Accounting for Business: Financial Ratio Analysis & Solvency

VerifiedAdded on 2023/03/21

|8

|1705

|90

Report

AI Summary

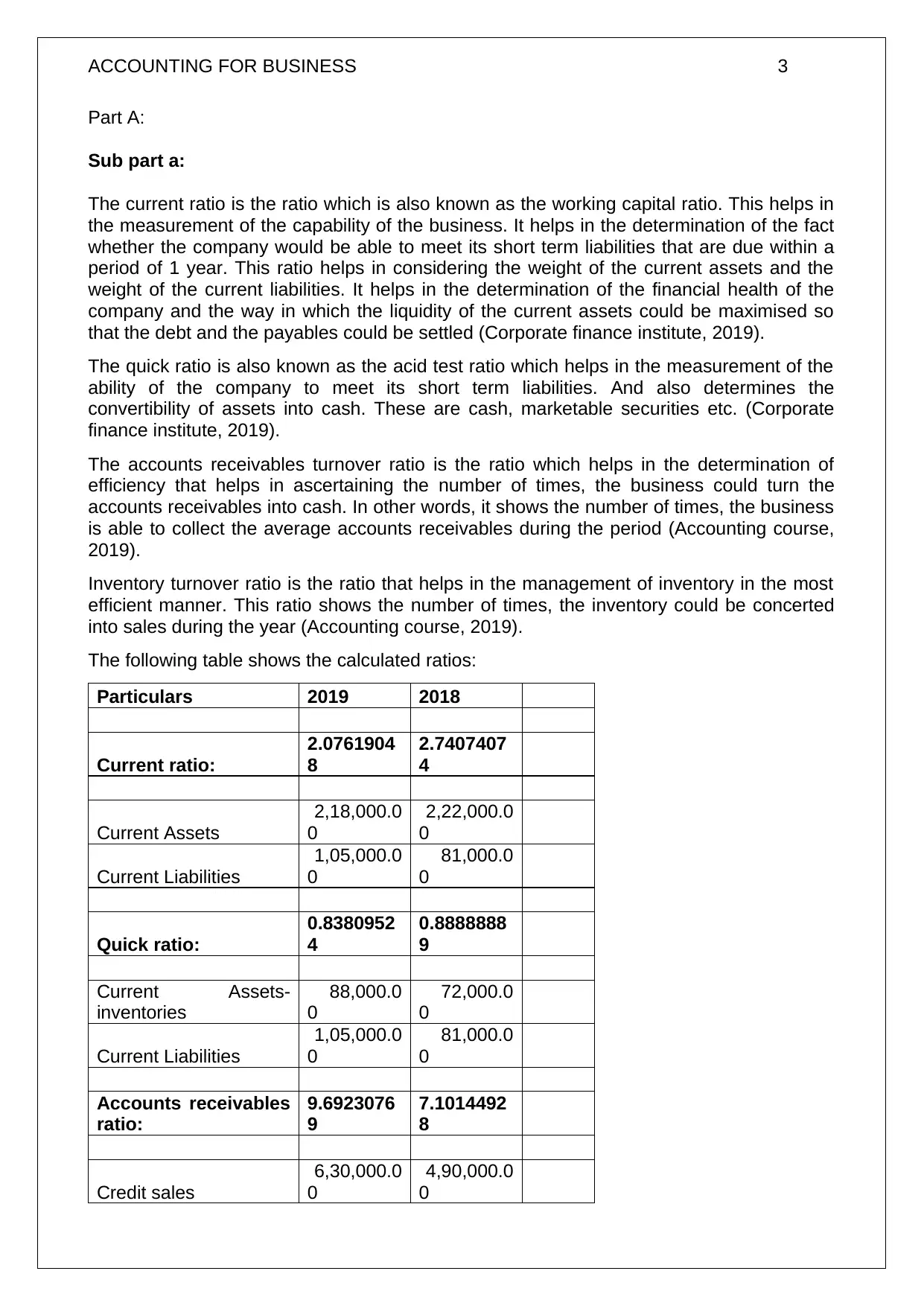

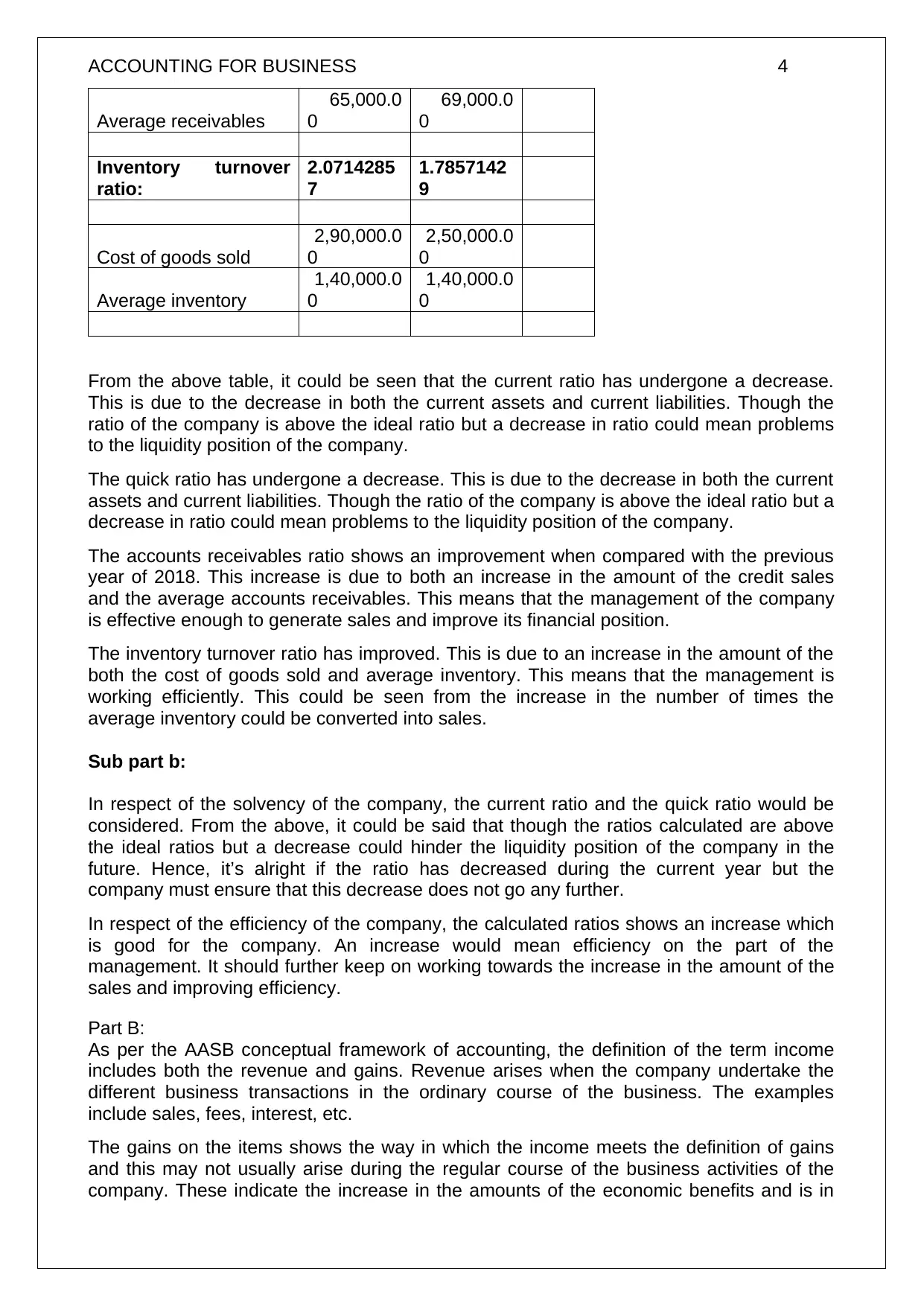

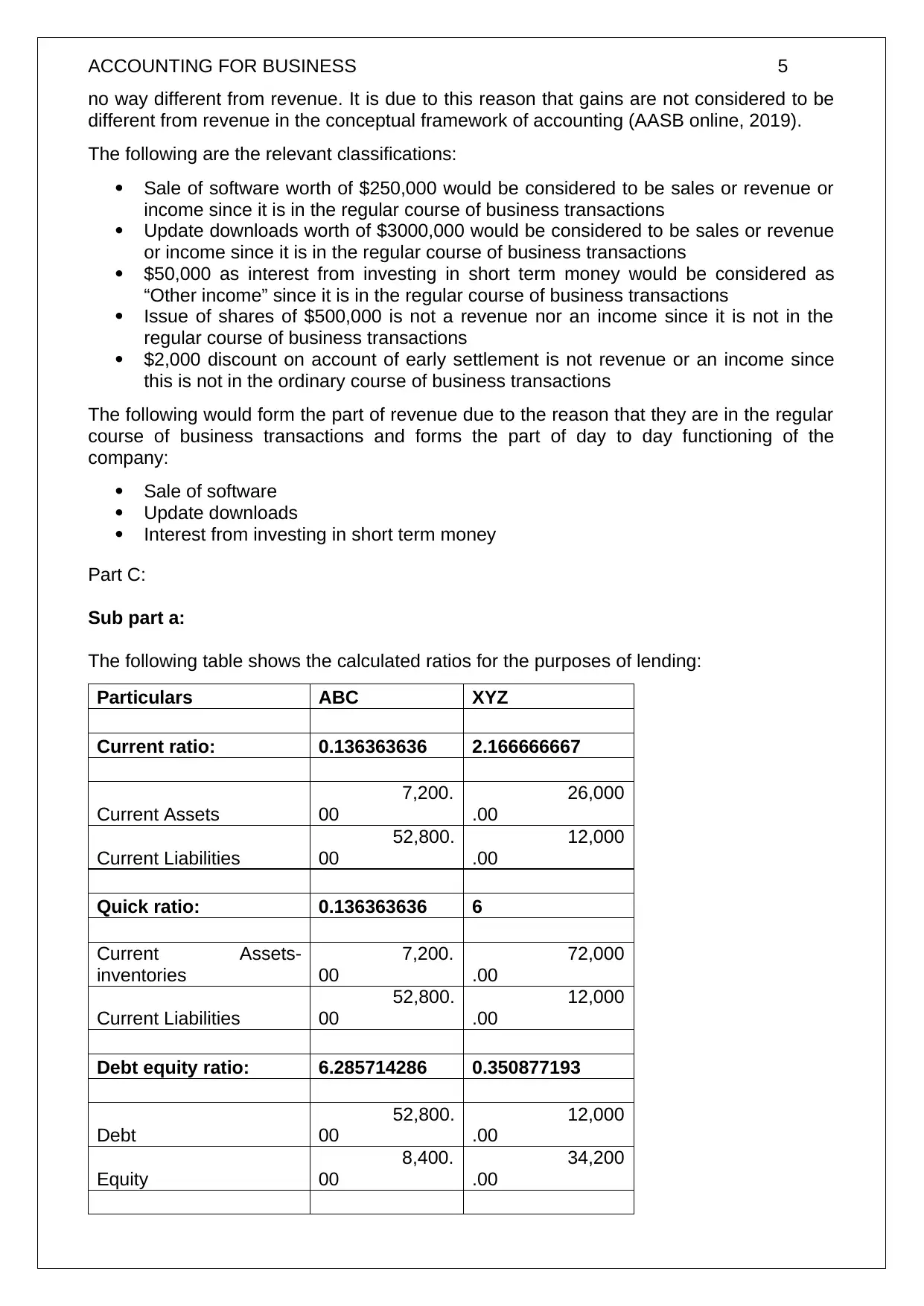

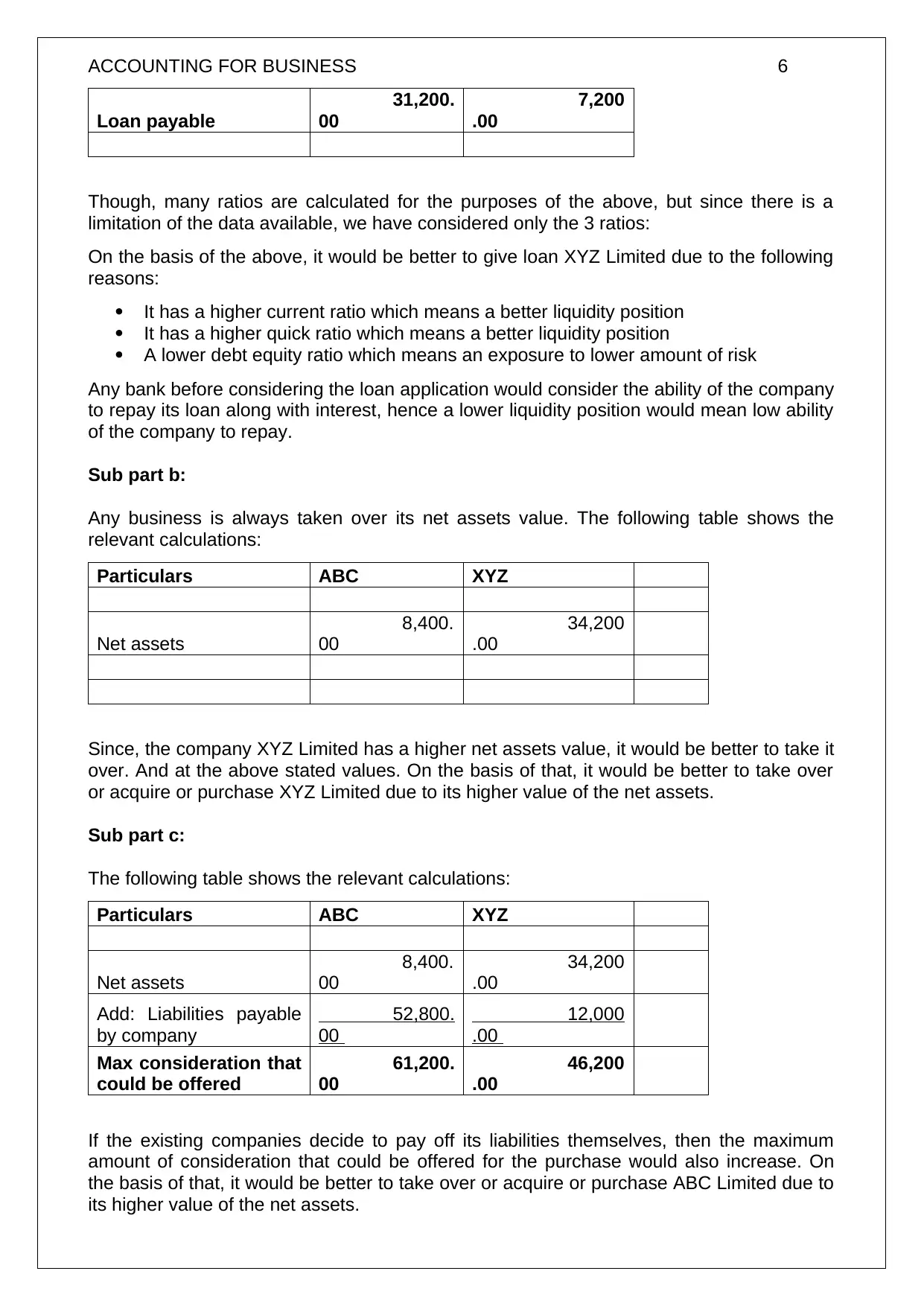

This report provides a detailed financial analysis of a business, focusing on key accounting ratios such as the current ratio, quick ratio, accounts receivable turnover ratio, and inventory turnover ratio. It analyzes the company's solvency and efficiency based on these ratios, comparing data from 2018 and 2019. The report also discusses the AASB conceptual framework of accounting, specifically regarding income, revenue, and gains. Furthermore, it evaluates the financial positions of two companies, ABC and XYZ Limited, using ratios like current ratio, quick ratio, and debt-equity ratio, to determine which would be a better loan candidate or acquisition target, considering net asset value and liabilities. This student contributed assignment is available on Desklib, where students can find similar resources and study tools.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.