Management Accounting for Decision Making: Cancer Charity

VerifiedAdded on 2022/08/22

|13

|3219

|24

Report

AI Summary

This report analyzes management accounting principles for a cancer charity, focusing on a balanced scorecard approach to decision-making. The report provides a detailed breakdown of financial, process, customer, and learning perspectives. The financial perspective emphasizes the importance of profitability, donations, and efficient resource utilization, including measures such as profit increase, growth in donations and grants, and efficient use of the annual budget. The process perspective examines innovative service development, awareness campaigns, compliance with regulations, and operational standards, with measures like the number of innovative services introduced and compliance with laws and regulations. The customer perspective focuses on patient satisfaction, service accessibility, service quality, and complaint resolution, using metrics like patient satisfaction levels and the resolution of complaints. Finally, the learning perspective highlights employee satisfaction, reward initiatives, and skill development, including measures like employee turnover and satisfaction surveys. The report provides a comprehensive framework for the charity to monitor and improve its performance across all key areas, promoting its financial stability and operational effectiveness.

Running head: MANAGEMENT ACCOUNTING FOR DECISION MAKING

Management Accounting for Decision Making

Name of the Student

Name of the University

Author’s Note

Management Accounting for Decision Making

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING FOR DECISION MAKING

Table of Contents

Balanced Scorecard on Monthly Basis......................................................................................2

Explanation of the Measures of Balanced Scorecard.................................................................3

Financial Perspective.............................................................................................................3

Process Perspective................................................................................................................4

Customer Perspective.............................................................................................................6

Learning Perspective..............................................................................................................8

References................................................................................................................................10

Table of Contents

Balanced Scorecard on Monthly Basis......................................................................................2

Explanation of the Measures of Balanced Scorecard.................................................................3

Financial Perspective.............................................................................................................3

Process Perspective................................................................................................................4

Customer Perspective.............................................................................................................6

Learning Perspective..............................................................................................................8

References................................................................................................................................10

2MANAGEMENT ACCOUNTING FOR DECISION MAKING

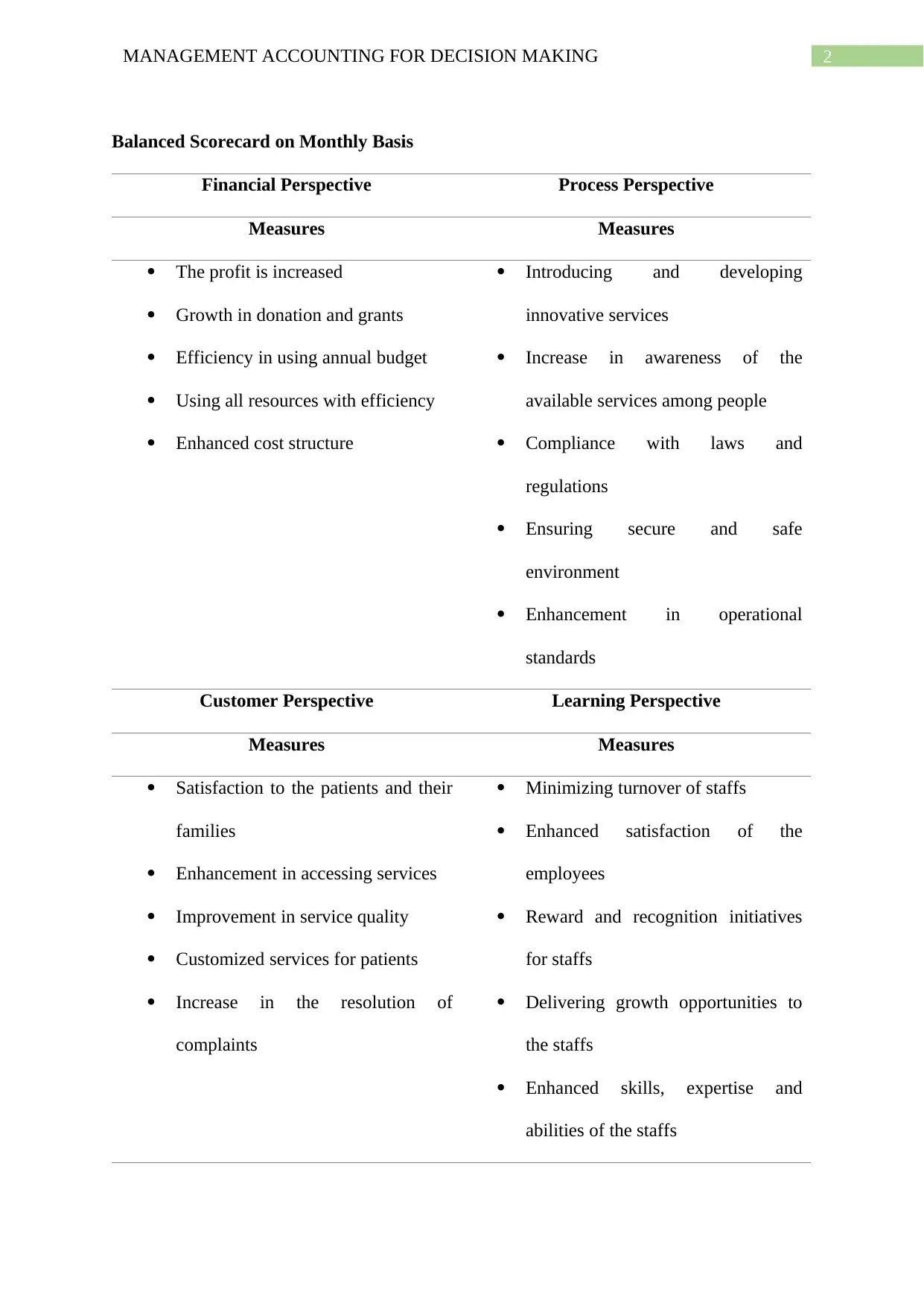

Balanced Scorecard on Monthly Basis

Financial Perspective Process Perspective

Measures Measures

The profit is increased

Growth in donation and grants

Efficiency in using annual budget

Using all resources with efficiency

Enhanced cost structure

Introducing and developing

innovative services

Increase in awareness of the

available services among people

Compliance with laws and

regulations

Ensuring secure and safe

environment

Enhancement in operational

standards

Customer Perspective Learning Perspective

Measures Measures

Satisfaction to the patients and their

families

Enhancement in accessing services

Improvement in service quality

Customized services for patients

Increase in the resolution of

complaints

Minimizing turnover of staffs

Enhanced satisfaction of the

employees

Reward and recognition initiatives

for staffs

Delivering growth opportunities to

the staffs

Enhanced skills, expertise and

abilities of the staffs

Balanced Scorecard on Monthly Basis

Financial Perspective Process Perspective

Measures Measures

The profit is increased

Growth in donation and grants

Efficiency in using annual budget

Using all resources with efficiency

Enhanced cost structure

Introducing and developing

innovative services

Increase in awareness of the

available services among people

Compliance with laws and

regulations

Ensuring secure and safe

environment

Enhancement in operational

standards

Customer Perspective Learning Perspective

Measures Measures

Satisfaction to the patients and their

families

Enhancement in accessing services

Improvement in service quality

Customized services for patients

Increase in the resolution of

complaints

Minimizing turnover of staffs

Enhanced satisfaction of the

employees

Reward and recognition initiatives

for staffs

Delivering growth opportunities to

the staffs

Enhanced skills, expertise and

abilities of the staffs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING FOR DECISION MAKING

Explanation of the Measures of Balanced Scorecard

Financial Perspective

1. Ensuring increase in profit is not considered as crucial, but a minimum amount of

profitability a charity like this small cancer charity needs to maintain in order to

remain operational (Boateng, Akamavi and Ndoro 2016). This requires the cancer

charity to ensure that their profitability is increased on every monthly basis as this is

crucial to uphold its overall stability in a good position. This can be done by tracking

the change in percentage of profitability on monthly basis. For example, there can be

a 5% increase in the current month’s profitability as compared to the previous month.

Alternative strategies need to be employed by the cancer charity in case it fails to be

profitable (Boateng, Akamavi and Ndoro 2016).

2. Donations and grants are the prime source of income of the cancer charity and

therefore, ensuring increase in these needs to be the greatest primacy for it. Increase in

donation is a good measure as this ensures the overall survival of the cancer charity.

This measure will tell that whether the charity is earning adequate income through

donations and grants in order to carry out its operations. Like profitability, this can be

measured by change in percentage. For instance, there can be 10% increase or

decrease in this in the present year (Colbran et al. 2019).

3. Efficient utilization of organizational resources is largely reliant of the development

of budget that includes the projection of income and expenditure. This is a good

measure because this helps in assessing the efficiency of budgetary control within the

cancer charity. This measures assesses the analysis of variance in budgeting. In the

cancer charity, this measure can well be used for assessing the increase or decrease in

the budget variance of one month as compared to the previous months. Variance

Explanation of the Measures of Balanced Scorecard

Financial Perspective

1. Ensuring increase in profit is not considered as crucial, but a minimum amount of

profitability a charity like this small cancer charity needs to maintain in order to

remain operational (Boateng, Akamavi and Ndoro 2016). This requires the cancer

charity to ensure that their profitability is increased on every monthly basis as this is

crucial to uphold its overall stability in a good position. This can be done by tracking

the change in percentage of profitability on monthly basis. For example, there can be

a 5% increase in the current month’s profitability as compared to the previous month.

Alternative strategies need to be employed by the cancer charity in case it fails to be

profitable (Boateng, Akamavi and Ndoro 2016).

2. Donations and grants are the prime source of income of the cancer charity and

therefore, ensuring increase in these needs to be the greatest primacy for it. Increase in

donation is a good measure as this ensures the overall survival of the cancer charity.

This measure will tell that whether the charity is earning adequate income through

donations and grants in order to carry out its operations. Like profitability, this can be

measured by change in percentage. For instance, there can be 10% increase or

decrease in this in the present year (Colbran et al. 2019).

3. Efficient utilization of organizational resources is largely reliant of the development

of budget that includes the projection of income and expenditure. This is a good

measure because this helps in assessing the efficiency of budgetary control within the

cancer charity. This measures assesses the analysis of variance in budgeting. In the

cancer charity, this measure can well be used for assessing the increase or decrease in

the budget variance of one month as compared to the previous months. Variance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING FOR DECISION MAKING

analysis will tell the charity the difference between the budgeted income and

expenditure and actual income and expenditure (Sherr et al. 2017).

4. Efficient use of the available financial resource is desired from the cancer charity in

order to ensure smooth operations. Since these types of charities do not have access to

sufficient amount of funds, they needs to use the available resources carefully in order

to avoid resource wastage. Therefore, this measure tells about the efficiency of the

cancer charity is using the available resources. There are two financial ratios that can

be measured under this on monthly basis for measuring its efficiency; they are return

on capital employed and return on assets. Outcome of these ratios will be crucial for

the cancer charity to measure its efficiency on monthly basis (Anjomshoae et al.

2017).

5. Charitable trusts like this cancer charity have to incur both fixed costs and variable

costs while conducting the operations and this forms the cost structure (Boateng,

Akamavi and Ndoro 2016). This can be considered as a crucial measure as this will

help the cancer charity in the assessment of the proportion of fixed costs and variable

costs. Under this particular measure, it will be required for the cancer charity to

measure whether there is increase in the cost structure in the current month as

compared to the previous month. This is crucial as cost is associated with profit

(Krstić, Sekulić and Ivanović 2015).

Process Perspective

1. It is needed for the cancer charity to measure how many innovative services it has

developed and introduced on monthly basis. This needs to be considered as a good

measure as it is possible to cater to the needs of the patients in better manner with

innovative services (Dimitropoulos, Kosmas and Douvis 2017). One major way to

measure this is to keep track of the newly introduced innovative services in terms of

analysis will tell the charity the difference between the budgeted income and

expenditure and actual income and expenditure (Sherr et al. 2017).

4. Efficient use of the available financial resource is desired from the cancer charity in

order to ensure smooth operations. Since these types of charities do not have access to

sufficient amount of funds, they needs to use the available resources carefully in order

to avoid resource wastage. Therefore, this measure tells about the efficiency of the

cancer charity is using the available resources. There are two financial ratios that can

be measured under this on monthly basis for measuring its efficiency; they are return

on capital employed and return on assets. Outcome of these ratios will be crucial for

the cancer charity to measure its efficiency on monthly basis (Anjomshoae et al.

2017).

5. Charitable trusts like this cancer charity have to incur both fixed costs and variable

costs while conducting the operations and this forms the cost structure (Boateng,

Akamavi and Ndoro 2016). This can be considered as a crucial measure as this will

help the cancer charity in the assessment of the proportion of fixed costs and variable

costs. Under this particular measure, it will be required for the cancer charity to

measure whether there is increase in the cost structure in the current month as

compared to the previous month. This is crucial as cost is associated with profit

(Krstić, Sekulić and Ivanović 2015).

Process Perspective

1. It is needed for the cancer charity to measure how many innovative services it has

developed and introduced on monthly basis. This needs to be considered as a good

measure as it is possible to cater to the needs of the patients in better manner with

innovative services (Dimitropoulos, Kosmas and Douvis 2017). One major way to

measure this is to keep track of the newly introduced innovative services in terms of

5MANAGEMENT ACCOUNTING FOR DECISION MAKING

numbers on monthly basis. In this way, the cancer charity will be able to know

whether there is any increased need to develop and introduce new innovative services

for the patients.

2. With the aim to inform the common people about the available services, the cancer

charity is needed to ensure the introduction of promotional activities in order to attract

increased number of people towards the organization. Increase in this awareness

needs to be ensured as this ensures the growth of the cancer charity. This can be

measured through two ways (Toklu 2017). First, the cancer charity needs to assess the

increase or decrease in the number of visitors to their facilities and official website on

monthly basis. Second, they can conduct surveys both online and offline basis for

gaining the number of people aware of the services and facilities of the organization

(Dimitropoulos, Kosmas and Douvis 2017).

3. There are certain legislations, laws and regulations that need to be adhered by the

cancer charity at the time to conduct its operations. Strict compliance with these laws

and regulations is paramount as violation of this can put the cancer charity in legal

issues. The most important way to measure the level of compliance with these laws

and regulations is to assess the increase or decrease in the number of cases associated

with the violation of these laws and regulations for every month (Kushner 2018).

4. One major way for the cancer charity to achieve operational excellence is develop a

secure and safe environment for its staffs, patients, their facilities and other visitors.

This is an important measure because a safe and secure environment is required to

satisfy all internal and external stakeholders of the charity. There are many ways that

can be utilized for measuring this on monthly basis; the cancer charity can track the

increase or decrease in the number of injuries and accidents in the workplace, number

of reported cases of medication error, percentage of people feeling safe within the

numbers on monthly basis. In this way, the cancer charity will be able to know

whether there is any increased need to develop and introduce new innovative services

for the patients.

2. With the aim to inform the common people about the available services, the cancer

charity is needed to ensure the introduction of promotional activities in order to attract

increased number of people towards the organization. Increase in this awareness

needs to be ensured as this ensures the growth of the cancer charity. This can be

measured through two ways (Toklu 2017). First, the cancer charity needs to assess the

increase or decrease in the number of visitors to their facilities and official website on

monthly basis. Second, they can conduct surveys both online and offline basis for

gaining the number of people aware of the services and facilities of the organization

(Dimitropoulos, Kosmas and Douvis 2017).

3. There are certain legislations, laws and regulations that need to be adhered by the

cancer charity at the time to conduct its operations. Strict compliance with these laws

and regulations is paramount as violation of this can put the cancer charity in legal

issues. The most important way to measure the level of compliance with these laws

and regulations is to assess the increase or decrease in the number of cases associated

with the violation of these laws and regulations for every month (Kushner 2018).

4. One major way for the cancer charity to achieve operational excellence is develop a

secure and safe environment for its staffs, patients, their facilities and other visitors.

This is an important measure because a safe and secure environment is required to

satisfy all internal and external stakeholders of the charity. There are many ways that

can be utilized for measuring this on monthly basis; the cancer charity can track the

increase or decrease in the number of injuries and accidents in the workplace, number

of reported cases of medication error, percentage of people feeling safe within the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING FOR DECISION MAKING

building of the cancer charity, percentage of people getting physical examination and

others (Johansson and Larsson 2015).

5. Improved operational standards is required in case the cancer charity wants to be

successful or to maintain its success (Johansson and Larsson 2015). This needs to be

considered as a crucial measure because enhanced operational standards ensure the

patients of the charity receive quality facilities and services from it. The most crucial

way to measure this on monthly basis is to assess the level of compliance with all the

required standards of operations and to assess whether there is any case where the

charity fails to maintain its compliance with the operational standards (Sands, Rae and

Gadenne 2016).

Customer Perspective

1. The aim of the cancer charity is to satisfy the needs of the patients and their facilities

with their services and facilities; and this puts the obligation on the charity to take into

account the desires and needs of the patients and their families. This can be

considered as a good measure as the level of satisfaction is positively associated with

their performance. Certain ways can be used to assess this; the charity can check the

number of cases where the patients’ families are unsatisfied or satisfied; or the charity

can conduct surveys by taking the views of the patients and their families (Manville et

al. 2019).

2. Since the key objective of the cancer charity is to help the cancer patients and their

families with the required medical services and resources, the charity needs to ensure

that these patients have easy access to these services, facilities and resources of them.

Improved access to the services and facilities of the charity is a crucial measure

because the satisfaction of the patients and services is associated with this. For

measuring this on monthly basis, the cancer charity can take feedbacks from the

building of the cancer charity, percentage of people getting physical examination and

others (Johansson and Larsson 2015).

5. Improved operational standards is required in case the cancer charity wants to be

successful or to maintain its success (Johansson and Larsson 2015). This needs to be

considered as a crucial measure because enhanced operational standards ensure the

patients of the charity receive quality facilities and services from it. The most crucial

way to measure this on monthly basis is to assess the level of compliance with all the

required standards of operations and to assess whether there is any case where the

charity fails to maintain its compliance with the operational standards (Sands, Rae and

Gadenne 2016).

Customer Perspective

1. The aim of the cancer charity is to satisfy the needs of the patients and their facilities

with their services and facilities; and this puts the obligation on the charity to take into

account the desires and needs of the patients and their families. This can be

considered as a good measure as the level of satisfaction is positively associated with

their performance. Certain ways can be used to assess this; the charity can check the

number of cases where the patients’ families are unsatisfied or satisfied; or the charity

can conduct surveys by taking the views of the patients and their families (Manville et

al. 2019).

2. Since the key objective of the cancer charity is to help the cancer patients and their

families with the required medical services and resources, the charity needs to ensure

that these patients have easy access to these services, facilities and resources of them.

Improved access to the services and facilities of the charity is a crucial measure

because the satisfaction of the patients and services is associated with this. For

measuring this on monthly basis, the cancer charity can take feedbacks from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING FOR DECISION MAKING

patients and their families on the fact that whether they are satisfied or not with the

services and facilities provided (Al-Hosaini and Sofian 2015).

3. Bringing continuous improvements in the quality of services provided is crucial for

the survival and success of the cancer charity. This measure is an important one

because of the fact that the families of the patients assess the quality of services

before taking them. This aspect can be measured through the introduction of rating

system of the provided services and facilities of the cancer charity. This will help the

charity to identify the areas with lowest rating and it means these areas require

additional consideration for improving the overall quality (Catuogno et al. 2017).

4. Since the main operation of the cancer charity is involved in providing services and

supports to the cancer patients, this can be done in better manner by providing the

cancer patients with the services customized as per their needs and demands. This is a

crucial measure as this ensures satisfying the unique requirements of the patients and

their families. One crucial way of measuring the progress of this is to assess the

number of customized services provided to the customers in order to cater to the

needs of them. Therefore, the number of newly developed customized services is the

way to measure this (Sri, Lestari and Nurcholisah 2015).

5. Receiving complaints from the customers is a normal process for the service-provider

organizations like cancer charity and the need is to effective tackling of these

complaints received so that timely resolution can be provided to the patients’ families.

Increased timely resolution of complaints is a crucial measure because this is

associated with satisfaction of the patients and their families. In order to measure this

on monthly basis, the cancer charity needs to assess whether there is an increase or

decrease in the number of complaints resolution in time. This is crucial for forming an

operational complaint management framework (Soysa, Jayamaha and Grigg 2016).

patients and their families on the fact that whether they are satisfied or not with the

services and facilities provided (Al-Hosaini and Sofian 2015).

3. Bringing continuous improvements in the quality of services provided is crucial for

the survival and success of the cancer charity. This measure is an important one

because of the fact that the families of the patients assess the quality of services

before taking them. This aspect can be measured through the introduction of rating

system of the provided services and facilities of the cancer charity. This will help the

charity to identify the areas with lowest rating and it means these areas require

additional consideration for improving the overall quality (Catuogno et al. 2017).

4. Since the main operation of the cancer charity is involved in providing services and

supports to the cancer patients, this can be done in better manner by providing the

cancer patients with the services customized as per their needs and demands. This is a

crucial measure as this ensures satisfying the unique requirements of the patients and

their families. One crucial way of measuring the progress of this is to assess the

number of customized services provided to the customers in order to cater to the

needs of them. Therefore, the number of newly developed customized services is the

way to measure this (Sri, Lestari and Nurcholisah 2015).

5. Receiving complaints from the customers is a normal process for the service-provider

organizations like cancer charity and the need is to effective tackling of these

complaints received so that timely resolution can be provided to the patients’ families.

Increased timely resolution of complaints is a crucial measure because this is

associated with satisfaction of the patients and their families. In order to measure this

on monthly basis, the cancer charity needs to assess whether there is an increase or

decrease in the number of complaints resolution in time. This is crucial for forming an

operational complaint management framework (Soysa, Jayamaha and Grigg 2016).

8MANAGEMENT ACCOUNTING FOR DECISION MAKING

Learning Perspective

1. Since the cancer charity is a charitable not-for-profit organization, staffs do not

receive any wage from it; therefore, this is a crucial job for the management of the

cancer charity to retain the staffs (Arena, Azzone and Bengo 2015). This measure is

important as the charity needs to motive and encourage its employees in such a

manner so that they agree to work for it without any expectation. One important way

to measure this on monthly basis is to assess whether there is increase or decrease in

the employee turnover as compared to the previous year. The outcome can be

presented in the form of percentage.

2. Satisfied staffs are always ready to give their full effort and commitment towards the

organizations and therefore, the cancer charity needs to ensure increase in employee

or staff satisfaction for gaining their full commitment. The staffs of the cancer charity

should receive career growth opportunities and learning opportunities from the

organization so they can be satisfied. One major way to measure this on monthly basis

is to conduct surveys on the employees through questionnaire that will contain

relevant questions associated with employee or staff satisfaction. Increase in

employee satisfaction reduced staff turnover and staff attrition (Kalender and Vayvay

2016).

3. In order to motivate the staffs, the cancer charity can employ the process of

recognizing and rewarding the staffs. In this process, the charity will identify the

staffs with superior performance so that they can be rewarded in front of everyone.

This measure is crucial as this plays a crucial role in identifying the good performing

staffs. In order to measure this on monthly basis, the cancer charity can assess the

number of employees recognized and rewarded in the current month as compared to

Learning Perspective

1. Since the cancer charity is a charitable not-for-profit organization, staffs do not

receive any wage from it; therefore, this is a crucial job for the management of the

cancer charity to retain the staffs (Arena, Azzone and Bengo 2015). This measure is

important as the charity needs to motive and encourage its employees in such a

manner so that they agree to work for it without any expectation. One important way

to measure this on monthly basis is to assess whether there is increase or decrease in

the employee turnover as compared to the previous year. The outcome can be

presented in the form of percentage.

2. Satisfied staffs are always ready to give their full effort and commitment towards the

organizations and therefore, the cancer charity needs to ensure increase in employee

or staff satisfaction for gaining their full commitment. The staffs of the cancer charity

should receive career growth opportunities and learning opportunities from the

organization so they can be satisfied. One major way to measure this on monthly basis

is to conduct surveys on the employees through questionnaire that will contain

relevant questions associated with employee or staff satisfaction. Increase in

employee satisfaction reduced staff turnover and staff attrition (Kalender and Vayvay

2016).

3. In order to motivate the staffs, the cancer charity can employ the process of

recognizing and rewarding the staffs. In this process, the charity will identify the

staffs with superior performance so that they can be rewarded in front of everyone.

This measure is crucial as this plays a crucial role in identifying the good performing

staffs. In order to measure this on monthly basis, the cancer charity can assess the

number of employees recognized and rewarded in the current month as compared to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING FOR DECISION MAKING

the previous month. This is an effective manner for motivating and encouraging the

employees with superior performance (Muda, Erlina and AA 2018).

4. In order to provide the staffs with learning and personal development opportunities,

the cancer charity needs to make it sure that the staffs are receiving opportunities for

their personal growth. This measure needs to be considered as an important one

because developed and skilful staffs are essential for delivering value services and

facilities to the cancer patients. In order to measure this on monthly basis, the cancer

charity needs to assess the increase or decrease in the number of newly introduced

career growth programs for its staffs as compared to the previous year (Hansen and

Schaltegger 2016).

5. Since staffs are the most valuable assets within the organizations, the organizational

excellence is reliant on the enhanced skills, expertise and abilities of its staffs.

Increase in the skills, expertise and abilities of the staffs is a crucial measure as skilful

expert staffs are required for catering to the unique needs of the cancer patients. In

order to measure this on monthly basis, cancer charity needs to assess increase or

decrease in the number of opportunities provided to its staffs for enhancing their

skills, expertise and abilities. At the same time, the method of performance appraisal

can be adopted by the cancer charity in order to assess the skills, expertise and

capabilities of its staffs (Muda, Erlina and AA 2018).

the previous month. This is an effective manner for motivating and encouraging the

employees with superior performance (Muda, Erlina and AA 2018).

4. In order to provide the staffs with learning and personal development opportunities,

the cancer charity needs to make it sure that the staffs are receiving opportunities for

their personal growth. This measure needs to be considered as an important one

because developed and skilful staffs are essential for delivering value services and

facilities to the cancer patients. In order to measure this on monthly basis, the cancer

charity needs to assess the increase or decrease in the number of newly introduced

career growth programs for its staffs as compared to the previous year (Hansen and

Schaltegger 2016).

5. Since staffs are the most valuable assets within the organizations, the organizational

excellence is reliant on the enhanced skills, expertise and abilities of its staffs.

Increase in the skills, expertise and abilities of the staffs is a crucial measure as skilful

expert staffs are required for catering to the unique needs of the cancer patients. In

order to measure this on monthly basis, cancer charity needs to assess increase or

decrease in the number of opportunities provided to its staffs for enhancing their

skills, expertise and abilities. At the same time, the method of performance appraisal

can be adopted by the cancer charity in order to assess the skills, expertise and

capabilities of its staffs (Muda, Erlina and AA 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING FOR DECISION MAKING

References

Al-Hosaini, F.F. and Sofian, S., 2015. A review of balanced scorecard framework in higher

education institution (HEIs). International Review of Management and Marketing, 5(1),

pp.26-35.

Anjomshoae, A., Hassan, A., Kunz, N., Wong, K.Y. and de Leeuw, S., 2017. Toward a

dynamic balanced scorecard model for humanitarian relief organizations’ performance

management. Journal of Humanitarian Logistics and Supply Chain Management.

Arena, M., Azzone, G. and Bengo, I., 2015. Performance measurement for social

enterprises. VOLUNTAS: International Journal of Voluntary and Nonprofit

Organizations, 26(2), pp.649-672.

Boateng, A., Akamavi, R.K. and Ndoro, G., 2016. Measuring performance of non‐profit

organisations: evidence from large charities. Business Ethics: A European Review, 25(1),

pp.59-74.

Catuogno, S., Arena, C., Saggese, S. and Sarto, F., 2017. Balanced performance measurement

in research hospitals: the participative case study of a haematology department. BMC health

services research, 17(1), p.522.

Colbran, R., Ramsden, R., Stagnitti, K. and Toumbourou, J.W., 2019. Advancing towards

contemporary practice: a systematic review of organisational performance measures for non-

acute health charities. BMC health services research, 19(1), p.132.

Dimitropoulos, P., Kosmas, I. and Douvis, I., 2017. Implementing the balanced scorecard in a

local government sport organization. International Journal of Productivity and Performance

Management.

References

Al-Hosaini, F.F. and Sofian, S., 2015. A review of balanced scorecard framework in higher

education institution (HEIs). International Review of Management and Marketing, 5(1),

pp.26-35.

Anjomshoae, A., Hassan, A., Kunz, N., Wong, K.Y. and de Leeuw, S., 2017. Toward a

dynamic balanced scorecard model for humanitarian relief organizations’ performance

management. Journal of Humanitarian Logistics and Supply Chain Management.

Arena, M., Azzone, G. and Bengo, I., 2015. Performance measurement for social

enterprises. VOLUNTAS: International Journal of Voluntary and Nonprofit

Organizations, 26(2), pp.649-672.

Boateng, A., Akamavi, R.K. and Ndoro, G., 2016. Measuring performance of non‐profit

organisations: evidence from large charities. Business Ethics: A European Review, 25(1),

pp.59-74.

Catuogno, S., Arena, C., Saggese, S. and Sarto, F., 2017. Balanced performance measurement

in research hospitals: the participative case study of a haematology department. BMC health

services research, 17(1), p.522.

Colbran, R., Ramsden, R., Stagnitti, K. and Toumbourou, J.W., 2019. Advancing towards

contemporary practice: a systematic review of organisational performance measures for non-

acute health charities. BMC health services research, 19(1), p.132.

Dimitropoulos, P., Kosmas, I. and Douvis, I., 2017. Implementing the balanced scorecard in a

local government sport organization. International Journal of Productivity and Performance

Management.

11MANAGEMENT ACCOUNTING FOR DECISION MAKING

Hansen, E.G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Johansson, A. and Larsson, L., 2015. A standalone sustainability balanced scorecard.

Kalender, Z.T. and Vayvay, Ö., 2016. The fifth pillar of the balanced scorecard:

sustainability. Procedia-Social and Behavioral Sciences, 235, pp.76-83.

Krstić, B., Sekulić, V. and Ivanović, V., 2015. How to apply the Sustainability Balanced

Scorecard concept. Economic Themes, 52(1), pp.65-80.

Kushner, R.J., 2018, July. Evaluating a Nonprofit Health Index as a Policy Tool. In Nonprofit

Policy Forum (Vol. 9, No. 3). De Gruyter.

Manville, G., Karakas, F., Polkinghorne, M. and Petford, N., 2019. Supporting open

innovation with the use of a balanced scorecard approach: a study on deep smarts and

effective knowledge transfer to SMEs. Production Planning & Control, 30(10-12), pp.842-

853.

Muda, I., Erlina, I.Y. and AA, N., 2018. Performance Audit and Balanced Scorecard

Perspective. International Journal of Civil Engineering and Technology, 9(5), pp.1321-1333.

Sands, J.S., Rae, K.N. and Gadenne, D., 2016. An empirical investigation on the links within

a sustainability balanced scorecard (SBSC) framework and their impact on financial

performance. Accounting Research Journal.

Sherr, K., Fernandes, Q., Kanté, A.M., Bawah, A., Condo, J. and Mutale, W., 2017.

Measuring health systems strength and its impact: experiences from the African Health

Initiative. BMC health services research, 17(3), p.827.

Soysa, I.B., Jayamaha, N.P. and Grigg, N.P., 2016. Operationalising performance

measurement dimensions for the Australasian nonprofit healthcare sector. The TQM Journal.

Hansen, E.G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Johansson, A. and Larsson, L., 2015. A standalone sustainability balanced scorecard.

Kalender, Z.T. and Vayvay, Ö., 2016. The fifth pillar of the balanced scorecard:

sustainability. Procedia-Social and Behavioral Sciences, 235, pp.76-83.

Krstić, B., Sekulić, V. and Ivanović, V., 2015. How to apply the Sustainability Balanced

Scorecard concept. Economic Themes, 52(1), pp.65-80.

Kushner, R.J., 2018, July. Evaluating a Nonprofit Health Index as a Policy Tool. In Nonprofit

Policy Forum (Vol. 9, No. 3). De Gruyter.

Manville, G., Karakas, F., Polkinghorne, M. and Petford, N., 2019. Supporting open

innovation with the use of a balanced scorecard approach: a study on deep smarts and

effective knowledge transfer to SMEs. Production Planning & Control, 30(10-12), pp.842-

853.

Muda, I., Erlina, I.Y. and AA, N., 2018. Performance Audit and Balanced Scorecard

Perspective. International Journal of Civil Engineering and Technology, 9(5), pp.1321-1333.

Sands, J.S., Rae, K.N. and Gadenne, D., 2016. An empirical investigation on the links within

a sustainability balanced scorecard (SBSC) framework and their impact on financial

performance. Accounting Research Journal.

Sherr, K., Fernandes, Q., Kanté, A.M., Bawah, A., Condo, J. and Mutale, W., 2017.

Measuring health systems strength and its impact: experiences from the African Health

Initiative. BMC health services research, 17(3), p.827.

Soysa, I.B., Jayamaha, N.P. and Grigg, N.P., 2016. Operationalising performance

measurement dimensions for the Australasian nonprofit healthcare sector. The TQM Journal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.