Managerial Accounting Case Studies: Cost Analysis & Decision Making

VerifiedAdded on 2023/01/11

|12

|3562

|87

Case Study

AI Summary

This managerial accounting case study analyzes cost concepts and their application in business decision-making. The case study examines cost classifications, including fixed, variable, direct, indirect, product, and period costs, and their relevance to the Franks' laundry business. It explores various options, such as outsourcing laundry services, using a Laundromat, and purchasing appliances, evaluating costs and benefits to determine the most financially sound decision. Furthermore, the case study delves into the implications of hiring an additional employee, assessing the associated costs and revenue generation to determine the profitability of expanding the business. Finally, the case study analyzes the expansion of the facility, considering the costs and regulations of moving to a new location to maximize profit. The analysis includes a critique of a journal article related to management accounting systems.

Managerial Accounting 1

MANAGEMENT ACCOUNTING CASE STUDIES

By (Name)

The Name of the Class

Professor

The Name of the School

The City and State

Date

MANAGEMENT ACCOUNTING CASE STUDIES

By (Name)

The Name of the Class

Professor

The Name of the School

The City and State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 2

Part A: Case Study Analysis

QNS 1

In business, there are always a lot of expenses incurred to run the day to day activities

of the business. The classification of production cost is done from different point of

views. There is a fixed and variable cost, which is based on the costs responsiveness to

the output level, direct and indirect costs and product and period costs. Although these

classifications of costs may seem to overlap one another, a firm may only use one

approach to classify its production costs. (Chenhall and Moers 2015). These costs are

discussed into details below;

a) Fixed and variable costs. This is a classification of costs based on whether the

costs are constant or they change with the changes in the level of output. Fixed

costs are those costs in the production which remain constant irrespective of

whether the level of output is increased or not. For example the rent of a room

will remain constant whether the firm is producing or not. Variable costs on the

other hand are those costs which change in direct proportion with the output. A

good example of variable cost is the cost of labor or direct materials. To produce

more and more output, one will need to use more and more direct materials and

more labor will also be required.

b) Direct and indirect costs. This method of classifying production costs focuses on

the ability to trace the costs to the end product. Direct costs can be seen as

variable cost as per the above discussion. They are those costs which are

incurred in direct proportion with the output level. They are the ones used in

costing the final product because one can easily determine how much was put

into a particular product. For example one can easily determine how much of the

raw materials were put into each unit of output. Indirect costs, also known as

production overheads, are those types of costs which are not easy to quantify in

the final output. The salary paid to production supervisor is a good example as

such expense cannot be easily traced to the final product.

c) Product and period costs. This classification method divides the costs from the

point of view of the end product. Product costs are those costs which are

incurred direct to the production. Such costs include the cost of raw materials

and the cost of direct labor. They are the same costs used to do the product

costing. Period costs on the other hand are those costs which are not closely

related to the product and they are treated as period expenses. Rent for instant is

seem as a periodic expense to be expensed every month other than a product

cost to be absorbed by the end product.

QNS 2

Part A: Case Study Analysis

QNS 1

In business, there are always a lot of expenses incurred to run the day to day activities

of the business. The classification of production cost is done from different point of

views. There is a fixed and variable cost, which is based on the costs responsiveness to

the output level, direct and indirect costs and product and period costs. Although these

classifications of costs may seem to overlap one another, a firm may only use one

approach to classify its production costs. (Chenhall and Moers 2015). These costs are

discussed into details below;

a) Fixed and variable costs. This is a classification of costs based on whether the

costs are constant or they change with the changes in the level of output. Fixed

costs are those costs in the production which remain constant irrespective of

whether the level of output is increased or not. For example the rent of a room

will remain constant whether the firm is producing or not. Variable costs on the

other hand are those costs which change in direct proportion with the output. A

good example of variable cost is the cost of labor or direct materials. To produce

more and more output, one will need to use more and more direct materials and

more labor will also be required.

b) Direct and indirect costs. This method of classifying production costs focuses on

the ability to trace the costs to the end product. Direct costs can be seen as

variable cost as per the above discussion. They are those costs which are

incurred in direct proportion with the output level. They are the ones used in

costing the final product because one can easily determine how much was put

into a particular product. For example one can easily determine how much of the

raw materials were put into each unit of output. Indirect costs, also known as

production overheads, are those types of costs which are not easy to quantify in

the final output. The salary paid to production supervisor is a good example as

such expense cannot be easily traced to the final product.

c) Product and period costs. This classification method divides the costs from the

point of view of the end product. Product costs are those costs which are

incurred direct to the production. Such costs include the cost of raw materials

and the cost of direct labor. They are the same costs used to do the product

costing. Period costs on the other hand are those costs which are not closely

related to the product and they are treated as period expenses. Rent for instant is

seem as a periodic expense to be expensed every month other than a product

cost to be absorbed by the end product.

QNS 2

Managerial Accounting 3

According to Collier (2015), to arrive at a valuable decision, one should be armed with

relevant and reliable information. The power of information in the process of decision

making cannot be under estimated. For the Franks to make a decision of whether to

purchase new appliances or not, first they should put into all the available alternatives

which are at their disposal. As per the case study, the couple can outsource the

laundering services to Red Oak Laundry and Dry Cleaning. The company can do the

laundering for the couple including pick-up and delivery for $ 52 per month.

Alternatively, the couple can do the laundry by themselves from Laundromat once per

week. However, under this arrangement, the couple will have to meet the expenses of

the detergent and fabric sheets.

With all this information, the Franks can the compute the cost for each alternative and

determine the one which is less expensive and more convenient to them. The couple is

in business and therefore they should only be interested in the alternative that

maximizes the value of their business.

Decision making utilizes the most current information which is influential to the possible

actions likely to be taken. The cost of the old appliances is not information current and

influential to the decision the couple is facing. The old appliances are no longer working

and their cost is a sunk cost which does not have an impact in the entire decision

concerning appliances (Zsambok, 2014).

QNS 3

There are three options available for the couple in solving the laundering problem. All

the three options and their related costs are discussed below;

Option one

For this option, the Frank can contract the Red Oak Laundry and Dry Cleaning

Company for all their laundry work. The company will do the laundering for the couple

which will include the pick-up and delivery for the cost of $ 52 per month.

Option two: taking clothes to Laundromat

Here the couple will do the laundry themselves from the Laundromat, three mile away

from their facility. The total cost under this option will include the transport cost and the

cost of buying the washing materials such as detergent and fabric sheets. The total cost

will be;

Laundering cost = U$ 8*4.33 =34.64 per month

According to Collier (2015), to arrive at a valuable decision, one should be armed with

relevant and reliable information. The power of information in the process of decision

making cannot be under estimated. For the Franks to make a decision of whether to

purchase new appliances or not, first they should put into all the available alternatives

which are at their disposal. As per the case study, the couple can outsource the

laundering services to Red Oak Laundry and Dry Cleaning. The company can do the

laundering for the couple including pick-up and delivery for $ 52 per month.

Alternatively, the couple can do the laundry by themselves from Laundromat once per

week. However, under this arrangement, the couple will have to meet the expenses of

the detergent and fabric sheets.

With all this information, the Franks can the compute the cost for each alternative and

determine the one which is less expensive and more convenient to them. The couple is

in business and therefore they should only be interested in the alternative that

maximizes the value of their business.

Decision making utilizes the most current information which is influential to the possible

actions likely to be taken. The cost of the old appliances is not information current and

influential to the decision the couple is facing. The old appliances are no longer working

and their cost is a sunk cost which does not have an impact in the entire decision

concerning appliances (Zsambok, 2014).

QNS 3

There are three options available for the couple in solving the laundering problem. All

the three options and their related costs are discussed below;

Option one

For this option, the Frank can contract the Red Oak Laundry and Dry Cleaning

Company for all their laundry work. The company will do the laundering for the couple

which will include the pick-up and delivery for the cost of $ 52 per month.

Option two: taking clothes to Laundromat

Here the couple will do the laundry themselves from the Laundromat, three mile away

from their facility. The total cost under this option will include the transport cost and the

cost of buying the washing materials such as detergent and fabric sheets. The total cost

will be;

Laundering cost = U$ 8*4.33 =34.64 per month

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 4

Transportation

=U$ 0.56 per mile*6 mile (to and fro) = U$ 3.36 per week.

Monthly cost

= 3.36 per week × 4.33 weeks = $ 14.55 per month.

Detergent or fabric sheets per month

= $ 35/3 = U$ 11.66 per month.

Total

Laundry cost =$ 34.64

Transport = $ 14.55

Detergents = $ 11.66

$ 60.85

Option Three: Purchase of appliances.

The last alternative available to Douglas and Pamela Frank is to purchase and install

the laundry machine in their facility. This option comes with a lot of costs associated

with the new appliances. First, the couple has to purchase the appliances, and then

they will incur the transportation cost and the cost of installation. However, some of

these costs will be incurred once and after the laundry machine is up and running, the

monthly costs will be very low. Below is a computation for all the costs under this

arrangement.

Costs

Washer: $420

Dryer: $380

Carriage: $35.

Installation: $43.72.

Power bills costs

Total cost for the dryer will be calculated by considering the cost of energy consumed

per year and then multiplying by the 8 years.

$ 145 × 8 years = $ 1 160

The amount of energy consumed by the washer will be calculated as follows;

Transportation

=U$ 0.56 per mile*6 mile (to and fro) = U$ 3.36 per week.

Monthly cost

= 3.36 per week × 4.33 weeks = $ 14.55 per month.

Detergent or fabric sheets per month

= $ 35/3 = U$ 11.66 per month.

Total

Laundry cost =$ 34.64

Transport = $ 14.55

Detergents = $ 11.66

$ 60.85

Option Three: Purchase of appliances.

The last alternative available to Douglas and Pamela Frank is to purchase and install

the laundry machine in their facility. This option comes with a lot of costs associated

with the new appliances. First, the couple has to purchase the appliances, and then

they will incur the transportation cost and the cost of installation. However, some of

these costs will be incurred once and after the laundry machine is up and running, the

monthly costs will be very low. Below is a computation for all the costs under this

arrangement.

Costs

Washer: $420

Dryer: $380

Carriage: $35.

Installation: $43.72.

Power bills costs

Total cost for the dryer will be calculated by considering the cost of energy consumed

per year and then multiplying by the 8 years.

$ 145 × 8 years = $ 1 160

The amount of energy consumed by the washer will be calculated as follows;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 5

$ 120 × 8 years = $ 960

The power cost of energy consumption for eight year = sum of energy consumption for

eight years

= $ 1 160 + $ 960= $ 2 120

Total cost of purchasing and installing laundry equipment will be;

Washer $ 420

Dryer $ 380

Installation costs $ 43.72

Carriage $ 35

Power bills $ 2 120

Total costs $ 2 998.72

The cost of energy consumption and the cost for purchasing, fright and installation for

one month will be the total cost for eight years divided by the number of months in eight

years

Energy consumption for one month = $ 2 998.72/96 months

= $ 22.08 per month.

This option seems to be the most favorable for the couple. It is cheap compared to the

other two. Although the Franks will have to spend a lot for the purchase and installation

of the laundry machine, the ultimate benefit is high. With this option, the couple will

exercise independency since they will be using their own machine. Apart from saving on

monthly costs, the couple will also save on time used to go for laundering to

Laundromat which is three miles away from their facility. Such time can be dedicated to

offering more quality care to the children and reducing on the cost of employing more

workers to take care for the children.

QNS 4: Considerations for Hiring an Employee

The franks have the ability to accept more children but only if they employ an additional

employee. The appropriateness of this option will be determined by the cost of

employing an additional employee compared to the revenue generated from the

additional children (Tseng, et al., 2014).

Salary expenses

The salary expense for the week will be calculated as;

= U$ 9*40 hours = U$ 360 per week

$ 120 × 8 years = $ 960

The power cost of energy consumption for eight year = sum of energy consumption for

eight years

= $ 1 160 + $ 960= $ 2 120

Total cost of purchasing and installing laundry equipment will be;

Washer $ 420

Dryer $ 380

Installation costs $ 43.72

Carriage $ 35

Power bills $ 2 120

Total costs $ 2 998.72

The cost of energy consumption and the cost for purchasing, fright and installation for

one month will be the total cost for eight years divided by the number of months in eight

years

Energy consumption for one month = $ 2 998.72/96 months

= $ 22.08 per month.

This option seems to be the most favorable for the couple. It is cheap compared to the

other two. Although the Franks will have to spend a lot for the purchase and installation

of the laundry machine, the ultimate benefit is high. With this option, the couple will

exercise independency since they will be using their own machine. Apart from saving on

monthly costs, the couple will also save on time used to go for laundering to

Laundromat which is three miles away from their facility. Such time can be dedicated to

offering more quality care to the children and reducing on the cost of employing more

workers to take care for the children.

QNS 4: Considerations for Hiring an Employee

The franks have the ability to accept more children but only if they employ an additional

employee. The appropriateness of this option will be determined by the cost of

employing an additional employee compared to the revenue generated from the

additional children (Tseng, et al., 2014).

Salary expenses

The salary expense for the week will be calculated as;

= U$ 9*40 hours = U$ 360 per week

Managerial Accounting 6

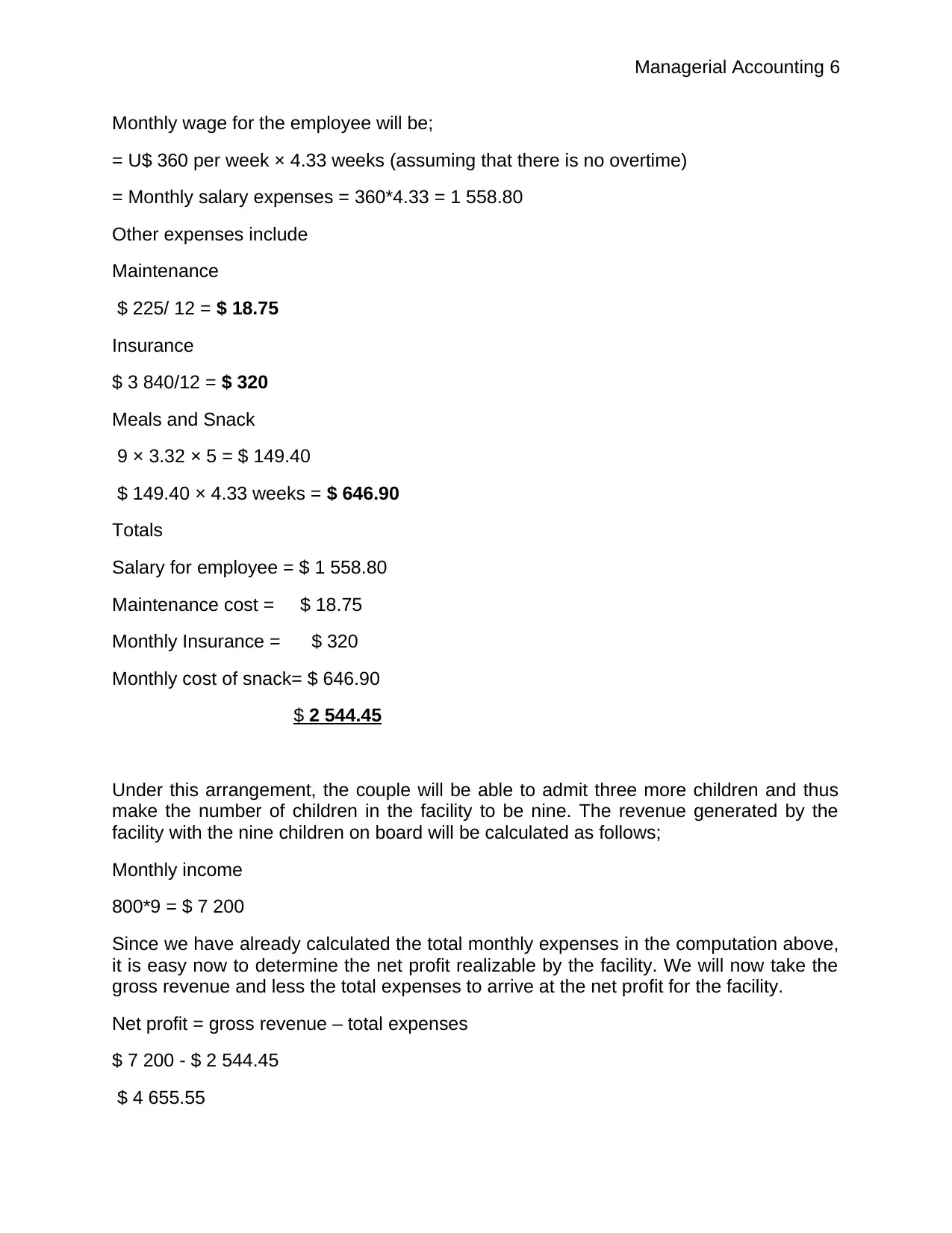

Monthly wage for the employee will be;

= U$ 360 per week × 4.33 weeks (assuming that there is no overtime)

= Monthly salary expenses = 360*4.33 = 1 558.80

Other expenses include

Maintenance

$ 225/ 12 = $ 18.75

Insurance

$ 3 840/12 = $ 320

Meals and Snack

9 × 3.32 × 5 = $ 149.40

$ 149.40 × 4.33 weeks = $ 646.90

Totals

Salary for employee = $ 1 558.80

Maintenance cost = $ 18.75

Monthly Insurance = $ 320

Monthly cost of snack= $ 646.90

$ 2 544.45

Under this arrangement, the couple will be able to admit three more children and thus

make the number of children in the facility to be nine. The revenue generated by the

facility with the nine children on board will be calculated as follows;

Monthly income

800*9 = $ 7 200

Since we have already calculated the total monthly expenses in the computation above,

it is easy now to determine the net profit realizable by the facility. We will now take the

gross revenue and less the total expenses to arrive at the net profit for the facility.

Net profit = gross revenue – total expenses

$ 7 200 - $ 2 544.45

$ 4 655.55

Monthly wage for the employee will be;

= U$ 360 per week × 4.33 weeks (assuming that there is no overtime)

= Monthly salary expenses = 360*4.33 = 1 558.80

Other expenses include

Maintenance

$ 225/ 12 = $ 18.75

Insurance

$ 3 840/12 = $ 320

Meals and Snack

9 × 3.32 × 5 = $ 149.40

$ 149.40 × 4.33 weeks = $ 646.90

Totals

Salary for employee = $ 1 558.80

Maintenance cost = $ 18.75

Monthly Insurance = $ 320

Monthly cost of snack= $ 646.90

$ 2 544.45

Under this arrangement, the couple will be able to admit three more children and thus

make the number of children in the facility to be nine. The revenue generated by the

facility with the nine children on board will be calculated as follows;

Monthly income

800*9 = $ 7 200

Since we have already calculated the total monthly expenses in the computation above,

it is easy now to determine the net profit realizable by the facility. We will now take the

gross revenue and less the total expenses to arrive at the net profit for the facility.

Net profit = gross revenue – total expenses

$ 7 200 - $ 2 544.45

$ 4 655.55

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 7

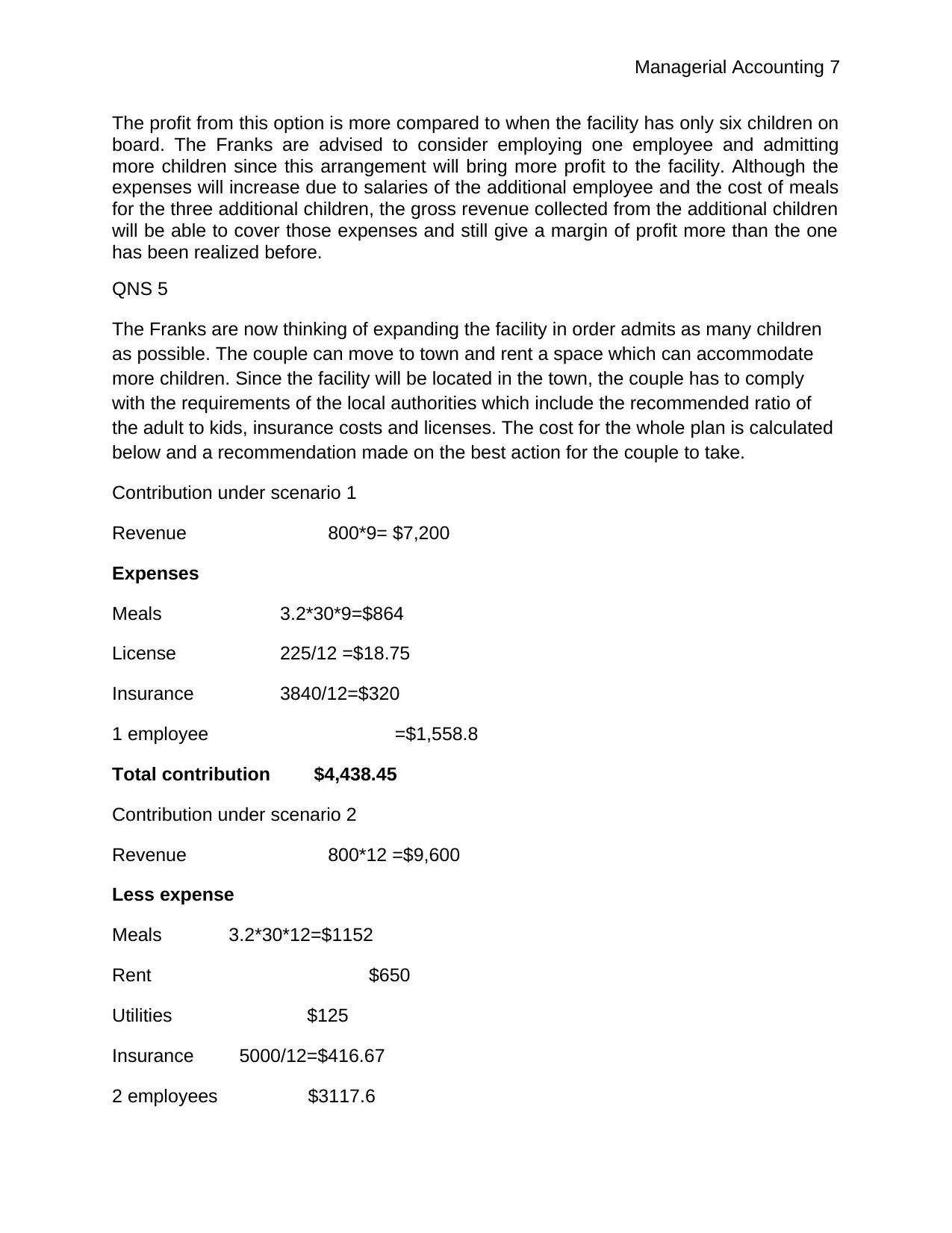

The profit from this option is more compared to when the facility has only six children on

board. The Franks are advised to consider employing one employee and admitting

more children since this arrangement will bring more profit to the facility. Although the

expenses will increase due to salaries of the additional employee and the cost of meals

for the three additional children, the gross revenue collected from the additional children

will be able to cover those expenses and still give a margin of profit more than the one

has been realized before.

QNS 5

The Franks are now thinking of expanding the facility in order admits as many children

as possible. The couple can move to town and rent a space which can accommodate

more children. Since the facility will be located in the town, the couple has to comply

with the requirements of the local authorities which include the recommended ratio of

the adult to kids, insurance costs and licenses. The cost for the whole plan is calculated

below and a recommendation made on the best action for the couple to take.

Contribution under scenario 1

Revenue 800*9= $7,200

Expenses

Meals 3.2*30*9=$864

License 225/12 =$18.75

Insurance 3840/12=$320

1 employee =$1,558.8

Total contribution $4,438.45

Contribution under scenario 2

Revenue 800*12 =$9,600

Less expense

Meals 3.2*30*12=$1152

Rent $650

Utilities $125

Insurance 5000/12=$416.67

2 employees $3117.6

The profit from this option is more compared to when the facility has only six children on

board. The Franks are advised to consider employing one employee and admitting

more children since this arrangement will bring more profit to the facility. Although the

expenses will increase due to salaries of the additional employee and the cost of meals

for the three additional children, the gross revenue collected from the additional children

will be able to cover those expenses and still give a margin of profit more than the one

has been realized before.

QNS 5

The Franks are now thinking of expanding the facility in order admits as many children

as possible. The couple can move to town and rent a space which can accommodate

more children. Since the facility will be located in the town, the couple has to comply

with the requirements of the local authorities which include the recommended ratio of

the adult to kids, insurance costs and licenses. The cost for the whole plan is calculated

below and a recommendation made on the best action for the couple to take.

Contribution under scenario 1

Revenue 800*9= $7,200

Expenses

Meals 3.2*30*9=$864

License 225/12 =$18.75

Insurance 3840/12=$320

1 employee =$1,558.8

Total contribution $4,438.45

Contribution under scenario 2

Revenue 800*12 =$9,600

Less expense

Meals 3.2*30*12=$1152

Rent $650

Utilities $125

Insurance 5000/12=$416.67

2 employees $3117.6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 8

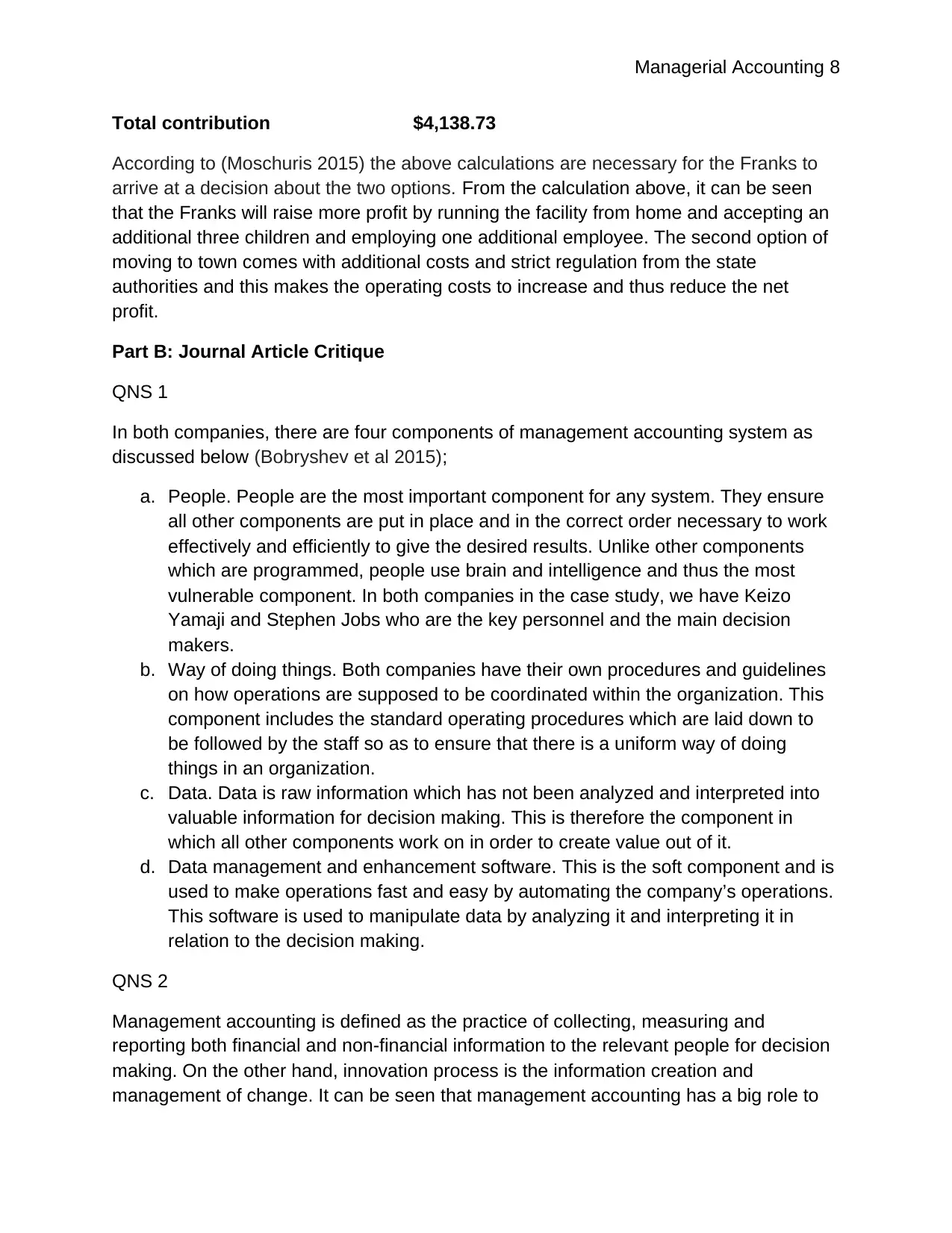

Total contribution $4,138.73

According to (Moschuris 2015) the above calculations are necessary for the Franks to

arrive at a decision about the two options. From the calculation above, it can be seen

that the Franks will raise more profit by running the facility from home and accepting an

additional three children and employing one additional employee. The second option of

moving to town comes with additional costs and strict regulation from the state

authorities and this makes the operating costs to increase and thus reduce the net

profit.

Part B: Journal Article Critique

QNS 1

In both companies, there are four components of management accounting system as

discussed below (Bobryshev et al 2015);

a. People. People are the most important component for any system. They ensure

all other components are put in place and in the correct order necessary to work

effectively and efficiently to give the desired results. Unlike other components

which are programmed, people use brain and intelligence and thus the most

vulnerable component. In both companies in the case study, we have Keizo

Yamaji and Stephen Jobs who are the key personnel and the main decision

makers.

b. Way of doing things. Both companies have their own procedures and guidelines

on how operations are supposed to be coordinated within the organization. This

component includes the standard operating procedures which are laid down to

be followed by the staff so as to ensure that there is a uniform way of doing

things in an organization.

c. Data. Data is raw information which has not been analyzed and interpreted into

valuable information for decision making. This is therefore the component in

which all other components work on in order to create value out of it.

d. Data management and enhancement software. This is the soft component and is

used to make operations fast and easy by automating the company’s operations.

This software is used to manipulate data by analyzing it and interpreting it in

relation to the decision making.

QNS 2

Management accounting is defined as the practice of collecting, measuring and

reporting both financial and non-financial information to the relevant people for decision

making. On the other hand, innovation process is the information creation and

management of change. It can be seen that management accounting has a big role to

Total contribution $4,138.73

According to (Moschuris 2015) the above calculations are necessary for the Franks to

arrive at a decision about the two options. From the calculation above, it can be seen

that the Franks will raise more profit by running the facility from home and accepting an

additional three children and employing one additional employee. The second option of

moving to town comes with additional costs and strict regulation from the state

authorities and this makes the operating costs to increase and thus reduce the net

profit.

Part B: Journal Article Critique

QNS 1

In both companies, there are four components of management accounting system as

discussed below (Bobryshev et al 2015);

a. People. People are the most important component for any system. They ensure

all other components are put in place and in the correct order necessary to work

effectively and efficiently to give the desired results. Unlike other components

which are programmed, people use brain and intelligence and thus the most

vulnerable component. In both companies in the case study, we have Keizo

Yamaji and Stephen Jobs who are the key personnel and the main decision

makers.

b. Way of doing things. Both companies have their own procedures and guidelines

on how operations are supposed to be coordinated within the organization. This

component includes the standard operating procedures which are laid down to

be followed by the staff so as to ensure that there is a uniform way of doing

things in an organization.

c. Data. Data is raw information which has not been analyzed and interpreted into

valuable information for decision making. This is therefore the component in

which all other components work on in order to create value out of it.

d. Data management and enhancement software. This is the soft component and is

used to make operations fast and easy by automating the company’s operations.

This software is used to manipulate data by analyzing it and interpreting it in

relation to the decision making.

QNS 2

Management accounting is defined as the practice of collecting, measuring and

reporting both financial and non-financial information to the relevant people for decision

making. On the other hand, innovation process is the information creation and

management of change. It can be seen that management accounting has a big role to

Managerial Accounting 9

play in the innovation process. While innovation is all about managing change and

taking the necessary response towards that change, management accounting will be

responsible to collect and analyze all the necessary information to justify the need to

make changes on the various management processes (Busco, Caglio and Scapens

2015).

In the Canon Company, management accounting has been used to measure and report

all the costs associated with the Mini Copier and an innovation has been initiated to

minimize such costs in order to maximize on the profits. For Apple Company,

management accounting has been used to provide information about quality and sizes

of the computers. As a results, an innovation is undertaken which reduced the size and

improved the efficiency of computers for the company (Nonaka and Kenney ,1991).

QNS 3

From the Canon Company, it is seen that it is necessary to diversify activities of the

company to achieve growth. In order to diversify the activities of any company,

management accountants need to be in the front line and provide the relevant

information about the products. Information about product cost of production, product

profit contribution and the market demand will be the key in deciding whether or not to

diversify company products. Canon also keeps on improving the existing products to

increase its efficiency and reduce the operation costs. All the relevant information to

make these decisions is provided by the management accountants.

For Apple Company, most of the improvements made in their products are as a result of

team work and brain storming. Although management accounting information is

indispensable in such improvements, the key emphasis is placed on the ability to work

as a team and share various ideas and acting on them. Also for Apple Company, its

success is associated with the strong leadership from Stephen Jobs. The lesson to be

learned from both companies is that management accountants should provide accurate

and reliable information which is going to be relevant in making company’s decisions.

They also need to embrace team work and always be open to taking ideas from other

stakeholders of the company and above all exercise good leadership skills to their

juniors (Nonaka and Kenney ,1991).

play in the innovation process. While innovation is all about managing change and

taking the necessary response towards that change, management accounting will be

responsible to collect and analyze all the necessary information to justify the need to

make changes on the various management processes (Busco, Caglio and Scapens

2015).

In the Canon Company, management accounting has been used to measure and report

all the costs associated with the Mini Copier and an innovation has been initiated to

minimize such costs in order to maximize on the profits. For Apple Company,

management accounting has been used to provide information about quality and sizes

of the computers. As a results, an innovation is undertaken which reduced the size and

improved the efficiency of computers for the company (Nonaka and Kenney ,1991).

QNS 3

From the Canon Company, it is seen that it is necessary to diversify activities of the

company to achieve growth. In order to diversify the activities of any company,

management accountants need to be in the front line and provide the relevant

information about the products. Information about product cost of production, product

profit contribution and the market demand will be the key in deciding whether or not to

diversify company products. Canon also keeps on improving the existing products to

increase its efficiency and reduce the operation costs. All the relevant information to

make these decisions is provided by the management accountants.

For Apple Company, most of the improvements made in their products are as a result of

team work and brain storming. Although management accounting information is

indispensable in such improvements, the key emphasis is placed on the ability to work

as a team and share various ideas and acting on them. Also for Apple Company, its

success is associated with the strong leadership from Stephen Jobs. The lesson to be

learned from both companies is that management accountants should provide accurate

and reliable information which is going to be relevant in making company’s decisions.

They also need to embrace team work and always be open to taking ideas from other

stakeholders of the company and above all exercise good leadership skills to their

juniors (Nonaka and Kenney ,1991).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 10

References

Bobryshev, A.N., Yakovenko, V.S., Tunin, S.A., Germanova, V.S. and Glushko, A.Y.,

2015. The Concept of Management Accounting in Crisis Conditions. Journal of

Advanced Research in Law and Economics, 6(3 (13)), p.520.

Busco, C., Caglio, A. and Scapens, R.W., 2015. Management and accounting

innovations: reflecting on what they are and why they are adopted. Journal of

Management & Governance, 19(3), pp.495-524

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Moschuris, S.J., 2015. Decision-making criteria in tactical make-or-buy issues: an

empirical analysis. EuroMed Journal of Business, 10(1), pp.2-20.

Nonaka and Kenney ,1991. “Towards a new theory of innovation management: A case

study comparing Canon, Inc. and Apple Computer, Inc.”, Journal of Engineering and

Technology Management, 8, p. 67-83.

Zsambok, C.E., 2014. Naturalistic decision making: where are we now?. In Naturalistic

decision making (pp. 23-36). Psychology Press

Abernathy, W., 1978. The Productivity Dilemma: Roadblock

to Innovation in the Automobile Industry. Johns Hopkins,

Baltimore, MD.

References

Bobryshev, A.N., Yakovenko, V.S., Tunin, S.A., Germanova, V.S. and Glushko, A.Y.,

2015. The Concept of Management Accounting in Crisis Conditions. Journal of

Advanced Research in Law and Economics, 6(3 (13)), p.520.

Busco, C., Caglio, A. and Scapens, R.W., 2015. Management and accounting

innovations: reflecting on what they are and why they are adopted. Journal of

Management & Governance, 19(3), pp.495-524

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Moschuris, S.J., 2015. Decision-making criteria in tactical make-or-buy issues: an

empirical analysis. EuroMed Journal of Business, 10(1), pp.2-20.

Nonaka and Kenney ,1991. “Towards a new theory of innovation management: A case

study comparing Canon, Inc. and Apple Computer, Inc.”, Journal of Engineering and

Technology Management, 8, p. 67-83.

Zsambok, C.E., 2014. Naturalistic decision making: where are we now?. In Naturalistic

decision making (pp. 23-36). Psychology Press

Abernathy, W., 1978. The Productivity Dilemma: Roadblock

to Innovation in the Automobile Industry. Johns Hopkins,

Baltimore, MD.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 11

Aoki, M., 1989. Information, Incentives and Bargaining in the

Japanese Economy. Cambridge University Press,

Cambridge.

Baumol, W. and Benhabib, J., 1989. Chaos, sign)ficance, mechanisms, and economic

applications. J. Econ. Perspect., 3(1): 77-105.

.

Daft, R. and Weick, K., 1984. Toward a model of organizations as interpretation

systems.

Acad. Manage. Rev., 9(2): 284-295.

Florida, R. and Kenney, M., 1990. The Breakthrough Illusion:

Corporate America'.s Inability to Link Production and

Innovation. Basic, New York.

Nonaka, 1. and Takeuchi, H., 1985. Managing the new

product development process:

Kenney, M., 1986. Some observations on the structure of

the U.S. and Japanese biotechnology industries.

Hitotsubashi Bus. Rev., 34 (December): 20 37 (in

Japanese).

Kodama, F., 1988. Japanese innovation in mechatronics

technology. Sci. Public Policy, 13 (1): 44 51.

Nonaka, 1., 1987. Managing the firm as an information

creation process. Working paper, Institute of Business

Research, Hitotsubashi University, January.

Nonaka, 1., 1988a. Creating organizational order out of chaos: Self-renewal in

Japanese firms.

Calif Manage. Rev., 30(3).

Aoki, M., 1989. Information, Incentives and Bargaining in the

Japanese Economy. Cambridge University Press,

Cambridge.

Baumol, W. and Benhabib, J., 1989. Chaos, sign)ficance, mechanisms, and economic

applications. J. Econ. Perspect., 3(1): 77-105.

.

Daft, R. and Weick, K., 1984. Toward a model of organizations as interpretation

systems.

Acad. Manage. Rev., 9(2): 284-295.

Florida, R. and Kenney, M., 1990. The Breakthrough Illusion:

Corporate America'.s Inability to Link Production and

Innovation. Basic, New York.

Nonaka, 1. and Takeuchi, H., 1985. Managing the new

product development process:

Kenney, M., 1986. Some observations on the structure of

the U.S. and Japanese biotechnology industries.

Hitotsubashi Bus. Rev., 34 (December): 20 37 (in

Japanese).

Kodama, F., 1988. Japanese innovation in mechatronics

technology. Sci. Public Policy, 13 (1): 44 51.

Nonaka, 1., 1987. Managing the firm as an information

creation process. Working paper, Institute of Business

Research, Hitotsubashi University, January.

Nonaka, 1., 1988a. Creating organizational order out of chaos: Self-renewal in

Japanese firms.

Calif Manage. Rev., 30(3).

Managerial Accounting 12

Nonaka, 1., 1988b. Toward middle-up-down management: Accelerating information

creation.

Sloan Manage. Rev., (Spring): 9-18.

Prigogine, l., 1980. From Being to Becoming. Freeman, San Francisco, CA.

Prigogine, l. and Stengers, I., 1984. Order Out of Chaos. New

Science Library, Boulder, CO. Quinn, W., 1985. Managing

innovation: Controlled chaos. Harv. Bus. Rev., (May-June):

73 80

Rose, H. and Rose, S. (Eds.), 1976. The Political Economy of

Science. Macmillan, London. Saito, K., 1984. Personal

interview by I. Nonaka (November 28).

Simon, H., 1969. The Science of the Artificial. Free Press, New York.

Takeuchi, H. and Nonaka, I., 1986. The new product

development game. Harv. Bus. Rev., 64 (1): 1.17 146

Nonaka, 1., 1988b. Toward middle-up-down management: Accelerating information

creation.

Sloan Manage. Rev., (Spring): 9-18.

Prigogine, l., 1980. From Being to Becoming. Freeman, San Francisco, CA.

Prigogine, l. and Stengers, I., 1984. Order Out of Chaos. New

Science Library, Boulder, CO. Quinn, W., 1985. Managing

innovation: Controlled chaos. Harv. Bus. Rev., (May-June):

73 80

Rose, H. and Rose, S. (Eds.), 1976. The Political Economy of

Science. Macmillan, London. Saito, K., 1984. Personal

interview by I. Nonaka (November 28).

Simon, H., 1969. The Science of the Artificial. Free Press, New York.

Takeuchi, H. and Nonaka, I., 1986. The new product

development game. Harv. Bus. Rev., 64 (1): 1.17 146

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.