Happy Traveller Limited: Traditional vs. ABC Costing Analysis Report

VerifiedAdded on 2021/05/31

|13

|1480

|18

Report

AI Summary

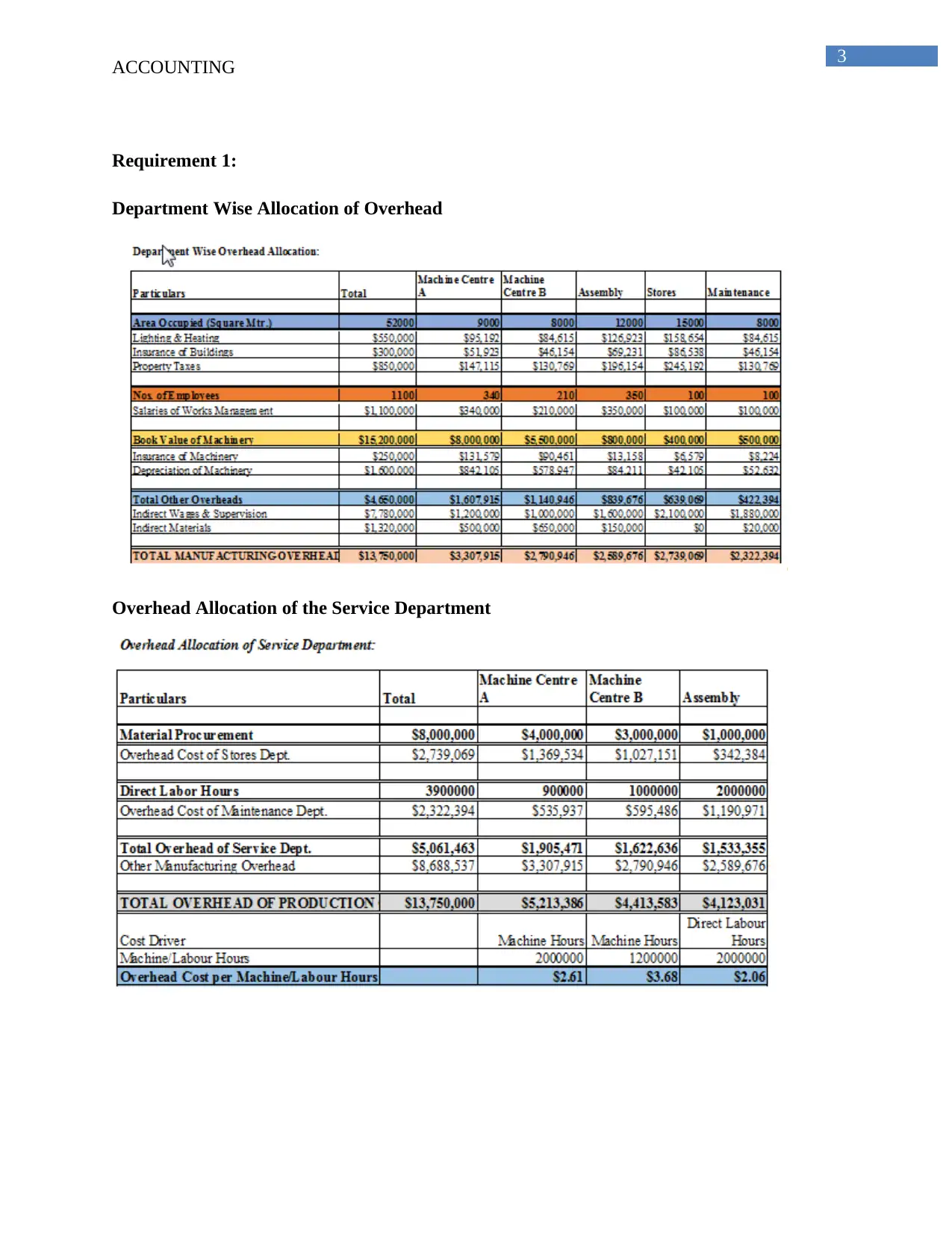

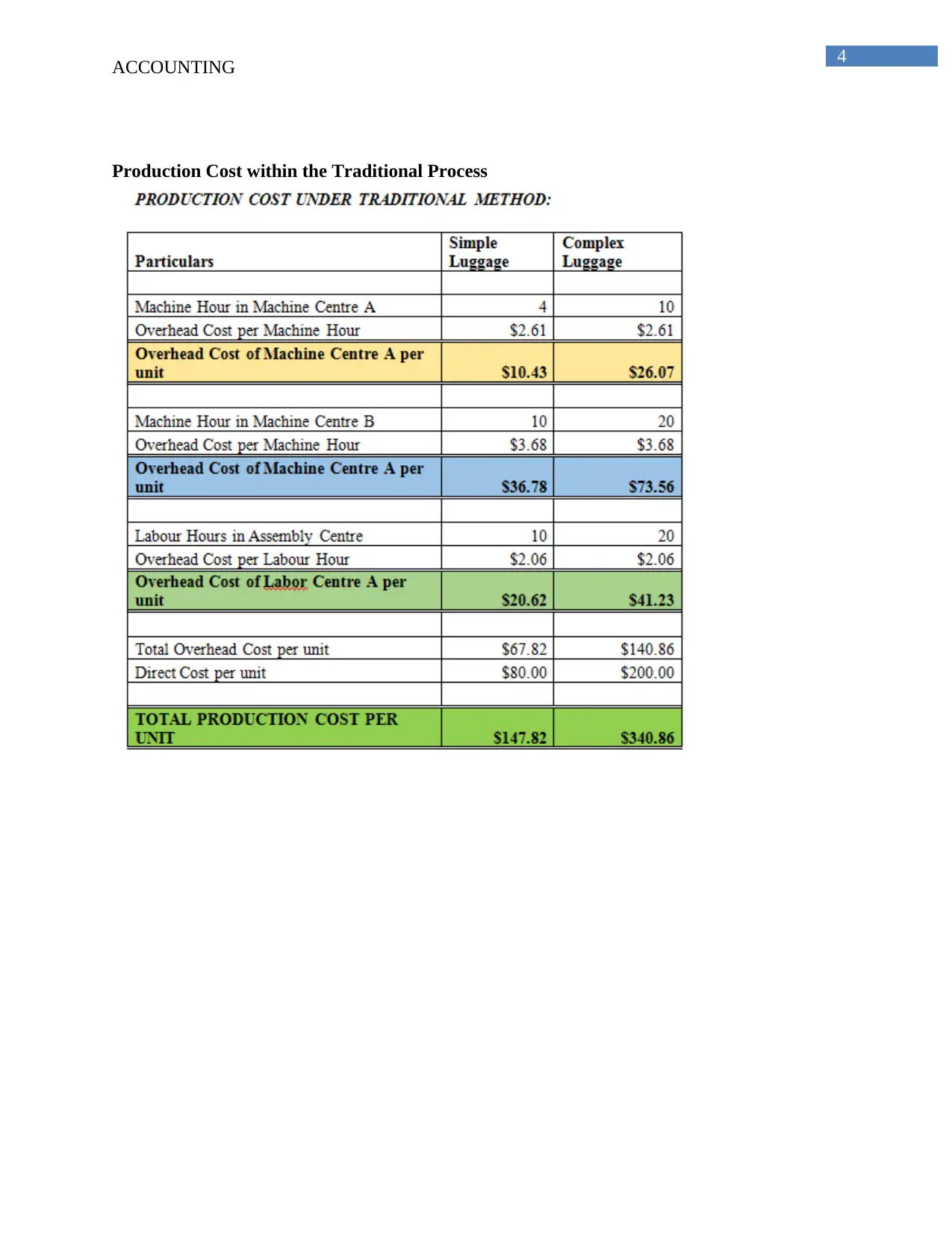

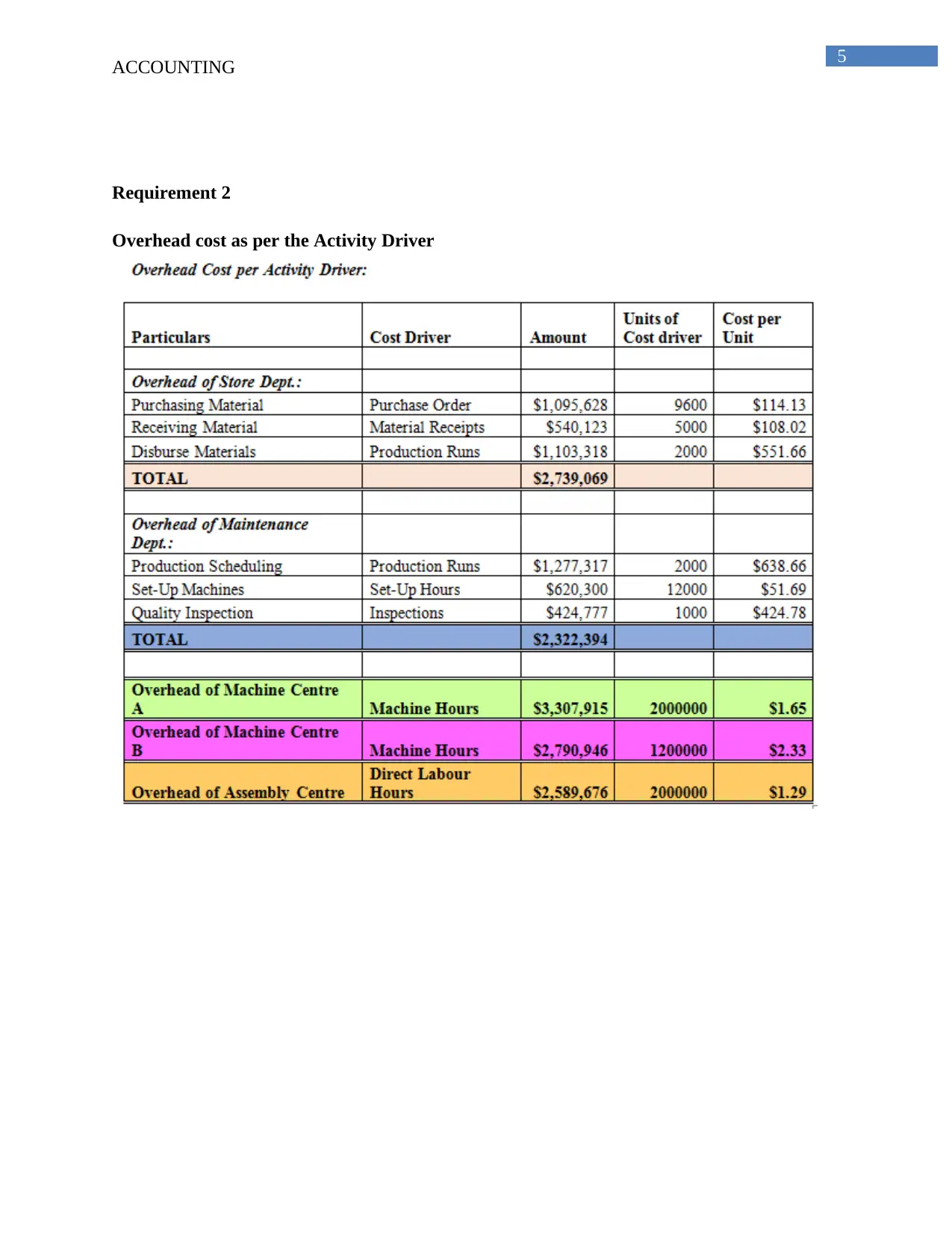

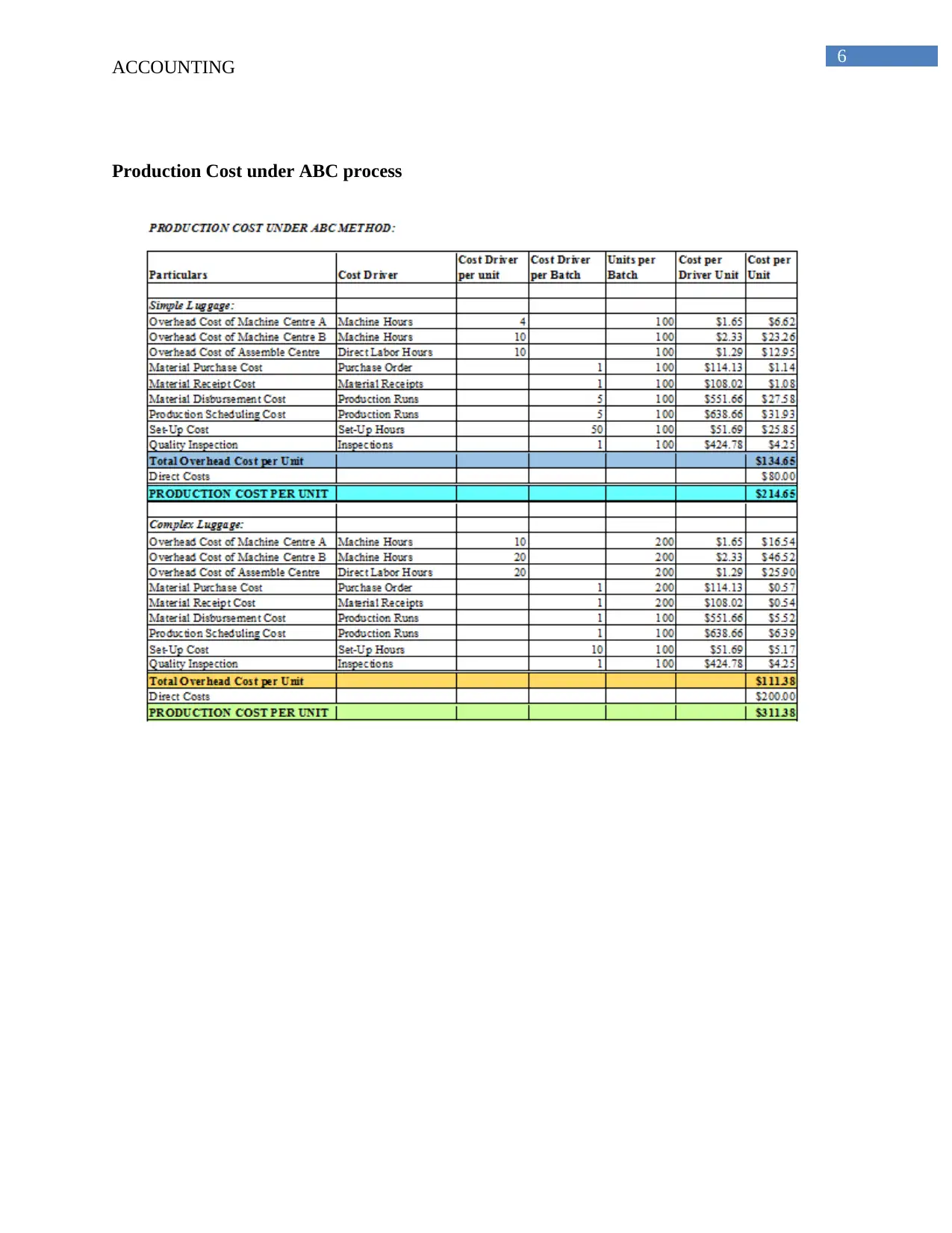

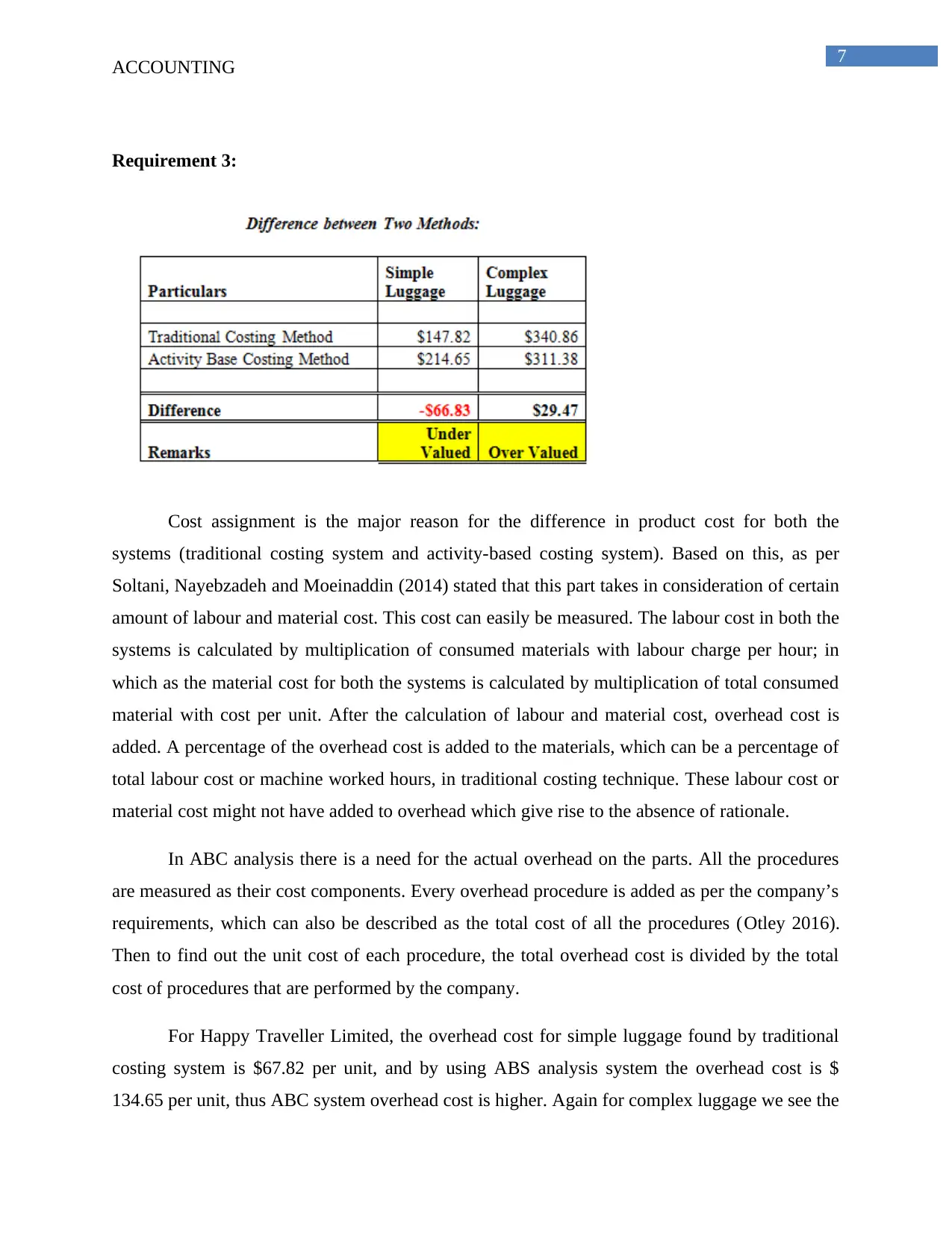

This report presents a comprehensive analysis of the Happy Traveller Limited case study, focusing on the application of traditional and activity-based costing (ABC) systems. The study begins by outlining the company's background as a luggage manufacturer and introduces the two costing methodologies used to determine product costs. The first part of the report details the traditional costing system, including department-wise overhead allocation and production cost calculations. The second part delves into the ABC system, explaining overhead costs based on activity drivers and production costs under this method. A significant portion of the report contrasts the two systems, highlighting the differences in cost assignment and the rationale behind these differences. The analysis includes specific cost comparisons for simple and complex luggage, illustrating how ABC provides a more accurate distribution of costs. The report then discusses the costs and benefits associated with implementing an ABC system, including the need for IT support, employee training, and the identification of non-value-added procedures. Furthermore, it outlines techniques for incorporating ABC based on the company's requirements, such as grouping procedures and leveraging technology. The conclusion emphasizes the importance of the ABC system in accurately allocating costs and its potential to reduce production costs, thereby offering Happy Traveller Limited a path to sustainable growth and competitive advantages.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.