Financial Report: Analysis of Accounting Cycle for Paul Services

VerifiedAdded on 2023/06/04

|14

|2246

|252

Report

AI Summary

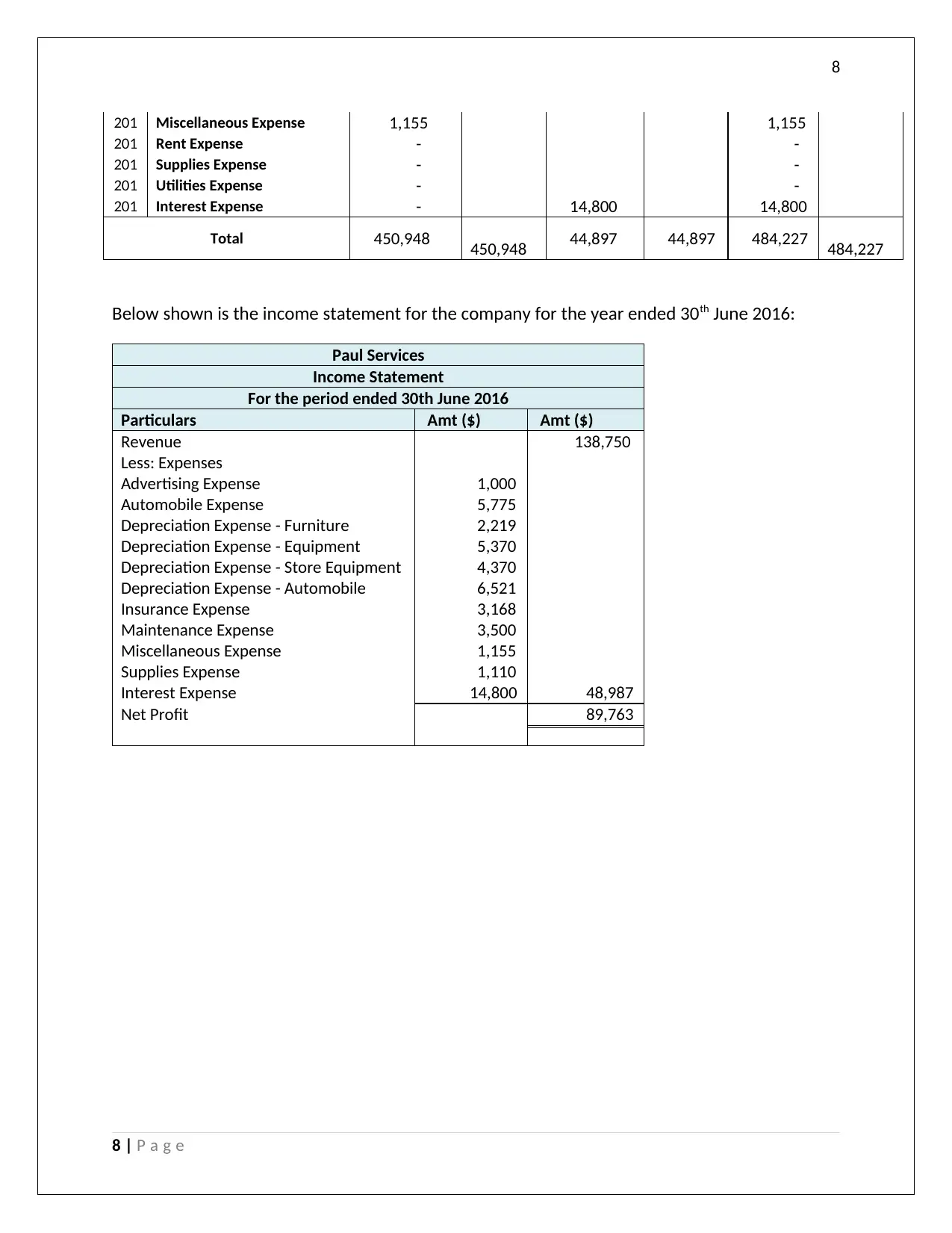

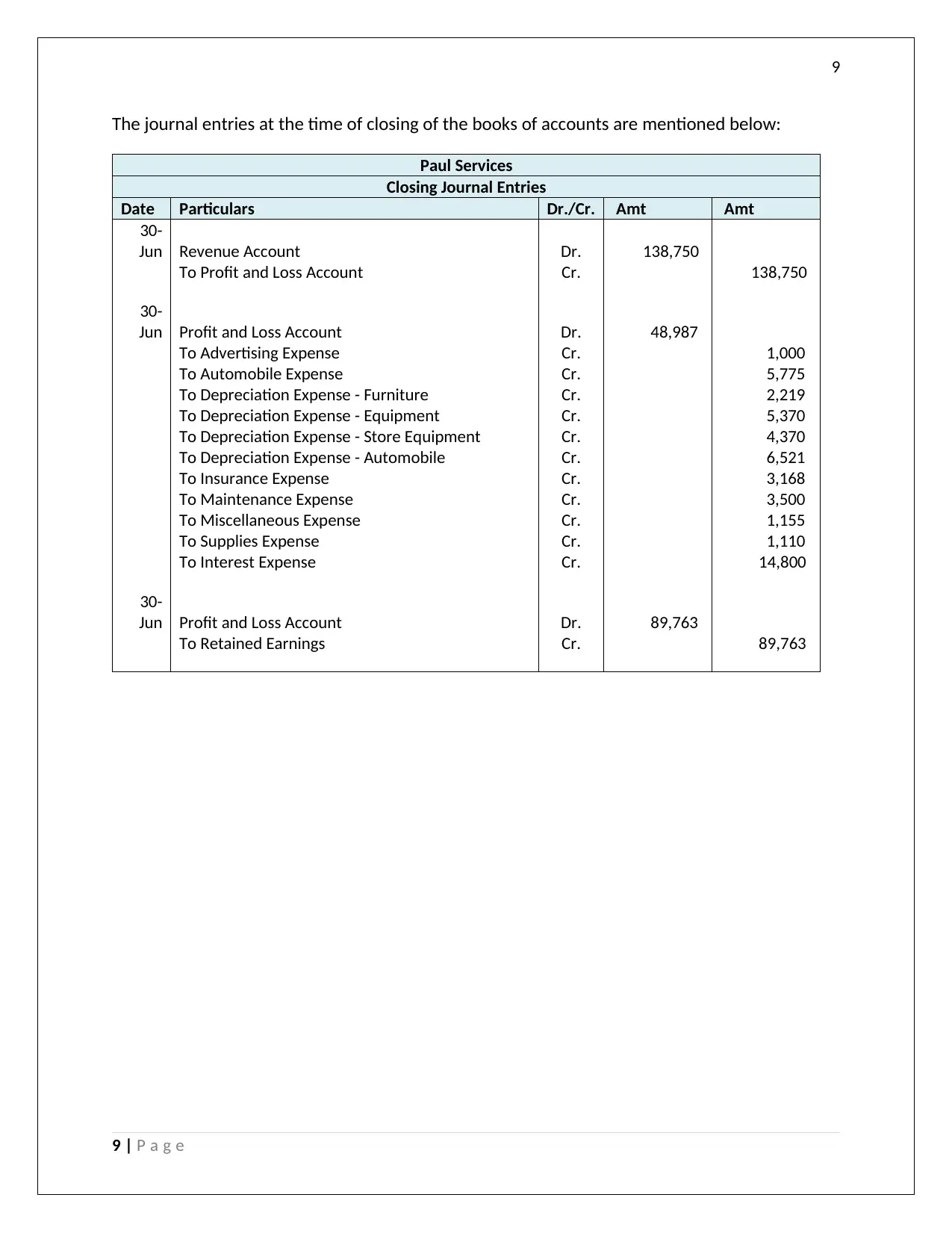

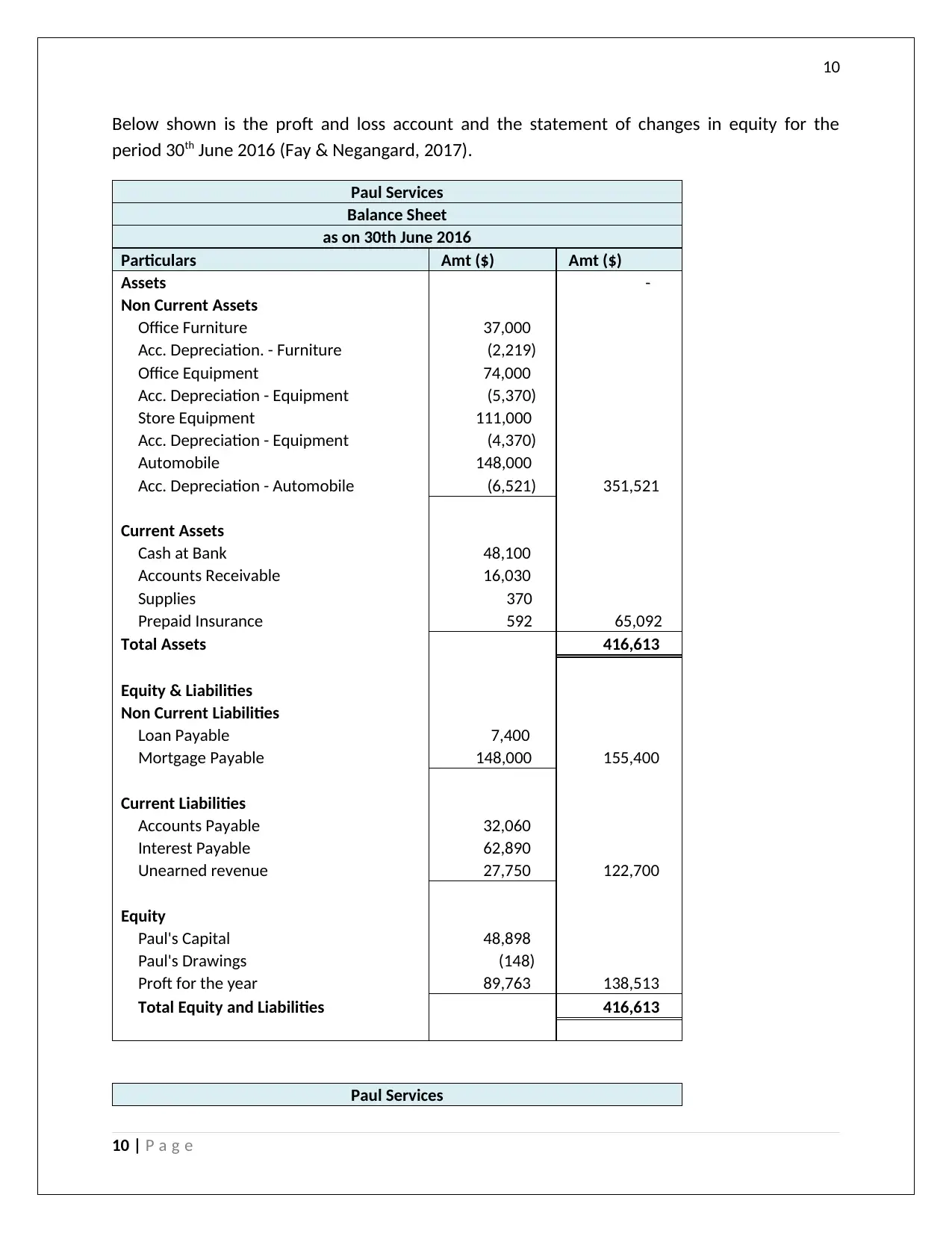

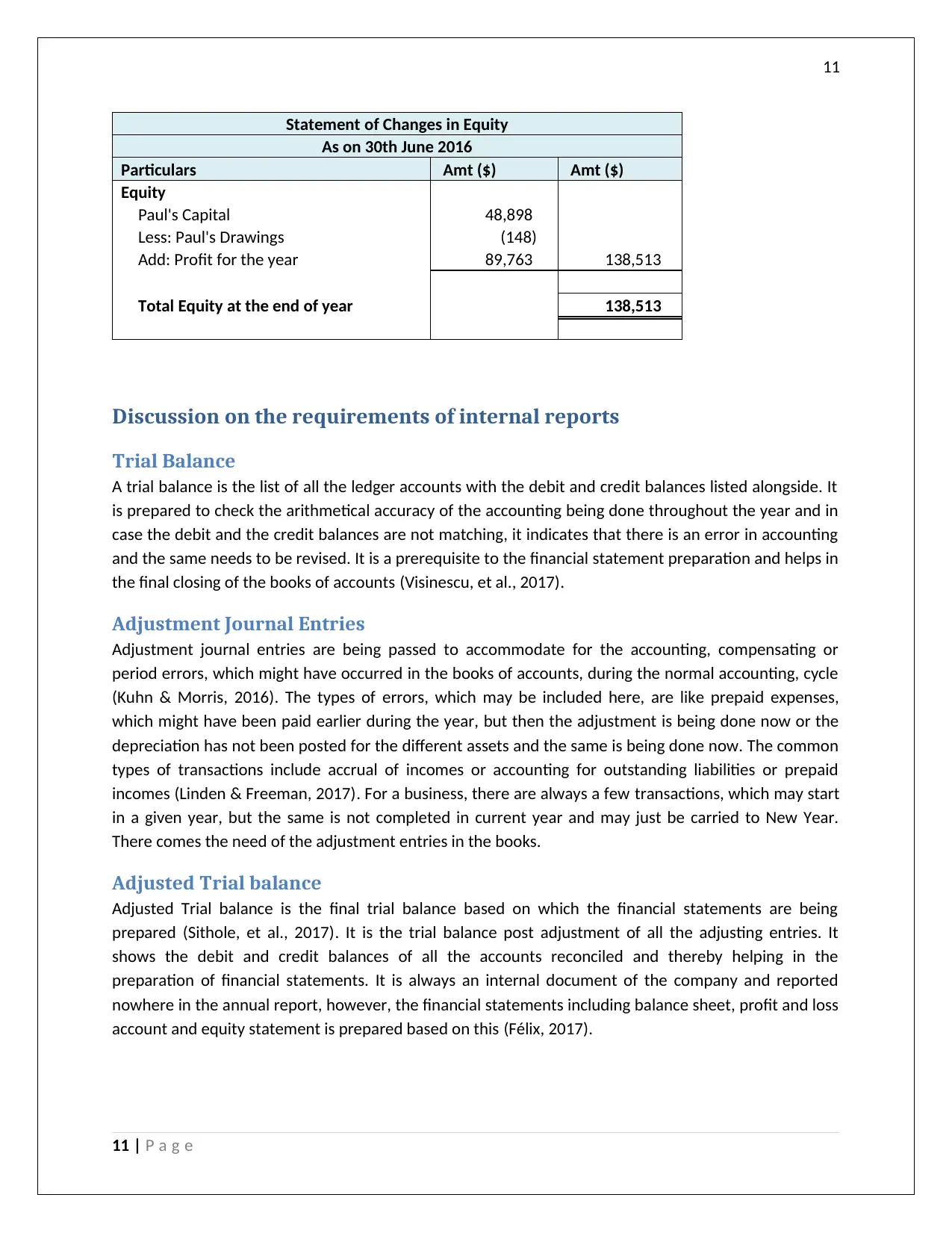

This report provides a comprehensive analysis of the financial accounting cycle for Paul Services, covering the period ending June 30, 2016. It begins with an executive summary and table of contents, followed by an introduction outlining the report's aim and scope, which is to demonstrate financial statement preparation using journal entries and trial balances. The report includes the initial unadjusted trial balance, adjustment journal entries, and the adjusted trial balance. It then presents the income statement and closing journal entries. Finally, the balance sheet and statement of changes in equity are presented. The report also includes a discussion of the purpose of internal reports such as the trial balance, adjustment journal entries, and closing journal entries. The report concludes with the key learnings from the financial report preparation.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.