Qualitative Characteristics of Accounting Information - ACC00712

VerifiedAdded on 2022/10/19

|12

|2635

|413

Essay

AI Summary

This essay delves into the qualitative characteristics of accounting information, with a focus on faithful representation, comparability, understandability, reliability, and relevance, referencing the Australian Accounting Standards Board (AASB). The essay examines how these characteristics are reflected in the annual reports of Virgin Holdings Limited. It analyzes the company's application of prudence, understandability, comparability, faithful representation, and relevance within its financial reporting, including revaluation practices and disclosure of key figures like sales revenue, expenses, and share information. The report also discusses the reactions of investors and the security market to the presented financial information, including how dividend declarations and earnings influence investment decisions and stock prices, ultimately emphasizing the importance of reliable and transparent accounting statements for decision-making.

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

1

STUDENT NAME

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

1

STUDENT NAME

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

2

EXECUTIVE SUMMARY

The purpose of this essay is to discuss the qualitative characteristics of a good accounting

information with reference to an Australian accounting standards (AASB).it deals with features

like faithful representation, comparability, understandability, reliability and relevance. The report

also shows how this features are shown in the annual reports of virgin holdings limited and how

investors and the security market react to this information.

2

EXECUTIVE SUMMARY

The purpose of this essay is to discuss the qualitative characteristics of a good accounting

information with reference to an Australian accounting standards (AASB).it deals with features

like faithful representation, comparability, understandability, reliability and relevance. The report

also shows how this features are shown in the annual reports of virgin holdings limited and how

investors and the security market react to this information.

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

3

Table of Contents

1.0 PART 1...................................................................................................................................................4

1.1 INTRODUCTION.................................................................................................................................4

1.2 REVALUATION....................................................................................................................................4

2.0 PART 2...................................................................................................................................................5

2.1 AUSTRALIAN CONCEPTUAL FRAMEWORK.........................................................................................5

2.2 FUNCTIONS OF AUSTRALIAN CONCEPTUAL FRAMEWORK................................................................5

2.3 QUALITATIVE FEATURES OF ACCOUNTING INFORMATION...............................................................5

2.4 COMPAREABLITY...............................................................................................................................6

2.5 RELIABILITY........................................................................................................................................6

2.6 FAITHFUL REPRESENTATION..............................................................................................................6

3.0 PART 3...................................................................................................................................................6

3.1.0 VIRGIN HOLDINGS LIMITED 2018 ANNUAL REPORTS.........................................................................6

3.1.1 PRUDENCE CONCEPT..................................................................................................................6

3.1.2 UNDERSTANDABILITY.................................................................................................................7

3.1.3 COMPAREABILTY........................................................................................................................7

3.1.4 FAITHFUL REPRESENTATION.......................................................................................................7

3.1.5 RELEVANCE.................................................................................................................................8

4.0 PART 4...................................................................................................................................................8

4.1 REACTION OF INVESTORS AND SECURITY MARKET...........................................................................8

5.0 CONCLUSION.........................................................................................................................................9

6.0 REFERENCES........................................................................................................................................10

7.0 APPENDICES:........................................................................................................................................12

7.1 APPENDIX I:SALES REVENUES..........................................................................................................12

3

Table of Contents

1.0 PART 1...................................................................................................................................................4

1.1 INTRODUCTION.................................................................................................................................4

1.2 REVALUATION....................................................................................................................................4

2.0 PART 2...................................................................................................................................................5

2.1 AUSTRALIAN CONCEPTUAL FRAMEWORK.........................................................................................5

2.2 FUNCTIONS OF AUSTRALIAN CONCEPTUAL FRAMEWORK................................................................5

2.3 QUALITATIVE FEATURES OF ACCOUNTING INFORMATION...............................................................5

2.4 COMPAREABLITY...............................................................................................................................6

2.5 RELIABILITY........................................................................................................................................6

2.6 FAITHFUL REPRESENTATION..............................................................................................................6

3.0 PART 3...................................................................................................................................................6

3.1.0 VIRGIN HOLDINGS LIMITED 2018 ANNUAL REPORTS.........................................................................6

3.1.1 PRUDENCE CONCEPT..................................................................................................................6

3.1.2 UNDERSTANDABILITY.................................................................................................................7

3.1.3 COMPAREABILTY........................................................................................................................7

3.1.4 FAITHFUL REPRESENTATION.......................................................................................................7

3.1.5 RELEVANCE.................................................................................................................................8

4.0 PART 4...................................................................................................................................................8

4.1 REACTION OF INVESTORS AND SECURITY MARKET...........................................................................8

5.0 CONCLUSION.........................................................................................................................................9

6.0 REFERENCES........................................................................................................................................10

7.0 APPENDICES:........................................................................................................................................12

7.1 APPENDIX I:SALES REVENUES..........................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

4

1.0 PART 1.

1.1 INTRODUCTION.

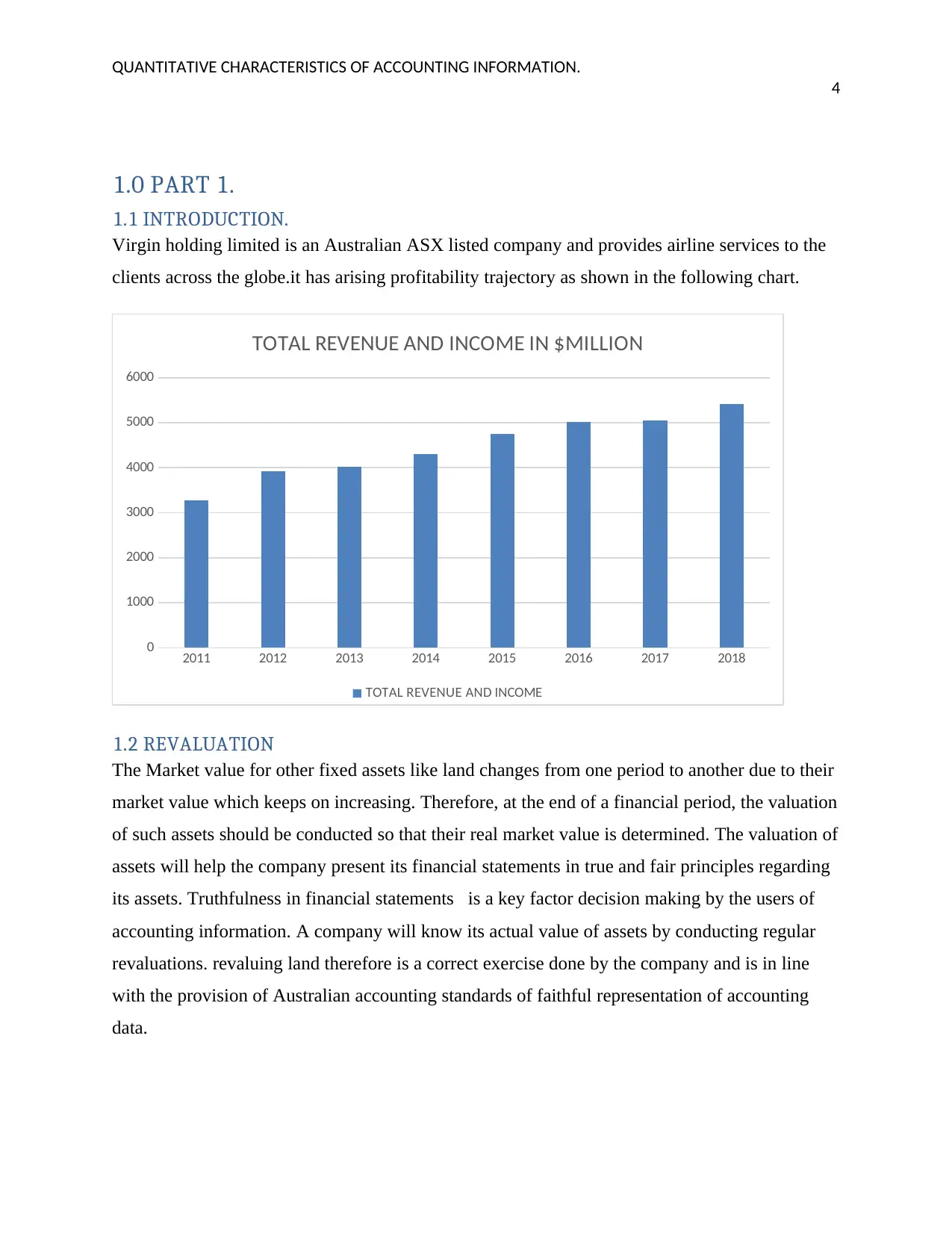

Virgin holding limited is an Australian ASX listed company and provides airline services to the

clients across the globe.it has arising profitability trajectory as shown in the following chart.

2011 2012 2013 2014 2015 2016 2017 2018

0

1000

2000

3000

4000

5000

6000

TOTAL REVENUE AND INCOME IN $MILLION

TOTAL REVENUE AND INCOME

1.2 REVALUATION

The Market value for other fixed assets like land changes from one period to another due to their

market value which keeps on increasing. Therefore, at the end of a financial period, the valuation

of such assets should be conducted so that their real market value is determined. The valuation of

assets will help the company present its financial statements in true and fair principles regarding

its assets. Truthfulness in financial statements is a key factor decision making by the users of

accounting information. A company will know its actual value of assets by conducting regular

revaluations. revaluing land therefore is a correct exercise done by the company and is in line

with the provision of Australian accounting standards of faithful representation of accounting

data.

4

1.0 PART 1.

1.1 INTRODUCTION.

Virgin holding limited is an Australian ASX listed company and provides airline services to the

clients across the globe.it has arising profitability trajectory as shown in the following chart.

2011 2012 2013 2014 2015 2016 2017 2018

0

1000

2000

3000

4000

5000

6000

TOTAL REVENUE AND INCOME IN $MILLION

TOTAL REVENUE AND INCOME

1.2 REVALUATION

The Market value for other fixed assets like land changes from one period to another due to their

market value which keeps on increasing. Therefore, at the end of a financial period, the valuation

of such assets should be conducted so that their real market value is determined. The valuation of

assets will help the company present its financial statements in true and fair principles regarding

its assets. Truthfulness in financial statements is a key factor decision making by the users of

accounting information. A company will know its actual value of assets by conducting regular

revaluations. revaluing land therefore is a correct exercise done by the company and is in line

with the provision of Australian accounting standards of faithful representation of accounting

data.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

5

2.0 PART 2.

2.1 AUSTRALIAN CONCEPTUAL FRAMEWORK

The Australian conceptual framework shows important characteristics of a best presentation of

accounting information including assets in financial statements. (Wagenhofer, 2009, pg. 76) this

Australian Conceptual framework has information on fundamentals of financial statements

which include techniques on features and recognition (Christensen, 2010, pg. 291).

2.2 FUNCTIONS OF AUSTRALIAN CONCEPTUAL FRAMEWORK.

a) It sets out harmonized rules and guidelines on good presentation of accounting

information.

b) The standards on proper preparation and presentation of accounting information as

highlighted in The Australian accounting standards helps accountants on utilization of

certain standards

c) It enhances quality of accounting information in that, the Australian Accounting

Standards Board (AASB) uses the conceptual framework to amend various accounting

standards

d) The uniform standards of financial statements preparation and presentation make it easy

to interpret accounting information.

e) It helps auditors arrive at a judgment on whether the preparation and presentation of

financial statements is in accordance of the required standards.

2.3 QUALITATIVE FEATURES OF ACCOUNTING INFORMATION.

Accounting information should be relevant to its users. this means that the presented information

is helpful the users as far as decision making are concerned (Karğın, 2013, pg.73).it should also

help the company or other users predict their future plans by analyzing previous performances.

therefore, key fundamentals like salaries, share price and dividends should be indicated clearly

so that to be relevant to investors decision making (Nobes&Stadler, 2015, Pg. 591).

The accounting information should be easy to understand. Ambiguous and complex figures

should not be used in presentation of information because users may find it difficult to

5

2.0 PART 2.

2.1 AUSTRALIAN CONCEPTUAL FRAMEWORK

The Australian conceptual framework shows important characteristics of a best presentation of

accounting information including assets in financial statements. (Wagenhofer, 2009, pg. 76) this

Australian Conceptual framework has information on fundamentals of financial statements

which include techniques on features and recognition (Christensen, 2010, pg. 291).

2.2 FUNCTIONS OF AUSTRALIAN CONCEPTUAL FRAMEWORK.

a) It sets out harmonized rules and guidelines on good presentation of accounting

information.

b) The standards on proper preparation and presentation of accounting information as

highlighted in The Australian accounting standards helps accountants on utilization of

certain standards

c) It enhances quality of accounting information in that, the Australian Accounting

Standards Board (AASB) uses the conceptual framework to amend various accounting

standards

d) The uniform standards of financial statements preparation and presentation make it easy

to interpret accounting information.

e) It helps auditors arrive at a judgment on whether the preparation and presentation of

financial statements is in accordance of the required standards.

2.3 QUALITATIVE FEATURES OF ACCOUNTING INFORMATION.

Accounting information should be relevant to its users. this means that the presented information

is helpful the users as far as decision making are concerned (Karğın, 2013, pg.73).it should also

help the company or other users predict their future plans by analyzing previous performances.

therefore, key fundamentals like salaries, share price and dividends should be indicated clearly

so that to be relevant to investors decision making (Nobes&Stadler, 2015, Pg. 591).

The accounting information should be easy to understand. Ambiguous and complex figures

should not be used in presentation of information because users may find it difficult to

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

6

understand. therefore, accounting information should be presented in a way that the user will

easily understand.

2.4 COMPAREABLITY

Good Accounting information should be comparable. this means that the presented information

of various periods should be easy to compare. The results of an item from previous, actual and

future information (Yip &Young, 2012, pg.1770) can be referred easily if comparable

information is prepared. For instance, firms within the similar industry should prepare and

present information in a format that is comparable for the users to make comparison with ease.

2.5 RELIABILITY

Good accounting information should be Reliable. reliability means the information presented

should not mislead and errors free. A time, relevant information would not automatically mean it

is reliable in that a recognized method that is used can actually present false facts. The damage

for a pending case in a company is the best example. The worth should not be indicated in full

because it will affect the position of the company’s earnings.

2.6 FAITHFUL REPRESENTATION

Faithfull and truth presentation of information means that the financial statements should be

prepared using true information .it should clearly disclose the accounting estimates and

assumptions. Presentation of fundamentals like assets, liabilities and equities should be in a true

manner and based on acceptable and understandable recognition format. Wrong measurement

methods and recognitions leads to presentation of untruthful information.in such a case, relevant

measures on how to disclose errors should be provided (Macintosh, 2009, pg. 150).

3.0 PART 3.

3.1.0 VIRGIN HOLDINGS LIMITED 2018 ANNUAL REPORTS.

3.1.1 PRUDENCE CONCEPT

Prudence concept states that Company’s revenues should not be overvalued as well as

undervaluing its expenses. The requirement of this concept is that, Revenues be recognized once

its inflows are known and certain (Barker, 2015, pg. 515). Virgin Australian Group annual report

on sales and revenues in pg.48 indicates clearly how the accountants are practicing prudence’s

concept. the company’s revenues and income the year 2018 is $ 5420.7 million and 5047.0

6

understand. therefore, accounting information should be presented in a way that the user will

easily understand.

2.4 COMPAREABLITY

Good Accounting information should be comparable. this means that the presented information

of various periods should be easy to compare. The results of an item from previous, actual and

future information (Yip &Young, 2012, pg.1770) can be referred easily if comparable

information is prepared. For instance, firms within the similar industry should prepare and

present information in a format that is comparable for the users to make comparison with ease.

2.5 RELIABILITY

Good accounting information should be Reliable. reliability means the information presented

should not mislead and errors free. A time, relevant information would not automatically mean it

is reliable in that a recognized method that is used can actually present false facts. The damage

for a pending case in a company is the best example. The worth should not be indicated in full

because it will affect the position of the company’s earnings.

2.6 FAITHFUL REPRESENTATION

Faithfull and truth presentation of information means that the financial statements should be

prepared using true information .it should clearly disclose the accounting estimates and

assumptions. Presentation of fundamentals like assets, liabilities and equities should be in a true

manner and based on acceptable and understandable recognition format. Wrong measurement

methods and recognitions leads to presentation of untruthful information.in such a case, relevant

measures on how to disclose errors should be provided (Macintosh, 2009, pg. 150).

3.0 PART 3.

3.1.0 VIRGIN HOLDINGS LIMITED 2018 ANNUAL REPORTS.

3.1.1 PRUDENCE CONCEPT

Prudence concept states that Company’s revenues should not be overvalued as well as

undervaluing its expenses. The requirement of this concept is that, Revenues be recognized once

its inflows are known and certain (Barker, 2015, pg. 515). Virgin Australian Group annual report

on sales and revenues in pg.48 indicates clearly how the accountants are practicing prudence’s

concept. the company’s revenues and income the year 2018 is $ 5420.7 million and 5047.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

7

million the year 2017.the difference in sales revenue of 2018 and 2017 is $373.7 million which is

a fair figure. The report on expenses is clearly listed and it has slight difference too

(Kirschenheiter &Ramakrishna, 2010). The net operating expenditure for the year 2018 is $

5473.0 million while for the year 2017 is 5169.4 million. Prudence is useful when determining

unforeseen economic situations like life of assets and debt collection probability.

3.1.2 UNDERSTANDABILITY

The feature of understandability in Virgin Australian Holdings’ annual report is shown in the

statements. the basic assumptions and relevant workings have been supported with some few

notes to help in understanding the information. For example, in pg.22 regarding equities and

liabilities, the company’s equity decreased at the current year while the liability exceeded the

assets by 544.4 million the year 2019 and 5608 in 2017.these notes brings aspect of

understandability into play.

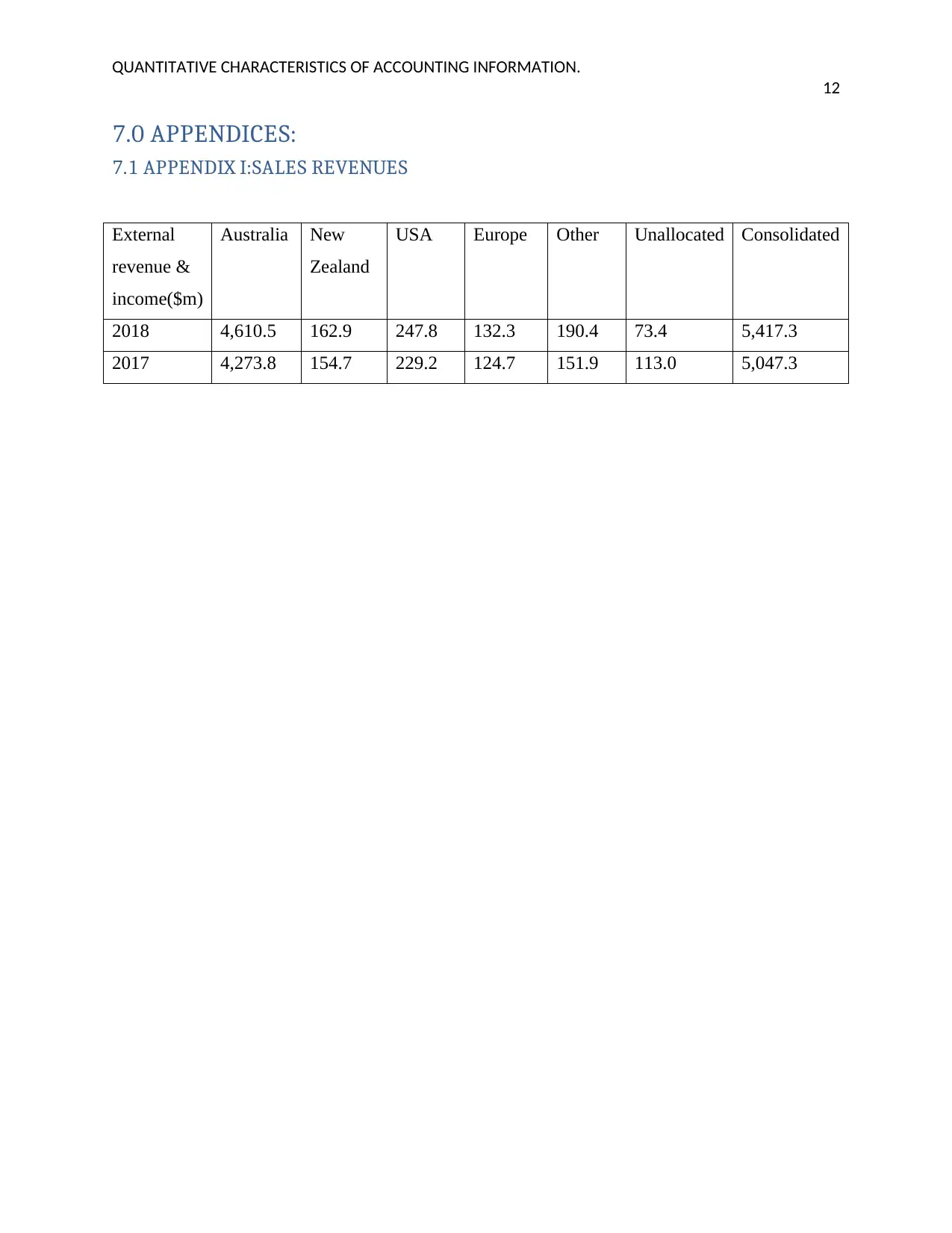

3.1.3 COMPAREABILTY

Comparability feature is shown in the annual financial report pg. 58 when the company is

comparing general sales revenue from domestic sales of tickets as shown in appendix I.

The report clearly shows that the revenue on ticket sales in Australia increased by 7.9% from $

4,273.8 million to $4,610.5 million. These shows that Virgin Australian group portray the

comparability feature.in pg. 18 of the 2018 annual report, the company clearly compares its

revenues and expenditure for 2018 and 2017.it clearly shows the net loss after tax of $653.3m

and $185.8m.this indicates the comparability nature of this statements since the user can easily

compare the losses made by the company each year an whether there is any improvement.it is

further disclosed that revenues and income rose from $5047.30M to $5420.70M indicating an

increase of $ 373.4M,this further confirms the comparability nature of the statements(Cascino &

Gassen, 2010)

3.1.4 FAITHFUL REPRESENTATION

faithful representation has been portrayed in Virgin Australian group’s annual financial report

where the company was able to show how it arrived at certain judgments. the report has been

prepared in historical cost method as seen in pg.52 of the annual report for the year 2018.the

users of this information are able to make important decisions using such disclosures regarding

7

million the year 2017.the difference in sales revenue of 2018 and 2017 is $373.7 million which is

a fair figure. The report on expenses is clearly listed and it has slight difference too

(Kirschenheiter &Ramakrishna, 2010). The net operating expenditure for the year 2018 is $

5473.0 million while for the year 2017 is 5169.4 million. Prudence is useful when determining

unforeseen economic situations like life of assets and debt collection probability.

3.1.2 UNDERSTANDABILITY

The feature of understandability in Virgin Australian Holdings’ annual report is shown in the

statements. the basic assumptions and relevant workings have been supported with some few

notes to help in understanding the information. For example, in pg.22 regarding equities and

liabilities, the company’s equity decreased at the current year while the liability exceeded the

assets by 544.4 million the year 2019 and 5608 in 2017.these notes brings aspect of

understandability into play.

3.1.3 COMPAREABILTY

Comparability feature is shown in the annual financial report pg. 58 when the company is

comparing general sales revenue from domestic sales of tickets as shown in appendix I.

The report clearly shows that the revenue on ticket sales in Australia increased by 7.9% from $

4,273.8 million to $4,610.5 million. These shows that Virgin Australian group portray the

comparability feature.in pg. 18 of the 2018 annual report, the company clearly compares its

revenues and expenditure for 2018 and 2017.it clearly shows the net loss after tax of $653.3m

and $185.8m.this indicates the comparability nature of this statements since the user can easily

compare the losses made by the company each year an whether there is any improvement.it is

further disclosed that revenues and income rose from $5047.30M to $5420.70M indicating an

increase of $ 373.4M,this further confirms the comparability nature of the statements(Cascino &

Gassen, 2010)

3.1.4 FAITHFUL REPRESENTATION

faithful representation has been portrayed in Virgin Australian group’s annual financial report

where the company was able to show how it arrived at certain judgments. the report has been

prepared in historical cost method as seen in pg.52 of the annual report for the year 2018.the

users of this information are able to make important decisions using such disclosures regarding

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

8

the treatment of some assets, they have further disclosed that the depreciation is done using

straight line method. This are the necessary information to show clearly the assumptions and

accounting estimates used in preparation of accounting reports.

Prudence concept in accounting means the use of judgement in treatment of certain estimates in

accounting. Virgin company has followed the standards required by this concept by showing

how they arrived at the useful life of some its assets like aircraft and aeronautic related which is

between (10-40) years, computer equipment (3-5) years and landing gears at (4-22) years. It’s

outlined in pg.70 of the annual financial report of the year 2018.capitalization method is used to

arrive at these rates. This clearly indicate how prudence concept has been used by the

accountants (Yurisandi & Puspitasari, 2015, pg. 645).

Virgin company has clearly depicted key fundamentals concerning the various obligations like

Like total assets of the company which was $6355.8 million the year 2017 and $ 6188.4 million

in 2018.the company’s total assets were estimated at $4782.0 million in 2017 and $ 5093.4

million in 2018.the reliability in this information will enable investors and various users to make

relevant decisions on investments (Lim, Lee, Kausar &Walker, 2014, pg. 270).

3.1.5 RELEVANCE.

Relevance characteristic in Virgin’s annual financial report is portrayed in its uniform

preparation of their yearly financial report ending every 30th June of the year. This shows that the

concern of the user is considered when preparing this report, therefore helping the user to foresee

the declaration of a companies’ performance at a particular given period.it will also aid investors

in predicting dividends payable the following year. The declaration of the dividends by the

company in their annual report of 8.1 and 2.8 cents shows that the accounting information is very

relevant to the potential investors of the company.pg 34 of 2018 annual report.

4.0 PART 4.

4.1 REACTION OF INVESTORS AND SECURITY MARKET

The declaration of earnings by Virgin company will encourage potential investors to make

investment in the company (Lee & Masulis, 2009, pg. 450). the annual financial report for the

year 2018 and 2017 shows that the company paid shares at a rate of 8.1 and 2.8 cents in 2018 and

2017 consecutively. This particular information on share are very useful to the investors as they

8

the treatment of some assets, they have further disclosed that the depreciation is done using

straight line method. This are the necessary information to show clearly the assumptions and

accounting estimates used in preparation of accounting reports.

Prudence concept in accounting means the use of judgement in treatment of certain estimates in

accounting. Virgin company has followed the standards required by this concept by showing

how they arrived at the useful life of some its assets like aircraft and aeronautic related which is

between (10-40) years, computer equipment (3-5) years and landing gears at (4-22) years. It’s

outlined in pg.70 of the annual financial report of the year 2018.capitalization method is used to

arrive at these rates. This clearly indicate how prudence concept has been used by the

accountants (Yurisandi & Puspitasari, 2015, pg. 645).

Virgin company has clearly depicted key fundamentals concerning the various obligations like

Like total assets of the company which was $6355.8 million the year 2017 and $ 6188.4 million

in 2018.the company’s total assets were estimated at $4782.0 million in 2017 and $ 5093.4

million in 2018.the reliability in this information will enable investors and various users to make

relevant decisions on investments (Lim, Lee, Kausar &Walker, 2014, pg. 270).

3.1.5 RELEVANCE.

Relevance characteristic in Virgin’s annual financial report is portrayed in its uniform

preparation of their yearly financial report ending every 30th June of the year. This shows that the

concern of the user is considered when preparing this report, therefore helping the user to foresee

the declaration of a companies’ performance at a particular given period.it will also aid investors

in predicting dividends payable the following year. The declaration of the dividends by the

company in their annual report of 8.1 and 2.8 cents shows that the accounting information is very

relevant to the potential investors of the company.pg 34 of 2018 annual report.

4.0 PART 4.

4.1 REACTION OF INVESTORS AND SECURITY MARKET

The declaration of earnings by Virgin company will encourage potential investors to make

investment in the company (Lee & Masulis, 2009, pg. 450). the annual financial report for the

year 2018 and 2017 shows that the company paid shares at a rate of 8.1 and 2.8 cents in 2018 and

2017 consecutively. This particular information on share are very useful to the investors as they

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

9

will use it make various investment decision. The information on securities will help the users to

predict anticipated fluctuations of share prices (Mlonzi, Kruger, & Nthoesane, 2011, pg.150).

According to Cready& Gurun (2010) they stated that low earnings results in increase in market

values and Hussin et al. (2010) also attributes negative market values to minimum earnings.

The disclosure of share prices and its share profitability has positive or negative impact on the

stock price (Hoggett et al, 2014).

5.0 CONCLUSION.

In conclusion, the above characteristics depicts a good accounting statement that is useful to the

users. The financial report prepared should present a true and reliable information to the users.the

disclosures regarding payment of shares will greatly influence the decisions of investors while

dividends declared will affect the stock prices in the security stock exchange.

9

will use it make various investment decision. The information on securities will help the users to

predict anticipated fluctuations of share prices (Mlonzi, Kruger, & Nthoesane, 2011, pg.150).

According to Cready& Gurun (2010) they stated that low earnings results in increase in market

values and Hussin et al. (2010) also attributes negative market values to minimum earnings.

The disclosure of share prices and its share profitability has positive or negative impact on the

stock price (Hoggett et al, 2014).

5.0 CONCLUSION.

In conclusion, the above characteristics depicts a good accounting statement that is useful to the

users. The financial report prepared should present a true and reliable information to the users.the

disclosures regarding payment of shares will greatly influence the decisions of investors while

dividends declared will affect the stock prices in the security stock exchange.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

10

6.0 REFERENCES.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Christensen, J., 2010. Conceptual frameworks of accounting from an information

perspective. Accounting and Business Research, 40(3), pp.287-299.

Geoffrey Booth, G., Kallunki, J.P., Sahlström, P. and Tyynelä, J., 2011. Foreign vs domestic

investors and the post-announcement drift. International Journal of Managerial Finance, 7(3),

pp.220-237.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting. John Wiley & Sons.

Karğın, S., 2013. The impact of IFRS on the value relevance of accounting information:

Evidence from Turkish firms. International Journal of Economics and Finance, 5(4), pp.71-80.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Lee, G. and Masulis, R.W., 2009. Seasoned equity offerings: Quality of accounting information

and expected flotation costs. Journal of Financial Economics, 92(3), pp.443-469.

Lim, C.Y., Lee, E., Kausar, A. and Walker, M., 2014. Bank accounting conservatism and bank

loan pricing. Journal of Accounting and Public Policy, 33(3), pp.260-278.

Macintosh, N.B., 2009. Accounting and the truth of earnings reports: philosophical

considerations. European Accounting Review, 18(1), pp.141-175.

Mlonzi, V.F., Kruger, J. and Nthoesane, M.G., 2011. Share price reaction to earnings

announcement on the JSE-ALtX: A test for market efficiency. Southern African Business

Review, 15(3), pp.142-166.

10

6.0 REFERENCES.

Barker, R., 2015. Conservatism, prudence and the IASB's conceptual framework. Accounting

and Business Research, 45(4), pp.514-538.

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Christensen, J., 2010. Conceptual frameworks of accounting from an information

perspective. Accounting and Business Research, 40(3), pp.287-299.

Geoffrey Booth, G., Kallunki, J.P., Sahlström, P. and Tyynelä, J., 2011. Foreign vs domestic

investors and the post-announcement drift. International Journal of Managerial Finance, 7(3),

pp.220-237.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting. John Wiley & Sons.

Karğın, S., 2013. The impact of IFRS on the value relevance of accounting information:

Evidence from Turkish firms. International Journal of Economics and Finance, 5(4), pp.71-80.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Lee, G. and Masulis, R.W., 2009. Seasoned equity offerings: Quality of accounting information

and expected flotation costs. Journal of Financial Economics, 92(3), pp.443-469.

Lim, C.Y., Lee, E., Kausar, A. and Walker, M., 2014. Bank accounting conservatism and bank

loan pricing. Journal of Accounting and Public Policy, 33(3), pp.260-278.

Macintosh, N.B., 2009. Accounting and the truth of earnings reports: philosophical

considerations. European Accounting Review, 18(1), pp.141-175.

Mlonzi, V.F., Kruger, J. and Nthoesane, M.G., 2011. Share price reaction to earnings

announcement on the JSE-ALtX: A test for market efficiency. Southern African Business

Review, 15(3), pp.142-166.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

11

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and Business

Research, 45(5), pp.572-601.

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Virgin holdings annual report<

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

fy18-annual-report.pdf>

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

Yip, R.W. and Young, D., 2012. Does mandatory IFRS adoption improve information

comparability? The Accounting Review, 87(5), pp.1767-1789.

Yurisandi, T. and Puspitasari, E., 2015. Financial Reporting Quality-Before and After IFRS

Adoption Using NiCE Qualitative Characteristics Measurement. Procedia-Social and Behavioral

Sciences, 211, pp.644-652

11

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and Business

Research, 45(5), pp.572-601.

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Virgin holdings annual report<

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

fy18-annual-report.pdf>

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

Yip, R.W. and Young, D., 2012. Does mandatory IFRS adoption improve information

comparability? The Accounting Review, 87(5), pp.1767-1789.

Yurisandi, T. and Puspitasari, E., 2015. Financial Reporting Quality-Before and After IFRS

Adoption Using NiCE Qualitative Characteristics Measurement. Procedia-Social and Behavioral

Sciences, 211, pp.644-652

QUANTITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION.

12

7.0 APPENDICES:

7.1 APPENDIX I:SALES REVENUES

External

revenue &

income($m)

Australia New

Zealand

USA Europe Other Unallocated Consolidated

2018 4,610.5 162.9 247.8 132.3 190.4 73.4 5,417.3

2017 4,273.8 154.7 229.2 124.7 151.9 113.0 5,047.3

12

7.0 APPENDICES:

7.1 APPENDIX I:SALES REVENUES

External

revenue &

income($m)

Australia New

Zealand

USA Europe Other Unallocated Consolidated

2018 4,610.5 162.9 247.8 132.3 190.4 73.4 5,417.3

2017 4,273.8 154.7 229.2 124.7 151.9 113.0 5,047.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.