Current Development of Accounting Thought: Analysis and Exposure Draft

VerifiedAdded on 2023/03/17

|15

|3766

|98

Report

AI Summary

This report provides an in-depth analysis of an accounting news article concerning CIMIC's $1.9 billion share plunge, exploring the company's alleged use of fraudulent accounting practices, including aggressive revenue recognition and manipulation of financial statements through hedge funds. The analysis connects these issues to key accounting concepts such as agency theory, corporate governance, and the importance of internal controls and ethical business practices. Furthermore, the report reviews the IFRS exposure draft on the classification of liabilities, discussing the accounting issues identified and the behavior of regulators based on the public interest theory. The report emphasizes the need for ethical conduct, robust auditing practices, and effective corporate governance to protect investor interests and ensure the reliability of financial reporting, including the application of ASA 315 and ASA 330 auditing standards. The study stresses the significance of internal auditing and the importance of ethical business practices for maintaining an internal control over business operations.

1

Current Development of Accounting Thought

Current Development of Accounting Thought

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Part 1: Analysis of Accounting News Article

Introduction

This section intends to identify and describe a recent accounting issue published within a

professional journal. The accounting news article selected for analysis purpose is ‘Hedge funds

may be behind CIMIC's $1.9b share plunge, investor claims’ published within the Sydney

Morning Herald (SMH) on 9th May, 2019. The key issues discussed within the article are

analyzed by the application of relevant accounting concepts for developing a proper insight into

them. The overall evaluation of the article is carried out to widen the knowledge base of CEO

regarding the key issues discussed within the article to be presented at an upcoming conference.

Description of Major Issues in Article

The selected article has presented the accounting news in relation to the use of fraudulent

accounting practices by CIMIC, an ASX listed Construction Company within Australia. The

company that was previously known as Leighton Holdings is known and is undertaking the

construction of multiple large-scale infrastructure projects such as building of $11 billion worth

of metro rail tunnel and new cross over retail in Brisbane of about $5.4 billion and many other

capital intensive construction projects. It has been reported by Sydney Morning Herald that the

company is adopting the use of inflating its share prices by manipulation of its financial

statements. It is adopting the use of hedge funds that is borrowing shares in expectation of their

decline in prices and thereafter repurchasing and retuning them when the price falls for realizing

gains from the difference. It has been accused by a Hong-Kong based research firm, GMT, of

inflating its profits by the use of hedge funds over the past two years. It has been reported by

GMT that the company is having the presence of unbilled revenue in its balance sheet and it is

about 9.3 per cent higher as compared to its peer group (Johanson, 2019).

This depicts that it is adopting the use of aggressive accounting practices for inflating its

profitability position. It has also been reported by Simply Wall that CIMIC Group Limited share

prices are subject to high volatility with increase in share price to A$52.51 at on time and

dropping to about A$44.59 at another time. Thus, this high volatility provided by the stock of the

company gives investors a chance to enter into opportunity for realizing gains at a lower price. It

was largely overvalued due to use of illegal trading practices and use of manipulated financial

Part 1: Analysis of Accounting News Article

Introduction

This section intends to identify and describe a recent accounting issue published within a

professional journal. The accounting news article selected for analysis purpose is ‘Hedge funds

may be behind CIMIC's $1.9b share plunge, investor claims’ published within the Sydney

Morning Herald (SMH) on 9th May, 2019. The key issues discussed within the article are

analyzed by the application of relevant accounting concepts for developing a proper insight into

them. The overall evaluation of the article is carried out to widen the knowledge base of CEO

regarding the key issues discussed within the article to be presented at an upcoming conference.

Description of Major Issues in Article

The selected article has presented the accounting news in relation to the use of fraudulent

accounting practices by CIMIC, an ASX listed Construction Company within Australia. The

company that was previously known as Leighton Holdings is known and is undertaking the

construction of multiple large-scale infrastructure projects such as building of $11 billion worth

of metro rail tunnel and new cross over retail in Brisbane of about $5.4 billion and many other

capital intensive construction projects. It has been reported by Sydney Morning Herald that the

company is adopting the use of inflating its share prices by manipulation of its financial

statements. It is adopting the use of hedge funds that is borrowing shares in expectation of their

decline in prices and thereafter repurchasing and retuning them when the price falls for realizing

gains from the difference. It has been accused by a Hong-Kong based research firm, GMT, of

inflating its profits by the use of hedge funds over the past two years. It has been reported by

GMT that the company is having the presence of unbilled revenue in its balance sheet and it is

about 9.3 per cent higher as compared to its peer group (Johanson, 2019).

This depicts that it is adopting the use of aggressive accounting practices for inflating its

profitability position. It has also been reported by Simply Wall that CIMIC Group Limited share

prices are subject to high volatility with increase in share price to A$52.51 at on time and

dropping to about A$44.59 at another time. Thus, this high volatility provided by the stock of the

company gives investors a chance to enter into opportunity for realizing gains at a lower price. It

was largely overvalued due to use of illegal trading practices and use of manipulated financial

3

accounting practices such as CMIC has used its acquisition of the construction services group

UGL in the year 2016 for inflating profits. The company has reported a loss of about $1.6 billion

within two days after it was claimed by the research report of GMT that it adopts the use of

illegal accounting practices for inflating its pre-tax profits (Htach, 2019).

The article has discussed on the issue on use of aggressive accounting policies and its

long-term impact on the future performance of a firm. As stated within the article, GMT has

reported that CIMIC has adopted the use of unethical accounting practices such as aggressive

revenue recognition, acquisition accounting and hedge funds for inflating its profitability

position. The management of the company derives higher incentives for inflating its share price

and thus enhancing its profitability position and improving the operating cash flows. It has

reportedly that Deloitte, the auditing partner of the firm, was unable to identify such illegal

accounting practices within the company. Deloitte responsible for providing advice to the

company on the matters related to risk management and financial controls. However, it has been

concluded from identification of illegal accounting practices within the company that Deloitte is

either unable to identify the risks associated with its business practices or has ignored them. The

article can be regarded as largely important from the perspective of investors of the company as

there is not adequate information for reliably forecasting the future cash flows. The high stock

price volatility of the company identified has reflected that potential investors need to be

cautious while undertaking decisions regarding investment (Johanson, 2019).

Linkage of Major Issues within Article in context of the Accounting Topics

The article has discussed the key issue of use of unethical and illegal accounting practices

by CIMIC that has resulted in causing the reduction in market value by about 50% the past two

years. The main reasons for causing the downfall in the market value of the company is use of

aggressive accounting practices for inflation of profits (Wiggins, 2016). The major responsible

for the prevalence of such accounting practices within the firm is lack of adequate internal

control policies and procedures (IFRS, 2018). The business managers were provided higher

incentives for the sake of maximizing share prices and thus reporting higher profits. The agency

theory, in this context, has stated that shareholders, who are the principals, tend to reduce the

agency cost by providing incentives to the business managers, who are the agent, for ensuring

that they act in the interests of the shareholders by creating maximum value for the firm.

accounting practices such as CMIC has used its acquisition of the construction services group

UGL in the year 2016 for inflating profits. The company has reported a loss of about $1.6 billion

within two days after it was claimed by the research report of GMT that it adopts the use of

illegal accounting practices for inflating its pre-tax profits (Htach, 2019).

The article has discussed on the issue on use of aggressive accounting policies and its

long-term impact on the future performance of a firm. As stated within the article, GMT has

reported that CIMIC has adopted the use of unethical accounting practices such as aggressive

revenue recognition, acquisition accounting and hedge funds for inflating its profitability

position. The management of the company derives higher incentives for inflating its share price

and thus enhancing its profitability position and improving the operating cash flows. It has

reportedly that Deloitte, the auditing partner of the firm, was unable to identify such illegal

accounting practices within the company. Deloitte responsible for providing advice to the

company on the matters related to risk management and financial controls. However, it has been

concluded from identification of illegal accounting practices within the company that Deloitte is

either unable to identify the risks associated with its business practices or has ignored them. The

article can be regarded as largely important from the perspective of investors of the company as

there is not adequate information for reliably forecasting the future cash flows. The high stock

price volatility of the company identified has reflected that potential investors need to be

cautious while undertaking decisions regarding investment (Johanson, 2019).

Linkage of Major Issues within Article in context of the Accounting Topics

The article has discussed the key issue of use of unethical and illegal accounting practices

by CIMIC that has resulted in causing the reduction in market value by about 50% the past two

years. The main reasons for causing the downfall in the market value of the company is use of

aggressive accounting practices for inflation of profits (Wiggins, 2016). The major responsible

for the prevalence of such accounting practices within the firm is lack of adequate internal

control policies and procedures (IFRS, 2018). The business managers were provided higher

incentives for the sake of maximizing share prices and thus reporting higher profits. The agency

theory, in this context, has stated that shareholders, who are the principals, tend to reduce the

agency cost by providing incentives to the business managers, who are the agent, for ensuring

that they act in the interests of the shareholders by creating maximum value for the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

However, the adoption of incentive schemes can lead to the occurrence of fraudulent accounting

practices by the business managers for realizing higher incentives. Thus, the occurrence of

aggressive accounting practices within CIMIC can be explained on the basis of agency theory as

the business managers were releasing higher incentives from the Board for delivering higher

returns for the shareholders (Solomon, 2007, p.20-27).

Also, it has emphasized on the adoption of a proper risk management policies and

procedures to ensure that there is presence of an effective risk management policies to maintain

an internal control over the business processes. The case discussed within the selected article has

also paced emphasized on presence of an effective corporate governance system within business

corporations. The presence of an adequate corporate governance system policies and procedures

will provide the ethical guidelines and procedures that bsuienss manager and employees of a

corporation should follow for conducting their work responsibilities and duties. The two

common motivations that can be regarded as responsible for committing fraud within CIMIC by

its business managers are personal greed and hiding its real financial performance from the

investors for the sake of increasing its share prices (Is CIMIC Group Limited (ASX:CIM)

Undervalued, 2018). The investor’s interests are negatively impacted largely by the occurrence

of such accounting issues within CIMIC. This is because the company was reflected to largely

profitable to its investors and its share prices were overvalued. However, after the report

developed by GMT and identification of its aggressive accounting policies the market value of

the company has suffered a drop due to negative impact on its investors mind regarding the

reliability of its stock performance in the future (Wiggins, 2016). As such, it has emphasized on

the need for presence of ethical business practices by developing an effective corporate

governance system for protecting the interests of the investors as per the stakeholder theory. The

stakeholder theory has stated that the main objective of a business corporation should be creating

maximum value for its stakeholders by conducting the business operations in an ethical and

moral manner (Solomon, 2007, p.20-27).

Also, as identified within the article the presence of such unethical business practices

within the company has also not been reported during its audit. Deloitte, the auditor of the

company has failed to identify and report the use of such aggressive accounting practices that are

responsible for manipulation of its financial information presented within its balance sheet. As

However, the adoption of incentive schemes can lead to the occurrence of fraudulent accounting

practices by the business managers for realizing higher incentives. Thus, the occurrence of

aggressive accounting practices within CIMIC can be explained on the basis of agency theory as

the business managers were releasing higher incentives from the Board for delivering higher

returns for the shareholders (Solomon, 2007, p.20-27).

Also, it has emphasized on the adoption of a proper risk management policies and

procedures to ensure that there is presence of an effective risk management policies to maintain

an internal control over the business processes. The case discussed within the selected article has

also paced emphasized on presence of an effective corporate governance system within business

corporations. The presence of an adequate corporate governance system policies and procedures

will provide the ethical guidelines and procedures that bsuienss manager and employees of a

corporation should follow for conducting their work responsibilities and duties. The two

common motivations that can be regarded as responsible for committing fraud within CIMIC by

its business managers are personal greed and hiding its real financial performance from the

investors for the sake of increasing its share prices (Is CIMIC Group Limited (ASX:CIM)

Undervalued, 2018). The investor’s interests are negatively impacted largely by the occurrence

of such accounting issues within CIMIC. This is because the company was reflected to largely

profitable to its investors and its share prices were overvalued. However, after the report

developed by GMT and identification of its aggressive accounting policies the market value of

the company has suffered a drop due to negative impact on its investors mind regarding the

reliability of its stock performance in the future (Wiggins, 2016). As such, it has emphasized on

the need for presence of ethical business practices by developing an effective corporate

governance system for protecting the interests of the investors as per the stakeholder theory. The

stakeholder theory has stated that the main objective of a business corporation should be creating

maximum value for its stakeholders by conducting the business operations in an ethical and

moral manner (Solomon, 2007, p.20-27).

Also, as identified within the article the presence of such unethical business practices

within the company has also not been reported during its audit. Deloitte, the auditor of the

company has failed to identify and report the use of such aggressive accounting practices that are

responsible for manipulation of its financial information presented within its balance sheet. As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

such, it can be said that auditor of the company has not followed due diligence in verifying the

financial reports (IFRS Foundation, 2018). Thus, the auditor has not complied with the

faithfulness principle of the conceptual accounting framework according to which the financial

reports developed must represent fair value of a corporation and should be free from any type of

materialistic error ("About the AASB", 2019). It has also emphasized on the need for carrying

out internal audit of a company for adding value and improving the internal control over its

business operations. The presence of internal auditing would ensure that the company is able to

conduct its business operations in an ethical manner by bringing a systematic and disciplined

approach and developing an effective risk management control system ("About ASIC", 2019).

Also, it has emphasized on the need for external auditors of a company to comply with the

Australian Auditing standards for ensuring that an auditor is able to accurately undertake the

auditing of financial report of a corporation. The auditing standards ASA 3151 and ASA 3302

should be applied for overcoming the risks related to material misstatements within a business

corporation due to presence of fraudulent accounting practices (Cooper, Funnell & Lee, 2012,

p.371-372).

Conclusion

The overall analysis of the article has inferred the need for presence of effective system

of internal control and corporate governing practice within a company for reducing the risk of

occurrence of any type of unethical accounting practices. The remuneration structure of the

business managers should be regularly reviewed and controlled by the Board to ensure that the

incentives schemes are not fostering the adoption of false accounting practices by business

managers for realizing higher personal benefits.

such, it can be said that auditor of the company has not followed due diligence in verifying the

financial reports (IFRS Foundation, 2018). Thus, the auditor has not complied with the

faithfulness principle of the conceptual accounting framework according to which the financial

reports developed must represent fair value of a corporation and should be free from any type of

materialistic error ("About the AASB", 2019). It has also emphasized on the need for carrying

out internal audit of a company for adding value and improving the internal control over its

business operations. The presence of internal auditing would ensure that the company is able to

conduct its business operations in an ethical manner by bringing a systematic and disciplined

approach and developing an effective risk management control system ("About ASIC", 2019).

Also, it has emphasized on the need for external auditors of a company to comply with the

Australian Auditing standards for ensuring that an auditor is able to accurately undertake the

auditing of financial report of a corporation. The auditing standards ASA 3151 and ASA 3302

should be applied for overcoming the risks related to material misstatements within a business

corporation due to presence of fraudulent accounting practices (Cooper, Funnell & Lee, 2012,

p.371-372).

Conclusion

The overall analysis of the article has inferred the need for presence of effective system

of internal control and corporate governing practice within a company for reducing the risk of

occurrence of any type of unethical accounting practices. The remuneration structure of the

business managers should be regularly reviewed and controlled by the Board to ensure that the

incentives schemes are not fostering the adoption of false accounting practices by business

managers for realizing higher personal benefits.

6

Part 2: Exposure Draft

This section will review the exposure draft that has been introduced by IFRS Foundation

on “Classification of Liabilities”. This exposure draft has been introduced in February 2015 as

“Exposure Draft ED/2015/1: Classification of Liabilities” and main purpose of this exposure

draft to make proposed changes to IAS 1. Exposure draft has been opened for public review and

comment letters are welcomed by IFRS Foundation till June 10, 2015 (IFRS Foundation:

Exposure Draft: ED/2015/1, 2015). IFRS Foundation is an international organization works to

issue, modify and maintain the International Accounting Standards for the purpose of

contributing in the development of global financial markets and economic activities in

international context.

A: Accounting Issues that has been identified in the exposure draft and changes that has

been introduced the selected exposure draft

The exposure draft ED/2015/1: Classification of Liabilities has been introduced to make

specific changes in the accounting standard IAS1: Presentation of Financial Statements. Initially

IAS1 requires entities to classify their liabilities as current liabilities (Short term liabilities)

unless entity has an unconditional right to postpone the liabilities settlement after 12 months.

Many requests have been received by the various entities around the world to IFRS interpretation

committee that they find it difficult to judge on which liabilities has to treat current or non-

current due to presence of ambiguity in its classification. Due to this issue, there have been cases

where entities classify same liabilities under different heading (Current and Non-Current). It

create situation hard for the investors to understand and compare financial statements of different

companies (Exposure Draft: About US, (2019).

IFRS interpretation committee and IASB after receiving the request from different

entities and preparer of financial statements, committee has recommended to IFRS Foundation to

see this issue and provide possible remedies. It has been mentioned that IASB has started the

maintain project that will provide detailed clarification on the requirement of unconditional right

to defer the settlement of liabilities. This exposure draft will seek to make necessary amendments

in the classification of liabilities through amending para 69 of IAS1. The main purpose of

Part 2: Exposure Draft

This section will review the exposure draft that has been introduced by IFRS Foundation

on “Classification of Liabilities”. This exposure draft has been introduced in February 2015 as

“Exposure Draft ED/2015/1: Classification of Liabilities” and main purpose of this exposure

draft to make proposed changes to IAS 1. Exposure draft has been opened for public review and

comment letters are welcomed by IFRS Foundation till June 10, 2015 (IFRS Foundation:

Exposure Draft: ED/2015/1, 2015). IFRS Foundation is an international organization works to

issue, modify and maintain the International Accounting Standards for the purpose of

contributing in the development of global financial markets and economic activities in

international context.

A: Accounting Issues that has been identified in the exposure draft and changes that has

been introduced the selected exposure draft

The exposure draft ED/2015/1: Classification of Liabilities has been introduced to make

specific changes in the accounting standard IAS1: Presentation of Financial Statements. Initially

IAS1 requires entities to classify their liabilities as current liabilities (Short term liabilities)

unless entity has an unconditional right to postpone the liabilities settlement after 12 months.

Many requests have been received by the various entities around the world to IFRS interpretation

committee that they find it difficult to judge on which liabilities has to treat current or non-

current due to presence of ambiguity in its classification. Due to this issue, there have been cases

where entities classify same liabilities under different heading (Current and Non-Current). It

create situation hard for the investors to understand and compare financial statements of different

companies (Exposure Draft: About US, (2019).

IFRS interpretation committee and IASB after receiving the request from different

entities and preparer of financial statements, committee has recommended to IFRS Foundation to

see this issue and provide possible remedies. It has been mentioned that IASB has started the

maintain project that will provide detailed clarification on the requirement of unconditional right

to defer the settlement of liabilities. This exposure draft will seek to make necessary amendments

in the classification of liabilities through amending para 69 of IAS1. The main purpose of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

exposure draft is to benefit the people and help them promote healthy compassion of different

companies (Exposure Draft: About US, (2019).

B: Behavior of Regulator by the use of Public Interest Theory

The public interest theory has been developed in context of the accounting regulation for

explaining the behavior of regulators for developing and introducing a respective legislation. The

theoretical framework of public interest has stated that regulators should introduce a proposed

legislation if it seeks to provide benefits to the general public. It should not in any form promote

the attainment of private interests of specific groups or driven by maximizing the personal

benefits of the regulators (Deegan, 2014). The IFRS Foundation has been established for serving

the public interests and ensuring the protection of interest of all the stakeholders of a corporation.

The Australian Accounting Standards Board (AASB) complies with the IFRS standard in

development and maintenance of accounting standards and legislations. AASB contributes to the

development of global financial reporting standards and ensuring that Australian business

entities comply with all the IFRS legislations and practices for the development of their

accounting standards.

The IFRS foundations is responsible for the development and introduction of

international accounting standards that promotes to maximize the general interests of the public

and should not seek to maximize the interests of any specific group. The governing body of IFRS

ensures that the process of establishing accounting standards remain independent and is not

impacted by the commercial interests of any specific stakeholder group. As such, it can be said

that exposure draft proposing changes within the accounting standard IAS it seeks to maximize

the public interest by enriching the quality of financial reports. The more clarification in regards

to identification of current and non-current liabilities as stated within the exposure draft will help

in meeting the general interests of public by providing them true and fair view of the financial

position of a company in terms of it meeting its short or long-term debt obligations. This in

specific will provide large help to the investors for gaining an insight into the type of liabilities

possessed by an entity and thus facilitating their decision-making process (IFRS: How we work

in the public interest, 2019).

exposure draft is to benefit the people and help them promote healthy compassion of different

companies (Exposure Draft: About US, (2019).

B: Behavior of Regulator by the use of Public Interest Theory

The public interest theory has been developed in context of the accounting regulation for

explaining the behavior of regulators for developing and introducing a respective legislation. The

theoretical framework of public interest has stated that regulators should introduce a proposed

legislation if it seeks to provide benefits to the general public. It should not in any form promote

the attainment of private interests of specific groups or driven by maximizing the personal

benefits of the regulators (Deegan, 2014). The IFRS Foundation has been established for serving

the public interests and ensuring the protection of interest of all the stakeholders of a corporation.

The Australian Accounting Standards Board (AASB) complies with the IFRS standard in

development and maintenance of accounting standards and legislations. AASB contributes to the

development of global financial reporting standards and ensuring that Australian business

entities comply with all the IFRS legislations and practices for the development of their

accounting standards.

The IFRS foundations is responsible for the development and introduction of

international accounting standards that promotes to maximize the general interests of the public

and should not seek to maximize the interests of any specific group. The governing body of IFRS

ensures that the process of establishing accounting standards remain independent and is not

impacted by the commercial interests of any specific stakeholder group. As such, it can be said

that exposure draft proposing changes within the accounting standard IAS it seeks to maximize

the public interest by enriching the quality of financial reports. The more clarification in regards

to identification of current and non-current liabilities as stated within the exposure draft will help

in meeting the general interests of public by providing them true and fair view of the financial

position of a company in terms of it meeting its short or long-term debt obligations. This in

specific will provide large help to the investors for gaining an insight into the type of liabilities

possessed by an entity and thus facilitating their decision-making process (IFRS: How we work

in the public interest, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

C: Outlining the Views Presented in Comment Letters by Highlighting the Areas of

Agreement and Disagreement in reference to Exposure Draft

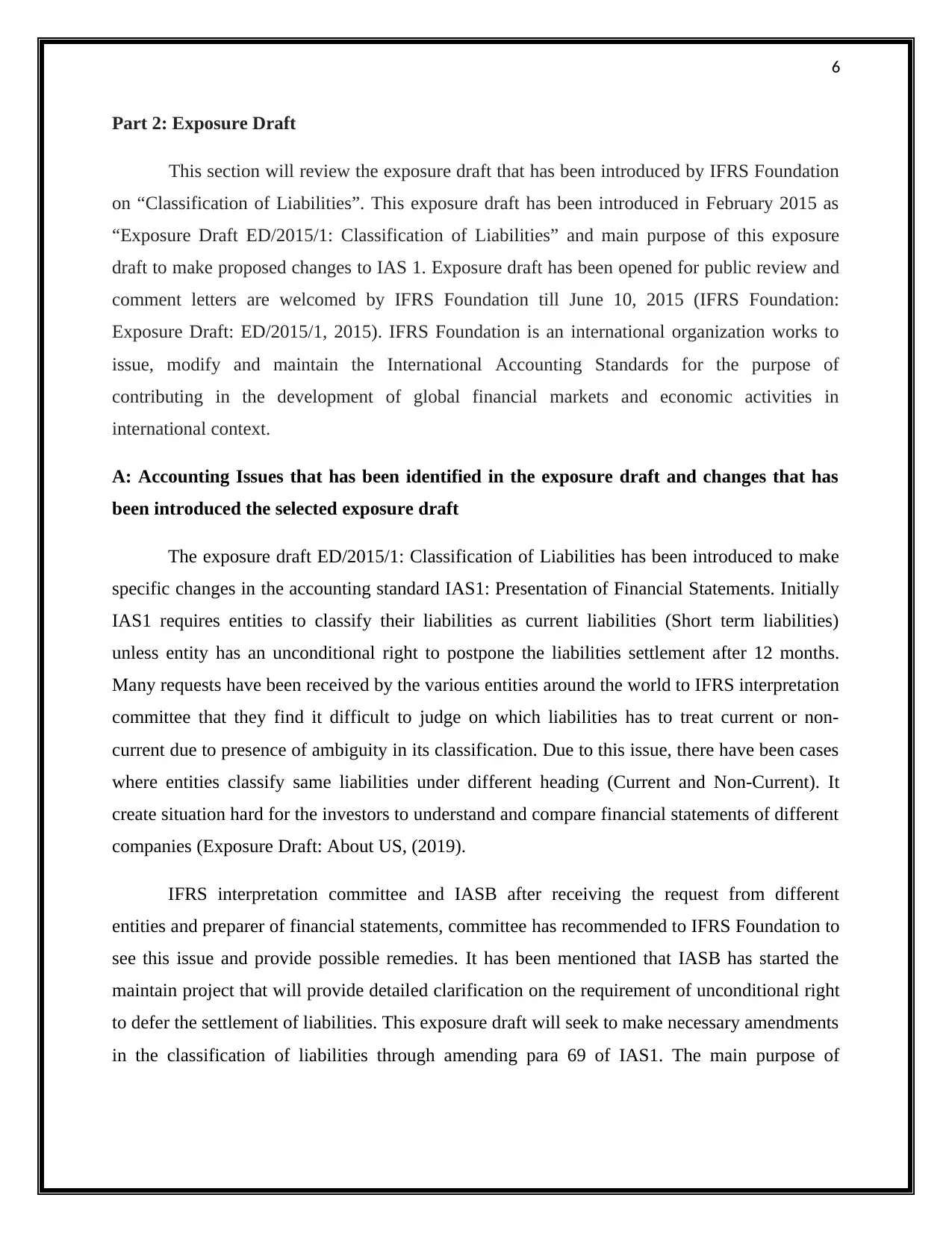

The selected exposure draft has presented three main questions to be addressed by the

respondents through their comment letters which are depicted as below:

Figure 1: Exposure Draft ED/2015/1: Classification of Liabilities (IFRS Foundation:

Exposure Draft: ED/2015/1, 2015)

Institute of Certified Public Accountants in Israel

C: Outlining the Views Presented in Comment Letters by Highlighting the Areas of

Agreement and Disagreement in reference to Exposure Draft

The selected exposure draft has presented three main questions to be addressed by the

respondents through their comment letters which are depicted as below:

Figure 1: Exposure Draft ED/2015/1: Classification of Liabilities (IFRS Foundation:

Exposure Draft: ED/2015/1, 2015)

Institute of Certified Public Accountants in Israel

9

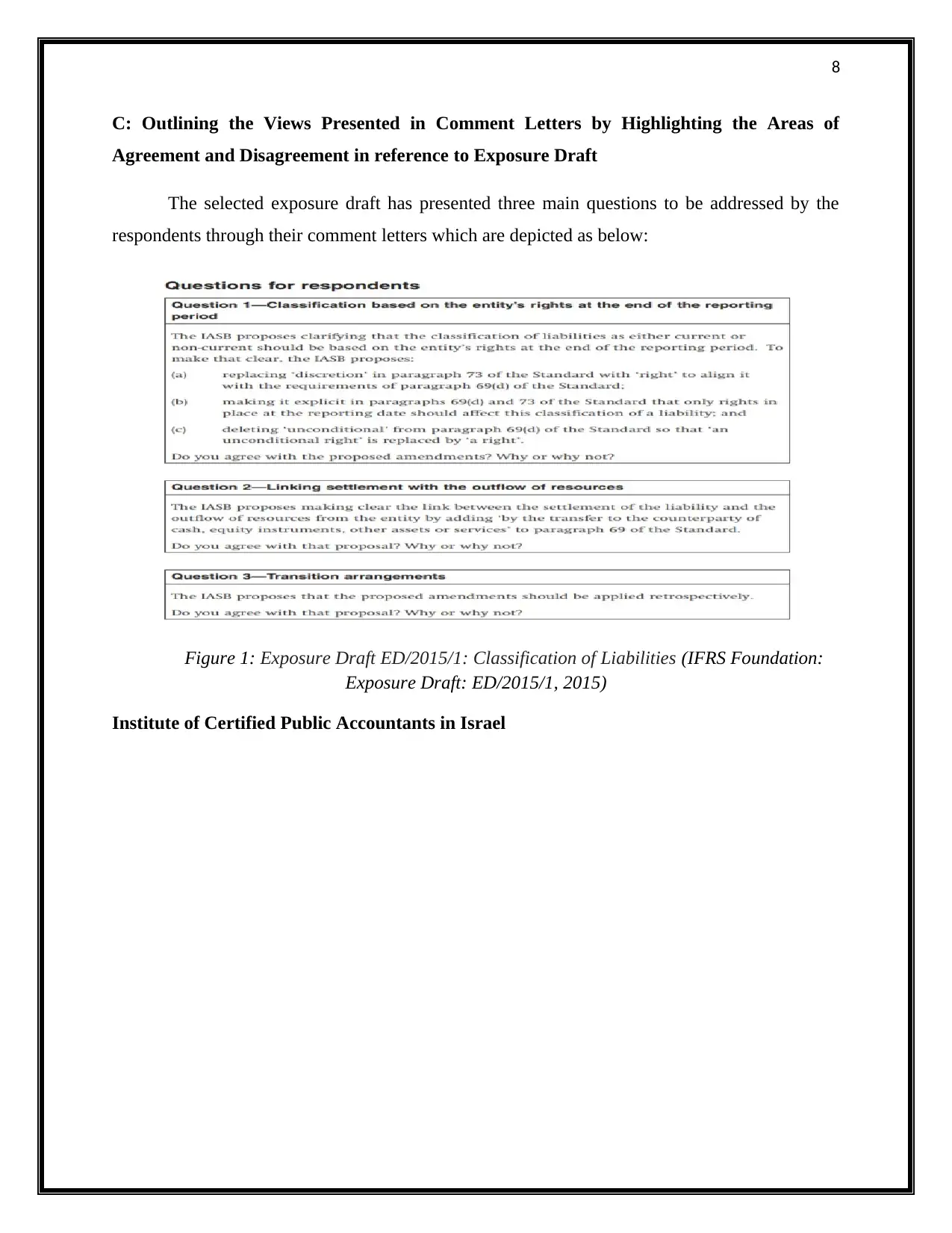

Figure 2: Exposure Draft ED/2015/1: Classification of Liabilities (Ratzkovsky, 2015)

The comment letter provided by the Institute of Certified Public Accountants in Israel has

stated in reference to exposure draft that it agrees with the proposed changes in the IASB

standards for classification of liabilities. However, it has required clarification in regard to the

notion of transferring equity instruments to the counterparty and stating the equity instruments

held by a reporting entity to be identified separately that are used for settlement of a liability

(Ratzkovsky, 2015, p. 2).

Certified Public Accountants

Figure 2: Exposure Draft ED/2015/1: Classification of Liabilities (Ratzkovsky, 2015)

The comment letter provided by the Institute of Certified Public Accountants in Israel has

stated in reference to exposure draft that it agrees with the proposed changes in the IASB

standards for classification of liabilities. However, it has required clarification in regard to the

notion of transferring equity instruments to the counterparty and stating the equity instruments

held by a reporting entity to be identified separately that are used for settlement of a liability

(Ratzkovsky, 2015, p. 2).

Certified Public Accountants

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

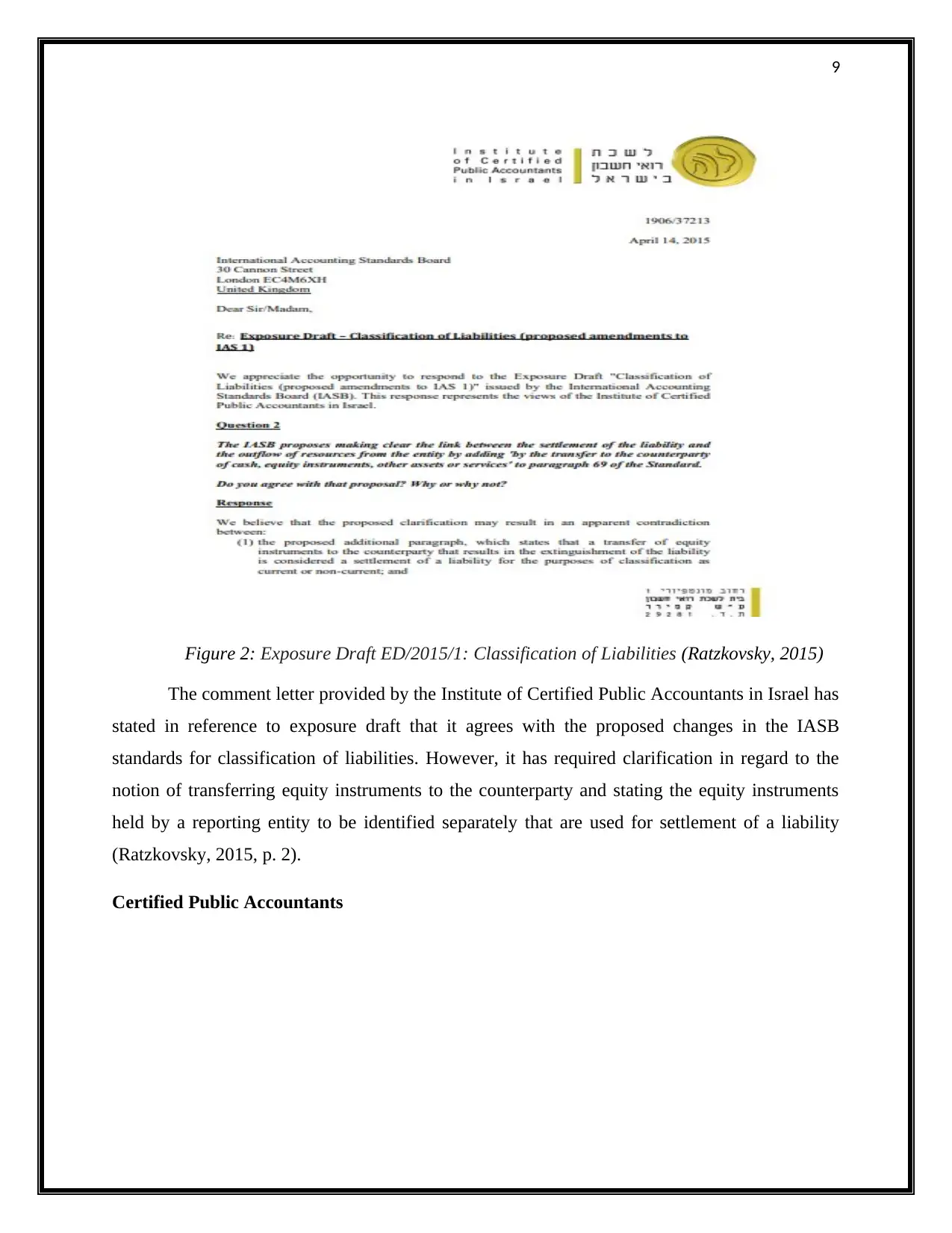

Figure 3: Exposure Draft ED/2015/1: Classification of Liabilities (Roxburgh, 2015)

This comment letter provided by the CPA has agreed to the proposed amendment stated

within the first question of the exposure draft relating to classification of the liabilities on the

basis of entity rights at the end of reporting period. It also approves the second requirement that

links settlement with the outflow of resources and also complies with the third question pointed

in the exposure draft relating to applying the changes retrospectively for maintaining consistency

with the accounting standards (Roxburgh, 2015, p.1).

The Linde Group

Figure 3: Exposure Draft ED/2015/1: Classification of Liabilities (Roxburgh, 2015)

This comment letter provided by the CPA has agreed to the proposed amendment stated

within the first question of the exposure draft relating to classification of the liabilities on the

basis of entity rights at the end of reporting period. It also approves the second requirement that

links settlement with the outflow of resources and also complies with the third question pointed

in the exposure draft relating to applying the changes retrospectively for maintaining consistency

with the accounting standards (Roxburgh, 2015, p.1).

The Linde Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Figure 4: Exposure Draft ED/2015/1: Classification of Liabilities (Schneider, 2015)

Linde Group, a world-leading gas and engineering company involved in developing its

consolidated financial statements as per the IFRS standards adopted by the European Union

(EU). The Group in this comment letter has appreciated the efforts that have been made by the

IASB in context of the amending changes in the IAS 1 accounting standard. It has provided its

agreements in regard to all the issues pointed within the above stated three questions mentioned

within the exposure draft (Schneider, 2015, p.2).

Grant Thornton

Figure 4: Exposure Draft ED/2015/1: Classification of Liabilities (Schneider, 2015)

Linde Group, a world-leading gas and engineering company involved in developing its

consolidated financial statements as per the IFRS standards adopted by the European Union

(EU). The Group in this comment letter has appreciated the efforts that have been made by the

IASB in context of the amending changes in the IAS 1 accounting standard. It has provided its

agreements in regard to all the issues pointed within the above stated three questions mentioned

within the exposure draft (Schneider, 2015, p.2).

Grant Thornton

12

Figure 5: Exposure Draft ED/2015/1: Classification of Liabilities (Sharp, 2015)

Grant Thornton International Ltd has also provided its views in regard to the issues

discussed within the exposure draft regarding the classification of liabilities. It has provided its

support to the proposed changes within the standard as it would help in seeking clarification for

the companies to classify their liabilities as current or non-current. However, it has required for

more clarification in respect of the proposed changes in the paragraph 69 and has stated that

classification of liabilities should be based on expected outflows of resources. In addition to this,

it also seeks for providing additional guidance for application of the proposed changes in a

retrospective format (Sharp, 2015, p. 1-2).

D: Application of Regulatory Theories to Explain the Comment Letters

The public interest theory is major theory of regulation that has been developed for

explaining the behavior of regulators and seeking to examine whether the proposed regulation

will result in providing the benefits to the public in comparison to the costs incurred. It

emphasizes that the introduction of a regulation should aim to maximize the general interest of

Figure 5: Exposure Draft ED/2015/1: Classification of Liabilities (Sharp, 2015)

Grant Thornton International Ltd has also provided its views in regard to the issues

discussed within the exposure draft regarding the classification of liabilities. It has provided its

support to the proposed changes within the standard as it would help in seeking clarification for

the companies to classify their liabilities as current or non-current. However, it has required for

more clarification in respect of the proposed changes in the paragraph 69 and has stated that

classification of liabilities should be based on expected outflows of resources. In addition to this,

it also seeks for providing additional guidance for application of the proposed changes in a

retrospective format (Sharp, 2015, p. 1-2).

D: Application of Regulatory Theories to Explain the Comment Letters

The public interest theory is major theory of regulation that has been developed for

explaining the behavior of regulators and seeking to examine whether the proposed regulation

will result in providing the benefits to the public in comparison to the costs incurred. It

emphasizes that the introduction of a regulation should aim to maximize the general interest of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.