Company Accounting Report: Tax, Business Combinations, Consolidation

VerifiedAdded on 2021/02/19

|16

|3028

|17

Report

AI Summary

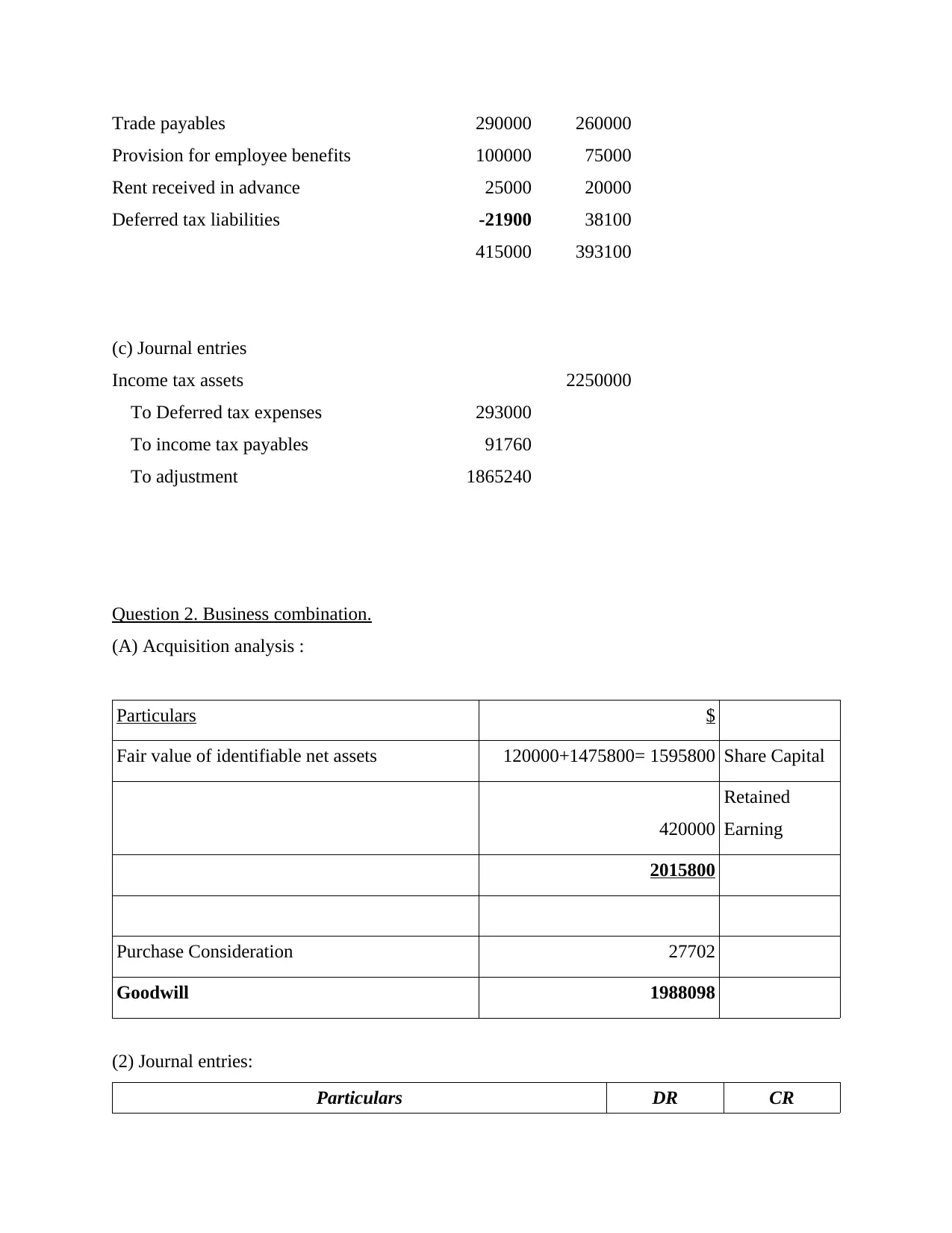

This report delves into key aspects of company accounting, providing a comprehensive analysis of various financial concepts. It begins with an examination of tax effect accounting, including the calculation of current and deferred tax liabilities and assets, supported by detailed working notes and journal entries. The report then explores business combinations, analyzing acquisition scenarios, purchase considerations, and goodwill calculations, along with relevant journal entries. The discussion extends to consolidation accounting, outlining the process, importance, and steps involved, including inter-company transactions and financial statement adjustments. The report also covers the consolidation of financial statements, including worksheet entries, elimination of investment, and goodwill impairment. Finally, the report addresses non-controlling interests, including goodwill calculations, journal entries, and elimination of inter-company transactions. The report uses a mix of calculations, journal entries, and explanations to cover these topics.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.