Accounting Assignment: Analysis of Spanish Company Financials

VerifiedAdded on 2022/08/21

|8

|879

|16

Homework Assignment

AI Summary

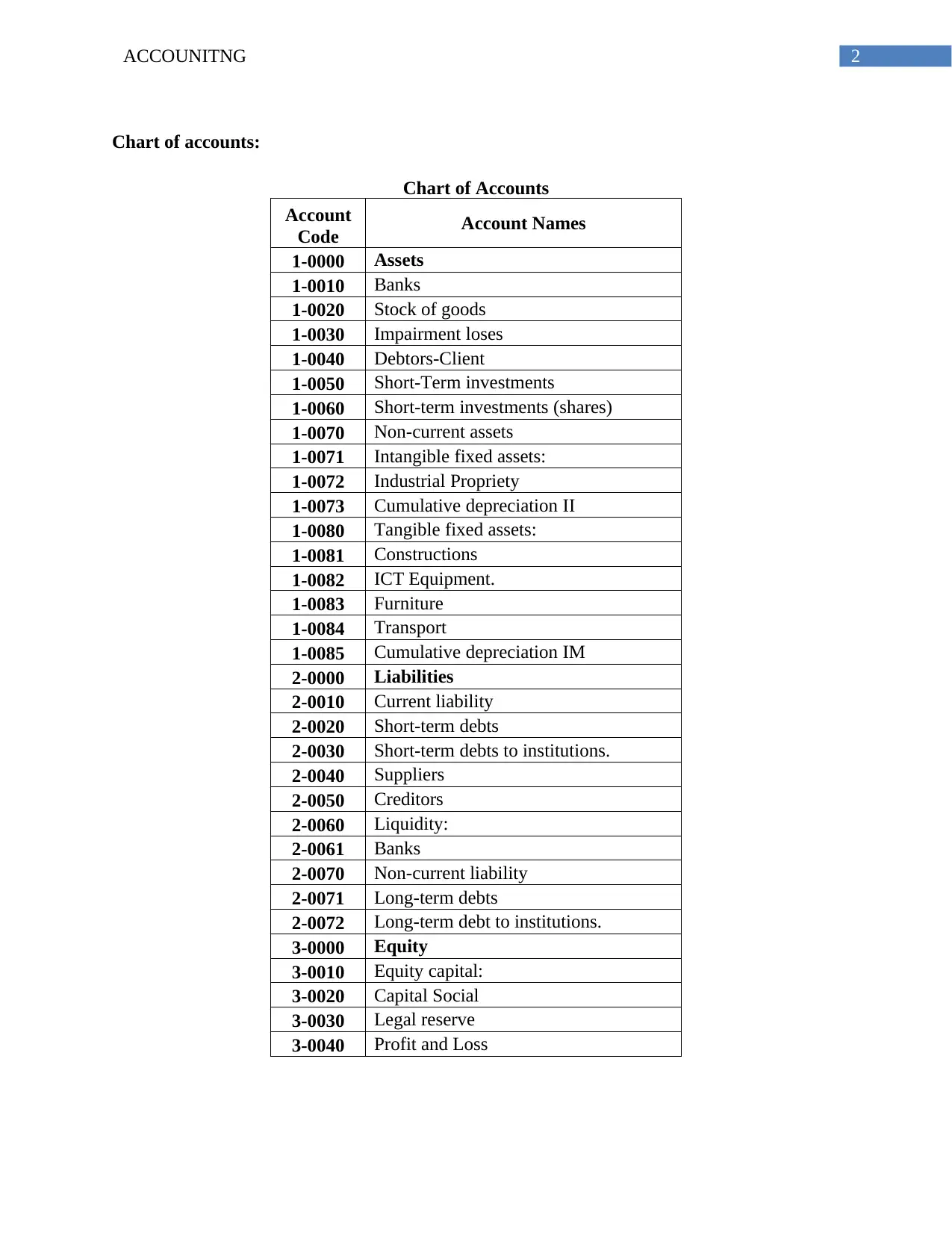

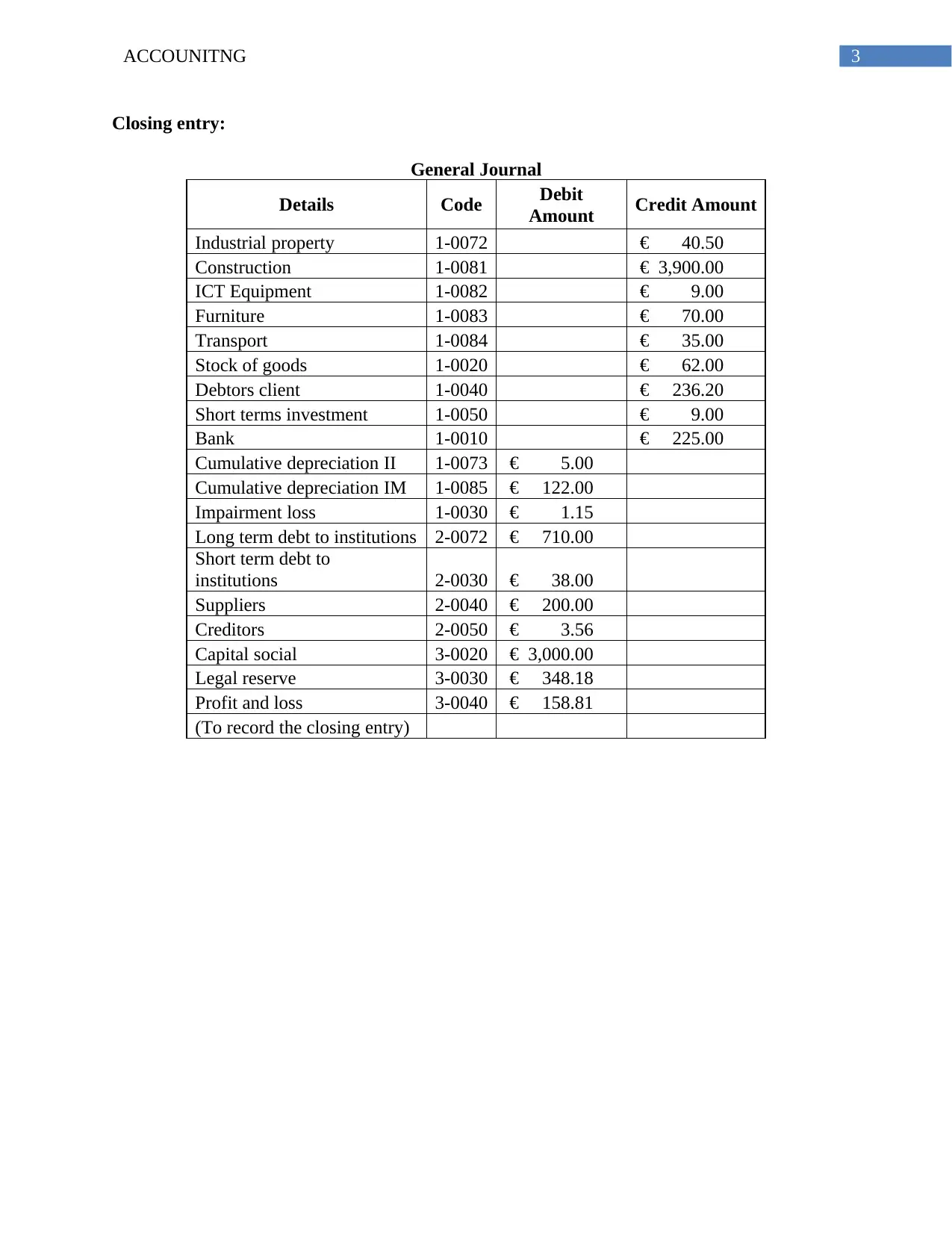

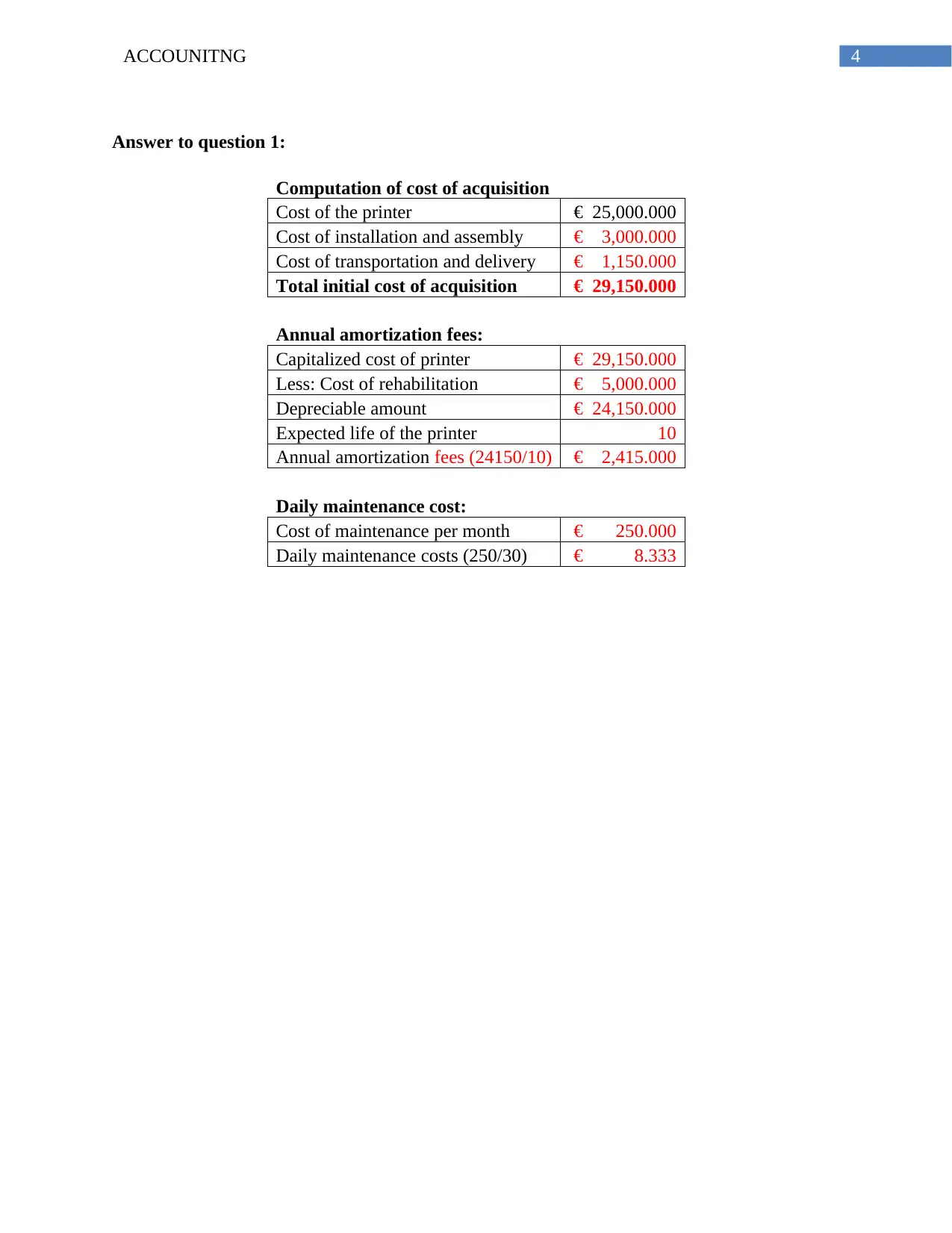

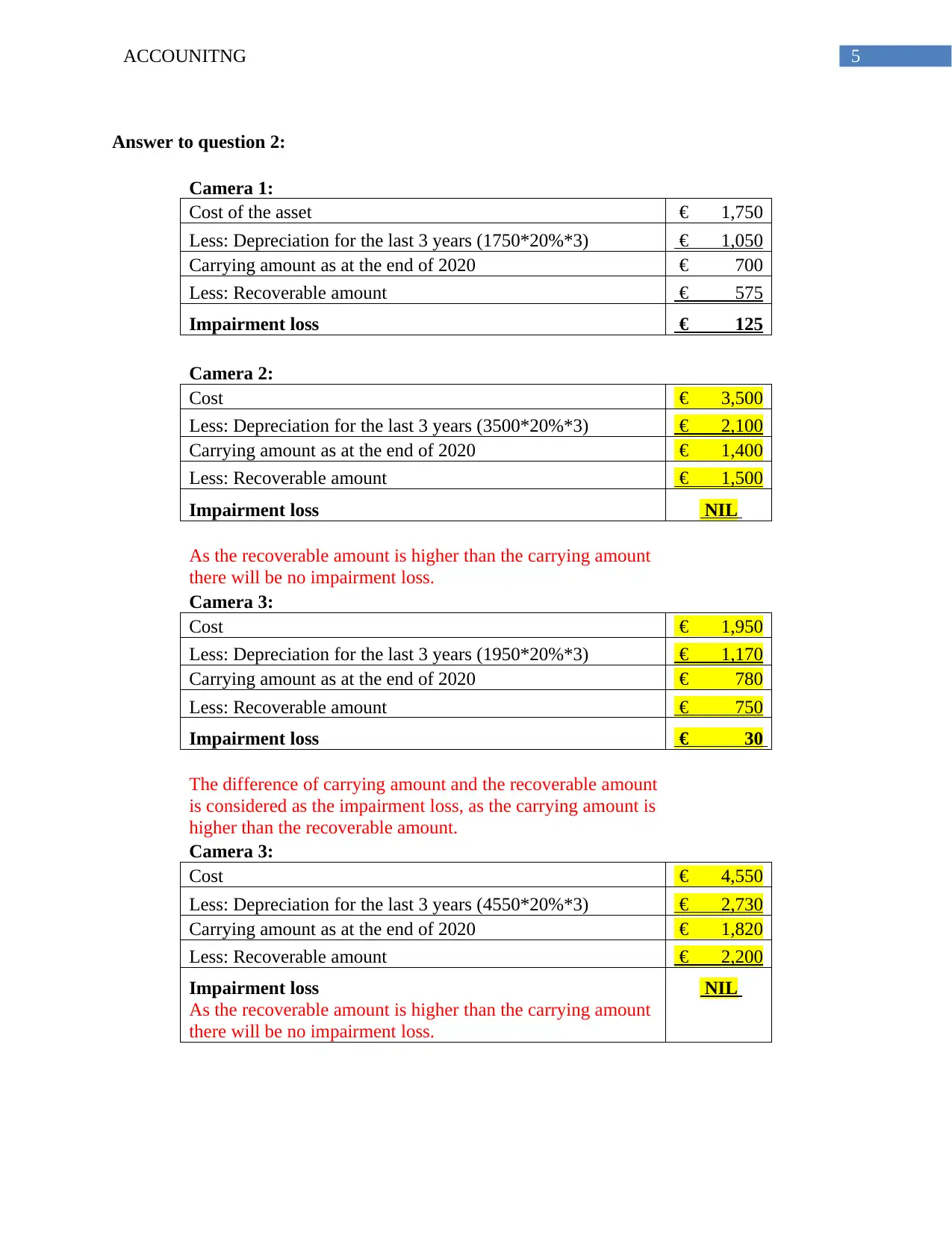

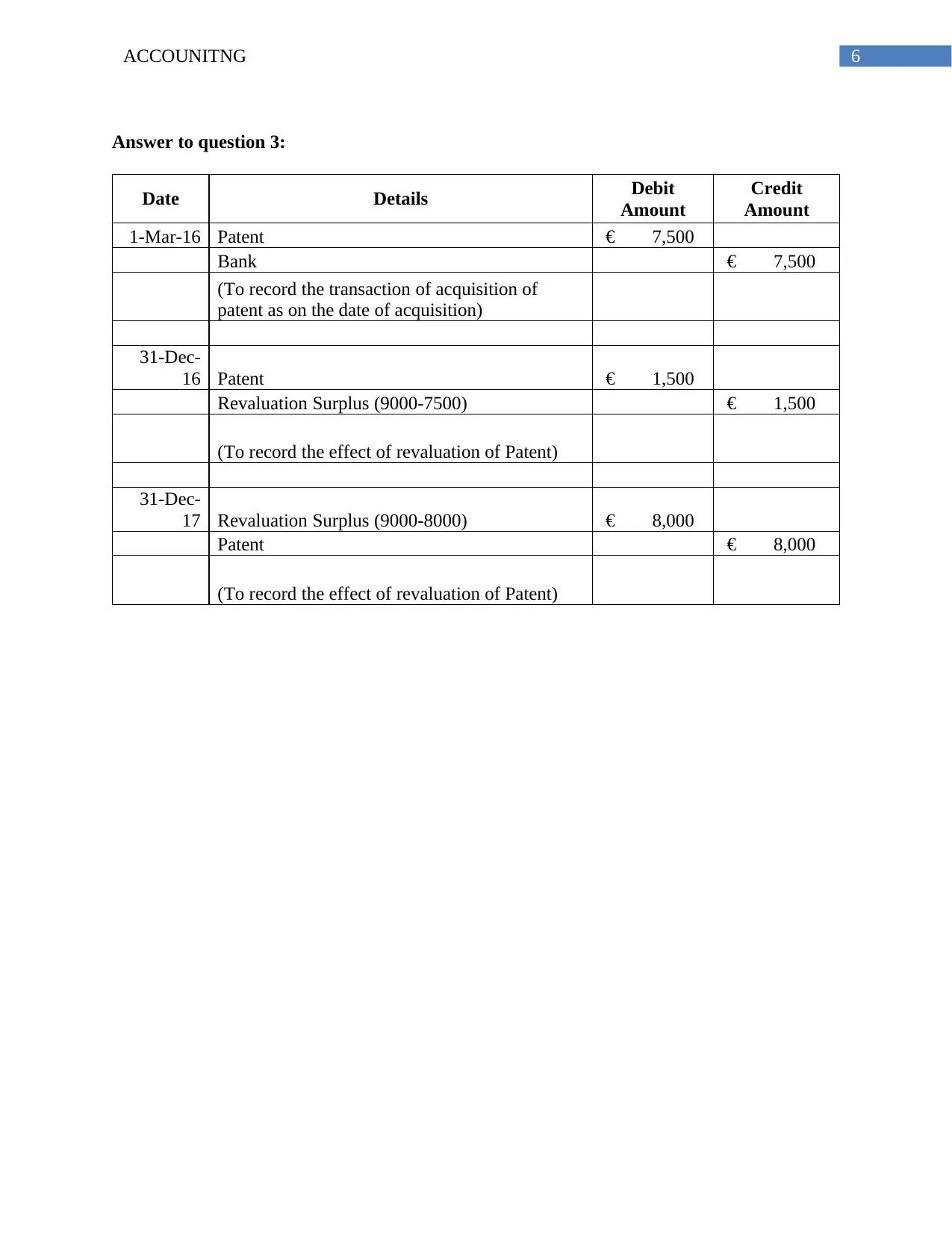

This accounting assignment analyzes the balance sheet of a Spanish company, requiring the student to categorize each item according to the Chart of Accounts and create the closing entry. The assignment includes a detailed chart of accounts, the closing entry with debits and credits, and answers to questions regarding asset valuation, depreciation, and impairment losses. The student calculates the cost of acquisition and annual amortization fees for a printer, determines impairment losses for different cameras, and records patent revaluation transactions. The document includes a bibliography of relevant accounting literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.