Management Accounting Analysis: Advance Construction Group Ltd Report

VerifiedAdded on 2020/01/28

|18

|5947

|216

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Advance Construction Group Ltd. It begins by defining management accounting and outlining the essential requirements of different systems, including traditional and lean accounting approaches. The report then delves into various management accounting reporting methods, such as job cost reports, sales reports, inventory reports, and performance reports. A key section of the report focuses on cost calculation using absorption and marginal costing techniques, providing a statement of income analysis. Furthermore, the report evaluates the advantages and disadvantages of planning tools used in budgetary control within the context of the construction company. Finally, it compares organizational strategies for adapting management accounting systems to address financial problems, concluding with a summary of the key findings and references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1 ..........................................................................................................................................4

P1 Management accounting and essential requirements of different types of systems of

management accounting..............................................................................................................4

P2 Different methods for management accounting reporting.....................................................6

TASK 2............................................................................................................................................8

P3 Calculation of cost using absorption and marginal cost techniques......................................8

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of planning tools used in budgetary control in case of

Advance Construction Group Ltd.............................................................................................12

TASK 4..........................................................................................................................................14

P5 Comparison between organisation for adapting management accounting system to respond

financial problems.....................................................................................................................14

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................4

TASK 1 ..........................................................................................................................................4

P1 Management accounting and essential requirements of different types of systems of

management accounting..............................................................................................................4

P2 Different methods for management accounting reporting.....................................................6

TASK 2............................................................................................................................................8

P3 Calculation of cost using absorption and marginal cost techniques......................................8

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of planning tools used in budgetary control in case of

Advance Construction Group Ltd.............................................................................................12

TASK 4..........................................................................................................................................14

P5 Comparison between organisation for adapting management accounting system to respond

financial problems.....................................................................................................................14

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting can be defined as the process by which mentioned entities can

analyse statements of finance and management which helps in giving detailed description of the

financial position of the entity, which may be required by various stakeholders of the entity. It is

basically a profession which involves assisting in administration decision making, planning and

systems for management of performance, and giving support in financial report and control so as

to assist administration in strategy implementation and formulation (Fullerton, Kennedy and

Widener, 2014). Managers use this accounting provisions for getting information before taking

decisions in the organisation, which helps in the performance and management of functions. This

report is based on the case study of Advance Construction Group Ltd is a construction company

in Scotland, it carries out business of civil engineering and dynamic groundwork. It has a good

reputation in industry which provides excellent workforce. In this report a detailed description is

given on management accounting and necessary requirement of different systems of

management accounting is given. This study will help in providing various methods of

management accounting, advantages and disadvantages of budgetary control planning tools.

Reports which are prepared on the basis of management accounting helps in showing what

amount is available with entity and also the profit which is generated from sales.

TASK 1

P1 Management accounting and essential requirements of different types of systems of

management accounting

Management accounting can be defined as the analysis, sourcing, use and communication

of various decisions which are related with the financial as well as non financial information so

as to preserve and generate value value for entity. It combines finance, accounting, and

administration with the skills and techniques of business which will be needed to add value in

any entity (Talha, Raja and Seetharaman, 2010). Management accounting work in the entire

business and not just in giving advise to managers, finance and implications of important

decisions, formulation of strategy of business and in risk monitoring. It uses all kinds of

information and not just related to finance so as to lead mentioned entity towards success.

Marginal costing and absorption are some of the tools and techniques of cost accounting by

Management accounting can be defined as the process by which mentioned entities can

analyse statements of finance and management which helps in giving detailed description of the

financial position of the entity, which may be required by various stakeholders of the entity. It is

basically a profession which involves assisting in administration decision making, planning and

systems for management of performance, and giving support in financial report and control so as

to assist administration in strategy implementation and formulation (Fullerton, Kennedy and

Widener, 2014). Managers use this accounting provisions for getting information before taking

decisions in the organisation, which helps in the performance and management of functions. This

report is based on the case study of Advance Construction Group Ltd is a construction company

in Scotland, it carries out business of civil engineering and dynamic groundwork. It has a good

reputation in industry which provides excellent workforce. In this report a detailed description is

given on management accounting and necessary requirement of different systems of

management accounting is given. This study will help in providing various methods of

management accounting, advantages and disadvantages of budgetary control planning tools.

Reports which are prepared on the basis of management accounting helps in showing what

amount is available with entity and also the profit which is generated from sales.

TASK 1

P1 Management accounting and essential requirements of different types of systems of

management accounting

Management accounting can be defined as the analysis, sourcing, use and communication

of various decisions which are related with the financial as well as non financial information so

as to preserve and generate value value for entity. It combines finance, accounting, and

administration with the skills and techniques of business which will be needed to add value in

any entity (Talha, Raja and Seetharaman, 2010). Management accounting work in the entire

business and not just in giving advise to managers, finance and implications of important

decisions, formulation of strategy of business and in risk monitoring. It uses all kinds of

information and not just related to finance so as to lead mentioned entity towards success.

Marginal costing and absorption are some of the tools and techniques of cost accounting by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which mentioned entity prepare efficient and effective strategies for the maintenance of

productivity.

There are various systems of management accounting which are very helpful in

development of Advance Construction Group Ltd. Management accounting helps in reducing

expenses of various operations . It is used by owners of business for reviewing cost of operations

of business and economic resources which are used by the entity. It helps in better understanding

of how much money will be required to run business (Hiebl, 2014). It can also be used to

conduct several analyses on resource quality which are used for the production. Management

accounting system helps in improving cash flow, as budget is the important part of it. Business

owners generally use budget so that the full analysis of financial map will be there for the

expenses of business in future. It helps in creating master budget for the company and will help

in careful analysis of useful and not so useful expenses. It helps in taking several business

decision based on analysis of quality and quantity and many more. It will also help in increasing

financial returns. Management accounting can prepare forecast report related to finance for

customer demands, sales. It can be used by the business owners so as to make sure how much

amount of goods and services should be produced to satisfy customer (Dillard and Roslender,

2011).

There is an essential requirements of management accounting system for various purpose.

These essential requirements can be like : Traditional Management Accounting: This type of management accounting system is

necessary as it focuses on cost as a means of job order and ways of process costing. With

the help of this method, Advance Construction Group Ltd will be able to allocate several

types of cost which is related to labour, material and manufacturing. Traditional

management accounting system is very helpful and necessary for entity. Technique of job

order costing is used in construction industry that has large projects. So in such cases

several types of cost are easy to trace and mentioned entity can allocate them easily in the

respective project. Techniques of process costing helps in allocating cost to several

processes (Contrafatto and Burns, 2013).

Lean Accounting: Lean accounting is the term used in the cited entity for the

requirement of changes related to control, accounting, management and measurement to

support lean thinking and manufacturing. It is revolutionary because it not only

productivity.

There are various systems of management accounting which are very helpful in

development of Advance Construction Group Ltd. Management accounting helps in reducing

expenses of various operations . It is used by owners of business for reviewing cost of operations

of business and economic resources which are used by the entity. It helps in better understanding

of how much money will be required to run business (Hiebl, 2014). It can also be used to

conduct several analyses on resource quality which are used for the production. Management

accounting system helps in improving cash flow, as budget is the important part of it. Business

owners generally use budget so that the full analysis of financial map will be there for the

expenses of business in future. It helps in creating master budget for the company and will help

in careful analysis of useful and not so useful expenses. It helps in taking several business

decision based on analysis of quality and quantity and many more. It will also help in increasing

financial returns. Management accounting can prepare forecast report related to finance for

customer demands, sales. It can be used by the business owners so as to make sure how much

amount of goods and services should be produced to satisfy customer (Dillard and Roslender,

2011).

There is an essential requirements of management accounting system for various purpose.

These essential requirements can be like : Traditional Management Accounting: This type of management accounting system is

necessary as it focuses on cost as a means of job order and ways of process costing. With

the help of this method, Advance Construction Group Ltd will be able to allocate several

types of cost which is related to labour, material and manufacturing. Traditional

management accounting system is very helpful and necessary for entity. Technique of job

order costing is used in construction industry that has large projects. So in such cases

several types of cost are easy to trace and mentioned entity can allocate them easily in the

respective project. Techniques of process costing helps in allocating cost to several

processes (Contrafatto and Burns, 2013).

Lean Accounting: Lean accounting is the term used in the cited entity for the

requirement of changes related to control, accounting, management and measurement to

support lean thinking and manufacturing. It is revolutionary because it not only

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concentrate on cost , but also gives support in making strategy to control or reduce the

management cost. With the help of lean accounting, accountant of management can make

several strategies in regards with reduction of cost and such strategies can be

implemented for Advance Construction Group Ltd benefit. By this manager of personnel

management can take necessary decisions.

There are various examples of management accounting system which can be explained as

follows: Cost accounting system: It is the type of structure which is used in Advance construction

group, so that cost estimation of the product can be made which will help in determining

control cost, profit and inventory. Entity should be aware of the various products that are

non-profitable or profitable, and it can only be possible if there will correct estimation of

product cost which is offered by firm. Job costing system: This type of system is helpful when there are different types of job.

In job costing there is the involvement of direct as well as indirect costs. It is helpful in

finding out the information which is in relation with the production and job cost. Batch costing system: It is a kind of particular order costing system, and have similarity

with the job costing. In every batch there are different identical units but each is different

from each other. Inventory management system: It is the kind of ongoing process which is involved with

moving parts and product in and outside of the company's current location. Whenever

there is a completion of new order regarding any product, firm manages its inventory

with the help of inventory management system. It can also be defined as the type of

software which helps in the proper administration of the stock or inventory.

Price optimisation system: This system is helpful in demand variations at different level

and then makes combination of data with the cost and inventory level in order to suggest

price which helps to improve profits.

P2 Different methods for management accounting reporting

Management accounting reporting is very necessary for the development of Advance

Construction Group Ltd. There are number of methods which are used for the management

accounting reporting which will help in the development an growth of the entity. It helps in

making several reports , strategies, plans which are necessary for the business to carry out its

management cost. With the help of lean accounting, accountant of management can make

several strategies in regards with reduction of cost and such strategies can be

implemented for Advance Construction Group Ltd benefit. By this manager of personnel

management can take necessary decisions.

There are various examples of management accounting system which can be explained as

follows: Cost accounting system: It is the type of structure which is used in Advance construction

group, so that cost estimation of the product can be made which will help in determining

control cost, profit and inventory. Entity should be aware of the various products that are

non-profitable or profitable, and it can only be possible if there will correct estimation of

product cost which is offered by firm. Job costing system: This type of system is helpful when there are different types of job.

In job costing there is the involvement of direct as well as indirect costs. It is helpful in

finding out the information which is in relation with the production and job cost. Batch costing system: It is a kind of particular order costing system, and have similarity

with the job costing. In every batch there are different identical units but each is different

from each other. Inventory management system: It is the kind of ongoing process which is involved with

moving parts and product in and outside of the company's current location. Whenever

there is a completion of new order regarding any product, firm manages its inventory

with the help of inventory management system. It can also be defined as the type of

software which helps in the proper administration of the stock or inventory.

Price optimisation system: This system is helpful in demand variations at different level

and then makes combination of data with the cost and inventory level in order to suggest

price which helps to improve profits.

P2 Different methods for management accounting reporting

Management accounting reporting is very necessary for the development of Advance

Construction Group Ltd. There are number of methods which are used for the management

accounting reporting which will help in the development an growth of the entity. It helps in

making several reports , strategies, plans which are necessary for the business to carry out its

activities in a proper and organised way. Several methods and techniques which are used for

management accounting reporting in Advance Construction Group Ltd are mentioned below : Job cost report: Job costing report can be defined as the process of allocating and coding

expenses of the project which are needed to track profitability and financial efficiency. It

is basically a mission critical activity. There are various kinds of expenses which are

included in a particular project at different stages. Therefore, it is very necessary to make

proper allocation of the expenses related to the project. Sales report: The proper record of the calls which are made and the products which are

sold by the company in a particular time is defined in the sales report. This kind of report

gives the overall view of the company sales. A typical sales report may include data

based on sales volume, current and new accounts which are contacted and their time and

cost which are involved in selling and promoting products. Inventory report: An inventory report can be defined as the summary of the items which

belongs to a business, organisation or industry. It supports in providing comprehensive

account of stock or supply of different items. This report can be presented in different

lengths and forms. A good inventory report should be simple, exhaustive and clear. Account receivable report: This report give detailed list of the balance due from the

subscription of the individuals. It includes all the debtors whose amounts are due on an

organisation. This report is helpful in analysing customer credit worthiness and

receivables, and also supports in forecasting collection of the customer's payments.

Performance report: It is an important activity helpful in project communication

management. It includes disseminating and collecting information of the project, resource

utilization, forecasting of future progress, communicating progress of project and

different stakeholders' status as per the plan of communication management.

M1

System and application of management accounting is very helpful in Advance

Construction Group Ltd for its development and proper management of accounting reports.

Management accounting is the process of making reports and accounts of management which

helps in providing timely and accurate information regarding finance and statistics. Systems of

management accounting helps in making long term and short term decisions. Systems of

management accounting has become an integral part of entity. It helps in determining aim and

management accounting reporting in Advance Construction Group Ltd are mentioned below : Job cost report: Job costing report can be defined as the process of allocating and coding

expenses of the project which are needed to track profitability and financial efficiency. It

is basically a mission critical activity. There are various kinds of expenses which are

included in a particular project at different stages. Therefore, it is very necessary to make

proper allocation of the expenses related to the project. Sales report: The proper record of the calls which are made and the products which are

sold by the company in a particular time is defined in the sales report. This kind of report

gives the overall view of the company sales. A typical sales report may include data

based on sales volume, current and new accounts which are contacted and their time and

cost which are involved in selling and promoting products. Inventory report: An inventory report can be defined as the summary of the items which

belongs to a business, organisation or industry. It supports in providing comprehensive

account of stock or supply of different items. This report can be presented in different

lengths and forms. A good inventory report should be simple, exhaustive and clear. Account receivable report: This report give detailed list of the balance due from the

subscription of the individuals. It includes all the debtors whose amounts are due on an

organisation. This report is helpful in analysing customer credit worthiness and

receivables, and also supports in forecasting collection of the customer's payments.

Performance report: It is an important activity helpful in project communication

management. It includes disseminating and collecting information of the project, resource

utilization, forecasting of future progress, communicating progress of project and

different stakeholders' status as per the plan of communication management.

M1

System and application of management accounting is very helpful in Advance

Construction Group Ltd for its development and proper management of accounting reports.

Management accounting is the process of making reports and accounts of management which

helps in providing timely and accurate information regarding finance and statistics. Systems of

management accounting helps in making long term and short term decisions. Systems of

management accounting has become an integral part of entity. It helps in determining aim and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

giving better services to customers. It increase efficiency of business, taking judgement will also

be easy, provides effective management control and maximize profits (Ward, 2012).

D1

According to Van Helden and et. al., (2010) , system of management accounting is vital

and provides effective management control. It increases the business efficiency and helps in the

measurement of performance. On the other hand Vaivioand Sirén, (2010), says that management

accounting reporting is another important factor which helps in significant planning related to

finance and other major resources used in various activities. Management accounting reporting

and systems both play important part in development of Advance Construction Group Ltd. As

per the view of Jansen, (2011) management accounting system and reporting helps in making

statements of fund flow and cash flow. This is very helpful for the entity in successful growth.

TASK 2

P3 Calculation of cost using absorption and marginal cost techniques

Calculation of net profit can be done with the help of several techniques in management

accounting. Net profit of Advance Construction Group Ltd as per the marginal costing and

absorption costing is given below:

Absorption Costing : Absorption costing can be defined as the management accounting

technique by which several cost which are in relation with various type of production

process that are implemented on a product. This method is also required for the

evaluation of inventory of mentioned entity. Forecasting is the important element used in

management accounting (Shah, Malik and Malik, 2011). All expenses are carried on a

specific basis therefore when there is actual occurrence of expenses, on that time it is

possible that the expense of the budget may get different from actual budget. With the

help of absorption costing, under and over absorption can be managed.

Statement of income according to absorption cost :

£ £

Sales 700 x 35 21,000

Less: Cost of Production 16 x 700 11,200

Less: Closing stock 16 x 100 (1,600)

be easy, provides effective management control and maximize profits (Ward, 2012).

D1

According to Van Helden and et. al., (2010) , system of management accounting is vital

and provides effective management control. It increases the business efficiency and helps in the

measurement of performance. On the other hand Vaivioand Sirén, (2010), says that management

accounting reporting is another important factor which helps in significant planning related to

finance and other major resources used in various activities. Management accounting reporting

and systems both play important part in development of Advance Construction Group Ltd. As

per the view of Jansen, (2011) management accounting system and reporting helps in making

statements of fund flow and cash flow. This is very helpful for the entity in successful growth.

TASK 2

P3 Calculation of cost using absorption and marginal cost techniques

Calculation of net profit can be done with the help of several techniques in management

accounting. Net profit of Advance Construction Group Ltd as per the marginal costing and

absorption costing is given below:

Absorption Costing : Absorption costing can be defined as the management accounting

technique by which several cost which are in relation with various type of production

process that are implemented on a product. This method is also required for the

evaluation of inventory of mentioned entity. Forecasting is the important element used in

management accounting (Shah, Malik and Malik, 2011). All expenses are carried on a

specific basis therefore when there is actual occurrence of expenses, on that time it is

possible that the expense of the budget may get different from actual budget. With the

help of absorption costing, under and over absorption can be managed.

Statement of income according to absorption cost :

£ £

Sales 700 x 35 21,000

Less: Cost of Production 16 x 700 11,200

Less: Closing stock 16 x 100 (1,600)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

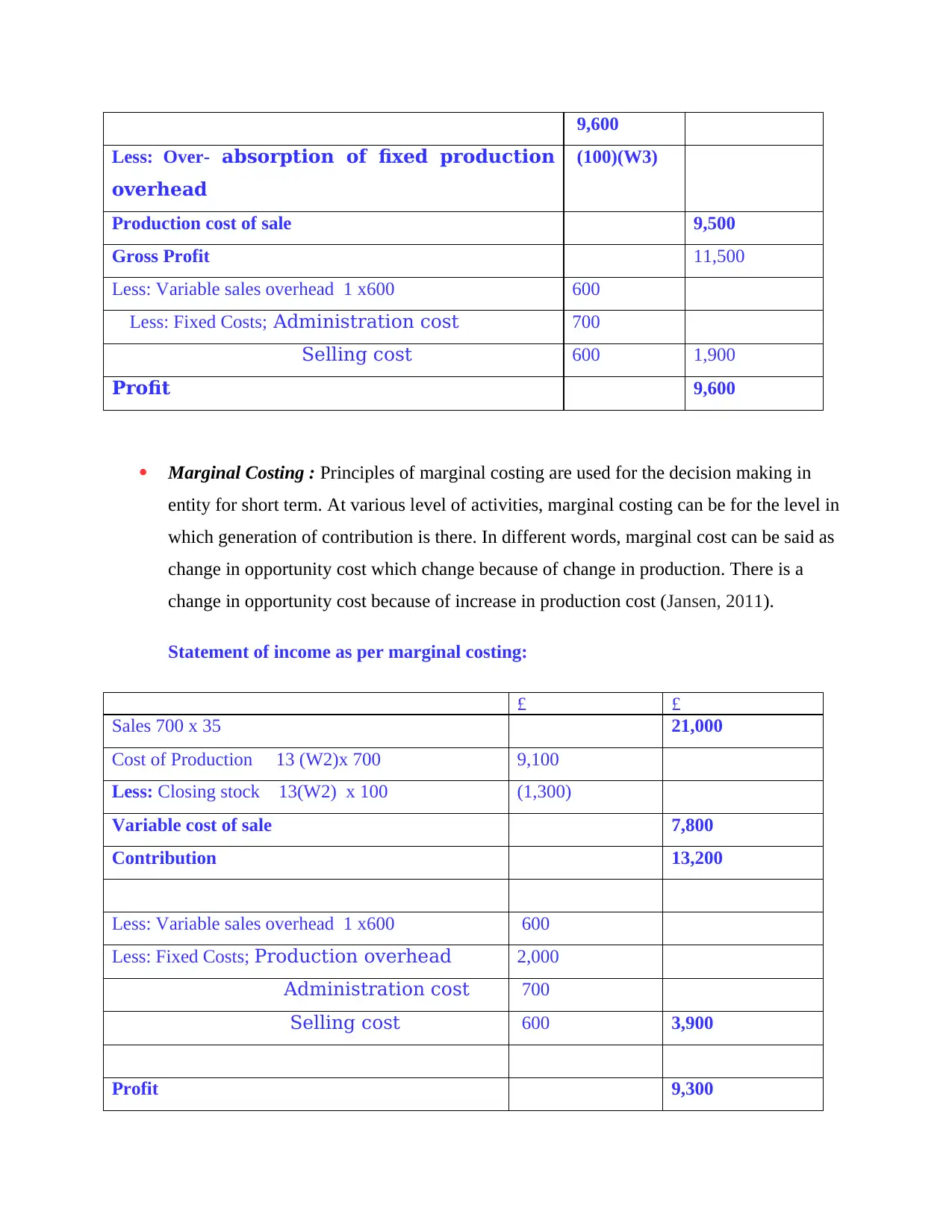

9,600

Less: Over- absorption of fixed production

overhead

(100)(W3)

Production cost of sale 9,500

Gross Profit 11,500

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Profit 9,600

Marginal Costing : Principles of marginal costing are used for the decision making in

entity for short term. At various level of activities, marginal costing can be for the level in

which generation of contribution is there. In different words, marginal cost can be said as

change in opportunity cost which change because of change in production. There is a

change in opportunity cost because of increase in production cost (Jansen, 2011).

Statement of income as per marginal costing:

£ £

Sales 700 x 35 21,000

Cost of Production 13 (W2)x 700 9,100

Less: Closing stock 13(W2) x 100 (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Production overhead 2,000

Administration cost 700

Selling cost 600 3,900

Profit 9,300

Less: Over- absorption of fixed production

overhead

(100)(W3)

Production cost of sale 9,500

Gross Profit 11,500

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Profit 9,600

Marginal Costing : Principles of marginal costing are used for the decision making in

entity for short term. At various level of activities, marginal costing can be for the level in

which generation of contribution is there. In different words, marginal cost can be said as

change in opportunity cost which change because of change in production. There is a

change in opportunity cost because of increase in production cost (Jansen, 2011).

Statement of income as per marginal costing:

£ £

Sales 700 x 35 21,000

Cost of Production 13 (W2)x 700 9,100

Less: Closing stock 13(W2) x 100 (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Production overhead 2,000

Administration cost 700

Selling cost 600 3,900

Profit 9,300

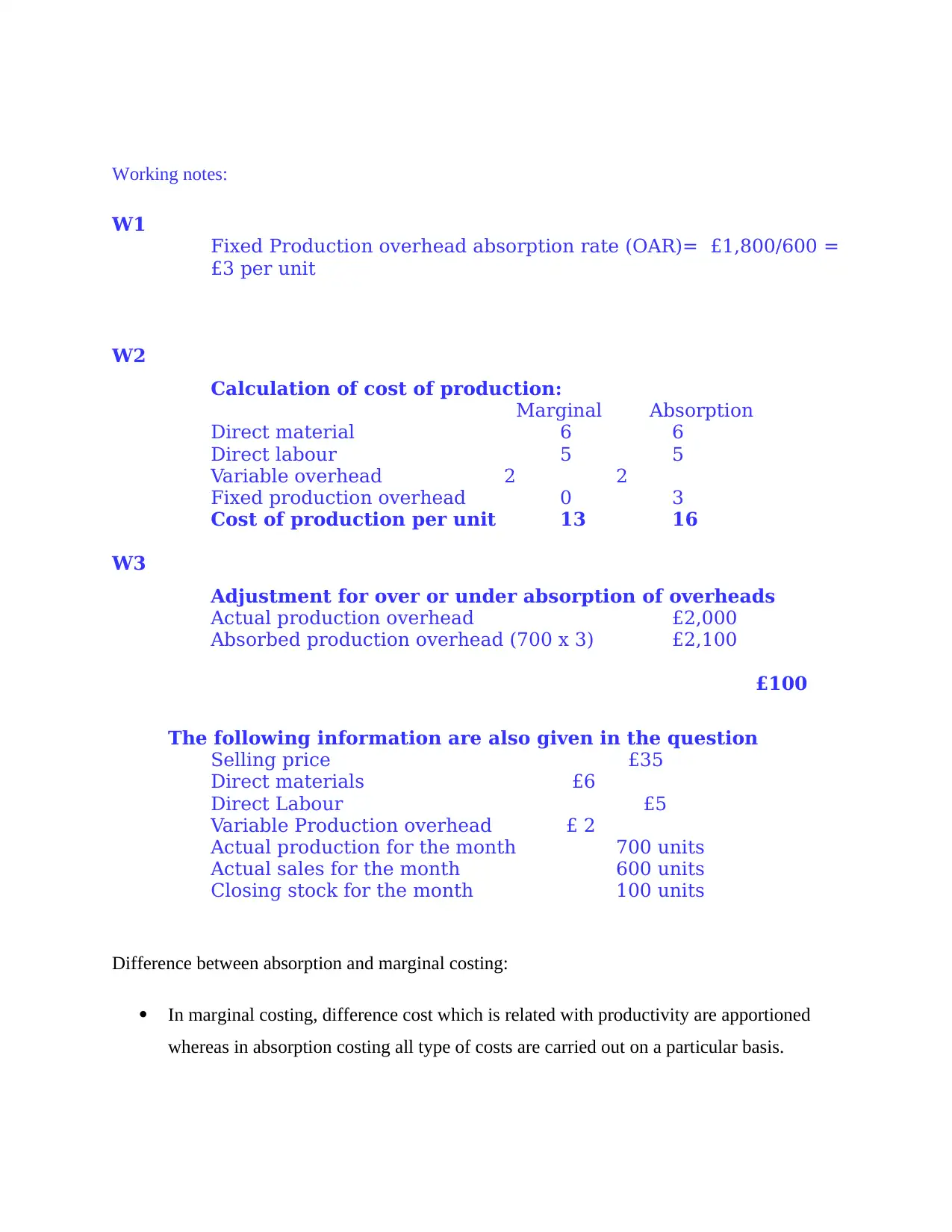

Working notes:

W1

Fixed Production overhead absorption rate (OAR)= £1,800/600 =

£3 per unit

W2

Calculation of cost of production:

Marginal Absorption

Direct material 6 6

Direct labour 5 5

Variable overhead 2 2

Fixed production overhead 0 3

Cost of production per unit 13 16

W3

Adjustment for over or under absorption of overheads

Actual production overhead £2,000

Absorbed production overhead (700 x 3) £2,100

£100

The following information are also given in the question

Selling price £35

Direct materials £6

Direct Labour £5

Variable Production overhead £ 2

Actual production for the month 700 units

Actual sales for the month 600 units

Closing stock for the month 100 units

Difference between absorption and marginal costing:

In marginal costing, difference cost which is related with productivity are apportioned

whereas in absorption costing all type of costs are carried out on a particular basis.

W1

Fixed Production overhead absorption rate (OAR)= £1,800/600 =

£3 per unit

W2

Calculation of cost of production:

Marginal Absorption

Direct material 6 6

Direct labour 5 5

Variable overhead 2 2

Fixed production overhead 0 3

Cost of production per unit 13 16

W3

Adjustment for over or under absorption of overheads

Actual production overhead £2,000

Absorbed production overhead (700 x 3) £2,100

£100

The following information are also given in the question

Selling price £35

Direct materials £6

Direct Labour £5

Variable Production overhead £ 2

Actual production for the month 700 units

Actual sales for the month 600 units

Closing stock for the month 100 units

Difference between absorption and marginal costing:

In marginal costing, difference cost which is related with productivity are apportioned

whereas in absorption costing all type of costs are carried out on a particular basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product cost includes variable cost in marginal costing whereas absorption costing

includes both fixed and variable cost (Shah, Malik and Malik, 2011).

Overheads are divided in variable and fixed in marginal costing and in absorption costing

overheads are divided in administration, production and distribution and selling.

M2

Advance Construction Group Ltd can use techniques of management accounting so as to

improve financial growth in market. The construction industry have approx 50 employees and

there turnover is £500, 000. So to increase their turnover they can use some functions to enhance

their performance. Some of the techniques are:

Absorption technique: This technique is used by entity for calculating their overall

expense. With the help of this they will be able to make income statements so that there will be

overall management of account (Renz, 2016). Advance Construction Group Ltd total fixed

production is £200 and total gross profit is £9800. On the basis of it they will assess their growth

in financial terms so that success can be achieved in market.

Cost volume profit technique: With the help of this approach, Advance Construction

Group Ltd can analyse their overall cost so as to identify their profit level. This will give benefit

to the construction industry, because of this they will be able to make growth.

D2

Entities are doing their business and performing business operations in the environment

of business so as to improve their growth (Pipan and Czarniawska, 2010). Here, Advance

Construction Group Ltd can use several techniques and methods so as to calculate their financial

data. With the help of these all expenses of the entity can be identified to make growth and

success. According to the method of marginal costing , net profit is 7500. By this effective

strategies can be made by business.

includes both fixed and variable cost (Shah, Malik and Malik, 2011).

Overheads are divided in variable and fixed in marginal costing and in absorption costing

overheads are divided in administration, production and distribution and selling.

M2

Advance Construction Group Ltd can use techniques of management accounting so as to

improve financial growth in market. The construction industry have approx 50 employees and

there turnover is £500, 000. So to increase their turnover they can use some functions to enhance

their performance. Some of the techniques are:

Absorption technique: This technique is used by entity for calculating their overall

expense. With the help of this they will be able to make income statements so that there will be

overall management of account (Renz, 2016). Advance Construction Group Ltd total fixed

production is £200 and total gross profit is £9800. On the basis of it they will assess their growth

in financial terms so that success can be achieved in market.

Cost volume profit technique: With the help of this approach, Advance Construction

Group Ltd can analyse their overall cost so as to identify their profit level. This will give benefit

to the construction industry, because of this they will be able to make growth.

D2

Entities are doing their business and performing business operations in the environment

of business so as to improve their growth (Pipan and Czarniawska, 2010). Here, Advance

Construction Group Ltd can use several techniques and methods so as to calculate their financial

data. With the help of these all expenses of the entity can be identified to make growth and

success. According to the method of marginal costing , net profit is 7500. By this effective

strategies can be made by business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Advantages and disadvantages of planning tools used in budgetary control in case of

Advance Construction Group Ltd

There are two types of control in budgets used in the entity which is budgetary control

and financial control in management accounting. Budget can be defined as the quantitative

expression of financial plan for a specific period of time. In budget volume of planned sales,

resource quantities, expenses and costs, liabilities, assets and cash flows are included. It defines

plans related to strategies of business, organisation, events and activities. Budgetary control is

the process by which planned results are compared with actual results (Setthasakko, 2010). It is a

system by which cost are controlled and it includes coordination with departments, budget

preparation, establishment of responsibilities, comparison of actual performance with budgeted

one and to take action on results for achieving profitability. With the help of these analysis ,

several differences can be controlled effectively and easily . There are number of budgetary tools

, which are mentioned below : Master Budget: Master budget can be defined as the projection of how administration

expects to conduct every aspect of business in the budgeted period. It gives summary of

projected activities with the help of cash budget , income statements and balance sheet.

Many master budgets include interrelated budgets from various departments (Sánchez-

Rodríguez and Spraakman, 2012). Operational Budget: Operational budget covers expenses and revenues of daily business

activities in entity. Revenue can be defined as the profit whereas expenses can be defined

as the cost. If the budgeting is done on annual basis operating budgets are broken into

periods of small reporting whether monthly or weekly. Cash Flow Budget: Budgets related to cash flow analyse outflow and inflow of cash

regarding daily activities of business. It analyse the ability of the company to take more

money in than it pays out. Cash flow budget is being monitored to examine shortfall

between sales and expenses. It also suggests storage levels and production cycle. Financial Budget: It is helpful for a business make report regarding receiving and

expenditure of money on business scale, which may include revenues from business and

cost and income of capital expenditure. It helps in managing assets such as building,

investment, property, equipments etc (Macintosh and Quattrone, 2010).

P4 Advantages and disadvantages of planning tools used in budgetary control in case of

Advance Construction Group Ltd

There are two types of control in budgets used in the entity which is budgetary control

and financial control in management accounting. Budget can be defined as the quantitative

expression of financial plan for a specific period of time. In budget volume of planned sales,

resource quantities, expenses and costs, liabilities, assets and cash flows are included. It defines

plans related to strategies of business, organisation, events and activities. Budgetary control is

the process by which planned results are compared with actual results (Setthasakko, 2010). It is a

system by which cost are controlled and it includes coordination with departments, budget

preparation, establishment of responsibilities, comparison of actual performance with budgeted

one and to take action on results for achieving profitability. With the help of these analysis ,

several differences can be controlled effectively and easily . There are number of budgetary tools

, which are mentioned below : Master Budget: Master budget can be defined as the projection of how administration

expects to conduct every aspect of business in the budgeted period. It gives summary of

projected activities with the help of cash budget , income statements and balance sheet.

Many master budgets include interrelated budgets from various departments (Sánchez-

Rodríguez and Spraakman, 2012). Operational Budget: Operational budget covers expenses and revenues of daily business

activities in entity. Revenue can be defined as the profit whereas expenses can be defined

as the cost. If the budgeting is done on annual basis operating budgets are broken into

periods of small reporting whether monthly or weekly. Cash Flow Budget: Budgets related to cash flow analyse outflow and inflow of cash

regarding daily activities of business. It analyse the ability of the company to take more

money in than it pays out. Cash flow budget is being monitored to examine shortfall

between sales and expenses. It also suggests storage levels and production cycle. Financial Budget: It is helpful for a business make report regarding receiving and

expenditure of money on business scale, which may include revenues from business and

cost and income of capital expenditure. It helps in managing assets such as building,

investment, property, equipments etc (Macintosh and Quattrone, 2010).

Static Budget: Static budget contain several elements which are not changed with

variation in level of sales. Example of static budget is the overhead cost. Various

department have fixed money in budget which needs to be spend, and it is the duty of

manager to ensure that these amounts are properly spent without over budgeting.

There are various advantages and disadvantages of planning tools which are used in

budgetary control in Advance Construction Group Ltd.

Advantages

Budgetary planning tools make involvement of employees in mentioned entity for the

budget preparation and therefore it motivates employees of Advance Construction Group

Ltd.

It helps officers who are related with management accounting in taking prompt decisions

in the cases where is difference between planned and desired outcome (Nandan, 2010).

It helps officers in making several strategies of future operation.

It helps in the coordination of different departments of Advance Construction Group Ltd,

so that they can work with each other properly so as to get efficient results.

Disadvantages

With the planning tools it is possible that Advance Construction Group Ltd managers

may make high cost in the budget preparation.

Allocation of resources with these tools may be less effective or improper.

These planning tools may put pressure on employees as it creates targets for them (Lukka

and Modell, 2010).

If targets will not get achieved than all departments will blame each other this will

increase disputes.

M3

Budgetary planning tools are used for forecasting and preparation of budget in Advance

Construction Group Ltd. Planning tools will help entity for making budget successful in relation

with various organisation and department. With the help of budgets current expenses can be

managed and projection of future expenses can be made. It helps in making reserves and

accountability. Master budget which the budget of utilities will help in controlling liquidity and

in maintaining revenues and expenses, also helps in giving sales, budget production and capital

variation in level of sales. Example of static budget is the overhead cost. Various

department have fixed money in budget which needs to be spend, and it is the duty of

manager to ensure that these amounts are properly spent without over budgeting.

There are various advantages and disadvantages of planning tools which are used in

budgetary control in Advance Construction Group Ltd.

Advantages

Budgetary planning tools make involvement of employees in mentioned entity for the

budget preparation and therefore it motivates employees of Advance Construction Group

Ltd.

It helps officers who are related with management accounting in taking prompt decisions

in the cases where is difference between planned and desired outcome (Nandan, 2010).

It helps officers in making several strategies of future operation.

It helps in the coordination of different departments of Advance Construction Group Ltd,

so that they can work with each other properly so as to get efficient results.

Disadvantages

With the planning tools it is possible that Advance Construction Group Ltd managers

may make high cost in the budget preparation.

Allocation of resources with these tools may be less effective or improper.

These planning tools may put pressure on employees as it creates targets for them (Lukka

and Modell, 2010).

If targets will not get achieved than all departments will blame each other this will

increase disputes.

M3

Budgetary planning tools are used for forecasting and preparation of budget in Advance

Construction Group Ltd. Planning tools will help entity for making budget successful in relation

with various organisation and department. With the help of budgets current expenses can be

managed and projection of future expenses can be made. It helps in making reserves and

accountability. Master budget which the budget of utilities will help in controlling liquidity and

in maintaining revenues and expenses, also helps in giving sales, budget production and capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.