Management Accounting Report: Financial Analysis and Decision Making

VerifiedAdded on 2020/01/28

|16

|5088

|31

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its importance for business decision-making, particularly for a company like R.L. Maynard. The report covers key concepts such as assets, liabilities, expenses, revenues, and owner's equity within a management accounting system. It then delves into various methods used in management accounting reports, including budget reports, accounts receivable aging, job cost reports, inventory and manufacturing reports, and performance reports. A significant portion of the report is dedicated to explaining and contrasting marginal costing and absorption costing methods for determining net profit. Furthermore, it discusses how management accounting systems respond to financial problems. The report aims to provide a clear understanding of these concepts and their practical applications in a business context.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...........................................................................................................................................3

P1 Management accounting and essential requirement in different management accounting systems

................................................................................................................................................................3

P2 Different methods used in management accounting report.............................................................5

P3 Calculate cost and difference among marginal costing and absorption costing system....................6

P4 Explaining the advantage and disadvantage of various budgetary planning tools ...........................8

P5 Management accounting system responding financial problems....................................................10

Conclusion............................................................................................................................................12

REFERENCES..............................................................................................................................................13

INTRODUCTION ...........................................................................................................................................3

P1 Management accounting and essential requirement in different management accounting systems

................................................................................................................................................................3

P2 Different methods used in management accounting report.............................................................5

P3 Calculate cost and difference among marginal costing and absorption costing system....................6

P4 Explaining the advantage and disadvantage of various budgetary planning tools ...........................8

P5 Management accounting system responding financial problems....................................................10

Conclusion............................................................................................................................................12

REFERENCES..............................................................................................................................................13

INTRODUCTION

Management accounting is most useful for the company for the purpose of making the most

important decision regards to firm. Thus, it includes both type of financial and non-financial data that are

used for the purpose of make the forwards decisions regards to business. In the present assignment there

is a mainly discussion on the the management accounting and how they are important for R.L. Maynard

to make most important decisions regards to business activities (Picker, 2016). Furthermore, there is also

describe among the marginal costing and absorption costing method that are used by the company to

determining the net profit. Thus, there is an also discussed in the report how management accounting

system respond financial problem.

P1 Management accounting and essential requirement in different management accounting systems

Concept of Management Accounting

Management accounting is a process it involves the managerial function such as

planning, organising, directing and controlling are done by the mangers, to prepare a final report

and making full control in formulation and implementation of an organisation's strategy. In this

way, it is a process of making a managerial report and account so that it will help to implement

day-to-day decisions by the mangers.

Importance of management accounting

It helps to determine the aim of an organisation.

Helps in preparation of plan

Provides better services to customers

Easy to make judgement

It is measuring tool of performance

It also increase the efficiency of a business

Provide effective management control

Difference between management accounting and Financial accounting

Management accounting is presented internally, whereas financial accounting is meant

for external stakeholders. Although financial management is of great importance to current and

potential investors, management accounting is necessary for managers to make current and

Management accounting is most useful for the company for the purpose of making the most

important decision regards to firm. Thus, it includes both type of financial and non-financial data that are

used for the purpose of make the forwards decisions regards to business. In the present assignment there

is a mainly discussion on the the management accounting and how they are important for R.L. Maynard

to make most important decisions regards to business activities (Picker, 2016). Furthermore, there is also

describe among the marginal costing and absorption costing method that are used by the company to

determining the net profit. Thus, there is an also discussed in the report how management accounting

system respond financial problem.

P1 Management accounting and essential requirement in different management accounting systems

Concept of Management Accounting

Management accounting is a process it involves the managerial function such as

planning, organising, directing and controlling are done by the mangers, to prepare a final report

and making full control in formulation and implementation of an organisation's strategy. In this

way, it is a process of making a managerial report and account so that it will help to implement

day-to-day decisions by the mangers.

Importance of management accounting

It helps to determine the aim of an organisation.

Helps in preparation of plan

Provides better services to customers

Easy to make judgement

It is measuring tool of performance

It also increase the efficiency of a business

Provide effective management control

Difference between management accounting and Financial accounting

Management accounting is presented internally, whereas financial accounting is meant

for external stakeholders. Although financial management is of great importance to current and

potential investors, management accounting is necessary for managers to make current and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

future financial decisions. Financial accounting is precise and must adhere to Generally

Accepted Accounting Principles (GAAP), but management accounting is often more of a guess

or estimate, since most managers do not have time for exact numbers when a decision needs to

be made.

There are various things which are required in management accounting system in an

organization by the managers. It includes following:

Assets- Assets are resource which are required for organisation's operational activity. To

make a item as a asset, managers should own it or have a right control and use it. For example: In

a delivery business, truck is used to deliver the products so in this way truck is also known as

asset in a business. In other words, assets also have there economic value and it will provide

economic benefit to the business. So that use of truck to deliver the products is also have there

economic benefit for the business.

Liabilities- In organization liabilities is also known as the business obligations. This is

based on past events such as buy an equipment in a loan for a business is also an obligation of

the business. All this type of obligation which occur by the business can not be avoid in a

business place. For example: In a RL Maynard business organization, mangers want to hire the

employees and pay for them salary as per the work they do in the organization. In this way,

hiring an employees is a past event and giving them salary is an obligation which can be

performed by the mangers, so it is called liabilities in an organisation which cannot be avoided.

Expenses- Expenses are all those which reduces the assets or increase the liabilities for a

given periods. For example, In a truck business fuel which are consumed by the trucks for

delivery is called the expenses but buying a gas is an assets because it reduces the cash. In this

way all the expenses are incurred in a business organisation is a repeating events and it is useful

to successful running the business, Because without making an expenses a business can not

achieve what they want in future. Expenses in an organisation it may be various form, it includes

salary, maintenance expenditure, facility expenses etc. in this way many expenses are done by

the manager in RL Maynard. In a management accounting all the business maintain a accrual

basis, in this business can record each and every transaction before the payment for the expenses.

So that while making an entry in a business, all such expenses are recorded in a debit side of

income & expenditure statements.

Accepted Accounting Principles (GAAP), but management accounting is often more of a guess

or estimate, since most managers do not have time for exact numbers when a decision needs to

be made.

There are various things which are required in management accounting system in an

organization by the managers. It includes following:

Assets- Assets are resource which are required for organisation's operational activity. To

make a item as a asset, managers should own it or have a right control and use it. For example: In

a delivery business, truck is used to deliver the products so in this way truck is also known as

asset in a business. In other words, assets also have there economic value and it will provide

economic benefit to the business. So that use of truck to deliver the products is also have there

economic benefit for the business.

Liabilities- In organization liabilities is also known as the business obligations. This is

based on past events such as buy an equipment in a loan for a business is also an obligation of

the business. All this type of obligation which occur by the business can not be avoid in a

business place. For example: In a RL Maynard business organization, mangers want to hire the

employees and pay for them salary as per the work they do in the organization. In this way,

hiring an employees is a past event and giving them salary is an obligation which can be

performed by the mangers, so it is called liabilities in an organisation which cannot be avoided.

Expenses- Expenses are all those which reduces the assets or increase the liabilities for a

given periods. For example, In a truck business fuel which are consumed by the trucks for

delivery is called the expenses but buying a gas is an assets because it reduces the cash. In this

way all the expenses are incurred in a business organisation is a repeating events and it is useful

to successful running the business, Because without making an expenses a business can not

achieve what they want in future. Expenses in an organisation it may be various form, it includes

salary, maintenance expenditure, facility expenses etc. in this way many expenses are done by

the manager in RL Maynard. In a management accounting all the business maintain a accrual

basis, in this business can record each and every transaction before the payment for the expenses.

So that while making an entry in a business, all such expenses are recorded in a debit side of

income & expenditure statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenues- Revenue are come from sales and delivery of the services. Revenues in result

it increases to assets accounts and decreases the liability account. By selling of goods in a cash

basis it will increasing the asset but in other side selling of goods on credit basis, it will reduces

the liabilities because in this conditions customers are pay for the goods in future time. So that

while making an accounting, Increases in revenue is recorded in debited side of the account and

reduction in revenue is recorded in credit side of the account.

Owner's Equity- Owners equity refers to all those capital which are put into the

organization by the owner to start-up a business. So that in technically, equity means all the

capital which are putting by the owners so that business operation's can run properly or

effectively. In accounting treatment owner's equity will be calculated by assets minus liability, in

the basic accounting equations. So that making an proper records, equity can be recorded as by

increasing in equity will be recorded in credit side of account and decrees in equity will be

recorded in debit side of the accounts. There will be direct relationship between investment and

revenues with equity. When investment or revenue are increases in an organisation than equity

will also increases and if there will be withdrawals and expenses are occurs than it will reduces

the equity in an organisation. Hence all above are essentials which are requiring for any

management accounting system. All the assets, liabilities, expenses, revenue etc. are major tool

for performing any managerial accounting by a manger in an organisation.

P2 Different methods used in management accounting report

Managerial accounting reports help business owners and mangers to make control in

company's performance and prepare such report as per accounting periods are needed.

Depending on time, sensitivity of information or structure of the business different managers

prepare different managerial report such as quarterly, monthly, annually. There are various

methods of making management accounting reports, such as:

Budget Report- Budget reports help small business's mangers to analysis the business

performance, and if the business are in good conditions than manager analysis the various

department's performance and control on there costs. Budget are decided in a business based on

the actual expenses which are occur from prior years. If the budget which are decided in present

time-period for the organisation is not enough than the criteria of budget will be increases, in this

way future estimation of budget amount kept to be high for the future, so that it will fulfil the

it increases to assets accounts and decreases the liability account. By selling of goods in a cash

basis it will increasing the asset but in other side selling of goods on credit basis, it will reduces

the liabilities because in this conditions customers are pay for the goods in future time. So that

while making an accounting, Increases in revenue is recorded in debited side of the account and

reduction in revenue is recorded in credit side of the account.

Owner's Equity- Owners equity refers to all those capital which are put into the

organization by the owner to start-up a business. So that in technically, equity means all the

capital which are putting by the owners so that business operation's can run properly or

effectively. In accounting treatment owner's equity will be calculated by assets minus liability, in

the basic accounting equations. So that making an proper records, equity can be recorded as by

increasing in equity will be recorded in credit side of account and decrees in equity will be

recorded in debit side of the accounts. There will be direct relationship between investment and

revenues with equity. When investment or revenue are increases in an organisation than equity

will also increases and if there will be withdrawals and expenses are occurs than it will reduces

the equity in an organisation. Hence all above are essentials which are requiring for any

management accounting system. All the assets, liabilities, expenses, revenue etc. are major tool

for performing any managerial accounting by a manger in an organisation.

P2 Different methods used in management accounting report

Managerial accounting reports help business owners and mangers to make control in

company's performance and prepare such report as per accounting periods are needed.

Depending on time, sensitivity of information or structure of the business different managers

prepare different managerial report such as quarterly, monthly, annually. There are various

methods of making management accounting reports, such as:

Budget Report- Budget reports help small business's mangers to analysis the business

performance, and if the business are in good conditions than manager analysis the various

department's performance and control on there costs. Budget are decided in a business based on

the actual expenses which are occur from prior years. If the budget which are decided in present

time-period for the organisation is not enough than the criteria of budget will be increases, in this

way future estimation of budget amount kept to be high for the future, so that it will fulfil the

organisation need. There are many cases, in which budget are used to give bonus to the

employees for meeting the specific goals.

Accounts Receivables Aging- Accounts Receivables Aging is a critical tool of making

report which mange the cash flow for companies that increase credit to their customers. This is a

report which make complete list of all those customers which are unpaid or unsues credit memos

by date ranges. This is a important method in management accounting which are determine

which invoices are overdue for payment. By using this report, it also contain the contact

information of each customers. This report is used by management to determine the effectiveness

of credit and collection functions. This report describes that the customers are good in credit

risks or not. By making periodically report it also helpful to look at the old debts in a company.

Job Cost Reports- Job cost reports shows all those expenses which are occur for a

specific project. This reports are make by the mangers so that it will help to match between the

revenue and profitability of an organisation. It includes all those activity, in which manger can

focus in such areas which gives high opportunities to gain there profits in comparison of those

area which can not generate the profitability of the organisation. In this way. mangers can

prepare a report so that they can more focus on those profitable areas and make expenses to

make it more grow and it also analysis the waste areas which gives less profitability and also

examine the progress so that manager can take effective actions to improve such waste before

costs escalate.

Inventory and Manufacturing- Inventory and manufacturing report make by the

organisation to achieve or determine that manufacturing processes are more efficient or not. This

reports include all those items such as inventory waste, hourly labour cost and per unit overhead

costs etc. In this manger can compare different assembly lines within a company to check that in

which way organisation can improve or offer bonuses to achieve the best performance.

Performance report- In management accounting report, performance report are prepared

to helps the managers plan for future demand in production which increases the cost. Managerial

accountant prepare a budget report to make comparison between actual expenditure and revenues

to the budgeted amounts. While making a budget report all the different calculation are listed in

it and all such amount related to the information are recorded in performance report. This

performance report are prepare as per the time such as quarterly, half-yearly, annually etc. In this

employees for meeting the specific goals.

Accounts Receivables Aging- Accounts Receivables Aging is a critical tool of making

report which mange the cash flow for companies that increase credit to their customers. This is a

report which make complete list of all those customers which are unpaid or unsues credit memos

by date ranges. This is a important method in management accounting which are determine

which invoices are overdue for payment. By using this report, it also contain the contact

information of each customers. This report is used by management to determine the effectiveness

of credit and collection functions. This report describes that the customers are good in credit

risks or not. By making periodically report it also helpful to look at the old debts in a company.

Job Cost Reports- Job cost reports shows all those expenses which are occur for a

specific project. This reports are make by the mangers so that it will help to match between the

revenue and profitability of an organisation. It includes all those activity, in which manger can

focus in such areas which gives high opportunities to gain there profits in comparison of those

area which can not generate the profitability of the organisation. In this way. mangers can

prepare a report so that they can more focus on those profitable areas and make expenses to

make it more grow and it also analysis the waste areas which gives less profitability and also

examine the progress so that manager can take effective actions to improve such waste before

costs escalate.

Inventory and Manufacturing- Inventory and manufacturing report make by the

organisation to achieve or determine that manufacturing processes are more efficient or not. This

reports include all those items such as inventory waste, hourly labour cost and per unit overhead

costs etc. In this manger can compare different assembly lines within a company to check that in

which way organisation can improve or offer bonuses to achieve the best performance.

Performance report- In management accounting report, performance report are prepared

to helps the managers plan for future demand in production which increases the cost. Managerial

accountant prepare a budget report to make comparison between actual expenditure and revenues

to the budgeted amounts. While making a budget report all the different calculation are listed in

it and all such amount related to the information are recorded in performance report. This

performance report are prepare as per the time such as quarterly, half-yearly, annually etc. In this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

way, performance report are created by the manger in an organisation to analysis the

performance or capability of the employee within a given time.

Other Report- Other reports also prepared by the managerial accountant. In which order

information report are prepared by the mangers. In all such orders which are receive or deliver

by the organisation can be recorded effectively, so that it can make mangers suitability to

understand the business performance or capability. It also include such type of report in which

manager can focus in such area which give the profitability so in this way manger can expenses

in such area to achieve more profitability. Hence in this way all above the various reports

prepared by the manager in management of accounting report so that it will help them to

determine the current and present condition of the company by analysing there performance and

capability.

P3 Calculate cost and difference among marginal costing and absorption costing system

Income statement: It is used by most of the company to understand the financial position for a

specific accounting period. It is summarized into revenues and expenses that are inured by the business

activities by both non-operating and operating activities. It indicated the firm outcomes of operating

during a specific time period that describe how the firm perform. Revenue can be defined as a inflow of

inventory in returns for goods they earned money and expenses is a sacrifice cost that are inured during

a period. In regard to this, R.L. Maynard determining the net profit through adopting marginal costing

and absorption costing method to know the financial position of a firm.

Difference among marginal costing and absorption costing method

Marginal costing is that type of management costing method through which they ascertaining

the both type of expenses are fixed and variable cost. Under this method, the variable cost are

to be charged into the operations but the fixed expenses are excluding at the time of

ascertaining the net profit during the period( Otley, 2016). Beside this, the absorption costing

are to be consider as a full costing in which it take all the type of cost whether its is variable

expenses and fixed expenses that are absorbed at the time of produced total units. Most of the

scholar has researched on this they say that marginal costing method is best management

costing to determine the net profit while other may adopted absorption costing method.

Marginal costing are to be known as a variable costing as it only consider the variable cost as it is

most useful to make decision that are relating to fixed and variable cost to finding out the

performance or capability of the employee within a given time.

Other Report- Other reports also prepared by the managerial accountant. In which order

information report are prepared by the mangers. In all such orders which are receive or deliver

by the organisation can be recorded effectively, so that it can make mangers suitability to

understand the business performance or capability. It also include such type of report in which

manager can focus in such area which give the profitability so in this way manger can expenses

in such area to achieve more profitability. Hence in this way all above the various reports

prepared by the manager in management of accounting report so that it will help them to

determine the current and present condition of the company by analysing there performance and

capability.

P3 Calculate cost and difference among marginal costing and absorption costing system

Income statement: It is used by most of the company to understand the financial position for a

specific accounting period. It is summarized into revenues and expenses that are inured by the business

activities by both non-operating and operating activities. It indicated the firm outcomes of operating

during a specific time period that describe how the firm perform. Revenue can be defined as a inflow of

inventory in returns for goods they earned money and expenses is a sacrifice cost that are inured during

a period. In regard to this, R.L. Maynard determining the net profit through adopting marginal costing

and absorption costing method to know the financial position of a firm.

Difference among marginal costing and absorption costing method

Marginal costing is that type of management costing method through which they ascertaining

the both type of expenses are fixed and variable cost. Under this method, the variable cost are

to be charged into the operations but the fixed expenses are excluding at the time of

ascertaining the net profit during the period( Otley, 2016). Beside this, the absorption costing

are to be consider as a full costing in which it take all the type of cost whether its is variable

expenses and fixed expenses that are absorbed at the time of produced total units. Most of the

scholar has researched on this they say that marginal costing method is best management

costing to determine the net profit while other may adopted absorption costing method.

Marginal costing are to be known as a variable costing as it only consider the variable cost as it is

most useful to make decision that are relating to fixed and variable cost to finding out the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

product for production. Beside this, absorption costing method is also used for the purpose of

valuation of inventory in which they consider all the manufacturing cost that are allocating into

the cost centers to recognizing the total cost of production. Thus, all the manufacturing

expenses are involve all variable as well as fixed expenses.

Marginal costing includes all the variable costing that are relating to product regards to cost.

Whereas, the fixed cost are to considering as periodic cost. Therefore, the absorption costing

method taken both type of costing are fixed and variable cost that are to be consider as a

product cost.

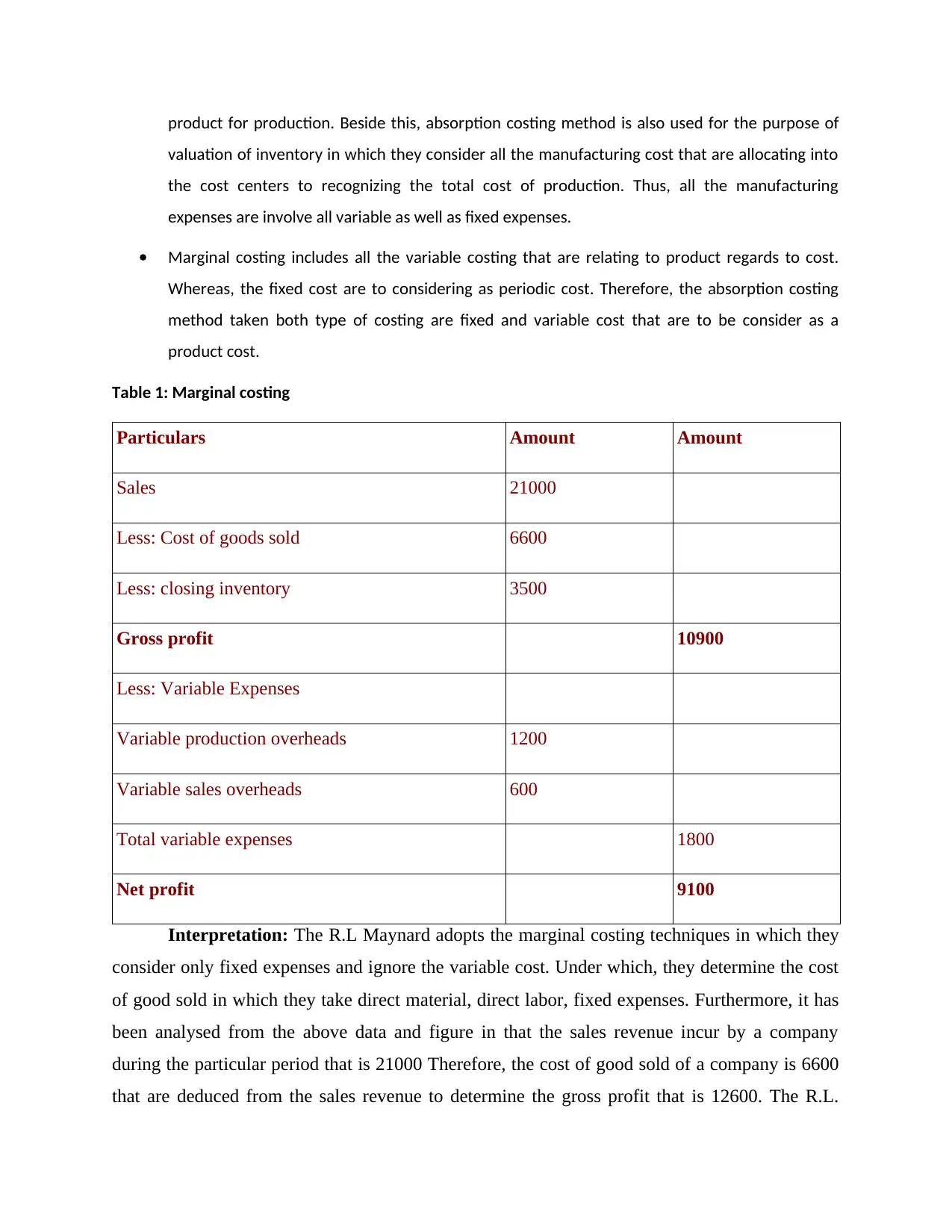

Table 1: Marginal costing

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Less: closing inventory 3500

Gross profit 10900

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Net profit 9100

Interpretation: The R.L Maynard adopts the marginal costing techniques in which they

consider only fixed expenses and ignore the variable cost. Under which, they determine the cost

of good sold in which they take direct material, direct labor, fixed expenses. Furthermore, it has

been analysed from the above data and figure in that the sales revenue incur by a company

during the particular period that is 21000 Therefore, the cost of good sold of a company is 6600

that are deduced from the sales revenue to determine the gross profit that is 12600. The R.L.

valuation of inventory in which they consider all the manufacturing cost that are allocating into

the cost centers to recognizing the total cost of production. Thus, all the manufacturing

expenses are involve all variable as well as fixed expenses.

Marginal costing includes all the variable costing that are relating to product regards to cost.

Whereas, the fixed cost are to considering as periodic cost. Therefore, the absorption costing

method taken both type of costing are fixed and variable cost that are to be consider as a

product cost.

Table 1: Marginal costing

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Less: closing inventory 3500

Gross profit 10900

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Net profit 9100

Interpretation: The R.L Maynard adopts the marginal costing techniques in which they

consider only fixed expenses and ignore the variable cost. Under which, they determine the cost

of good sold in which they take direct material, direct labor, fixed expenses. Furthermore, it has

been analysed from the above data and figure in that the sales revenue incur by a company

during the particular period that is 21000 Therefore, the cost of good sold of a company is 6600

that are deduced from the sales revenue to determine the gross profit that is 12600. The R.L.

Maynard determine net profit by deducting only fixed expenses from the gross profit that is

9100.

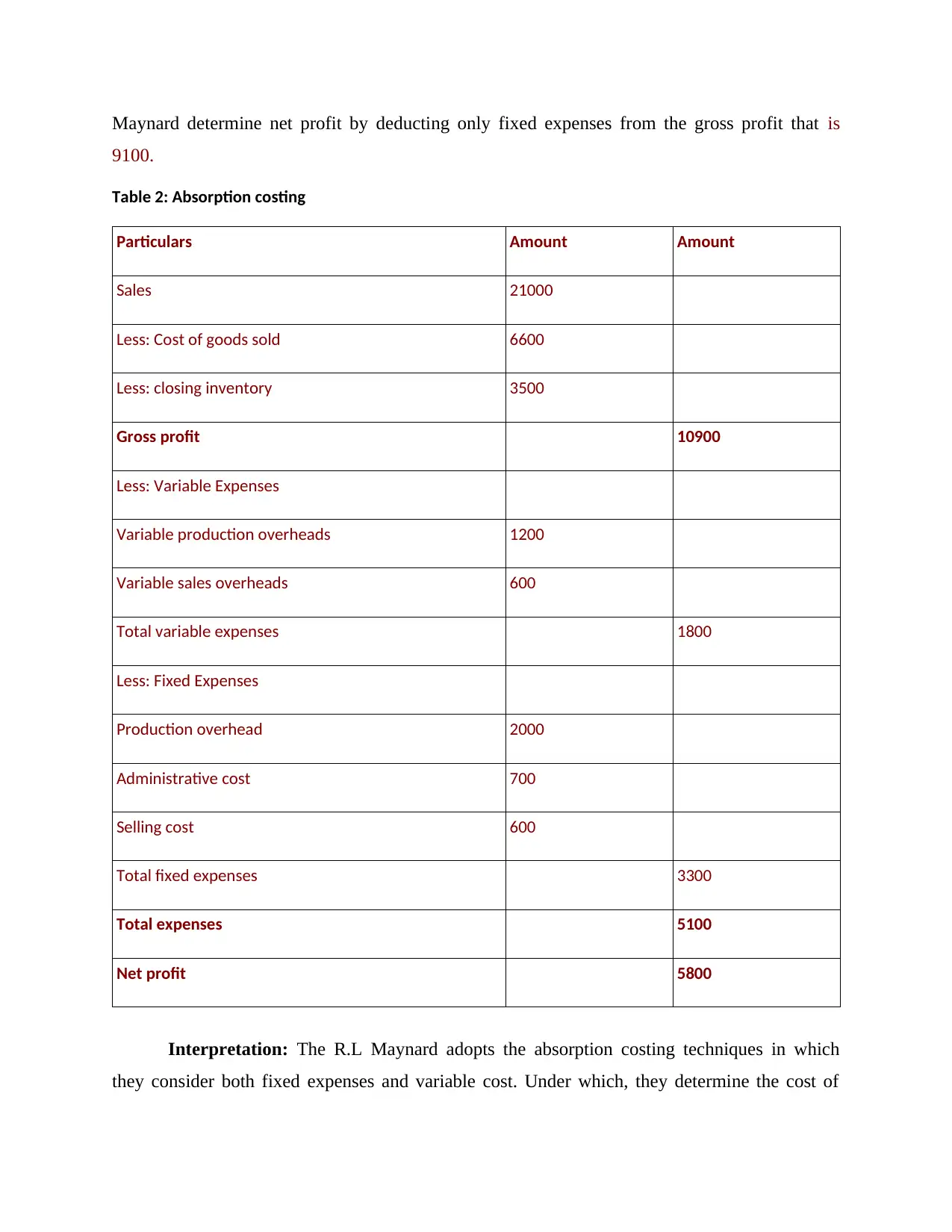

Table 2: Absorption costing

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Less: closing inventory 3500

Gross profit 10900

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit 5800

Interpretation: The R.L Maynard adopts the absorption costing techniques in which

they consider both fixed expenses and variable cost. Under which, they determine the cost of

9100.

Table 2: Absorption costing

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Less: closing inventory 3500

Gross profit 10900

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit 5800

Interpretation: The R.L Maynard adopts the absorption costing techniques in which

they consider both fixed expenses and variable cost. Under which, they determine the cost of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

good sold in which they take direct material, direct labor, fixed expenses and variable expenses.

Furthermore, it has been analysed from the above data and figure in that the sales revenue incur

by a company during the particular period that is 21000 Therefore, the cost of good sold of a

company is 6600 that are deduced from the sales revenue to determine the gross profit that is

10900 The R.L. Maynard determine net profit by deducting all type of cost from the gross profit

that is 5800.

P4 Explaining the advantage and disadvantage of various budgetary planning tools

Budgetary planning & controlling is a process that is followed to prepare a number of

budgets like material purchase, marketing, labour, variable overhead, cash budget, production

budget and many others through forecasting the possible financial outcome of the activities that

will be carried out by Unicorn in the next year. Thus, it can be presented as a quantitative

expression of the result of future business activities by the projection of income & spendings.

The main focus or aim of using budgetary plan in the business is to attain the targeted aims &

goals covering both the revenues & the possible spending. It helps the business entity to attain

the decided outcome by implementing the effective control in order to ensure better use of

resources at an controlled cost and maximum revenue. A multiple of methods are being available

to Unicorn’s managerial team which can be assisted the entity in creating budgets, that are stated

below:

Incremental budgeting: This is a classical way or approach of budgeting which begins

with the previous period budget as a starting point because it believes that operations and regular

activities that has been carried out by Unicorn in historical years will be defintely continue in the

future also. However, for the projection about future, it add some additional amount in both the

revenue & expenses and justify only the incremental charges and income.

Advantages:

The primary benefit of this method is its simplicity because it uses either the latest period budget

or actual performance which can be easily verified.

It is helpful in ensuring proper funding requirement that will be necessary to have to run the

programme.

Furthermore, it has been analysed from the above data and figure in that the sales revenue incur

by a company during the particular period that is 21000 Therefore, the cost of good sold of a

company is 6600 that are deduced from the sales revenue to determine the gross profit that is

10900 The R.L. Maynard determine net profit by deducting all type of cost from the gross profit

that is 5800.

P4 Explaining the advantage and disadvantage of various budgetary planning tools

Budgetary planning & controlling is a process that is followed to prepare a number of

budgets like material purchase, marketing, labour, variable overhead, cash budget, production

budget and many others through forecasting the possible financial outcome of the activities that

will be carried out by Unicorn in the next year. Thus, it can be presented as a quantitative

expression of the result of future business activities by the projection of income & spendings.

The main focus or aim of using budgetary plan in the business is to attain the targeted aims &

goals covering both the revenues & the possible spending. It helps the business entity to attain

the decided outcome by implementing the effective control in order to ensure better use of

resources at an controlled cost and maximum revenue. A multiple of methods are being available

to Unicorn’s managerial team which can be assisted the entity in creating budgets, that are stated

below:

Incremental budgeting: This is a classical way or approach of budgeting which begins

with the previous period budget as a starting point because it believes that operations and regular

activities that has been carried out by Unicorn in historical years will be defintely continue in the

future also. However, for the projection about future, it add some additional amount in both the

revenue & expenses and justify only the incremental charges and income.

Advantages:

The primary benefit of this method is its simplicity because it uses either the latest period budget

or actual performance which can be easily verified.

It is helpful in ensuring proper funding requirement that will be necessary to have to run the

programme.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This budgeting approach assure operational stability that believes that all the divisions of

Unicorn will operate their regular functions in a consistent or stabilized manner.

Disadvantages:

The major limitation of this method is it fosters overspending, however, the focus should be on

curtailment of cost to gain the benefits of higher return. The method believes that past

operations will be continue consistently which leads to encourage wasteful spending.

As it makes very minor changes in the budget therefore, there is very little incentives provided to

the Unicorn’s departmental managers to review & examine the budget comprehensively.

It leads to arise budgetary slack by little bit or small improvement in revenues and high growth

in spending so that they will attain favourable variances.

Zero-based budgeting: It is a modern way which begins with zero to arrive a budget for

the new period. The method involves detailed analysis by the Unicorn’s mangers of the market

trends and external industrial forces for the purpose of forecasting. By this, each & every

element of budget is justified very well in order to create a budget for the newer period.

Advantages:

Unlike IB, it does not believes in the previous year’s resource allocation system and do not apply

the same method for the current year.

Inefficient, wasteful and obsolete activities are eliminated from the operations so as to bring

improvement in the net yield by controlled the cost.

Disadvantages:

Zero-based budgeting requires paper work to justify the inclusion of every item that goes into a

budget. In this manager can take a documentation in ranking manner to each item according to

its importance and cost.

It is very time consuming process because to make proper implementation of work, there should

be training program of there workers, so that all this process take lots of time.

As per above there are many advantages of budgetary control techniques such as, it

defines the goals, plan and objects of the enterprise. It also fixes the target and secure better co-

ordination among various departments. Budgetary control helps to management in finding up the

Unicorn will operate their regular functions in a consistent or stabilized manner.

Disadvantages:

The major limitation of this method is it fosters overspending, however, the focus should be on

curtailment of cost to gain the benefits of higher return. The method believes that past

operations will be continue consistently which leads to encourage wasteful spending.

As it makes very minor changes in the budget therefore, there is very little incentives provided to

the Unicorn’s departmental managers to review & examine the budget comprehensively.

It leads to arise budgetary slack by little bit or small improvement in revenues and high growth

in spending so that they will attain favourable variances.

Zero-based budgeting: It is a modern way which begins with zero to arrive a budget for

the new period. The method involves detailed analysis by the Unicorn’s mangers of the market

trends and external industrial forces for the purpose of forecasting. By this, each & every

element of budget is justified very well in order to create a budget for the newer period.

Advantages:

Unlike IB, it does not believes in the previous year’s resource allocation system and do not apply

the same method for the current year.

Inefficient, wasteful and obsolete activities are eliminated from the operations so as to bring

improvement in the net yield by controlled the cost.

Disadvantages:

Zero-based budgeting requires paper work to justify the inclusion of every item that goes into a

budget. In this manager can take a documentation in ranking manner to each item according to

its importance and cost.

It is very time consuming process because to make proper implementation of work, there should

be training program of there workers, so that all this process take lots of time.

As per above there are many advantages of budgetary control techniques such as, it

defines the goals, plan and objects of the enterprise. It also fixes the target and secure better co-

ordination among various departments. Budgetary control helps to management in finding up the

responsibility. It also help to reduce cost in production by eliminating the wasteful expenses. It

also gives centralized control in an organisation. By promoting cost consciousness among the

employees, budgetary control brings in efficiency and economy. Budgetary control also help to

make smooth functioning of the organisation. At last budgetary control help to give the guidance

that in which areas action are required to improve its performance. But in other side it also have

there some disadvantage such as it is very difficult process to estimate the accurate budget in

inflationary conditions. It also have high expenditure during the operational activity, so that

small business can not afford such type of strategy. Budget are always prepared on the basis of

future estimation, such type of estimation are uncertain in future because it is only a management

tool. The success of budgetary control is depend on the support of the top management level. So

in this way budgetary control is useful techniques for management accounting but it also has

there some limitation which make the techniques less effective in management accounting

system.

P5 Management accounting system responding financial problems

The R.L Maynard adopts the management accounting system for the purpose of

responding the financial problems these are describe as follows:-

Traditional management accounting system: It is used by the R.L. Maynard ltd. for the

purpose of tracking costs through adopting process costing or job costing methods. It

assist the company to ascertaining the allocating cost that are regards to direct labor,

direct material and manufacturing overhead. Thus, job costing method is used by the

company for the allocating cost for the larger projects. Furthermore, the cited company

used process costing method through which they allocating costs that are based upon the

process numbers that are using for the purpose of establish homogeneous products.

Lean accounting system: It is that type of accounting management system that are

adopted by R.L Maynard company for the aim of minimizing costs through removing

wastage. Under this system assist the firm to quickly providing financial data for making

the immediate decisions, measured profits and also evaluate value streams. Thus, this

lean accounting system helps in cut the excess wastage from wastage (Noordin,

Zainuddin and Mail,2017). There are reason among one is a positive that used the lean

accounting to timely understand information on right time and accurate manner.

also gives centralized control in an organisation. By promoting cost consciousness among the

employees, budgetary control brings in efficiency and economy. Budgetary control also help to

make smooth functioning of the organisation. At last budgetary control help to give the guidance

that in which areas action are required to improve its performance. But in other side it also have

there some disadvantage such as it is very difficult process to estimate the accurate budget in

inflationary conditions. It also have high expenditure during the operational activity, so that

small business can not afford such type of strategy. Budget are always prepared on the basis of

future estimation, such type of estimation are uncertain in future because it is only a management

tool. The success of budgetary control is depend on the support of the top management level. So

in this way budgetary control is useful techniques for management accounting but it also has

there some limitation which make the techniques less effective in management accounting

system.

P5 Management accounting system responding financial problems

The R.L Maynard adopts the management accounting system for the purpose of

responding the financial problems these are describe as follows:-

Traditional management accounting system: It is used by the R.L. Maynard ltd. for the

purpose of tracking costs through adopting process costing or job costing methods. It

assist the company to ascertaining the allocating cost that are regards to direct labor,

direct material and manufacturing overhead. Thus, job costing method is used by the

company for the allocating cost for the larger projects. Furthermore, the cited company

used process costing method through which they allocating costs that are based upon the

process numbers that are using for the purpose of establish homogeneous products.

Lean accounting system: It is that type of accounting management system that are

adopted by R.L Maynard company for the aim of minimizing costs through removing

wastage. Under this system assist the firm to quickly providing financial data for making

the immediate decisions, measured profits and also evaluate value streams. Thus, this

lean accounting system helps in cut the excess wastage from wastage (Noordin,

Zainuddin and Mail,2017). There are reason among one is a positive that used the lean

accounting to timely understand information on right time and accurate manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.