Accounting Consolidation Report: Intra-Group Transactions and NCI

VerifiedAdded on 2023/02/01

|14

|3014

|37

Report

AI Summary

This report provides a comprehensive overview of accounting consolidation, focusing on intra-group transactions and non-controlling interests (NCI). It begins by explaining the elimination of intra-group transactions as per accounting regulations, including debts, claims, incomes, and expenditures. The report then delves into the equity method of accounting, detailing its application when a company has significant influence over another, and illustrates the relevant journal entries. Furthermore, it addresses the calculation of goodwill in consolidation, the treatment of NCI, and the requirements of AASB 127 concerning the elimination of intra-group transactions. The report also highlights the importance of reconciliation in the consolidation process and explores the concept of NCI, explaining its representation in financial statements and its impact on the parent company's reporting. Finally, the report covers the required disclosures for non-controlling interests, including ownership percentages and the application of accounting standards such as IAS 8 and IFRS 10.

ACCOUNTING 1

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 2

Executive summary:

This report talks about the process of consolidation and the need and the rules that have been

laid down under the process of consolidation. The need and the logic behind eliminating all

of the intra group transactions has been discussed. Further, the meaning of the non-

controlling interest and the way the same is calculated and the same is reported is also

discussed in this report.

Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................4

Part B:.........................................................................................................................................5

Part C:.........................................................................................................................................6

Conclusion:................................................................................................................................8

References..................................................................................................................................9

Executive summary:

This report talks about the process of consolidation and the need and the rules that have been

laid down under the process of consolidation. The need and the logic behind eliminating all

of the intra group transactions has been discussed. Further, the meaning of the non-

controlling interest and the way the same is calculated and the same is reported is also

discussed in this report.

Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................4

Part B:.........................................................................................................................................5

Part C:.........................................................................................................................................6

Conclusion:................................................................................................................................8

References..................................................................................................................................9

ACCOUNTING 3

Introduction:

As per the rules that have been laid down under the schedule 6 of the Accounting

Regulations, there is a requirement of the elimination of all of the intra group transactions

when the group accounts of two or more companies are being prepared. There has to be an

elimination of all of the debts and the claims along with the incomes and the expenditures

which are connected with the transactions to the entities included in the process of

consolidation. Further, the profits and the losses on all of the transactions have to be

eliminated to the tune these are included in the book value of the assets. The elimination of

these entries are done in the proportion of the shares held by the investor company in the

investee company. The company (JKY Ltd) needs to follow the requirements of the AASB.

Introduction:

As per the rules that have been laid down under the schedule 6 of the Accounting

Regulations, there is a requirement of the elimination of all of the intra group transactions

when the group accounts of two or more companies are being prepared. There has to be an

elimination of all of the debts and the claims along with the incomes and the expenditures

which are connected with the transactions to the entities included in the process of

consolidation. Further, the profits and the losses on all of the transactions have to be

eliminated to the tune these are included in the book value of the assets. The elimination of

these entries are done in the proportion of the shares held by the investor company in the

investee company. The company (JKY Ltd) needs to follow the requirements of the AASB.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 4

Part A:

The following are the rules and the requirements as have been laid down under the AASB

framework which are applicable in the case of JKY Ltd:

The equity method of accounting is the method which is used for the investments when one

company has a significant influence or control over another company. But when we say

significant control, it doesn’t mean a full control. This is the case when there is an existence

of some relationship between the parent company and the subsidiary. This does not mean the

relationship between the two companies as in the consolidation of financial statements.

An investor would be considered to have a significant influence when there is a control over

the investor by the investor. An investor is considered to have some significant control over

the investor when the investor owns between 20 to 50% of the share capital of the investee. In

the case wherein an investor holds less than 20% of the share capital of the investee, then the

investor could still go on to use the equity method inspite of the cost method. In the equity

method, there is no consolidation or any process of elimination. Under this method, an

investor would report his proportionate share in the equity of the investee as an investment

and that too at cost. The amount of the investment would be increased by the share of the

profit and loss and this amount would be on proportion of the shares of the investor in the

investee. This is known as the equity pick up. The amount of the dividend which has been

paid by the investor would be subtracted from the investment amount of the investor (ACCA

global, 2019).

In order to illustrate, if A company purchases 30% shares of B company, and if the company

reports an income of $ 100,000 and also the dividend of $50,000, then the A company would

report investments under the head of “Investments in associates or affiliates".

Part A:

The following are the rules and the requirements as have been laid down under the AASB

framework which are applicable in the case of JKY Ltd:

The equity method of accounting is the method which is used for the investments when one

company has a significant influence or control over another company. But when we say

significant control, it doesn’t mean a full control. This is the case when there is an existence

of some relationship between the parent company and the subsidiary. This does not mean the

relationship between the two companies as in the consolidation of financial statements.

An investor would be considered to have a significant influence when there is a control over

the investor by the investor. An investor is considered to have some significant control over

the investor when the investor owns between 20 to 50% of the share capital of the investee. In

the case wherein an investor holds less than 20% of the share capital of the investee, then the

investor could still go on to use the equity method inspite of the cost method. In the equity

method, there is no consolidation or any process of elimination. Under this method, an

investor would report his proportionate share in the equity of the investee as an investment

and that too at cost. The amount of the investment would be increased by the share of the

profit and loss and this amount would be on proportion of the shares of the investor in the

investee. This is known as the equity pick up. The amount of the dividend which has been

paid by the investor would be subtracted from the investment amount of the investor (ACCA

global, 2019).

In order to illustrate, if A company purchases 30% shares of B company, and if the company

reports an income of $ 100,000 and also the dividend of $50,000, then the A company would

report investments under the head of “Investments in associates or affiliates".

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 5

The following would be journal entries that would be recorded:

Dr. Investments in Associates

Cr. Cash

A company received the dividend of $15,000 which amounts to $50,000 and this amount of

the dividend received would be reduced from the amount of an investment. The sole reason

for the same is the fact that the same has been received from the invested.

The following would be its journal entry:

Dr. Cash

Cr. Investments in Associates

In the end, A company would record the following net income and this would increase the

investment amount:

Dr. Investments in Associates

Cr. Investment Revenue

(Corporate finance institute, 2019).

The following would be journal entries that would be recorded:

Dr. Investments in Associates

Cr. Cash

A company received the dividend of $15,000 which amounts to $50,000 and this amount of

the dividend received would be reduced from the amount of an investment. The sole reason

for the same is the fact that the same has been received from the invested.

The following would be its journal entry:

Dr. Cash

Cr. Investments in Associates

In the end, A company would record the following net income and this would increase the

investment amount:

Dr. Investments in Associates

Cr. Investment Revenue

(Corporate finance institute, 2019).

ACCOUNTING 6

In the consolidation method, the amount of the goodwill is calculated by subtracting the

amount of the net assets of the investee from the consideration of the investor. The incomes

and the expenses would accrue in the proportion if the share capital which has been held with

the minority interest or the non-controlling interest. All of the assets and the liabilities would

be reported in the books of the parent company which has sole major influence on the

operations of the investee (Small business chron, 2019).

Under the equity method, the company which is investing into the investee company would

combine its books to report its control over the investee to the extent of equity share capital,

reserves and the retained earnings. The apt method to be used would depend upon one

scenario to another. In case, the company has a major control over the subsidiary including

the voting rights and also has a major influence including the controlling of the voting rights,

then the board of directors would decide to consolidate its financial statements (PWC, 2019).

Part B:

As per the relevant requirements of the AASB 127 which relates with the Consolidated and

Separate Financial Statements, any sort of intra group transactions or any transaction with

regard to the incomes, expenses, and dividends have to be completely eliminated from the

financial statements of the companies. The profits and the losses which are the result of the

intra group transactions will have to be recognised as assets such as the inventory and the

fixed assets. Any amount of the losses which occur due to the losses due to the transactions

entered into between the two companies, which may be the result of an impairment on the

assets would require a recognition in the consolidated financial statements. The AASB 112

which deals with the Incomes Taxes applies to the differences that arise due to the

elimination of the profits and the losses that results from these intra group transactions

(AASB, 2019).

In the consolidation method, the amount of the goodwill is calculated by subtracting the

amount of the net assets of the investee from the consideration of the investor. The incomes

and the expenses would accrue in the proportion if the share capital which has been held with

the minority interest or the non-controlling interest. All of the assets and the liabilities would

be reported in the books of the parent company which has sole major influence on the

operations of the investee (Small business chron, 2019).

Under the equity method, the company which is investing into the investee company would

combine its books to report its control over the investee to the extent of equity share capital,

reserves and the retained earnings. The apt method to be used would depend upon one

scenario to another. In case, the company has a major control over the subsidiary including

the voting rights and also has a major influence including the controlling of the voting rights,

then the board of directors would decide to consolidate its financial statements (PWC, 2019).

Part B:

As per the relevant requirements of the AASB 127 which relates with the Consolidated and

Separate Financial Statements, any sort of intra group transactions or any transaction with

regard to the incomes, expenses, and dividends have to be completely eliminated from the

financial statements of the companies. The profits and the losses which are the result of the

intra group transactions will have to be recognised as assets such as the inventory and the

fixed assets. Any amount of the losses which occur due to the losses due to the transactions

entered into between the two companies, which may be the result of an impairment on the

assets would require a recognition in the consolidated financial statements. The AASB 112

which deals with the Incomes Taxes applies to the differences that arise due to the

elimination of the profits and the losses that results from these intra group transactions

(AASB, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 7

These intra group transactions form the part of the process of consolidation since these entries

have to be completely eliminated at the time of the consolidation. This forms a core part of

the close of the financial statements. These transactions are effective cut off tracking and

require the differences which are the result of the disputes and the arbitration (IAS plus,

2019). The result of the process of reconciliation can work in many ways when it comes to

the process of closing and also improves the reliability of the financial statements. The term

optimisation refers to the sources of all of the potential differences that need to be identified.

There are many of the financial and the commercial transactions that include the two

companies from the same industry to work side by side. An example of this is the issuance of

the sales invoice when any product is sold or any service is rendered. The company that has

rendered the service or sold the product would report as a receivable and the company to

which that invoice has been issued would report it as a payable, but when the companies are

working side by side, it is not recommended that these companies report the same amount as

a receivables and as payable, since that would be illogical. So, when the process of

consolidation takes place for these companies, these entries are eliminated in full. As on the

closing date of the balance sheet, the consolidated balance sheet or the financial statements

would include the assets and the liabilities which is the result of the reciprocal transactions

that does not exist within the group. If these entries are not eliminated, then it would mean an

overstatement or the overvaluation of the income and the overestimation of the expenses.

The process of searching for these account balances are tough for the consolidation manager

(Signma consco, 2019).

The financial statements of the two companies are consolidated as if they were functioning as

a separate company or as a single company. The various effects of the transactions between

these entities would be eliminated in full. Also FRS 102 requires the elimination of these

These intra group transactions form the part of the process of consolidation since these entries

have to be completely eliminated at the time of the consolidation. This forms a core part of

the close of the financial statements. These transactions are effective cut off tracking and

require the differences which are the result of the disputes and the arbitration (IAS plus,

2019). The result of the process of reconciliation can work in many ways when it comes to

the process of closing and also improves the reliability of the financial statements. The term

optimisation refers to the sources of all of the potential differences that need to be identified.

There are many of the financial and the commercial transactions that include the two

companies from the same industry to work side by side. An example of this is the issuance of

the sales invoice when any product is sold or any service is rendered. The company that has

rendered the service or sold the product would report as a receivable and the company to

which that invoice has been issued would report it as a payable, but when the companies are

working side by side, it is not recommended that these companies report the same amount as

a receivables and as payable, since that would be illogical. So, when the process of

consolidation takes place for these companies, these entries are eliminated in full. As on the

closing date of the balance sheet, the consolidated balance sheet or the financial statements

would include the assets and the liabilities which is the result of the reciprocal transactions

that does not exist within the group. If these entries are not eliminated, then it would mean an

overstatement or the overvaluation of the income and the overestimation of the expenses.

The process of searching for these account balances are tough for the consolidation manager

(Signma consco, 2019).

The financial statements of the two companies are consolidated as if they were functioning as

a separate company or as a single company. The various effects of the transactions between

these entities would be eliminated in full. Also FRS 102 requires the elimination of these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

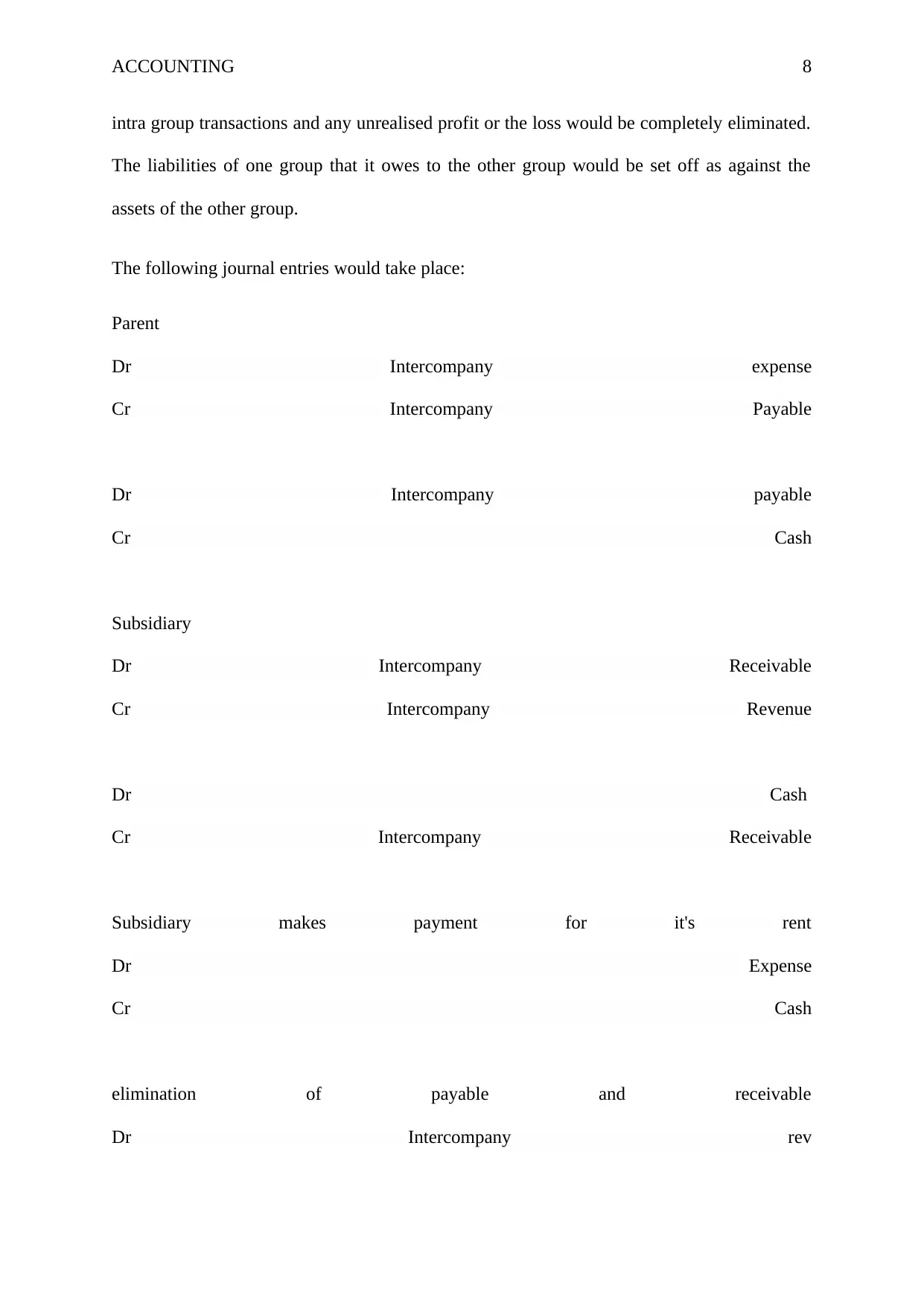

intra group transactions and any unrealised profit or the loss would be completely eliminated.

The liabilities of one group that it owes to the other group would be set off as against the

assets of the other group.

The following journal entries would take place:

Parent

Dr Intercompany expense

Cr Intercompany Payable

Dr Intercompany payable

Cr Cash

Subsidiary

Dr Intercompany Receivable

Cr Intercompany Revenue

Dr Cash

Cr Intercompany Receivable

Subsidiary makes payment for it's rent

Dr Expense

Cr Cash

elimination of payable and receivable

Dr Intercompany rev

intra group transactions and any unrealised profit or the loss would be completely eliminated.

The liabilities of one group that it owes to the other group would be set off as against the

assets of the other group.

The following journal entries would take place:

Parent

Dr Intercompany expense

Cr Intercompany Payable

Dr Intercompany payable

Cr Cash

Subsidiary

Dr Intercompany Receivable

Cr Intercompany Revenue

Dr Cash

Cr Intercompany Receivable

Subsidiary makes payment for it's rent

Dr Expense

Cr Cash

elimination of payable and receivable

Dr Intercompany rev

ACCOUNTING 9

Cr Intercompany exp

elimination of the revenue and expenses

Part C:

A non-controlling interest is also known as the minority interest which is the position of

ownership wherein the shareholder of the company owns less than 50% of the shares of the

company and is able to influence the management instead of controlling them.

This is the amount of the share capital of the investee company which is owned by the

outsiders. This is apart from the parent company. This amount of the sum total of the share

capital, reserves, etc are not owned by the parent company. The investor company would

always report this amount in the financial statements of the investee company in the

consolidated balance sheet. This represents the claim on the assets by the minority

shareholders and also in the consolidated statement of income as being the % of the profits

which is with the minority shareholders. These minority shareholders have a lesser amount of

influence on the management and the policies of the company and also, they have a very

limited number of voting rights. But they offer some significant growth with their experience

and capital, hence they are considered to be important. These are reported in the balance

sheet separately in the “Liabilities” section of the financial statements of the companies (My

accounting course, 2019).

A consolidation of the financial statements is considered to be the set of combined accounting

record that puts together the financials of the two companies. These include the parent

company as being the majority owner, the subsidiary or the purchased firm and the non-

controlling interest company. These companies are assumed to be separate companies when

consolidation is not done (Corporate finance institute, 2019).

Cr Intercompany exp

elimination of the revenue and expenses

Part C:

A non-controlling interest is also known as the minority interest which is the position of

ownership wherein the shareholder of the company owns less than 50% of the shares of the

company and is able to influence the management instead of controlling them.

This is the amount of the share capital of the investee company which is owned by the

outsiders. This is apart from the parent company. This amount of the sum total of the share

capital, reserves, etc are not owned by the parent company. The investor company would

always report this amount in the financial statements of the investee company in the

consolidated balance sheet. This represents the claim on the assets by the minority

shareholders and also in the consolidated statement of income as being the % of the profits

which is with the minority shareholders. These minority shareholders have a lesser amount of

influence on the management and the policies of the company and also, they have a very

limited number of voting rights. But they offer some significant growth with their experience

and capital, hence they are considered to be important. These are reported in the balance

sheet separately in the “Liabilities” section of the financial statements of the companies (My

accounting course, 2019).

A consolidation of the financial statements is considered to be the set of combined accounting

record that puts together the financials of the two companies. These include the parent

company as being the majority owner, the subsidiary or the purchased firm and the non-

controlling interest company. These companies are assumed to be separate companies when

consolidation is not done (Corporate finance institute, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 10

As per the relevant requirements that have been laid down by the relevant accounting

standards, a parent would represent the non-controlling interests in the statement of

consolidation of the financial statements of the company within the equity. The % of income

which is allocated between the parent and the non-controlling interest would be determined

on the basis of the interest which represents the ownership of these companies.

There are as such no disclosure requirements under the IFRS 10 of the Accounting Standards.

Any retrospective application of the accounting standards would be done as per the IAS 8

which deals with the Accounting policies, changes in the estimates of accounting and errors.

But in case, an entity is required to make any sort of adjustments to the accounting when it

comes to the involvement of the companies, then the previously prepared consolidated

financial statements will have to be revised. The stated financial statements. But these

companies are not required to consolidate any financial statements that were unconsolidated

previously and the same would continue not to be consolidated as on the date of the

application of the IFRS.

As per the IFRS 10, the entity would still be consolidated as on the date of the consolidation,

the entity shall not be consolidated if it were not been consolidated before.

The IAS 28 deals with the Investments in the Associates and the Joint ventures (IAS plus,

2019).

The following are some of the other disclosures that are required for the non-controlling of

the minority interest:

The interest of the ownership in the various subsidiaries that are held by the parties

other than the parent company will have to be clearly identified, labelled. These have

to be reported in the consolidated financial statements within the equity which is

separate from the equity of the parent company.

As per the relevant requirements that have been laid down by the relevant accounting

standards, a parent would represent the non-controlling interests in the statement of

consolidation of the financial statements of the company within the equity. The % of income

which is allocated between the parent and the non-controlling interest would be determined

on the basis of the interest which represents the ownership of these companies.

There are as such no disclosure requirements under the IFRS 10 of the Accounting Standards.

Any retrospective application of the accounting standards would be done as per the IAS 8

which deals with the Accounting policies, changes in the estimates of accounting and errors.

But in case, an entity is required to make any sort of adjustments to the accounting when it

comes to the involvement of the companies, then the previously prepared consolidated

financial statements will have to be revised. The stated financial statements. But these

companies are not required to consolidate any financial statements that were unconsolidated

previously and the same would continue not to be consolidated as on the date of the

application of the IFRS.

As per the IFRS 10, the entity would still be consolidated as on the date of the consolidation,

the entity shall not be consolidated if it were not been consolidated before.

The IAS 28 deals with the Investments in the Associates and the Joint ventures (IAS plus,

2019).

The following are some of the other disclosures that are required for the non-controlling of

the minority interest:

The interest of the ownership in the various subsidiaries that are held by the parties

other than the parent company will have to be clearly identified, labelled. These have

to be reported in the consolidated financial statements within the equity which is

separate from the equity of the parent company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 11

There must be a clear understanding of the amount of the net income which is

attributable to the parent and which needs some presentation in the financial

statements.

Any amount of change in the non-controlling interest of the parent company will have

to be disclosed consolidated financial statements on some consistent basis. The

ownership interest in the subsidiary would go in for change in case, the parent goes in

for a purchase of some additional interest in the ownership of the subsidiary of the

company. Or, the necessary changes will have to be reported in case, the parent goes

on to sell some part of the ownership interest or goes in for issue of some additional

interest in the ownership. All of these transactions are somewhat same in nature and

the standard requires that these be accounted for some regular basis and also be

treated as the equity transactions.

Whenever any subsidiary is deconsolidated, then the amount of the retained non-

controlling equity portion of the investment of the investee company would be valued

and reported at its fair value. Any amount of the gain or the loss which arises from the

deconsolidation of this investee company would be reported as the fair value of any

non-controlling equity investment instead of being reported at its carrying value.

Any company will have to provide enough disclosures which would clearly show and

identify and separate out the interest of the parent company with that of the interests

of the owners of the non-controlling companies (FASB, 2019).

Conclusion:

In the nutshell, whenever any two companies come together in which one company takes

over the other, then it is necessary for them to show their financial statements as one and

report them as a single company. Any amount of transaction which takes place between them

There must be a clear understanding of the amount of the net income which is

attributable to the parent and which needs some presentation in the financial

statements.

Any amount of change in the non-controlling interest of the parent company will have

to be disclosed consolidated financial statements on some consistent basis. The

ownership interest in the subsidiary would go in for change in case, the parent goes in

for a purchase of some additional interest in the ownership of the subsidiary of the

company. Or, the necessary changes will have to be reported in case, the parent goes

on to sell some part of the ownership interest or goes in for issue of some additional

interest in the ownership. All of these transactions are somewhat same in nature and

the standard requires that these be accounted for some regular basis and also be

treated as the equity transactions.

Whenever any subsidiary is deconsolidated, then the amount of the retained non-

controlling equity portion of the investment of the investee company would be valued

and reported at its fair value. Any amount of the gain or the loss which arises from the

deconsolidation of this investee company would be reported as the fair value of any

non-controlling equity investment instead of being reported at its carrying value.

Any company will have to provide enough disclosures which would clearly show and

identify and separate out the interest of the parent company with that of the interests

of the owners of the non-controlling companies (FASB, 2019).

Conclusion:

In the nutshell, whenever any two companies come together in which one company takes

over the other, then it is necessary for them to show their financial statements as one and

report them as a single company. Any amount of transaction which takes place between them

ACCOUNTING 12

would have to be eliminated no matter what since the same has been laid down by the

relevant accounting standards.

The amount of the non-controlling interest is the amount which does not belong to the parent

company and this has to be reported under the head of “Equity” in the consolidated financial

statements (Croneri, 2019).

References

Aasb.gov.au. (2019). Consolidated and Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB127_03-08_ERDRjun10_07-09.pdf

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Equity Method Accounting - Definition, Explanation,

Examples. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/equity-method/

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Equity Method Accounting - Definition, Explanation,

Examples. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/equity-method/

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Non Controlling Interest (NCI) / Minority Interest -

Examples, Guide. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/non-controlling-

interest/ [Accessed 6 May 2019].

Iasplus.com. (2019). IFRS 10 — Consolidated Financial Statements. [online] Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs10 [Accessed 6 May 2019].

would have to be eliminated no matter what since the same has been laid down by the

relevant accounting standards.

The amount of the non-controlling interest is the amount which does not belong to the parent

company and this has to be reported under the head of “Equity” in the consolidated financial

statements (Croneri, 2019).

References

Aasb.gov.au. (2019). Consolidated and Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB127_03-08_ERDRjun10_07-09.pdf

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Equity Method Accounting - Definition, Explanation,

Examples. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/equity-method/

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Equity Method Accounting - Definition, Explanation,

Examples. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/equity-method/

[Accessed 6 May 2019].

Corporate Finance Institute. (2019). Non Controlling Interest (NCI) / Minority Interest -

Examples, Guide. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/non-controlling-

interest/ [Accessed 6 May 2019].

Iasplus.com. (2019). IFRS 10 — Consolidated Financial Statements. [online] Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs10 [Accessed 6 May 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.