Financial Statement Analysis and Cash Flow: An Accounting Case Study

VerifiedAdded on 2023/01/18

|9

|1880

|23

Case Study

AI Summary

This accounting case study provides a detailed analysis of financial statements, including the balance sheet, statement of changes in equity, and profit and loss account. It covers the preparation of these statements and explains the treatment of leased assets in the balance sheet. The study further examines cash flow statements, including the classification of cash flows from investing and financing activities, and discusses the limitations of cash flow statements. The case study presents calculations and interpretations for each component, offering a comprehensive understanding of financial statement analysis. References to accounting standards and relevant literature are also included, providing a robust framework for understanding the concepts discussed.

Accounting Case

Study/Analysis

Study/Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a. Statement of balance sheet .....................................................................................................1

b. preparation of the change in equity statement and income statement ....................................2

c. Reasons for showing a leased asset in the balance sheet even in case the asset is not owned

legally..........................................................................................................................................2

Question 2........................................................................................................................................3

a. Framing cash flow using investing activities .........................................................................3

b. Preparing cash flow using financing activity .........................................................................4

c. Limitation of the cash flow statement ....................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a. Statement of balance sheet .....................................................................................................1

b. preparation of the change in equity statement and income statement ....................................2

c. Reasons for showing a leased asset in the balance sheet even in case the asset is not owned

legally..........................................................................................................................................2

Question 2........................................................................................................................................3

a. Framing cash flow using investing activities .........................................................................3

b. Preparing cash flow using financing activity .........................................................................4

c. Limitation of the cash flow statement ....................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

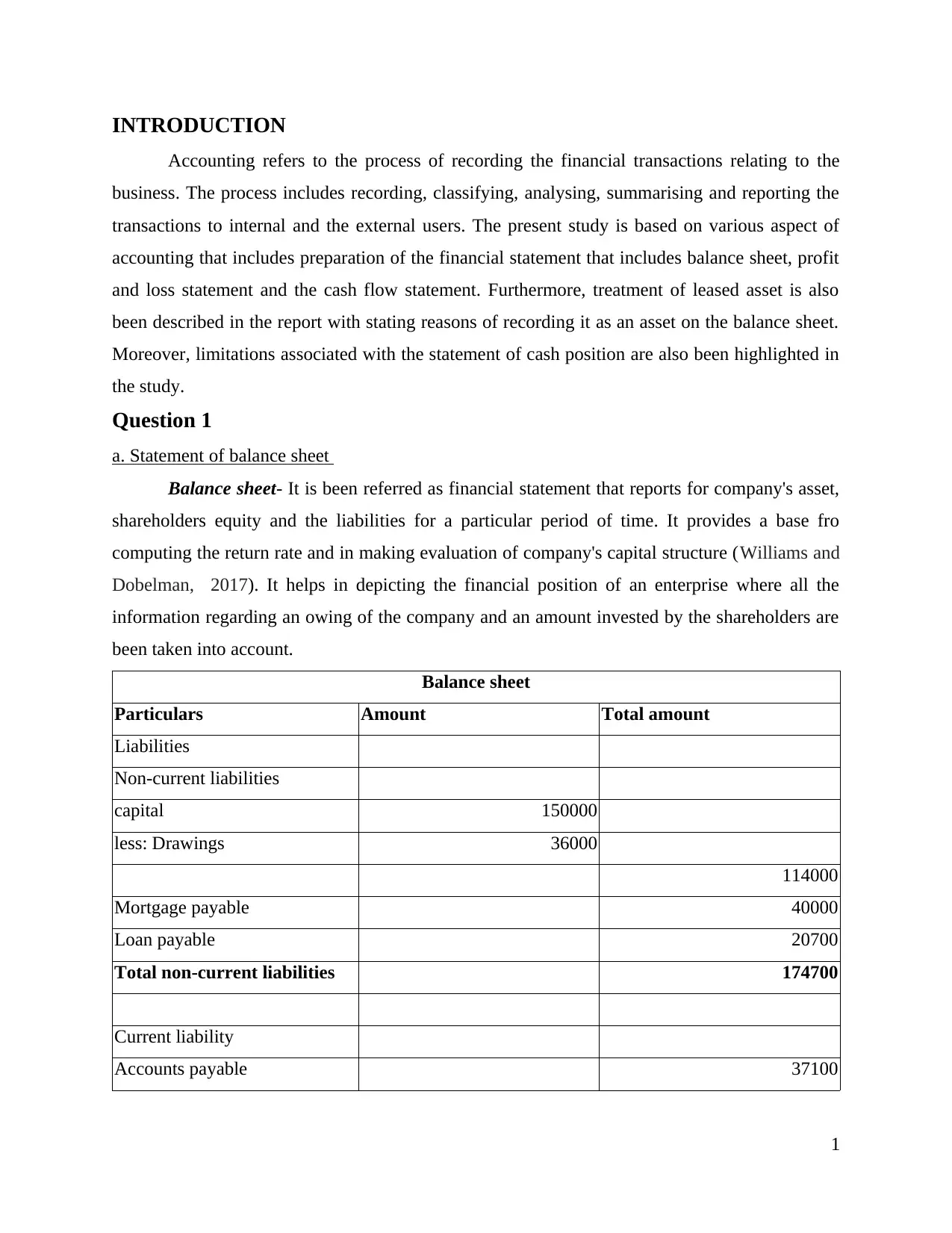

INTRODUCTION

Accounting refers to the process of recording the financial transactions relating to the

business. The process includes recording, classifying, analysing, summarising and reporting the

transactions to internal and the external users. The present study is based on various aspect of

accounting that includes preparation of the financial statement that includes balance sheet, profit

and loss statement and the cash flow statement. Furthermore, treatment of leased asset is also

been described in the report with stating reasons of recording it as an asset on the balance sheet.

Moreover, limitations associated with the statement of cash position are also been highlighted in

the study.

Question 1

a. Statement of balance sheet

Balance sheet- It is been referred as financial statement that reports for company's asset,

shareholders equity and the liabilities for a particular period of time. It provides a base fro

computing the return rate and in making evaluation of company's capital structure (Williams and

Dobelman, 2017). It helps in depicting the financial position of an enterprise where all the

information regarding an owing of the company and an amount invested by the shareholders are

been taken into account.

Balance sheet

Particulars Amount Total amount

Liabilities

Non-current liabilities

capital 150000

less: Drawings 36000

114000

Mortgage payable 40000

Loan payable 20700

Total non-current liabilities 174700

Current liability

Accounts payable 37100

1

Accounting refers to the process of recording the financial transactions relating to the

business. The process includes recording, classifying, analysing, summarising and reporting the

transactions to internal and the external users. The present study is based on various aspect of

accounting that includes preparation of the financial statement that includes balance sheet, profit

and loss statement and the cash flow statement. Furthermore, treatment of leased asset is also

been described in the report with stating reasons of recording it as an asset on the balance sheet.

Moreover, limitations associated with the statement of cash position are also been highlighted in

the study.

Question 1

a. Statement of balance sheet

Balance sheet- It is been referred as financial statement that reports for company's asset,

shareholders equity and the liabilities for a particular period of time. It provides a base fro

computing the return rate and in making evaluation of company's capital structure (Williams and

Dobelman, 2017). It helps in depicting the financial position of an enterprise where all the

information regarding an owing of the company and an amount invested by the shareholders are

been taken into account.

Balance sheet

Particulars Amount Total amount

Liabilities

Non-current liabilities

capital 150000

less: Drawings 36000

114000

Mortgage payable 40000

Loan payable 20700

Total non-current liabilities 174700

Current liability

Accounts payable 37100

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

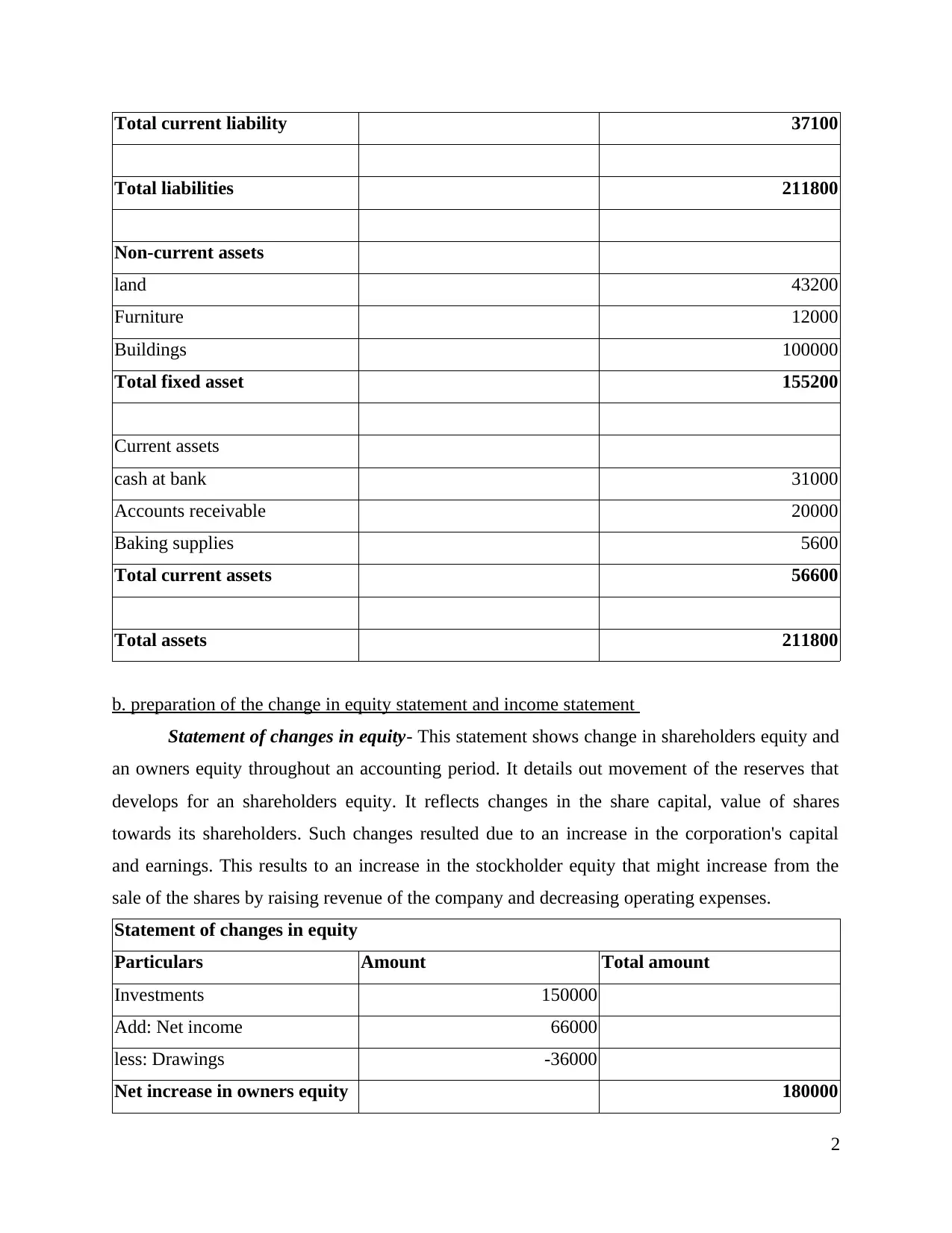

Total current liability 37100

Total liabilities 211800

Non-current assets

land 43200

Furniture 12000

Buildings 100000

Total fixed asset 155200

Current assets

cash at bank 31000

Accounts receivable 20000

Baking supplies 5600

Total current assets 56600

Total assets 211800

b. preparation of the change in equity statement and income statement

Statement of changes in equity- This statement shows change in shareholders equity and

an owners equity throughout an accounting period. It details out movement of the reserves that

develops for an shareholders equity. It reflects changes in the share capital, value of shares

towards its shareholders. Such changes resulted due to an increase in the corporation's capital

and earnings. This results to an increase in the stockholder equity that might increase from the

sale of the shares by raising revenue of the company and decreasing operating expenses.

Statement of changes in equity

Particulars Amount Total amount

Investments 150000

Add: Net income 66000

less: Drawings -36000

Net increase in owners equity 180000

2

Total liabilities 211800

Non-current assets

land 43200

Furniture 12000

Buildings 100000

Total fixed asset 155200

Current assets

cash at bank 31000

Accounts receivable 20000

Baking supplies 5600

Total current assets 56600

Total assets 211800

b. preparation of the change in equity statement and income statement

Statement of changes in equity- This statement shows change in shareholders equity and

an owners equity throughout an accounting period. It details out movement of the reserves that

develops for an shareholders equity. It reflects changes in the share capital, value of shares

towards its shareholders. Such changes resulted due to an increase in the corporation's capital

and earnings. This results to an increase in the stockholder equity that might increase from the

sale of the shares by raising revenue of the company and decreasing operating expenses.

Statement of changes in equity

Particulars Amount Total amount

Investments 150000

Add: Net income 66000

less: Drawings -36000

Net increase in owners equity 180000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

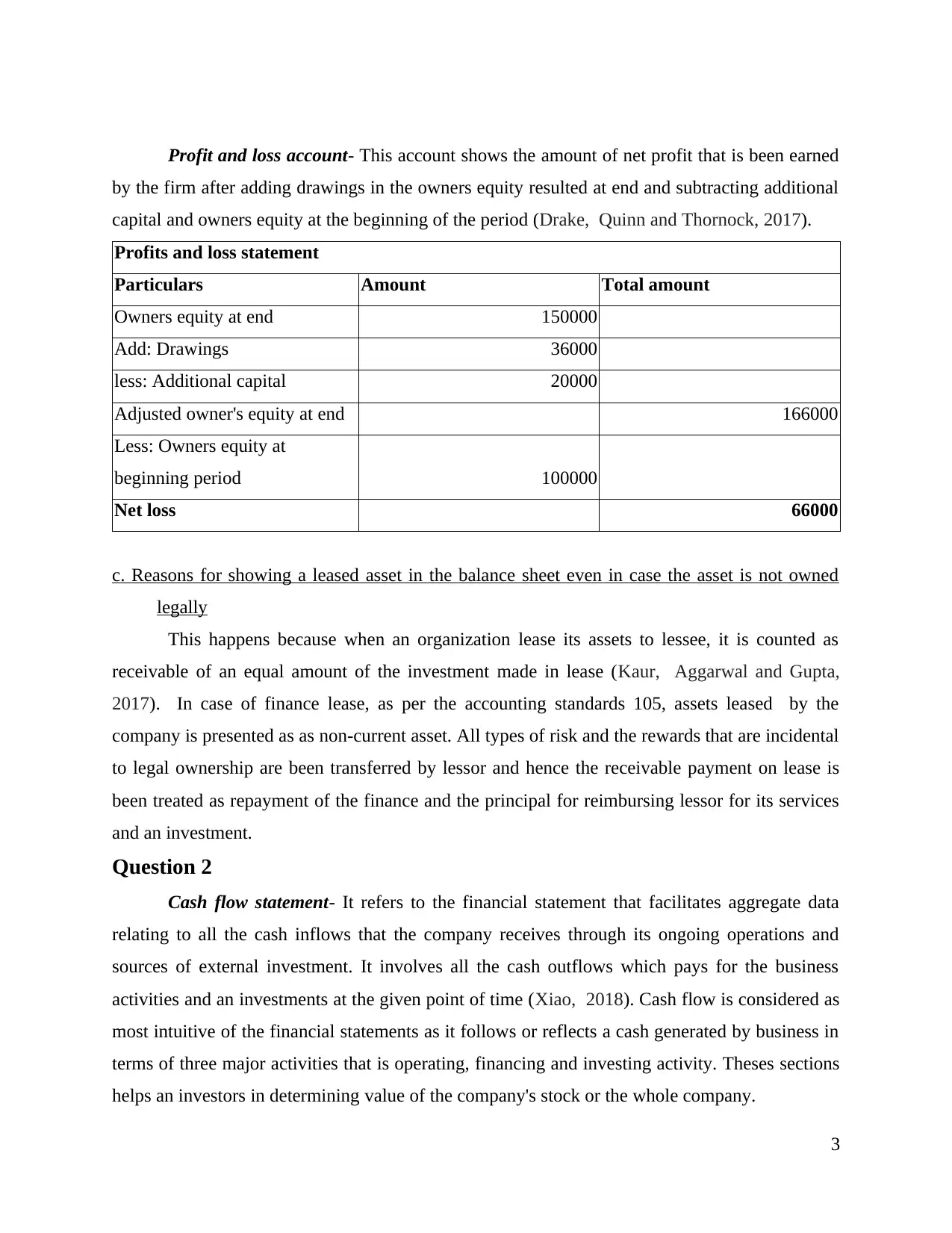

Profit and loss account- This account shows the amount of net profit that is been earned

by the firm after adding drawings in the owners equity resulted at end and subtracting additional

capital and owners equity at the beginning of the period (Drake, Quinn and Thornock, 2017).

Profits and loss statement

Particulars Amount Total amount

Owners equity at end 150000

Add: Drawings 36000

less: Additional capital 20000

Adjusted owner's equity at end 166000

Less: Owners equity at

beginning period 100000

Net loss 66000

c. Reasons for showing a leased asset in the balance sheet even in case the asset is not owned

legally

This happens because when an organization lease its assets to lessee, it is counted as

receivable of an equal amount of the investment made in lease (Kaur, Aggarwal and Gupta,

2017). In case of finance lease, as per the accounting standards 105, assets leased by the

company is presented as as non-current asset. All types of risk and the rewards that are incidental

to legal ownership are been transferred by lessor and hence the receivable payment on lease is

been treated as repayment of the finance and the principal for reimbursing lessor for its services

and an investment.

Question 2

Cash flow statement- It refers to the financial statement that facilitates aggregate data

relating to all the cash inflows that the company receives through its ongoing operations and

sources of external investment. It involves all the cash outflows which pays for the business

activities and an investments at the given point of time (Xiao, 2018). Cash flow is considered as

most intuitive of the financial statements as it follows or reflects a cash generated by business in

terms of three major activities that is operating, financing and investing activity. Theses sections

helps an investors in determining value of the company's stock or the whole company.

3

by the firm after adding drawings in the owners equity resulted at end and subtracting additional

capital and owners equity at the beginning of the period (Drake, Quinn and Thornock, 2017).

Profits and loss statement

Particulars Amount Total amount

Owners equity at end 150000

Add: Drawings 36000

less: Additional capital 20000

Adjusted owner's equity at end 166000

Less: Owners equity at

beginning period 100000

Net loss 66000

c. Reasons for showing a leased asset in the balance sheet even in case the asset is not owned

legally

This happens because when an organization lease its assets to lessee, it is counted as

receivable of an equal amount of the investment made in lease (Kaur, Aggarwal and Gupta,

2017). In case of finance lease, as per the accounting standards 105, assets leased by the

company is presented as as non-current asset. All types of risk and the rewards that are incidental

to legal ownership are been transferred by lessor and hence the receivable payment on lease is

been treated as repayment of the finance and the principal for reimbursing lessor for its services

and an investment.

Question 2

Cash flow statement- It refers to the financial statement that facilitates aggregate data

relating to all the cash inflows that the company receives through its ongoing operations and

sources of external investment. It involves all the cash outflows which pays for the business

activities and an investments at the given point of time (Xiao, 2018). Cash flow is considered as

most intuitive of the financial statements as it follows or reflects a cash generated by business in

terms of three major activities that is operating, financing and investing activity. Theses sections

helps an investors in determining value of the company's stock or the whole company.

3

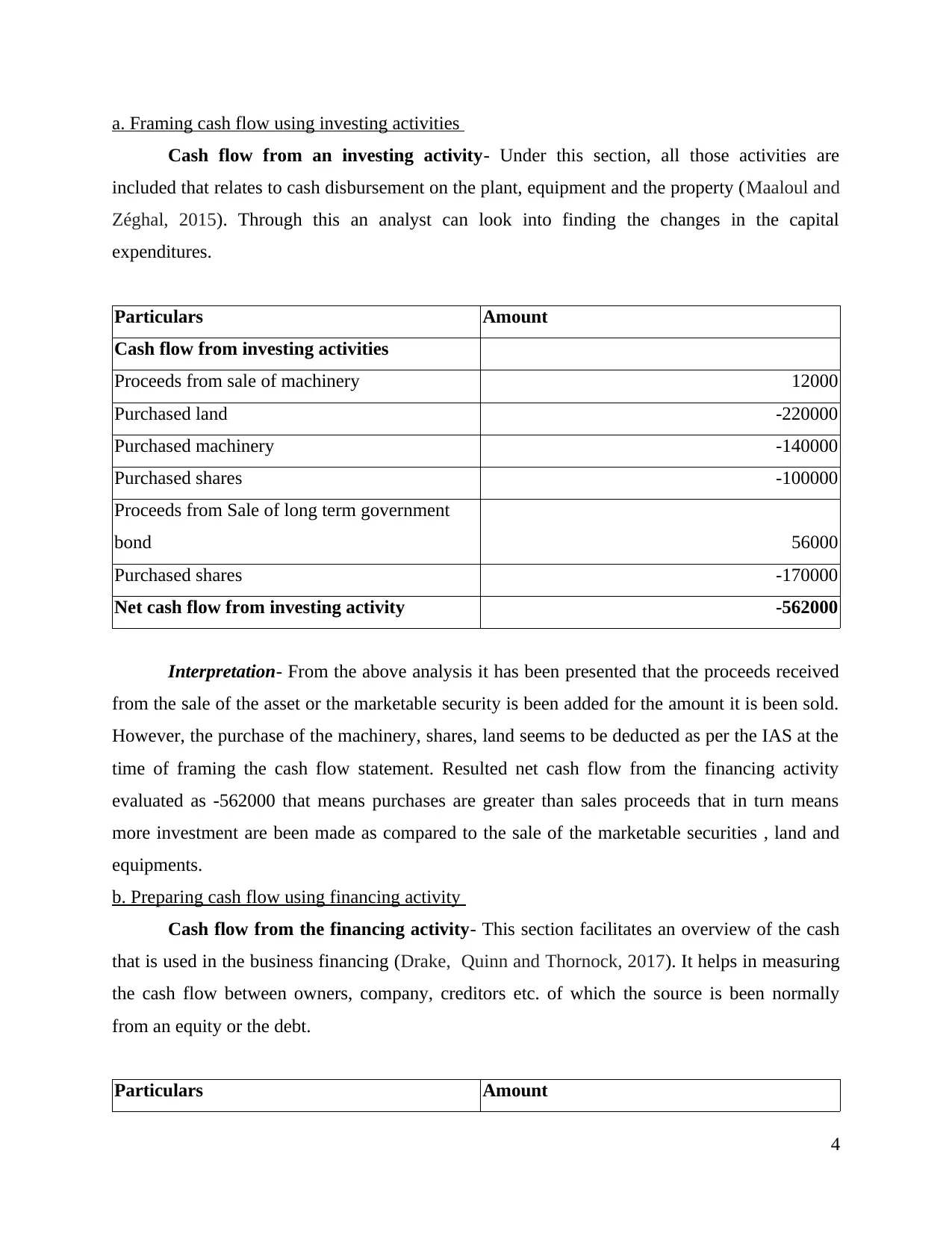

a. Framing cash flow using investing activities

Cash flow from an investing activity- Under this section, all those activities are

included that relates to cash disbursement on the plant, equipment and the property (Maaloul and

Zéghal, 2015). Through this an analyst can look into finding the changes in the capital

expenditures.

Particulars Amount

Cash flow from investing activities

Proceeds from sale of machinery 12000

Purchased land -220000

Purchased machinery -140000

Purchased shares -100000

Proceeds from Sale of long term government

bond 56000

Purchased shares -170000

Net cash flow from investing activity -562000

Interpretation- From the above analysis it has been presented that the proceeds received

from the sale of the asset or the marketable security is been added for the amount it is been sold.

However, the purchase of the machinery, shares, land seems to be deducted as per the IAS at the

time of framing the cash flow statement. Resulted net cash flow from the financing activity

evaluated as -562000 that means purchases are greater than sales proceeds that in turn means

more investment are been made as compared to the sale of the marketable securities , land and

equipments.

b. Preparing cash flow using financing activity

Cash flow from the financing activity- This section facilitates an overview of the cash

that is used in the business financing (Drake, Quinn and Thornock, 2017). It helps in measuring

the cash flow between owners, company, creditors etc. of which the source is been normally

from an equity or the debt.

Particulars Amount

4

Cash flow from an investing activity- Under this section, all those activities are

included that relates to cash disbursement on the plant, equipment and the property (Maaloul and

Zéghal, 2015). Through this an analyst can look into finding the changes in the capital

expenditures.

Particulars Amount

Cash flow from investing activities

Proceeds from sale of machinery 12000

Purchased land -220000

Purchased machinery -140000

Purchased shares -100000

Proceeds from Sale of long term government

bond 56000

Purchased shares -170000

Net cash flow from investing activity -562000

Interpretation- From the above analysis it has been presented that the proceeds received

from the sale of the asset or the marketable security is been added for the amount it is been sold.

However, the purchase of the machinery, shares, land seems to be deducted as per the IAS at the

time of framing the cash flow statement. Resulted net cash flow from the financing activity

evaluated as -562000 that means purchases are greater than sales proceeds that in turn means

more investment are been made as compared to the sale of the marketable securities , land and

equipments.

b. Preparing cash flow using financing activity

Cash flow from the financing activity- This section facilitates an overview of the cash

that is used in the business financing (Drake, Quinn and Thornock, 2017). It helps in measuring

the cash flow between owners, company, creditors etc. of which the source is been normally

from an equity or the debt.

Particulars Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

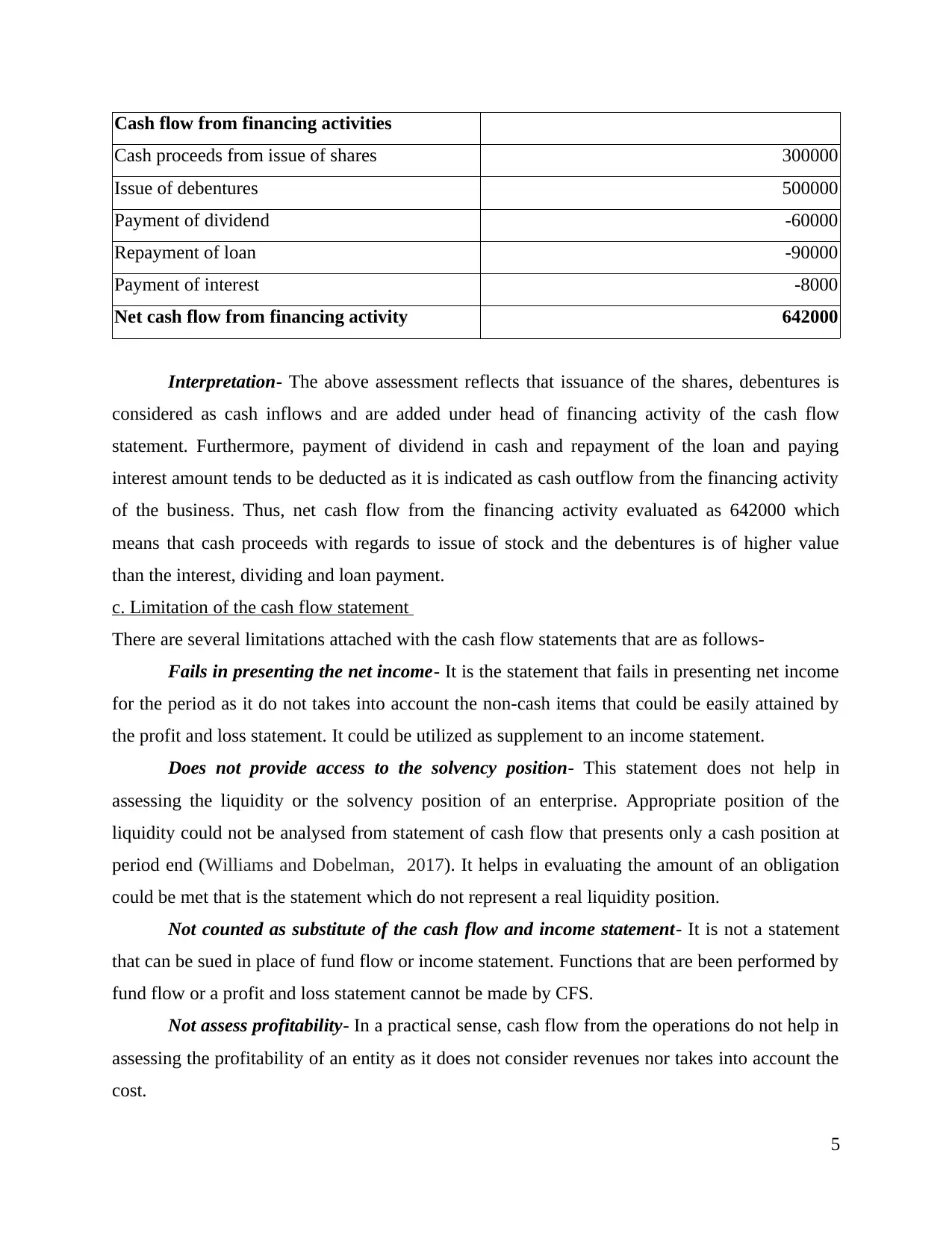

Cash flow from financing activities

Cash proceeds from issue of shares 300000

Issue of debentures 500000

Payment of dividend -60000

Repayment of loan -90000

Payment of interest -8000

Net cash flow from financing activity 642000

Interpretation- The above assessment reflects that issuance of the shares, debentures is

considered as cash inflows and are added under head of financing activity of the cash flow

statement. Furthermore, payment of dividend in cash and repayment of the loan and paying

interest amount tends to be deducted as it is indicated as cash outflow from the financing activity

of the business. Thus, net cash flow from the financing activity evaluated as 642000 which

means that cash proceeds with regards to issue of stock and the debentures is of higher value

than the interest, dividing and loan payment.

c. Limitation of the cash flow statement

There are several limitations attached with the cash flow statements that are as follows-

Fails in presenting the net income- It is the statement that fails in presenting net income

for the period as it do not takes into account the non-cash items that could be easily attained by

the profit and loss statement. It could be utilized as supplement to an income statement.

Does not provide access to the solvency position- This statement does not help in

assessing the liquidity or the solvency position of an enterprise. Appropriate position of the

liquidity could not be analysed from statement of cash flow that presents only a cash position at

period end (Williams and Dobelman, 2017). It helps in evaluating the amount of an obligation

could be met that is the statement which do not represent a real liquidity position.

Not counted as substitute of the cash flow and income statement- It is not a statement

that can be sued in place of fund flow or income statement. Functions that are been performed by

fund flow or a profit and loss statement cannot be made by CFS.

Not assess profitability- In a practical sense, cash flow from the operations do not help in

assessing the profitability of an entity as it does not consider revenues nor takes into account the

cost.

5

Cash proceeds from issue of shares 300000

Issue of debentures 500000

Payment of dividend -60000

Repayment of loan -90000

Payment of interest -8000

Net cash flow from financing activity 642000

Interpretation- The above assessment reflects that issuance of the shares, debentures is

considered as cash inflows and are added under head of financing activity of the cash flow

statement. Furthermore, payment of dividend in cash and repayment of the loan and paying

interest amount tends to be deducted as it is indicated as cash outflow from the financing activity

of the business. Thus, net cash flow from the financing activity evaluated as 642000 which

means that cash proceeds with regards to issue of stock and the debentures is of higher value

than the interest, dividing and loan payment.

c. Limitation of the cash flow statement

There are several limitations attached with the cash flow statements that are as follows-

Fails in presenting the net income- It is the statement that fails in presenting net income

for the period as it do not takes into account the non-cash items that could be easily attained by

the profit and loss statement. It could be utilized as supplement to an income statement.

Does not provide access to the solvency position- This statement does not help in

assessing the liquidity or the solvency position of an enterprise. Appropriate position of the

liquidity could not be analysed from statement of cash flow that presents only a cash position at

period end (Williams and Dobelman, 2017). It helps in evaluating the amount of an obligation

could be met that is the statement which do not represent a real liquidity position.

Not counted as substitute of the cash flow and income statement- It is not a statement

that can be sued in place of fund flow or income statement. Functions that are been performed by

fund flow or a profit and loss statement cannot be made by CFS.

Not assess profitability- In a practical sense, cash flow from the operations do not help in

assessing the profitability of an entity as it does not consider revenues nor takes into account the

cost.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Not conform with companies act- The provisions that are been made by companies act

are in conformity with the income and the balance sheet with respect to cash flow that is been

prepared in accordance with AS 3.

Does not analyse future cash position- Since the CFS is been framed based on historical

cost and it do not help in knowing or estimating future cash flows.

Not facilitate inter-industry contrast- Since this statement do not measure an economic

efficiency of an entity as compared to the other industry is not seen as possible. For example-

company having low amount of capital investment will be having less amount of cash flow in

comparison to other forms that has more and more investment in capital having the higher value

of the cash flow.

CONCLUSION

By summing up the above report it has been analysed that financial statement helps in

knowing the financial position, profitability and the cash position of an entity. Though, there are

various limitation attached to these statements but it is counted as the best way of reporting to

users and helping them in making appropriate or suitable decisions.

6

are in conformity with the income and the balance sheet with respect to cash flow that is been

prepared in accordance with AS 3.

Does not analyse future cash position- Since the CFS is been framed based on historical

cost and it do not help in knowing or estimating future cash flows.

Not facilitate inter-industry contrast- Since this statement do not measure an economic

efficiency of an entity as compared to the other industry is not seen as possible. For example-

company having low amount of capital investment will be having less amount of cash flow in

comparison to other forms that has more and more investment in capital having the higher value

of the cash flow.

CONCLUSION

By summing up the above report it has been analysed that financial statement helps in

knowing the financial position, profitability and the cash position of an entity. Though, there are

various limitation attached to these statements but it is counted as the best way of reporting to

users and helping them in making appropriate or suitable decisions.

6

REFERENCES

Books and Journals

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from EDGAR. Accounting

Horizons. 31(3). pp.55-68.

Kaur, M., Aggarwal, N. and Gupta, M., 2017. An Investigation into Returns from Financial

Statement Analysis among High Book-to-Market Stocks. Indian Journal of Economics and

Development. 13(2). pp.353-358.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual capital

disclosure: An empirical analysis. Journal of Financial Reporting and Accounting. 13(1).

pp.66-90.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Xiao, P., 2018, August. The Application of Financial Statement Analysis in Strategic

Management. In 2018 International Conference on Management, Economics, Education

and Social Sciences (MEESS 2018). Atlantis Press.

7

Books and Journals

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from EDGAR. Accounting

Horizons. 31(3). pp.55-68.

Kaur, M., Aggarwal, N. and Gupta, M., 2017. An Investigation into Returns from Financial

Statement Analysis among High Book-to-Market Stocks. Indian Journal of Economics and

Development. 13(2). pp.353-358.

Maaloul, A. and Zéghal, D., 2015. Financial statement informativeness and intellectual capital

disclosure: An empirical analysis. Journal of Financial Reporting and Accounting. 13(1).

pp.66-90.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Xiao, P., 2018, August. The Application of Financial Statement Analysis in Strategic

Management. In 2018 International Conference on Management, Economics, Education

and Social Sciences (MEESS 2018). Atlantis Press.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.