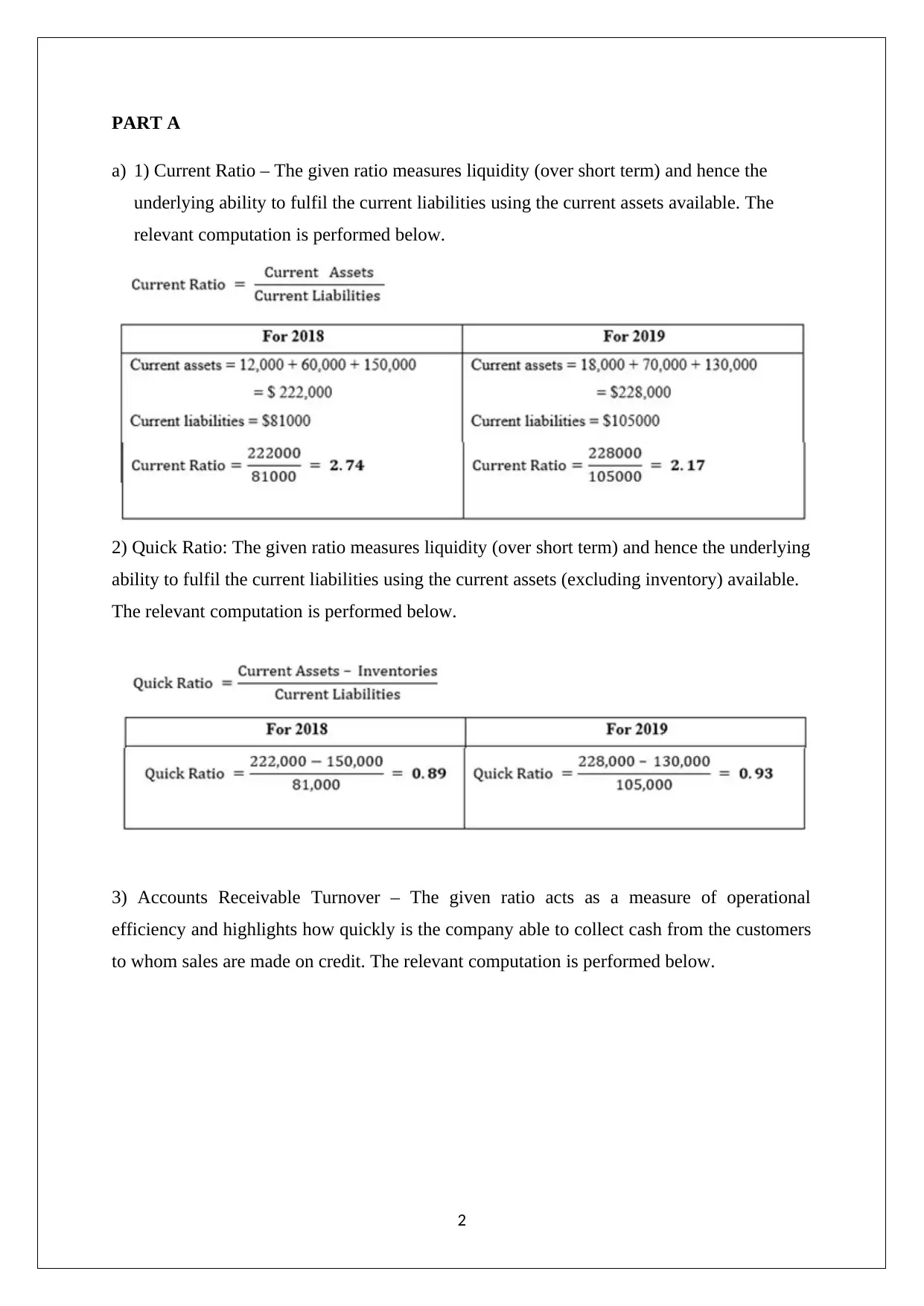

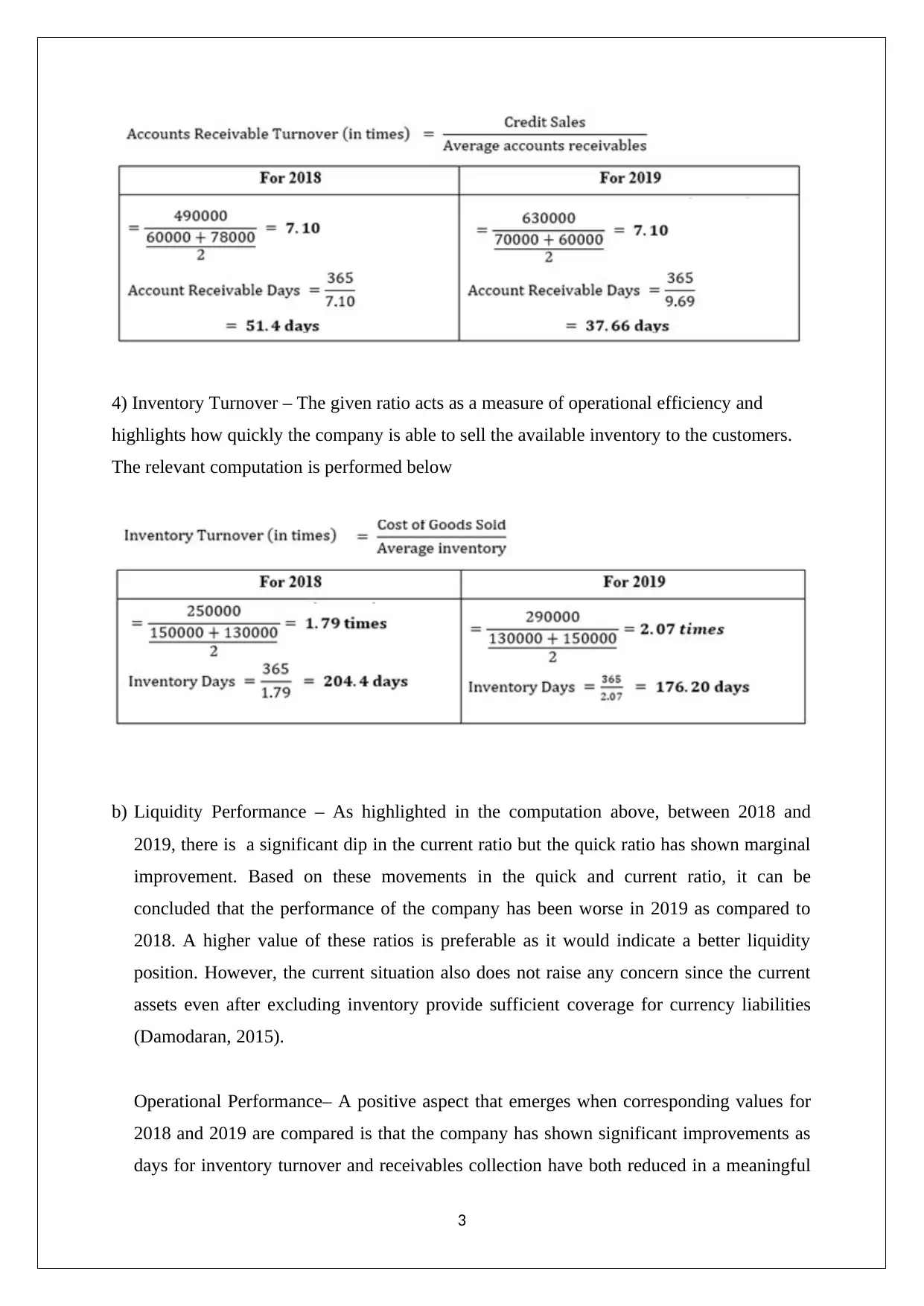

This assignment solution addresses key concepts in accounting and finance. Part A focuses on financial ratio analysis, including liquidity and operational performance metrics such as current ratio, quick ratio, accounts receivable turnover, and inventory turnover. The analysis compares the company's performance between 2018 and 2019, highlighting improvements and areas needing attention. Part B delves into the definitions of income and revenue, classifying various transactions like software sales, update downloads, and interest proceeds. It also examines the treatment of discounts and share issuances. Part C applies financial analysis to a lending scenario, comparing two companies, XYZ and ABC, based on liquidity and business risk. The analysis considers how changes in liabilities affect valuation and investment decisions, providing a comprehensive overview of financial statement analysis and its implications for business decision-making.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.