SE-ACC220 Accounting Basics II Assignment: Liabilities and Assets

VerifiedAdded on 2023/01/17

|7

|878

|52

Homework Assignment

AI Summary

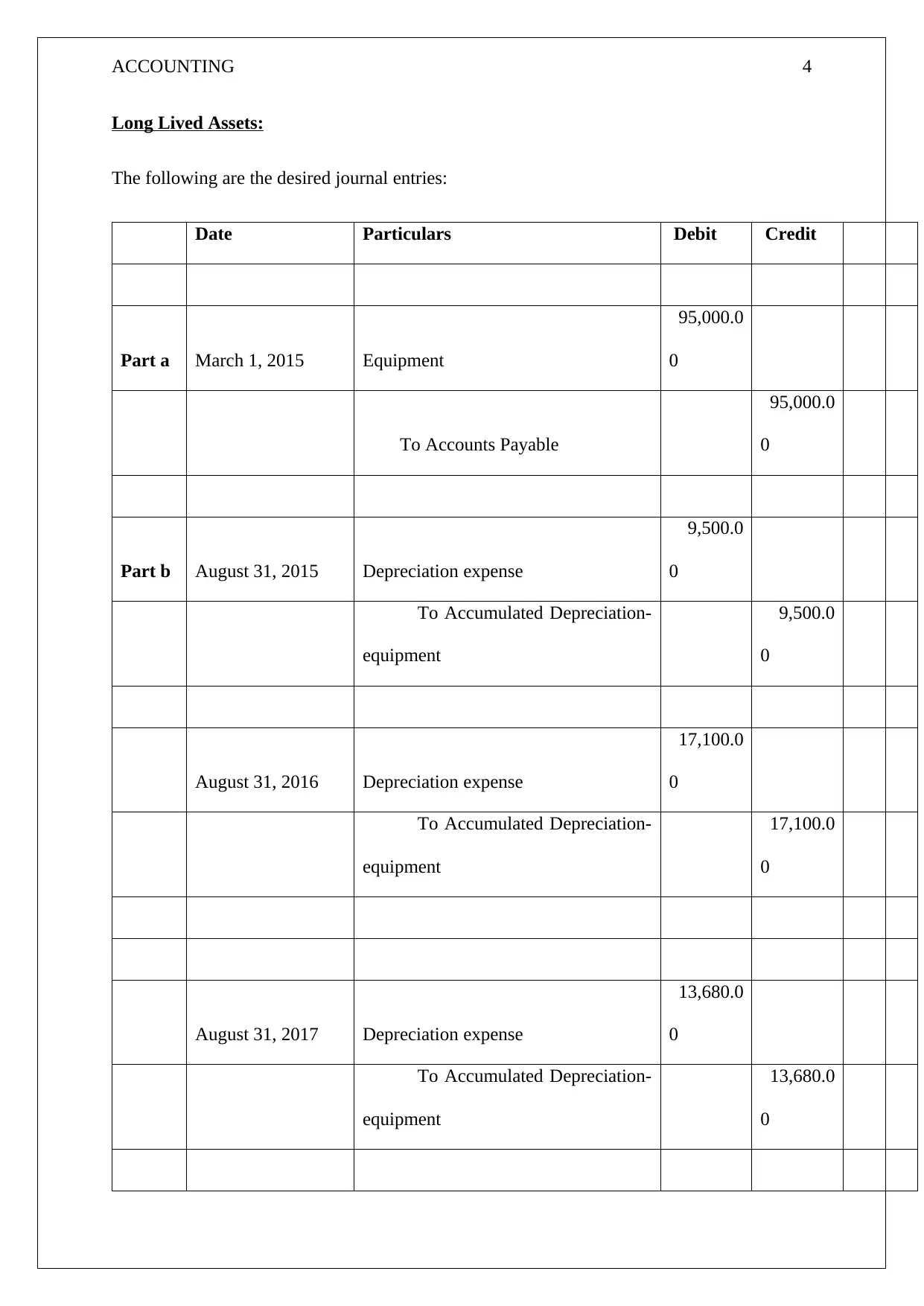

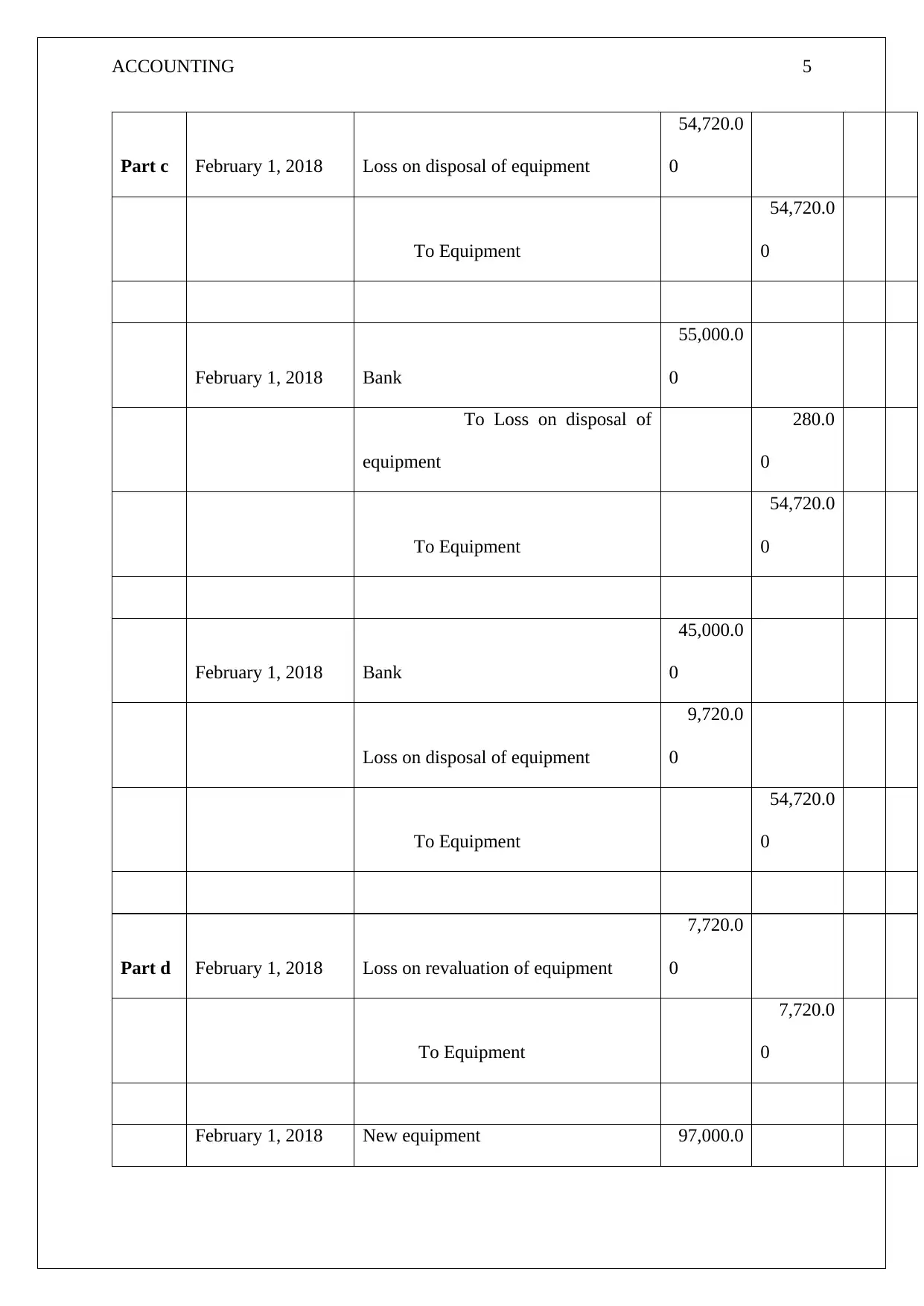

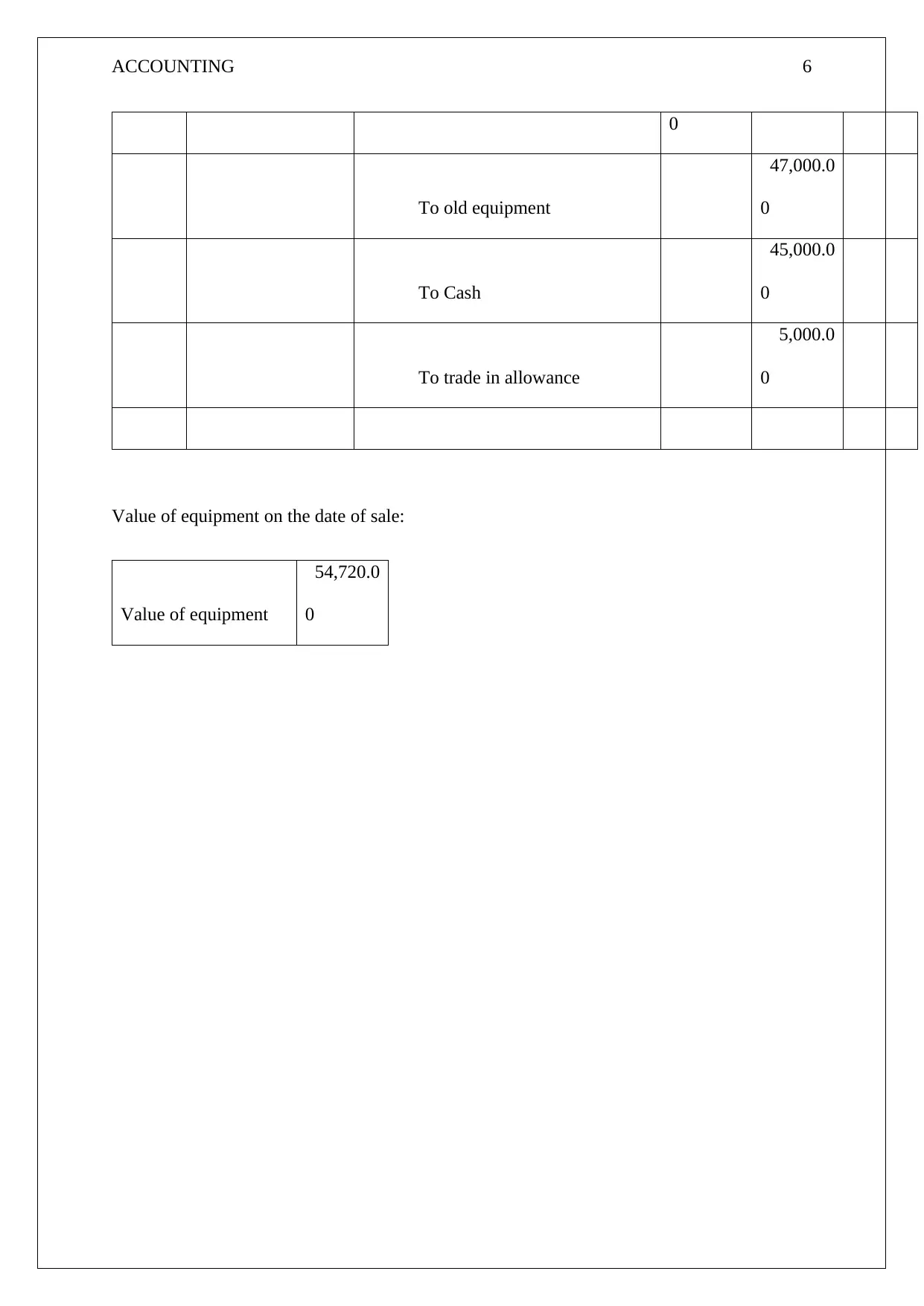

This accounting assignment addresses the complexities of contingent liabilities and long-lived assets, covering the necessary accounting treatments according to AASB standards. The assignment analyzes the scenario of Batteries4U and its environmental cleanup obligations, determining when a provision should be recorded versus disclosed. It explains the conditions under which a contingent liability is recognized, disclosed, or neither, and the importance of reliable estimation. The solution includes detailed journal entries for equipment, depreciation, and disposal, providing a comprehensive understanding of the accounting processes involved. The provided solution offers a detailed analysis of the case, including the appropriate accounting treatments and journal entries for different scenarios, such as the environmental cleanup costs and the disposal of long-lived assets. It emphasizes the importance of proper financial reporting and the application of accounting standards to real-world situations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.