A Comparison of Traditional and Modern Costing Systems in Accounting

VerifiedAdded on 2021/10/29

|9

|1846

|161

Report

AI Summary

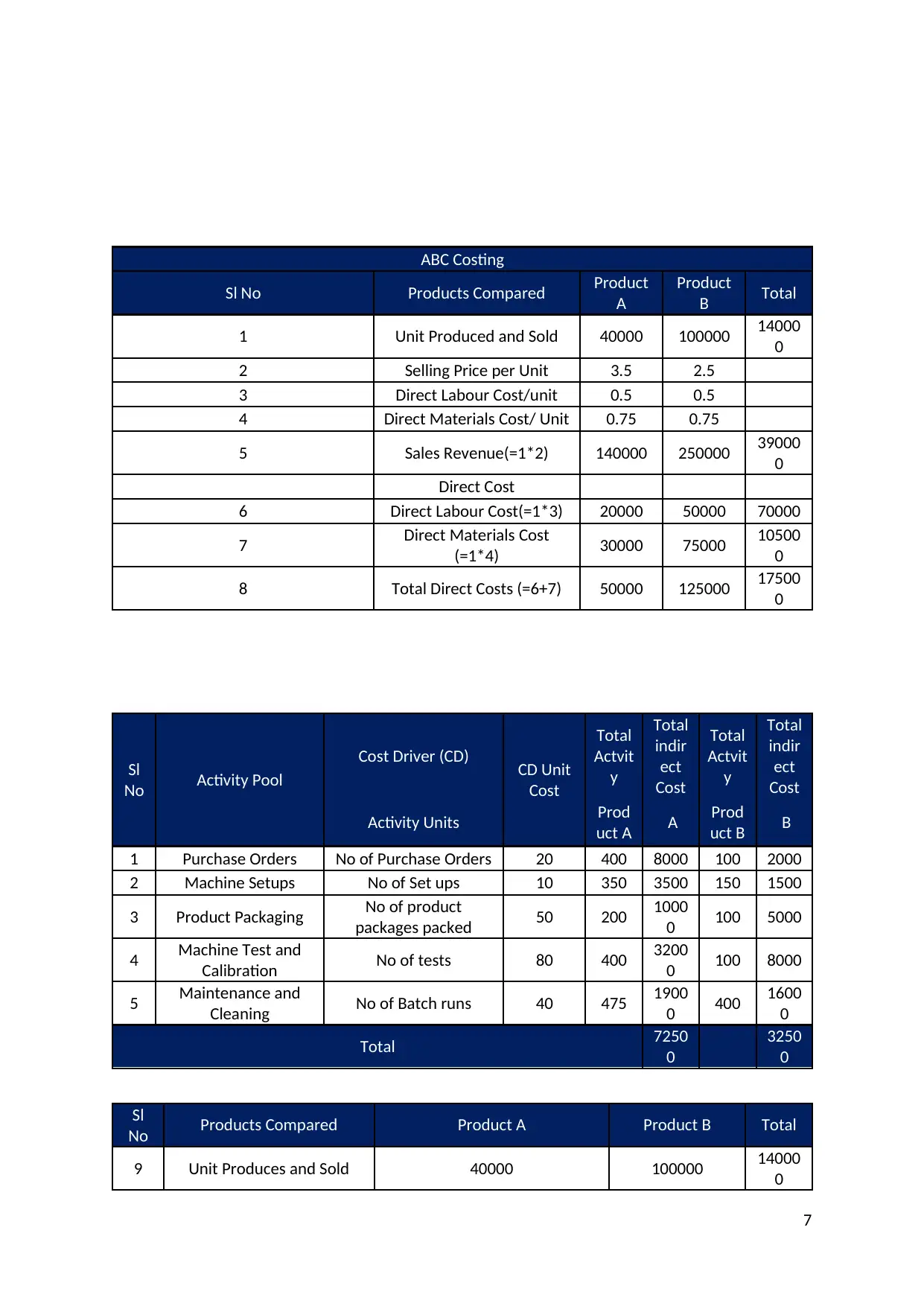

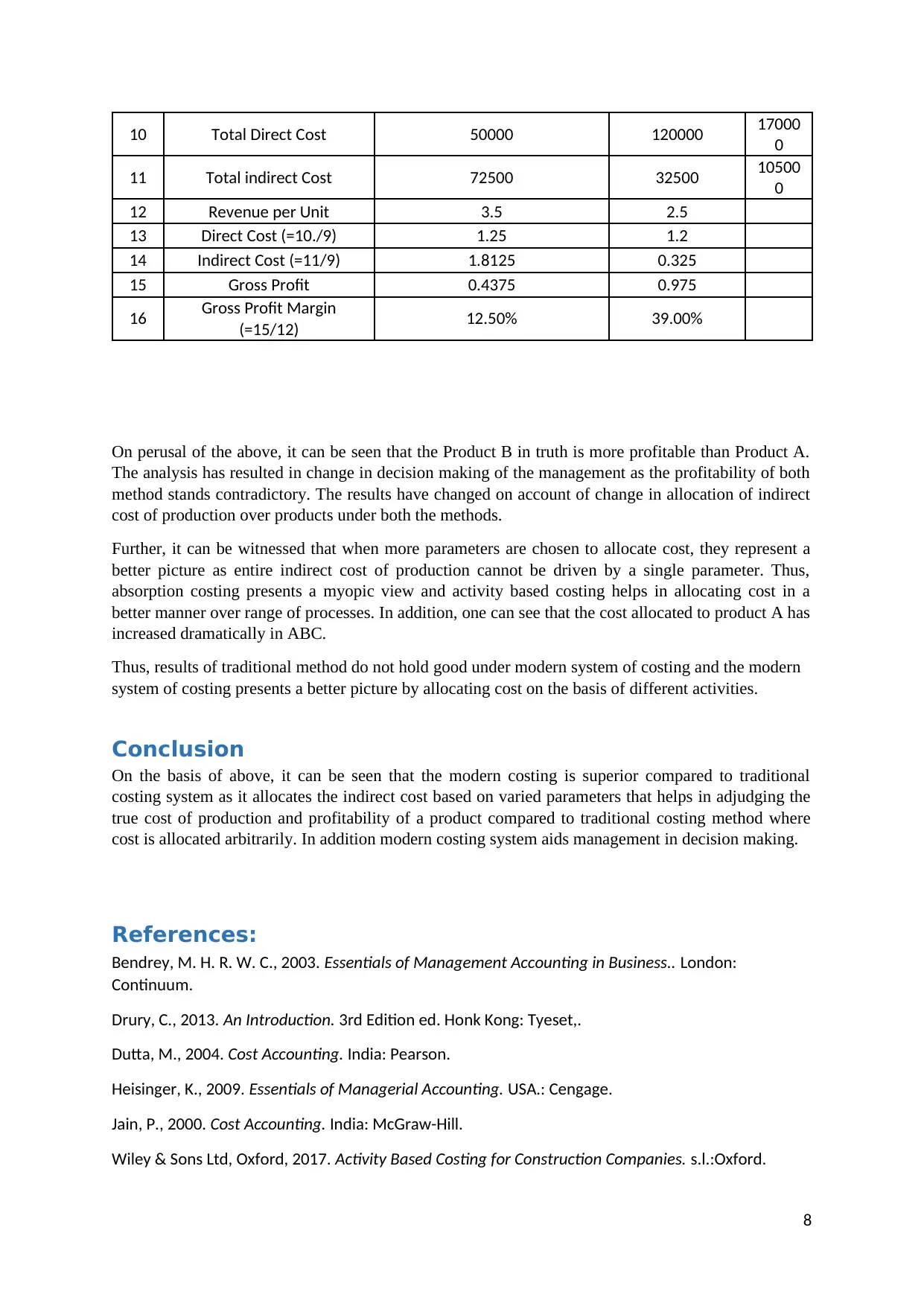

This report provides a comprehensive comparison between traditional and modern costing systems in management accounting. It begins by defining costing systems and their purpose, then delves into the specifics of both traditional and modern (Activity-Based Costing) approaches, outlining their advantages and disadvantages. The report highlights the evolution from traditional costing, which was prevalent in the mid-20th century, to the modern system developed to address the shortcomings of its predecessor. A key focus is on the allocation of indirect costs under each method and the subsequent impact on product profitability and decision-making. A case study is included to illustrate how the choice of costing system affects cost allocation, and how different parameters can lead to varied profitability assessments, ultimately influencing managerial decisions. The analysis shows that Activity-Based Costing offers a more accurate view of product profitability compared to the traditional method, which allocates costs based on a single parameter. The report concludes by emphasizing the superiority of modern costing in providing a more precise assessment of production costs and product profitability, supporting better-informed decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.