Accounting for Managers: ABC Department Clothing Line Analysis Report

VerifiedAdded on 2023/04/05

|5

|415

|232

Report

AI Summary

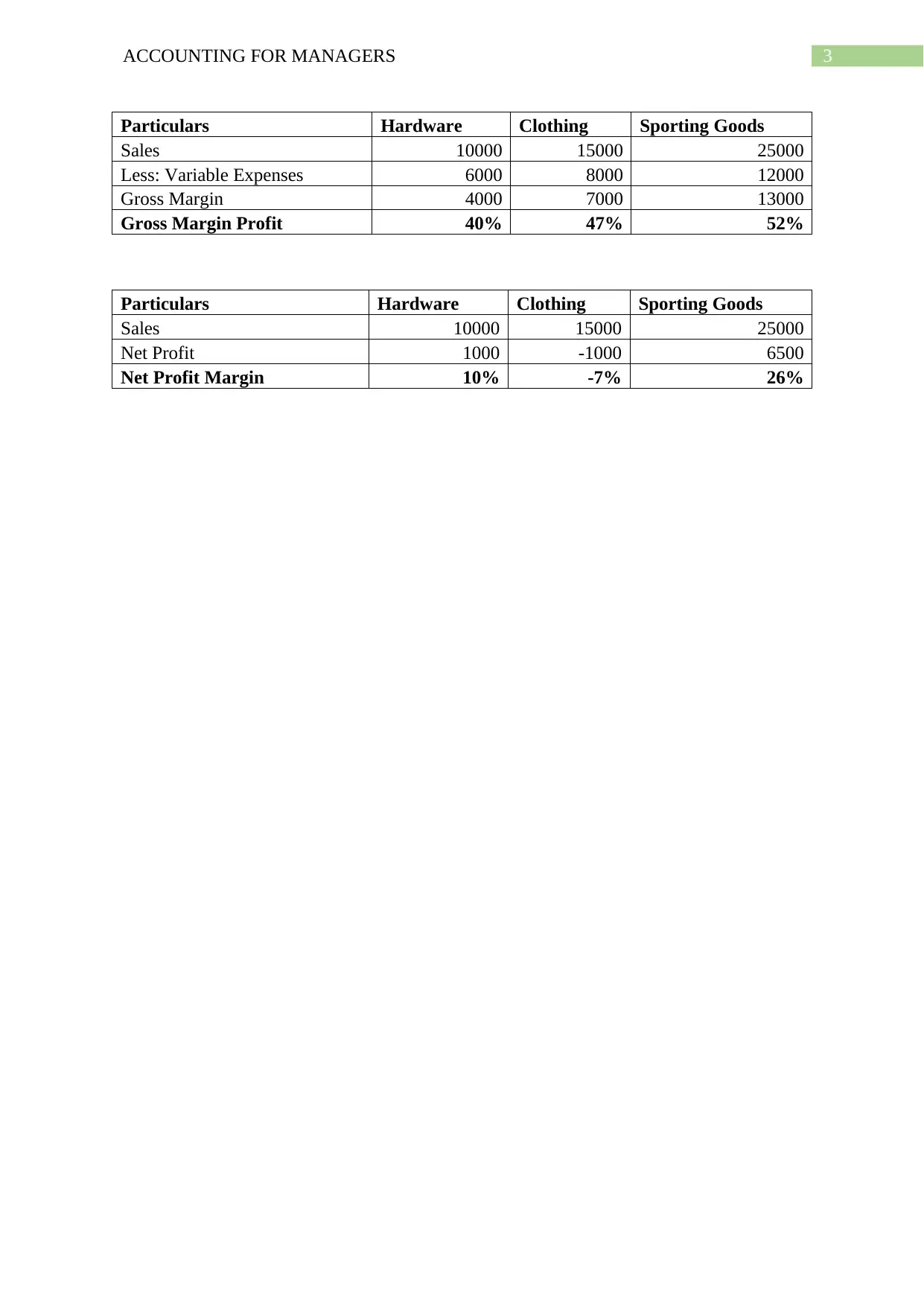

This report analyzes the financial performance of the ABC department's clothing line, which is considering being dropped due to reported losses. The analysis includes an examination of sales revenue, variable expenses, and fixed costs, highlighting that the clothing line's revenue covers direct costs but not allocated overhead. The report emphasizes the importance of cost allocation and suggests that the clothing line should not be dropped. Recommendations include increasing sales volume, cost-cutting measures, and adopting a pricing policy to attract customers and improve profitability. The report also includes an income statement that details sales, variable expenses, gross margin, and net profit for the hardware, clothing, and sporting goods product lines, along with their respective profit margins. The report concludes with a discussion on the potential for increasing sales and profitability through efficient operations and strategic pricing.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.