Comprehensive Accounting Management Report: Jeffrey & Son's Case Study

VerifiedAdded on 2020/01/28

|25

|6772

|43

Report

AI Summary

This report provides a detailed analysis of accounting management principles, focusing on cost classification, unit cost calculation, and the application of absorption costing techniques. It presents a case study of Jeffrey & Son's Ltd, calculating the cost of a product ('Exquisite') using absorption costing, and analyzes the results. The report also covers the preparation and analysis of cost reports, including variance analysis to identify areas for improvement and suggest cost reduction strategies. Furthermore, it discusses the purpose and nature of budgeting, different budgeting methods, and the preparation of various budget types, including a cash budget. The report concludes with a discussion of variance analysis, reconciliation statements, and findings for management, providing a comprehensive overview of accounting management concepts and their practical application within a business context.

Accounting Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

1.1 Description of cost classification...........................................................................................4

1.2 Calculating unit cost and total job cost..................................................................................5

1.3 Calculating the cost of Exquisite using absorption costing technique...................................5

1.4 Analyzing cost of Exquisite...................................................................................................9

TASK 2..........................................................................................................................................10

2.1 Preparing and analyzing cost report for month of September.............................................10

2.2 Using various performance indicator to identify areas of improvement.............................12

2.3 Suggesting ways to reduce cost, enhance value and quality................................................12

TASK 3..........................................................................................................................................13

3.1 Purpose and nature of budgeting process............................................................................13

3.2 Selecting appropriate budgeting methods for organization.................................................14

3.3 Preparation of different types of budget..............................................................................15

3.4 Preparing cash budget..........................................................................................................16

TASK 4..........................................................................................................................................20

4.1 Calculating variance............................................................................................................20

4.2 Preparing reconciliation operating statement......................................................................22

4.3 Findings to management in accordance with identified responsibility centres...................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................25

2

INTRODUCTION...........................................................................................................................4

1.1 Description of cost classification...........................................................................................4

1.2 Calculating unit cost and total job cost..................................................................................5

1.3 Calculating the cost of Exquisite using absorption costing technique...................................5

1.4 Analyzing cost of Exquisite...................................................................................................9

TASK 2..........................................................................................................................................10

2.1 Preparing and analyzing cost report for month of September.............................................10

2.2 Using various performance indicator to identify areas of improvement.............................12

2.3 Suggesting ways to reduce cost, enhance value and quality................................................12

TASK 3..........................................................................................................................................13

3.1 Purpose and nature of budgeting process............................................................................13

3.2 Selecting appropriate budgeting methods for organization.................................................14

3.3 Preparation of different types of budget..............................................................................15

3.4 Preparing cash budget..........................................................................................................16

TASK 4..........................................................................................................................................20

4.1 Calculating variance............................................................................................................20

4.2 Preparing reconciliation operating statement......................................................................22

4.3 Findings to management in accordance with identified responsibility centres...................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................25

2

INDEX OF TABLES

Table 1: Unit cost.............................................................................................................................5

Table 2: Allocation of cost of support departments on the basis of machine hours........................8

Table 3: Allocation of criteria of cost..............................................................................................8

Table 4: Units to be produced..........................................................................................................9

Table 5: Overhead absorption rate...................................................................................................9

Table 6: Exquisite calculation.........................................................................................................9

Table 7: Calculation of absorption rate on the basis of labor hours................................................9

Table 8: Calculation of Exquisite..................................................................................................10

Table 9: Material purchase budget................................................................................................15

Table 10: Material purchase budget of Jeffrey and Son's..............................................................16

Table 11: Cash budget...................................................................................................................16

Table 12: Reconciliation operating statement................................................................................22

3

Table 1: Unit cost.............................................................................................................................5

Table 2: Allocation of cost of support departments on the basis of machine hours........................8

Table 3: Allocation of criteria of cost..............................................................................................8

Table 4: Units to be produced..........................................................................................................9

Table 5: Overhead absorption rate...................................................................................................9

Table 6: Exquisite calculation.........................................................................................................9

Table 7: Calculation of absorption rate on the basis of labor hours................................................9

Table 8: Calculation of Exquisite..................................................................................................10

Table 9: Material purchase budget................................................................................................15

Table 10: Material purchase budget of Jeffrey and Son's..............................................................16

Table 11: Cash budget...................................................................................................................16

Table 12: Reconciliation operating statement................................................................................22

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A procedure used for the analysis and interpretation of data collected by cost and

financial accounting is termed as management accounting. The major objective of this

accounting is to help the manager for making viable decisions so that aims and objectives of the

corporate can be achieved in an effective manner. Further, this kind of accounting helps in

reducing the unnecessary expenses because; it maintains a track over all the expenses and

surplus. Moreover, through this cash flow of the firm get improvised. This report focuses on the

evaluation of several concepts of cost by considering information of Jeffrey & Son’s Ltd.

Furthermore, this report also includes the theoretical description and practical application

regarding the cost computation, budget and variance analysis.

1.1 Description of cost classification

Cost can be described as an amount paid or payable by the company or business

organization for obtaining product or services. Thus, the classification of the cost can be done on

the basis of below mentioned factors: Element: This classification is mainly based on the objectives of cost. On the basis of

which cost can be classified into direct or indirect cost. Further, direct cost can be

incurred while doing production activities such as manufacturing, acquiring raw

materials, stocking of work in progress, etc (Burns and et.al, 2004). These activities are

necessary for conducting business. Moreover, indirect cost is incurred in order to attain

economic benefit so that efficiency and profitability of the business can be enhanced.

For Example: Direct cost incurred at the time of purchasing of raw material and indirect cost can

be the amount incurred on selling and distribution expenses. Nature: As per the nature of expenses, cost can be classified into three segments that are

material, labour and overhead expenses. Through this, identification of cost classification

can be done (Dekker, 2015).

For Example: Material cost can be referred to as the amount incurred on variables that are

required for manufacturing such as raw materials. Further, labour cost involves wages and

salaries. Moreover, overhead expenses include other related expenses such rent (Kastantin,

2005).

A procedure used for the analysis and interpretation of data collected by cost and

financial accounting is termed as management accounting. The major objective of this

accounting is to help the manager for making viable decisions so that aims and objectives of the

corporate can be achieved in an effective manner. Further, this kind of accounting helps in

reducing the unnecessary expenses because; it maintains a track over all the expenses and

surplus. Moreover, through this cash flow of the firm get improvised. This report focuses on the

evaluation of several concepts of cost by considering information of Jeffrey & Son’s Ltd.

Furthermore, this report also includes the theoretical description and practical application

regarding the cost computation, budget and variance analysis.

1.1 Description of cost classification

Cost can be described as an amount paid or payable by the company or business

organization for obtaining product or services. Thus, the classification of the cost can be done on

the basis of below mentioned factors: Element: This classification is mainly based on the objectives of cost. On the basis of

which cost can be classified into direct or indirect cost. Further, direct cost can be

incurred while doing production activities such as manufacturing, acquiring raw

materials, stocking of work in progress, etc (Burns and et.al, 2004). These activities are

necessary for conducting business. Moreover, indirect cost is incurred in order to attain

economic benefit so that efficiency and profitability of the business can be enhanced.

For Example: Direct cost incurred at the time of purchasing of raw material and indirect cost can

be the amount incurred on selling and distribution expenses. Nature: As per the nature of expenses, cost can be classified into three segments that are

material, labour and overhead expenses. Through this, identification of cost classification

can be done (Dekker, 2015).

For Example: Material cost can be referred to as the amount incurred on variables that are

required for manufacturing such as raw materials. Further, labour cost involves wages and

salaries. Moreover, overhead expenses include other related expenses such rent (Kastantin,

2005).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Function: Functional activities carried out in the organization also lead to the increment

of cost. Thus, such cost can affect the profitability in a positive manner because this cost

improves the performance level of people employed in an organization.

For Example: Functional cost consists of production, marketing, administration and distribution

cost. Behaviour: The factor of behaviour can also be considered while classifying the cost. In

this, cost can be bifurcated into variable, fixed and semi-variable cost. Fixed cost remains

constant irrespective of the production units (Wildavsky, 2006). Whereas, variable cost

increases in direct proportion with number of units produced. Further, in semi-variable

cost characteristics of both fixed and variable cost are included.

For Example: Variable cost is per unit material cost, fixed cost refers to as the rental charges and

lastly; the semi-variable cost which involves the cost such as electricity expense (Youseef,

2013).

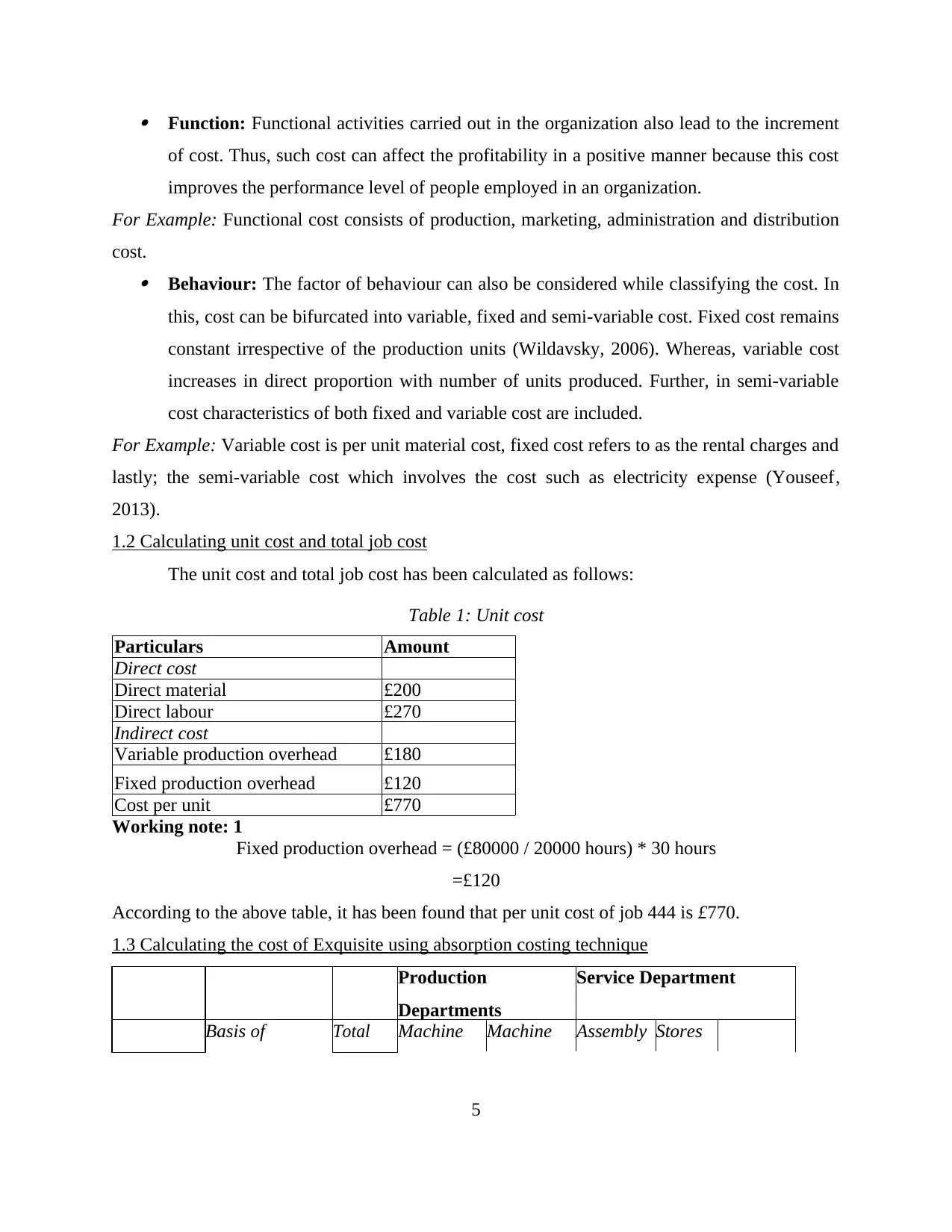

1.2 Calculating unit cost and total job cost

The unit cost and total job cost has been calculated as follows:

Table 1: Unit cost

Particulars Amount

Direct cost

Direct material £200

Direct labour £270

Indirect cost

Variable production overhead £180

Fixed production overhead £120

Cost per unit £770

Working note: 1

Fixed production overhead = (£80000 / 20000 hours) * 30 hours

=£120

According to the above table, it has been found that per unit cost of job 444 is £770.

1.3 Calculating the cost of Exquisite using absorption costing technique

Production

Departments

Service Department

Basis of Total Machine Machine Assembly Stores

5

of cost. Thus, such cost can affect the profitability in a positive manner because this cost

improves the performance level of people employed in an organization.

For Example: Functional cost consists of production, marketing, administration and distribution

cost. Behaviour: The factor of behaviour can also be considered while classifying the cost. In

this, cost can be bifurcated into variable, fixed and semi-variable cost. Fixed cost remains

constant irrespective of the production units (Wildavsky, 2006). Whereas, variable cost

increases in direct proportion with number of units produced. Further, in semi-variable

cost characteristics of both fixed and variable cost are included.

For Example: Variable cost is per unit material cost, fixed cost refers to as the rental charges and

lastly; the semi-variable cost which involves the cost such as electricity expense (Youseef,

2013).

1.2 Calculating unit cost and total job cost

The unit cost and total job cost has been calculated as follows:

Table 1: Unit cost

Particulars Amount

Direct cost

Direct material £200

Direct labour £270

Indirect cost

Variable production overhead £180

Fixed production overhead £120

Cost per unit £770

Working note: 1

Fixed production overhead = (£80000 / 20000 hours) * 30 hours

=£120

According to the above table, it has been found that per unit cost of job 444 is £770.

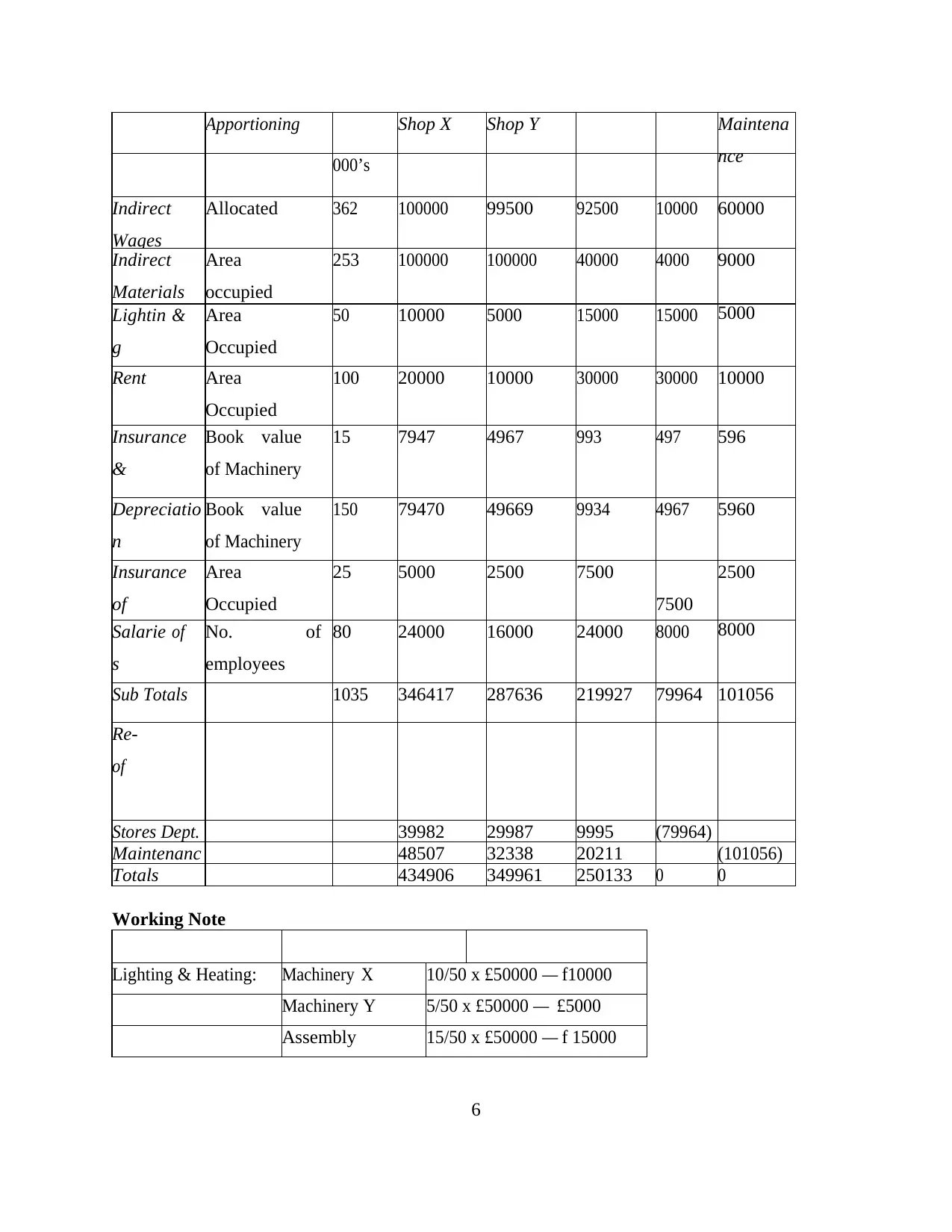

1.3 Calculating the cost of Exquisite using absorption costing technique

Production

Departments

Service Department

Basis of Total Machine Machine Assembly Stores

5

Apportioning Shop X Shop Y Maintena

nce000’s

Indirect

Wages

Allocated 362 100000 99500 92500 10000 60000

Indirect

Materials

Area

occupied

253 100000 100000 40000 4000 9000

Lightin

g

& Area

Occupied

50 10000 5000 15000 15000 5000

Rent Area

Occupied

100 20000 10000 30000 30000 10000

Insurance

&

Book value

of Machinery

15 7947 4967 993 497 596

Depreciatio

n

Book value

of Machinery

150 79470 49669 9934 4967 5960

Insurance

of

Area

Occupied

25 5000 2500 7500

7500

2500

Salarie

s

of No.

employees

of 80 24000 16000 24000 8000 8000

Sub Totals 1035 346417 287636 219927 79964 101056

Re-

of

service dept.Stores Dept. 39982 29987 9995 (79964)

Maintenanc 48507 32338 20211 (101056)

Totals 434906 349961 250133 0 0

Working Note

Lighting & Heating: Machinery X 10/50 x £50000 — f10000

Machinery Y 5/50 x £50000 — £5000

Assembly 15/50 x £50000 — f 15000

6

nce000’s

Indirect

Wages

Allocated 362 100000 99500 92500 10000 60000

Indirect

Materials

Area

occupied

253 100000 100000 40000 4000 9000

Lightin

g

& Area

Occupied

50 10000 5000 15000 15000 5000

Rent Area

Occupied

100 20000 10000 30000 30000 10000

Insurance

&

Book value

of Machinery

15 7947 4967 993 497 596

Depreciatio

n

Book value

of Machinery

150 79470 49669 9934 4967 5960

Insurance

of

Area

Occupied

25 5000 2500 7500

7500

2500

Salarie

s

of No.

employees

of 80 24000 16000 24000 8000 8000

Sub Totals 1035 346417 287636 219927 79964 101056

Re-

of

service dept.Stores Dept. 39982 29987 9995 (79964)

Maintenanc 48507 32338 20211 (101056)

Totals 434906 349961 250133 0 0

Working Note

Lighting & Heating: Machinery X 10/50 x £50000 — f10000

Machinery Y 5/50 x £50000 — £5000

Assembly 15/50 x £50000 — f 15000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

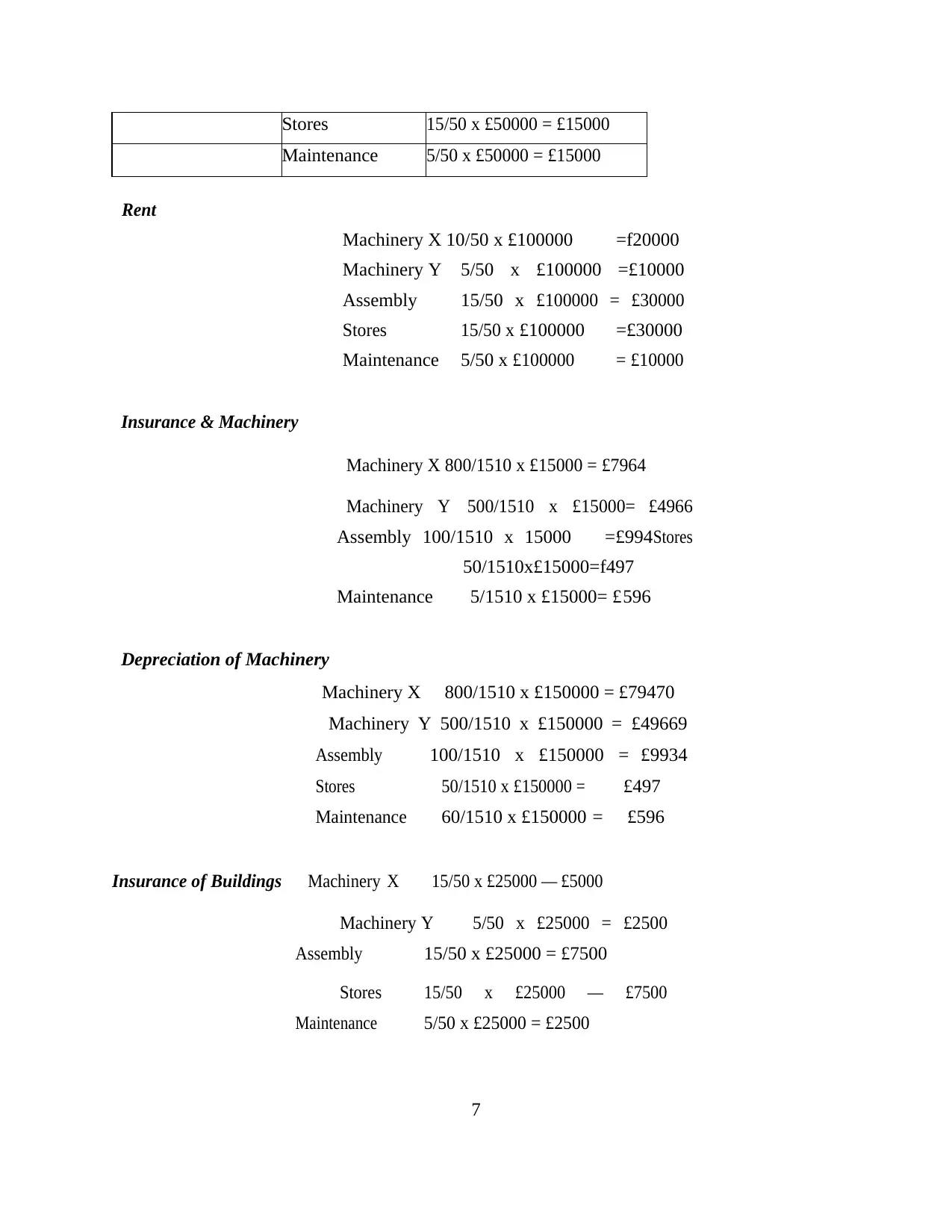

Stores 15/50 x £50000 = £15000

Maintenance 5/50 x £50000 = £15000

Rent

Machinery X 10/50 x £100000 =f20000

Machinery Y 5/50 x £100000 =£10000

Assembly 15/50 x £100000 = £30000

Stores 15/50 x £100000 =£30000

Maintenance 5/50 x £100000 = £10000

Insurance & Machinery

Machinery X 800/1510 x £15000 = £7964

Machinery Y 500/1510 x £15000= £4966

Assembly 100/1510 x 15000 =£994 Stores

50/1510x£15000=f497

Maintenance 5/1510 x £15000= £596

Depreciation of Machinery

Machinery X 800/1510 x £150000 = £79470

Machinery Y 500/1510 x £150000 = £49669

Assembly 100/1510 x £150000 = £9934

Stores 50/1510 x £150000 = £497

Maintenance 60/1510 x £150000 = £596

Insurance of Buildings Machinery X 15/50 x £25000 — £5000

Machinery Y 5/50 x £25000 = £2500

Assembly 15/50 x £25000 = £7500

Stores 15/50 x £25000 — £7500

Maintenance 5/50 x £25000 = £2500

7

Maintenance 5/50 x £50000 = £15000

Rent

Machinery X 10/50 x £100000 =f20000

Machinery Y 5/50 x £100000 =£10000

Assembly 15/50 x £100000 = £30000

Stores 15/50 x £100000 =£30000

Maintenance 5/50 x £100000 = £10000

Insurance & Machinery

Machinery X 800/1510 x £15000 = £7964

Machinery Y 500/1510 x £15000= £4966

Assembly 100/1510 x 15000 =£994 Stores

50/1510x£15000=f497

Maintenance 5/1510 x £15000= £596

Depreciation of Machinery

Machinery X 800/1510 x £150000 = £79470

Machinery Y 500/1510 x £150000 = £49669

Assembly 100/1510 x £150000 = £9934

Stores 50/1510 x £150000 = £497

Maintenance 60/1510 x £150000 = £596

Insurance of Buildings Machinery X 15/50 x £25000 — £5000

Machinery Y 5/50 x £25000 = £2500

Assembly 15/50 x £25000 = £7500

Stores 15/50 x £25000 — £7500

Maintenance 5/50 x £25000 = £2500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

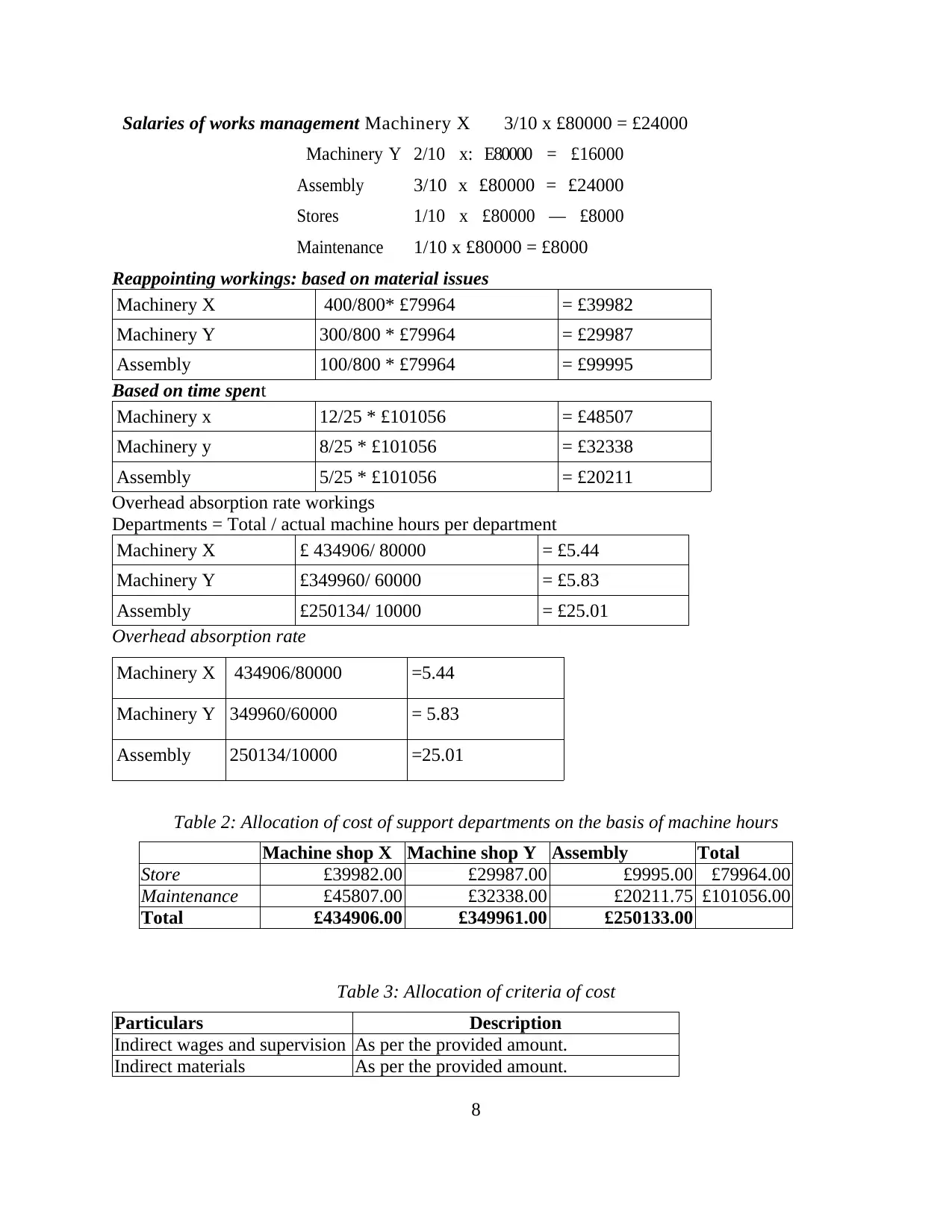

Salaries of works management Machinery X 3/10 x £80000 = £24000

Machinery Y 2/10 x: E80000 = £16000

Assembly 3/10 x £80000 = £24000

Stores 1/10 x £80000 — £8000

Maintenance 1/10 x £80000 = £8000

Reappointing workings: based on material issues

Machinery X 400/800* £79964 = £39982

Machinery Y 300/800 * £79964 = £29987

Assembly 100/800 * £79964 = £99995

Based on time spent

Machinery x 12/25 * £101056 = £48507

Machinery y 8/25 * £101056 = £32338

Assembly 5/25 * £101056 = £20211

Overhead absorption rate workings

Departments = Total / actual machine hours per department

Machinery X £ 434906/ 80000 = £5.44

Machinery Y £349960/ 60000 = £5.83

Assembly £250134/ 10000 = £25.01

Overhead absorption rate

Machinery X 434906/80000 =5.44

Machinery Y 349960/60000 = 5.83

Assembly 250134/10000 =25.01

Table 2: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39982.00 £29987.00 £9995.00 £79964.00

Maintenance £45807.00 £32338.00 £20211.75 £101056.00

Total £434906.00 £349961.00 £250133.00

Table 3: Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

8

Machinery Y 2/10 x: E80000 = £16000

Assembly 3/10 x £80000 = £24000

Stores 1/10 x £80000 — £8000

Maintenance 1/10 x £80000 = £8000

Reappointing workings: based on material issues

Machinery X 400/800* £79964 = £39982

Machinery Y 300/800 * £79964 = £29987

Assembly 100/800 * £79964 = £99995

Based on time spent

Machinery x 12/25 * £101056 = £48507

Machinery y 8/25 * £101056 = £32338

Assembly 5/25 * £101056 = £20211

Overhead absorption rate workings

Departments = Total / actual machine hours per department

Machinery X £ 434906/ 80000 = £5.44

Machinery Y £349960/ 60000 = £5.83

Assembly £250134/ 10000 = £25.01

Overhead absorption rate

Machinery X 434906/80000 =5.44

Machinery Y 349960/60000 = 5.83

Assembly 250134/10000 =25.01

Table 2: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39982.00 £29987.00 £9995.00 £79964.00

Maintenance £45807.00 £32338.00 £20211.75 £101056.00

Total £434906.00 £349961.00 £250133.00

Table 3: Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

8

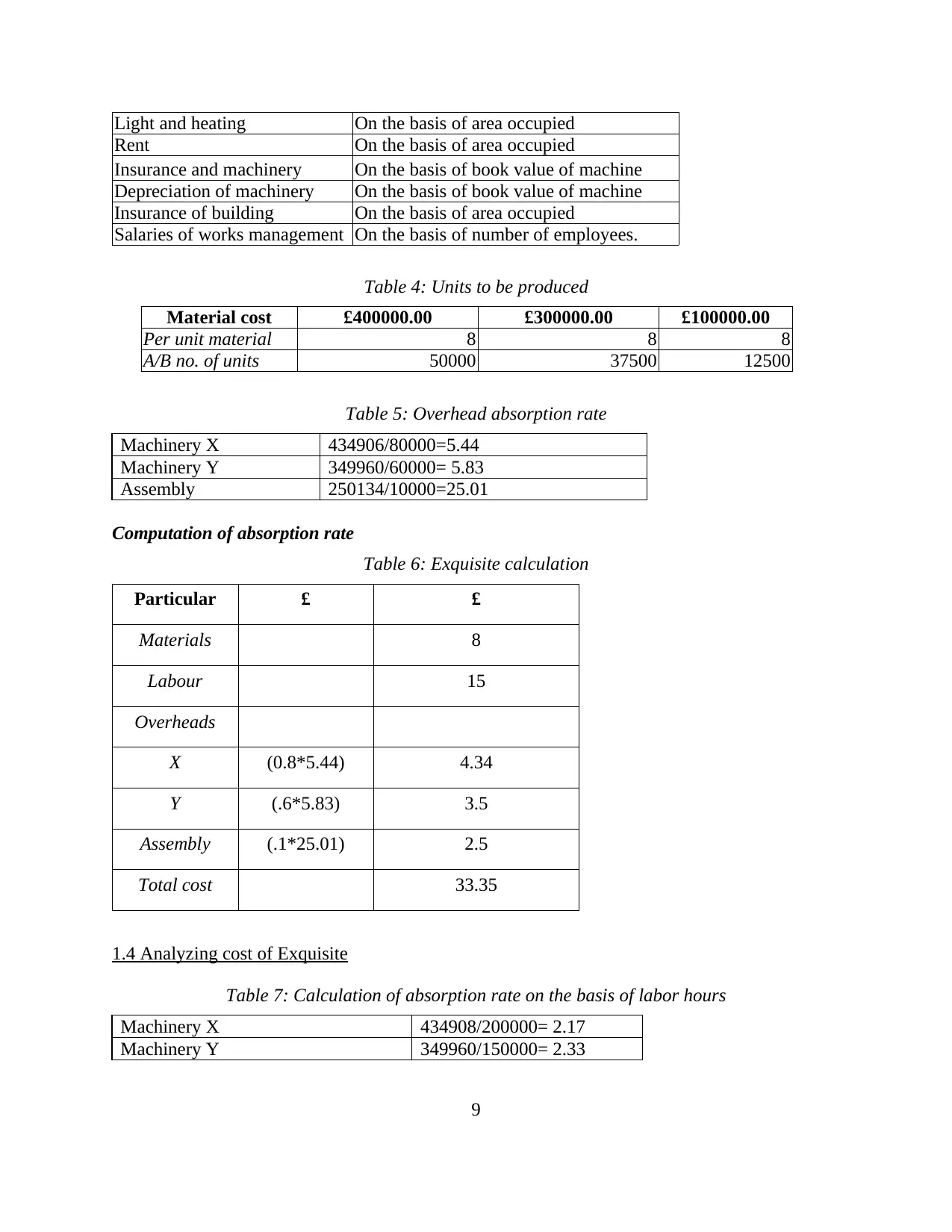

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 4: Units to be produced

Material cost £400000.00 £300000.00 £100000.00

Per unit material 8 8 8

A/B no. of units 50000 37500 12500

Table 5: Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Table 6: Exquisite calculation

Particular £ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing cost of Exquisite

Table 7: Calculation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

9

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 4: Units to be produced

Material cost £400000.00 £300000.00 £100000.00

Per unit material 8 8 8

A/B no. of units 50000 37500 12500

Table 5: Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Table 6: Exquisite calculation

Particular £ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing cost of Exquisite

Table 7: Calculation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assembly 250134/20000= 2.15

Table 8: Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

The above mentioned tables depict that for finding total cost of product of Jeffery and

Son's, labor hour absorption is effective means. It aids to bring changes in per unit absorption

cost rate.

TASK 2

2.1 Preparing and analyzing cost report for month of September

The cost reports for the month of September have been prepared as follows. It is helpful

for management of Jeffrey & Sons Ltd to analyse the performance and issues faced by

corporation so-as-to take appropriate action on right time.

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

10

Table 8: Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

The above mentioned tables depict that for finding total cost of product of Jeffery and

Son's, labor hour absorption is effective means. It aids to bring changes in per unit absorption

cost rate.

TASK 2

2.1 Preparing and analyzing cost report for month of September

The cost reports for the month of September have been prepared as follows. It is helpful

for management of Jeffrey & Sons Ltd to analyse the performance and issues faced by

corporation so-as-to take appropriate action on right time.

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

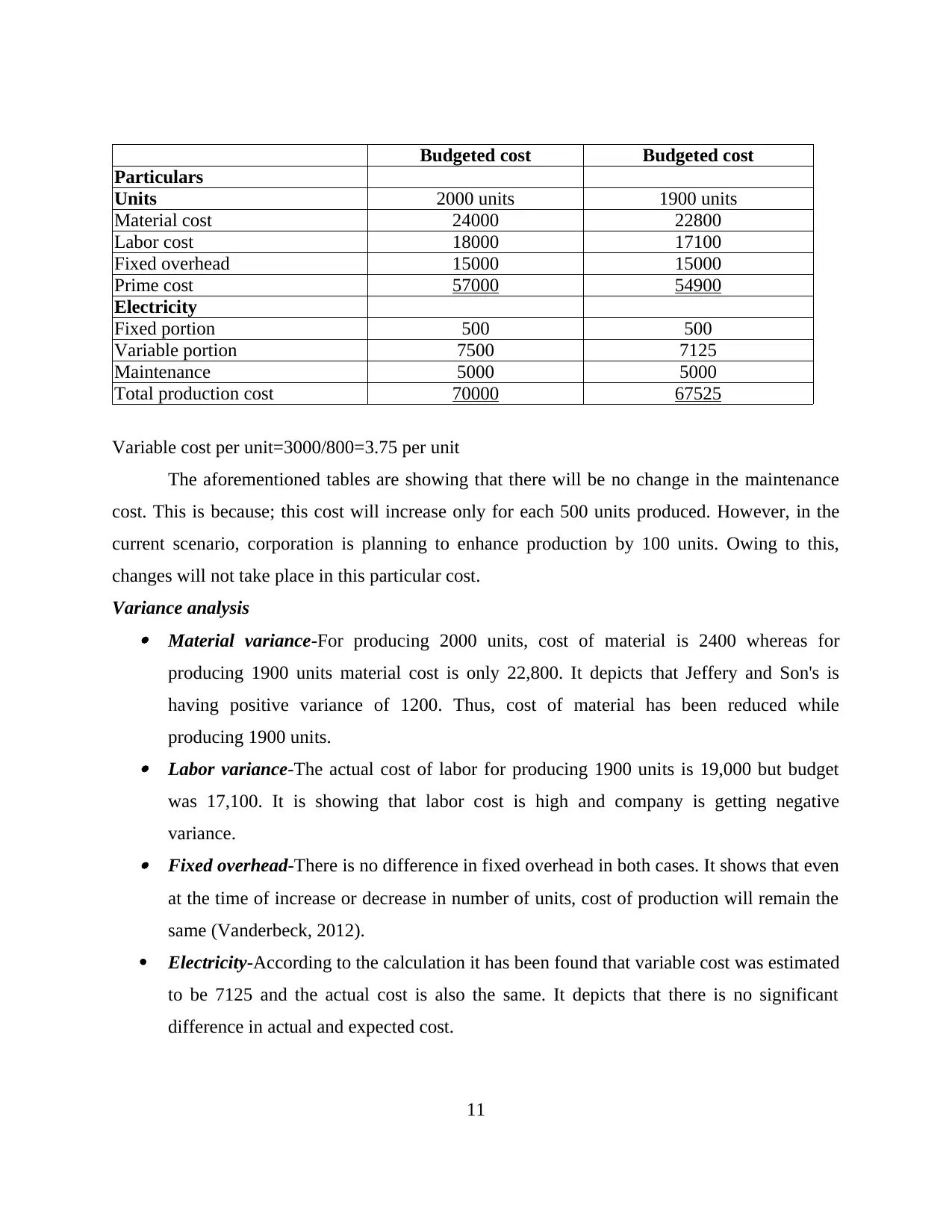

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Variable cost per unit=3000/800=3.75 per unit

The aforementioned tables are showing that there will be no change in the maintenance

cost. This is because; this cost will increase only for each 500 units produced. However, in the

current scenario, corporation is planning to enhance production by 100 units. Owing to this,

changes will not take place in this particular cost.

Variance analysis Material variance-For producing 2000 units, cost of material is 2400 whereas for

producing 1900 units material cost is only 22,800. It depicts that Jeffery and Son's is

having positive variance of 1200. Thus, cost of material has been reduced while

producing 1900 units. Labor variance-The actual cost of labor for producing 1900 units is 19,000 but budget

was 17,100. It is showing that labor cost is high and company is getting negative

variance. Fixed overhead-There is no difference in fixed overhead in both cases. It shows that even

at the time of increase or decrease in number of units, cost of production will remain the

same (Vanderbeck, 2012).

Electricity-According to the calculation it has been found that variable cost was estimated

to be 7125 and the actual cost is also the same. It depicts that there is no significant

difference in actual and expected cost.

11

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

Total production cost 70000 67525

Variable cost per unit=3000/800=3.75 per unit

The aforementioned tables are showing that there will be no change in the maintenance

cost. This is because; this cost will increase only for each 500 units produced. However, in the

current scenario, corporation is planning to enhance production by 100 units. Owing to this,

changes will not take place in this particular cost.

Variance analysis Material variance-For producing 2000 units, cost of material is 2400 whereas for

producing 1900 units material cost is only 22,800. It depicts that Jeffery and Son's is

having positive variance of 1200. Thus, cost of material has been reduced while

producing 1900 units. Labor variance-The actual cost of labor for producing 1900 units is 19,000 but budget

was 17,100. It is showing that labor cost is high and company is getting negative

variance. Fixed overhead-There is no difference in fixed overhead in both cases. It shows that even

at the time of increase or decrease in number of units, cost of production will remain the

same (Vanderbeck, 2012).

Electricity-According to the calculation it has been found that variable cost was estimated

to be 7125 and the actual cost is also the same. It depicts that there is no significant

difference in actual and expected cost.

11

2.2 Using various performance indicator to identify areas of improvement

The performance appraisal of organization is crucial task which assists management to

concentrate on key performance indicator (Key Performance Indicators, 2014). These key

performance indicators are the effective means through which improvement can take place in

internal or external environment of Jeffrey & Sons Ltd. Key performance indicators are

explained as follows- Qualitative indicators-Performance of corporation can be assessed with the help of

qualitative indicators like increased customer base, high sales turnover and retention of

buyers. In case the indicators are not shown, then company might take decision to bring

improvement in its internal business environment (Weygandt and et.al., 2009). It shows

that management needs to focus on potential areas like marketing strategies, retention etc.

Thus, qualitative performance indicators help to ensure continuous improvement at

workplace so-as-to deliver higher level of satisfaction among buyers.

Quantitative indicators-The qualitative performance indicators include factors like high

rate of return, sales turnover and cost of production. According to findings, management

assess what kind of strategies could be adopted to ensure good performance (Elmassri

and Harris, 2011). Thus, all of these indicators depict that who should be improved and

how. Furthermore, high cost of production shows that company is not focusing on its

production activities. Therefore, changes can be done in an effectual manner.

2.3 Suggesting ways to reduce cost, enhance value and quality

There are different ways to reduce cost and enhance value as well quality of Jeffrey &

Sons Ltd. These are explained as follows- Total quality management- Under this, company can assess issues that are taking place

in production process. It assists management to ensure that good quality of products and

services are delivered to end users. On the other hand, as per the total quality

management, aspect management of Jeffrey & Sons Ltd can meet the expectations of

buyers in the most effective manner (Kate-Riin Kont, 2012). This in turn leads to increase

in rate of return and decrease in cost of production to a great extent. However, at the

initial stage, non-monetary cost can be incurred but it will enhance quality.

12

The performance appraisal of organization is crucial task which assists management to

concentrate on key performance indicator (Key Performance Indicators, 2014). These key

performance indicators are the effective means through which improvement can take place in

internal or external environment of Jeffrey & Sons Ltd. Key performance indicators are

explained as follows- Qualitative indicators-Performance of corporation can be assessed with the help of

qualitative indicators like increased customer base, high sales turnover and retention of

buyers. In case the indicators are not shown, then company might take decision to bring

improvement in its internal business environment (Weygandt and et.al., 2009). It shows

that management needs to focus on potential areas like marketing strategies, retention etc.

Thus, qualitative performance indicators help to ensure continuous improvement at

workplace so-as-to deliver higher level of satisfaction among buyers.

Quantitative indicators-The qualitative performance indicators include factors like high

rate of return, sales turnover and cost of production. According to findings, management

assess what kind of strategies could be adopted to ensure good performance (Elmassri

and Harris, 2011). Thus, all of these indicators depict that who should be improved and

how. Furthermore, high cost of production shows that company is not focusing on its

production activities. Therefore, changes can be done in an effectual manner.

2.3 Suggesting ways to reduce cost, enhance value and quality

There are different ways to reduce cost and enhance value as well quality of Jeffrey &

Sons Ltd. These are explained as follows- Total quality management- Under this, company can assess issues that are taking place

in production process. It assists management to ensure that good quality of products and

services are delivered to end users. On the other hand, as per the total quality

management, aspect management of Jeffrey & Sons Ltd can meet the expectations of

buyers in the most effective manner (Kate-Riin Kont, 2012). This in turn leads to increase

in rate of return and decrease in cost of production to a great extent. However, at the

initial stage, non-monetary cost can be incurred but it will enhance quality.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.