Accounting for Contract Costs: AASB 15 and Terra Corporation

VerifiedAdded on 2023/04/10

|6

|784

|481

Report

AI Summary

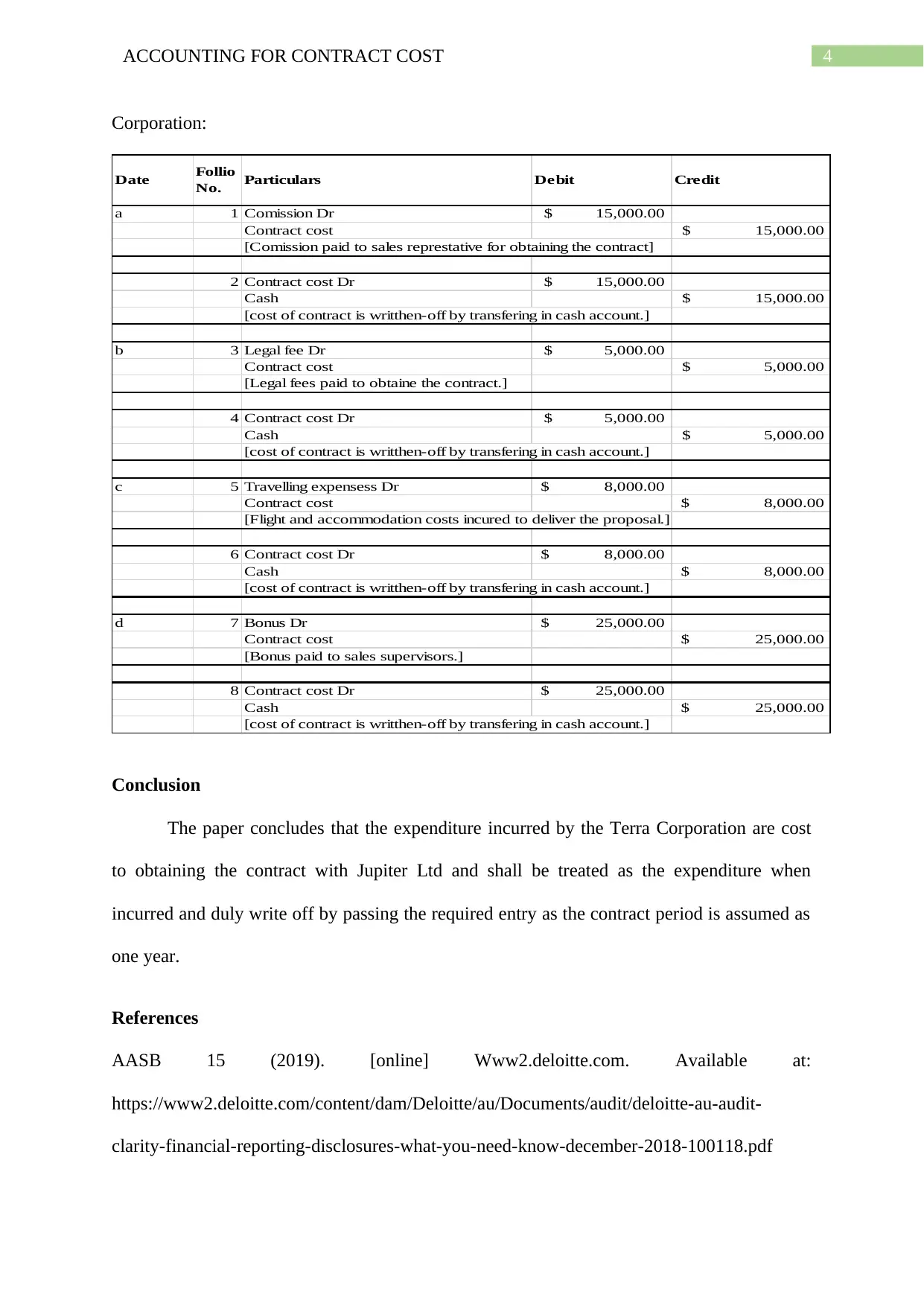

This report analyzes the accounting treatment of costs incurred by Terra Corporation to obtain a contract with Jupiter Ltd., focusing on the application of Australian Accounting Standards (AASB 15). The analysis addresses the classification of these costs as assets or expenses, referencing specific paragraphs within AASB 15. It advises treating the expenditures as expenses due to the contract's renewable one-year period. The report details the relevant journal entries for commission, legal fees, travel expenses, and bonuses, demonstrating how these costs are recorded in Terra Corporation's books. Assumptions made include the contract's one-year renewable period. The conclusion summarizes the correct accounting treatment of the expenditures and the importance of proper journal entries.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.