Community Engagement and Value Addition for Accounting Professionals

VerifiedAdded on 2023/06/04

|3

|623

|360

Project

AI Summary

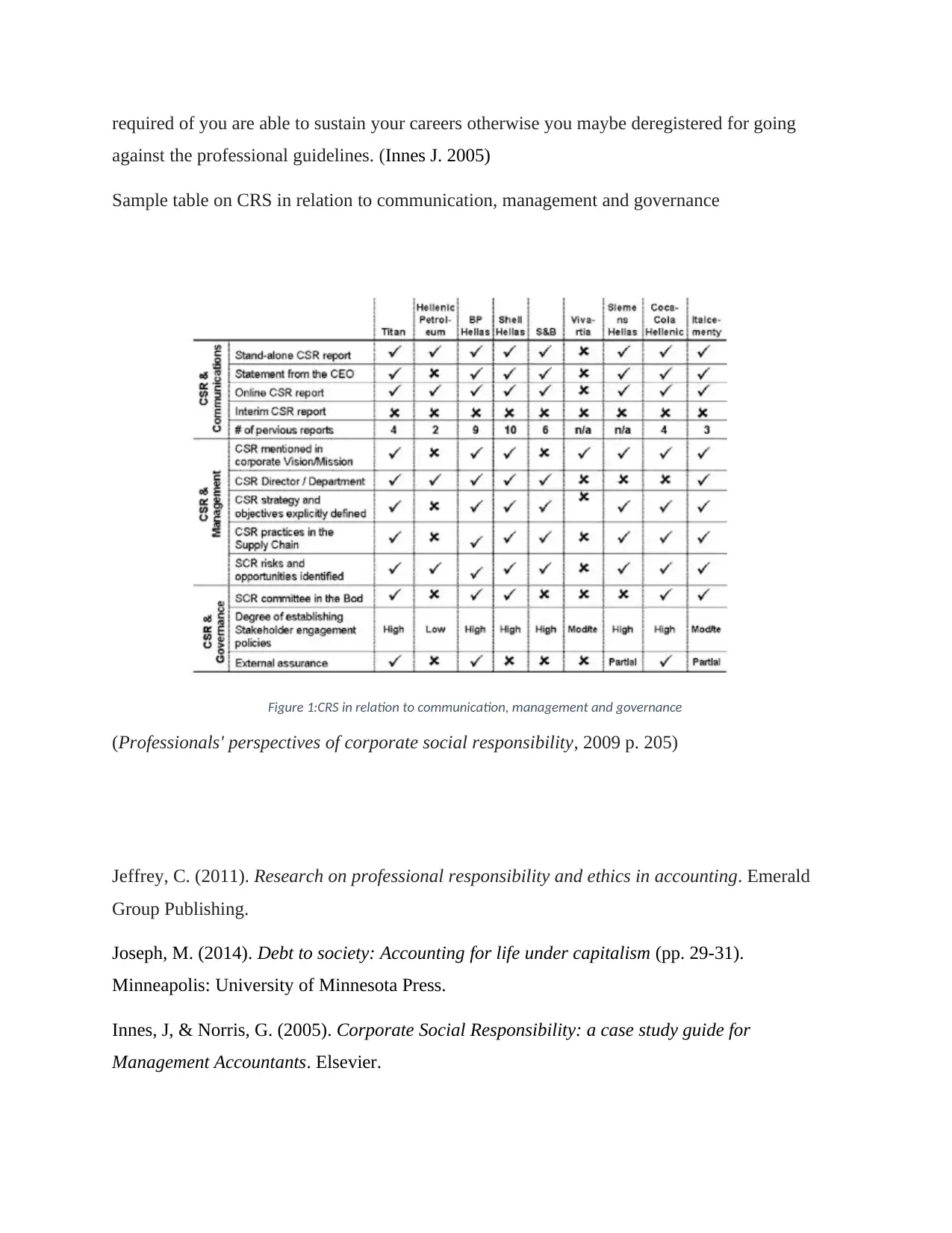

This project examines how accounting professionals engage with the community to add value to stakeholders and themselves. It emphasizes the importance of aligning accounting practices with community needs and long-term sustainability, moving beyond short-term profit goals. The assignment highlights the role of accounting professionals in promoting Corporate Social Responsibility (CSR) through policy implementation, performance management system changes, and transparent financial reporting. It discusses how these actions build trust, enhance a company's public image, and ultimately add value to stakeholders. The project also stresses the importance of professional integrity and adherence to ethical guidelines in maintaining a successful career in accounting, referencing various academic sources and figures to illustrate key concepts like the relationship between CSR, management, and governance.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.