ACC301: Analysis of Contemporary Accounting Framework Issues

VerifiedAdded on 2022/09/22

|11

|716

|25

Report

AI Summary

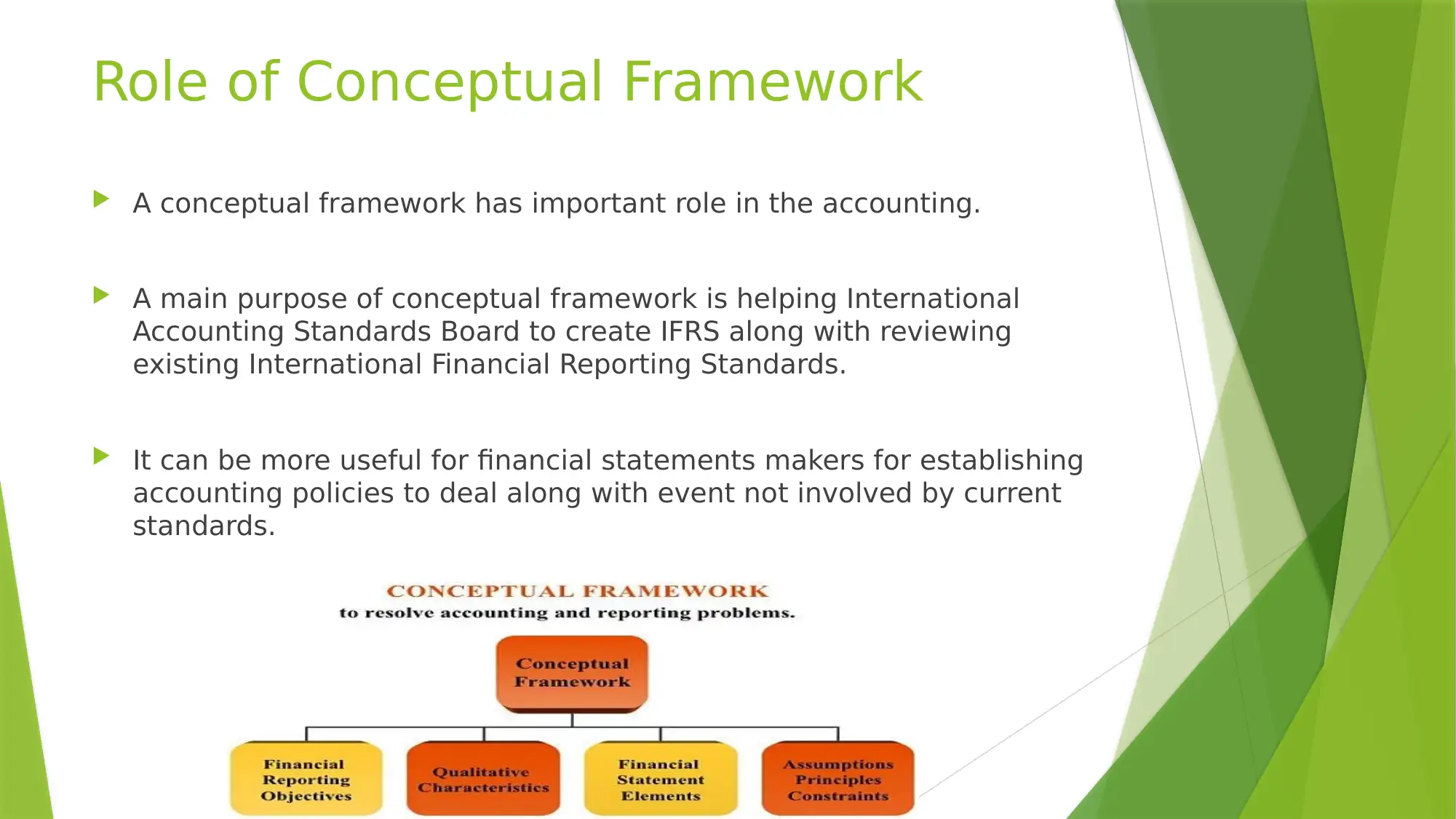

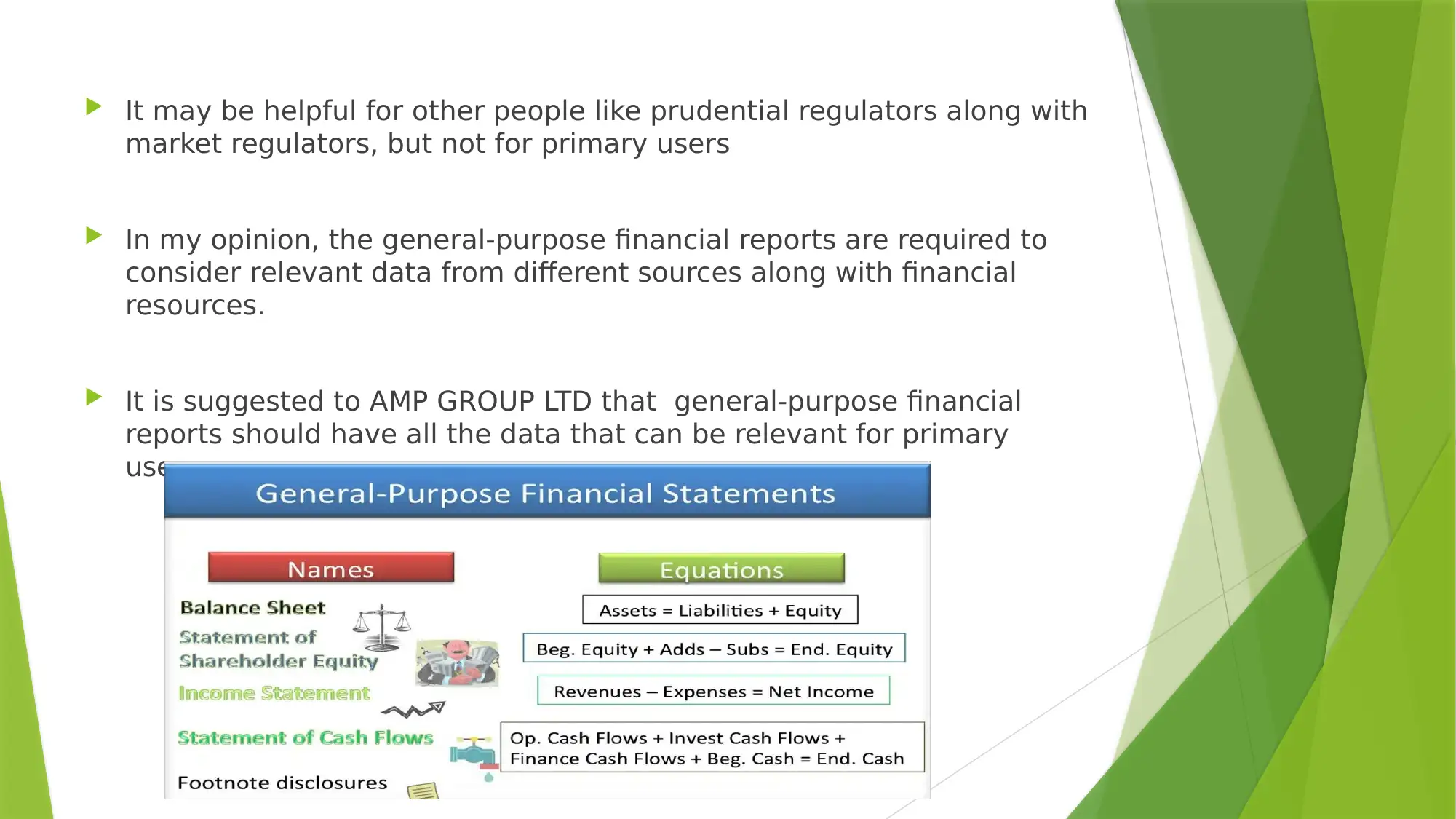

This report analyzes the revised (2018) conceptual framework for financial reporting, focusing on its role in assisting the IASB in creating and reviewing IFRS, and its utility for financial statement makers. It addresses criticisms of the 2010 framework, highlighting issues such as lack of clarity and insufficient data for users. The report examines key concepts like general-purpose financial reporting, emphasizing the need for relevant data for primary users. It also discusses prudence, including asymmetrical prudence, and the importance of substance over form. The report uses references to support its analysis, providing a comprehensive overview of the framework's evolution and key elements. The report provides a critical review of the conceptual framework, offering suggestions for improvement and highlighting its importance in financial reporting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.