BIZ201: Analyzing Crystal Hotel's Financial Position and Performance

VerifiedAdded on 2022/08/31

|14

|2532

|17

Report

AI Summary

This report provides a comprehensive financial analysis of Crystal Palace Pty Ltd, evaluating its financial standing to inform a decision on hotel renovation. The analysis employs vertical analysis of the income statement and statement of financial position, alongside an examination of profitability, efficiency, liquidity, and solvency ratios. The findings reveal weaknesses in profitability, efficiency, and liquidity, while highlighting a strong solvency position. The report also recommends additional industry-specific benchmarks such as RevPAR, ADR, and occupancy rate. The overall financial performance indicates areas for improvement, especially in revenue generation and cost management. The analysis aims to guide the management's decision-making regarding the proposed renovation plan, emphasizing the need to address identified financial weaknesses.

Running head: ACCOUNTING FOR DECISION MAKING

Accounting for Decision Making

Name of the Student

Name of the University

Author’s Note

Accounting for Decision Making

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR DECISION MAKING

Executive Summary

This report aims at analyzing the income statement and statement of financial position of Crystal

Palace Pty Ltd with the intention to assess their current financial standing before proceeding with

the decision to increase the hotel star by renovating the hotel while improving the services. The

main techniques used for this analysis purpose are vertical analysis of income statement and

statement of financial position and the analysis of four types of financial ratios which are

profitability ratios, efficiency ratios, liquidity ratios and solvency ratios. Findings of the vertical

analysis shows that Crystal Palace Pty Ltd has not been able in registering increase in revenue in

2018, but the expenses have been increased as compared to the industry standards. This

demonstrates that the financial performance of the hotel has not been as effective as per the

industry standard. On the other hand, findings of the ratio analysis point towards the weakness of

Crystal Palace Pty Ltd in profitability, efficiency and liquidity position which demonstrates the

ineffective financial position of the hotel as compared to the industry standards. The positive is

that Crystal Palace Pty Ltd has less reliance on debt capital which has strengthened its solvency

position. In case the management of Crystal Palace Pty Ltd wants to take a major decision about

the plan to renovate the hotels, the above-mentioned areas need to be considered as this may

affect the decision to implement the plan.

Executive Summary

This report aims at analyzing the income statement and statement of financial position of Crystal

Palace Pty Ltd with the intention to assess their current financial standing before proceeding with

the decision to increase the hotel star by renovating the hotel while improving the services. The

main techniques used for this analysis purpose are vertical analysis of income statement and

statement of financial position and the analysis of four types of financial ratios which are

profitability ratios, efficiency ratios, liquidity ratios and solvency ratios. Findings of the vertical

analysis shows that Crystal Palace Pty Ltd has not been able in registering increase in revenue in

2018, but the expenses have been increased as compared to the industry standards. This

demonstrates that the financial performance of the hotel has not been as effective as per the

industry standard. On the other hand, findings of the ratio analysis point towards the weakness of

Crystal Palace Pty Ltd in profitability, efficiency and liquidity position which demonstrates the

ineffective financial position of the hotel as compared to the industry standards. The positive is

that Crystal Palace Pty Ltd has less reliance on debt capital which has strengthened its solvency

position. In case the management of Crystal Palace Pty Ltd wants to take a major decision about

the plan to renovate the hotels, the above-mentioned areas need to be considered as this may

affect the decision to implement the plan.

2ACCOUNTING FOR DECISION MAKING

Table of Contents

Part 1: Excel Workbook Calculations..............................................................................................3

1. Vertical Analysis.....................................................................................................................3

Requirement (a).......................................................................................................................3

Requirement (b).......................................................................................................................4

2. Ratio Analysis..........................................................................................................................5

Part 2: Business Report....................................................................................................................6

Introduction..................................................................................................................................6

Income Statement Comparative Analysis....................................................................................6

Ratio Analysis..............................................................................................................................8

Recommendation on Three Additional Industry Specific Benchmarks......................................9

Conclusion.................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Part 1: Excel Workbook Calculations..............................................................................................3

1. Vertical Analysis.....................................................................................................................3

Requirement (a).......................................................................................................................3

Requirement (b).......................................................................................................................4

2. Ratio Analysis..........................................................................................................................5

Part 2: Business Report....................................................................................................................6

Introduction..................................................................................................................................6

Income Statement Comparative Analysis....................................................................................6

Ratio Analysis..............................................................................................................................8

Recommendation on Three Additional Industry Specific Benchmarks......................................9

Conclusion.................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR DECISION MAKING

Part 1: Excel Workbook Calculations

1. Vertical Analysis

Requirement (a)

Part 1: Excel Workbook Calculations

1. Vertical Analysis

Requirement (a)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR DECISION MAKING

Requirement (b)

Requirement (b)

5ACCOUNTING FOR DECISION MAKING

2. Ratio Analysis

2. Ratio Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR DECISION MAKING

Part 2: Business Report

Introduction

Crystal Hotel Pty Ltd (Crystal Hotel) is considering a plan to upsurge the star rating of

the hotel by modernizing it and this requires the management to assess their present financial

performance and financial standings as compared to the industry. Using the financial analysis

tools like vertical analysis, ratio analysis and others help the companies helps the managements

of the companies to assess their businesses’ current financial position and performance.

Therefore, the main aim of this report is the analysis of the current financial performance and

position of Crystal Hotel through conducting vertical analysis on its income statement and

statement of financial position along with the analysis of certain key financial ratios. This report

also suggests other performance indicators for the business of Crystal Hotel.

Income Statement Comparative Analysis

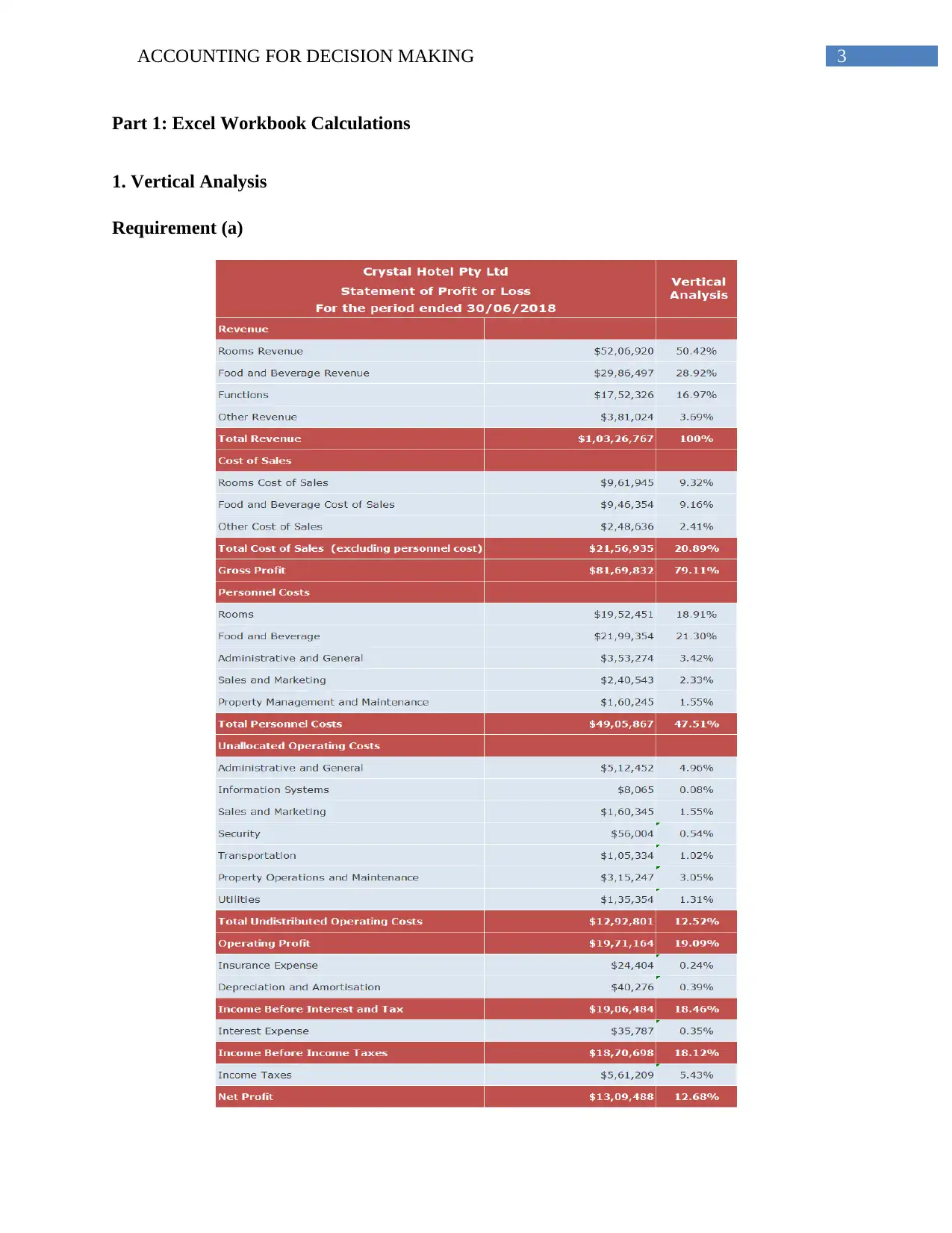

Revenue – Crystal Hotel has earned 50.42% of total revenue from rooms which is lower than the

industry standard that is 65%; but its revenue from foods and beverages that is 28.92% of the

total sales is higher than the industry average that is 27%. Since the key source of revenue of the

hotel is rooms, it has not performed well in 2018 as compared to the other hotels in the same

industry (Robinson, 2020).

Cost of Sales – The hotel’s cost of sales for rooms that is 9.32% is higher than the industry

standard; and the same can be seen in case of the cost of cost of goods sold of foods and

beverages and others. It demonstrates the inefficiency of managing costs of its services as

compared to the industry; and this has negative impact on the hotel’s profitability (Robinson et

al., 2015).

Part 2: Business Report

Introduction

Crystal Hotel Pty Ltd (Crystal Hotel) is considering a plan to upsurge the star rating of

the hotel by modernizing it and this requires the management to assess their present financial

performance and financial standings as compared to the industry. Using the financial analysis

tools like vertical analysis, ratio analysis and others help the companies helps the managements

of the companies to assess their businesses’ current financial position and performance.

Therefore, the main aim of this report is the analysis of the current financial performance and

position of Crystal Hotel through conducting vertical analysis on its income statement and

statement of financial position along with the analysis of certain key financial ratios. This report

also suggests other performance indicators for the business of Crystal Hotel.

Income Statement Comparative Analysis

Revenue – Crystal Hotel has earned 50.42% of total revenue from rooms which is lower than the

industry standard that is 65%; but its revenue from foods and beverages that is 28.92% of the

total sales is higher than the industry average that is 27%. Since the key source of revenue of the

hotel is rooms, it has not performed well in 2018 as compared to the other hotels in the same

industry (Robinson, 2020).

Cost of Sales – The hotel’s cost of sales for rooms that is 9.32% is higher than the industry

standard; and the same can be seen in case of the cost of cost of goods sold of foods and

beverages and others. It demonstrates the inefficiency of managing costs of its services as

compared to the industry; and this has negative impact on the hotel’s profitability (Robinson et

al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR DECISION MAKING

Personnel Costs –Crystal Hotel’s personnel costs for rooms, food and beverages, and sales and

marketing are higher than the industry standards which demonstrates that the hotel is providing

higher salaries, wages and compensation to their personnel and all these are higher than the

industry standard. Its personnel expenses in the areas of administration and general, and property

management and maintenance are lower than when compared it to the industry standard (Easton

&Sommers, 2018).

Unallocated Operating Costs – The unallocated operating costs of Crystal Hotel in

administrative and general and property operation and maintenance are higher as compared to

the industry standards and it indicates towards incurring higher expenses by Crystal Hotel in

these areas than the other hotels in the same sector. Expenses of the hotel in the other areas like

information system, sales and marketing, security and transportation are lower than the industry

standards (Gad, 2015).

Total Costs Proportions – The total costs of Crystal Hotel in costs of sales, total personnel costs

and total unallocated operating costs are higher than the proportions of industry standards.

Therefore, the hotel has incurred higher expenses in every aspect while has registered less

revenue as compared to the other companies in the industry. This shows ineffective business

performance of Crystal Hotel as compared to the industry as the revenue has become lower

where the expenses have become higher (Welc, 2017).

Recommendations – Some recommendations are made for Crystal Hotel based on the above

analysis:

1. It is recommended to Crystal Hotel to increase its revenue from rooms by increase the

number of rooms and renovating them as it is the main revenue source for Crystal Hotel.

Personnel Costs –Crystal Hotel’s personnel costs for rooms, food and beverages, and sales and

marketing are higher than the industry standards which demonstrates that the hotel is providing

higher salaries, wages and compensation to their personnel and all these are higher than the

industry standard. Its personnel expenses in the areas of administration and general, and property

management and maintenance are lower than when compared it to the industry standard (Easton

&Sommers, 2018).

Unallocated Operating Costs – The unallocated operating costs of Crystal Hotel in

administrative and general and property operation and maintenance are higher as compared to

the industry standards and it indicates towards incurring higher expenses by Crystal Hotel in

these areas than the other hotels in the same sector. Expenses of the hotel in the other areas like

information system, sales and marketing, security and transportation are lower than the industry

standards (Gad, 2015).

Total Costs Proportions – The total costs of Crystal Hotel in costs of sales, total personnel costs

and total unallocated operating costs are higher than the proportions of industry standards.

Therefore, the hotel has incurred higher expenses in every aspect while has registered less

revenue as compared to the other companies in the industry. This shows ineffective business

performance of Crystal Hotel as compared to the industry as the revenue has become lower

where the expenses have become higher (Welc, 2017).

Recommendations – Some recommendations are made for Crystal Hotel based on the above

analysis:

1. It is recommended to Crystal Hotel to increase its revenue from rooms by increase the

number of rooms and renovating them as it is the main revenue source for Crystal Hotel.

8ACCOUNTING FOR DECISION MAKING

2. Crystal Hotel is recommended to implement effective financial strategies for decreasing

the costs of sales as this will help the company to increase overall profitability.

3. The recommendation to Crystal Hotel is to decrease the costs like personnel costs and

unallocated operating costs as they are higher than the industry standards.

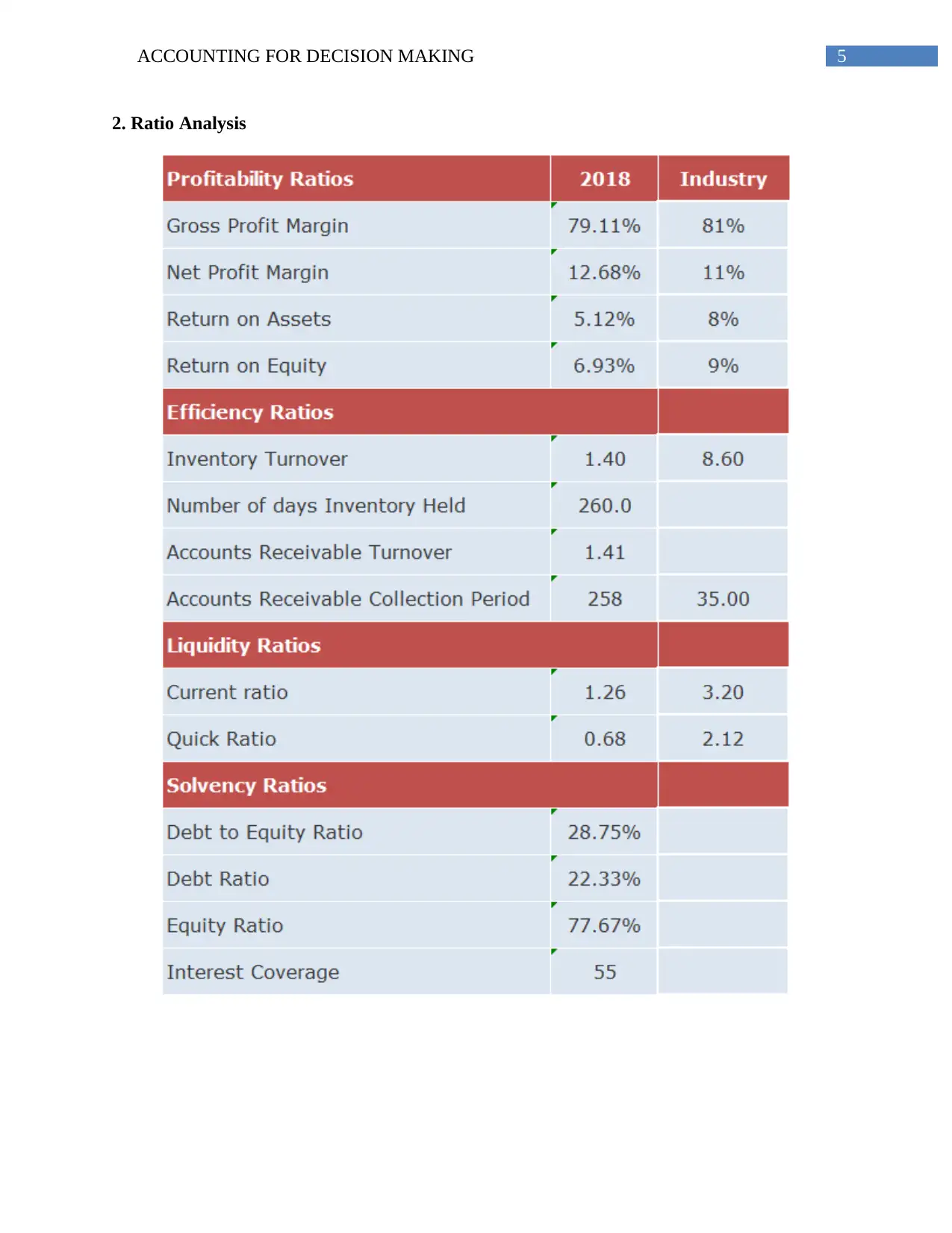

Ratio Analysis

Profitability – The gross profit ratio of Crystal Hotel is lower than the industry standard and the

prime reason for decrease in this ratio is the increase in cost of sales. Net profit margin is higher

than the industry standards which demonstrate the company’s ability to effectively manage the

expenses for making profit. Since return on assets of Crystal of the hotel is lower than the

industry standard, this demonstrates the inefficiency of the hotels in using its assets for

generating profit as compared to other companies in the same industry. Crystal Hotel has also not

been able in generating adequate profit from the investment of equity shareholders as this ratio is

less than the industry standard (Satryo, Rokhmania&Diptyana, 2017). The recommendation to

the hotel is to reduce its cost of sales while ensuring effective utilization of its assets and equity

investments.

Efficiency – Inventory turnover ratio of Crystal Hotel is significantly lesser than the industry

standard which demonstrates issues like unnecessary accumulation of stock, inefficient use of

investments and over-investments in inventories. This increase the number of days in inventory.

Moreover, the collection period of accounts receivable is significantly higher than the industry

standards and this indicates towards the issues like high collection period allowed to customers

and ineffective credit policy within the hotel. These aspects indicate towards the high financial

inefficiencies in Crystal Hotel (Havidz&Setiawan, 2015). The recommendations to Crystal Hotel

are to increase inventory turnover and decrease the collection period for accounts receivable.

2. Crystal Hotel is recommended to implement effective financial strategies for decreasing

the costs of sales as this will help the company to increase overall profitability.

3. The recommendation to Crystal Hotel is to decrease the costs like personnel costs and

unallocated operating costs as they are higher than the industry standards.

Ratio Analysis

Profitability – The gross profit ratio of Crystal Hotel is lower than the industry standard and the

prime reason for decrease in this ratio is the increase in cost of sales. Net profit margin is higher

than the industry standards which demonstrate the company’s ability to effectively manage the

expenses for making profit. Since return on assets of Crystal of the hotel is lower than the

industry standard, this demonstrates the inefficiency of the hotels in using its assets for

generating profit as compared to other companies in the same industry. Crystal Hotel has also not

been able in generating adequate profit from the investment of equity shareholders as this ratio is

less than the industry standard (Satryo, Rokhmania&Diptyana, 2017). The recommendation to

the hotel is to reduce its cost of sales while ensuring effective utilization of its assets and equity

investments.

Efficiency – Inventory turnover ratio of Crystal Hotel is significantly lesser than the industry

standard which demonstrates issues like unnecessary accumulation of stock, inefficient use of

investments and over-investments in inventories. This increase the number of days in inventory.

Moreover, the collection period of accounts receivable is significantly higher than the industry

standards and this indicates towards the issues like high collection period allowed to customers

and ineffective credit policy within the hotel. These aspects indicate towards the high financial

inefficiencies in Crystal Hotel (Havidz&Setiawan, 2015). The recommendations to Crystal Hotel

are to increase inventory turnover and decrease the collection period for accounts receivable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR DECISION MAKING

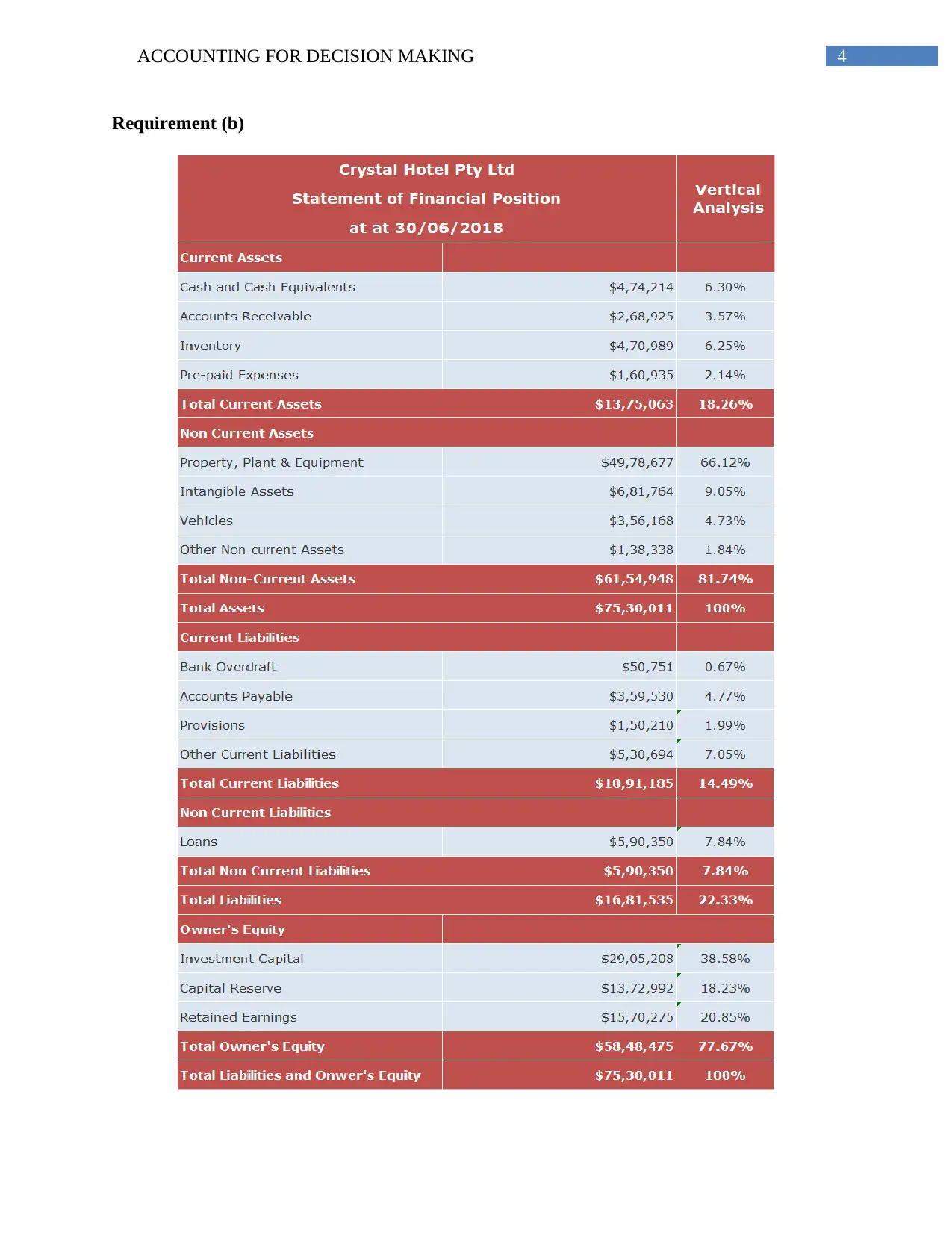

Liquidity –Both the liquidity ratios that are the current ratio and quick ratio of Crystal Hotel are

lesser than the industry standard which indicates towards major liquidity issues within the hotel.

Significantly lower current ratio than industry demonstrates the presence of key working capital

issues within the hotel. Moreover, the quick ratio is also lower than the industry standard where

it is also less than 1:1; this means the hotel does not have sufficient quick assets for paying off its

current business obligations (Hiran, 2016). Therefore, the recommendation to Crystal Hotel is to

improve its overall liquidity position by increasing the amount of current and quick assets in the

business.

Solvency –The debt to equity ratio of Crystal Hotel is lower than 50% and it means the hotel has

less reliance on the funds of the creditors as it raises majority portion of the capital from

shareholders. The same reflects from the debt ratio of the hotel as low debt ratio shows minimum

overall dependency on the debts. Moreover, Crystal Hotel has high equity ratio shows that the

hotel is worth investing as the business is more sustainable as well as less risky for future loans.

Lastly,Crystal Hotel has an interest coverage ratio of 55 times which makes the hotel able in

paying interests for 55 times in a year from its operating profit. Overall, Crystal Hotel has a good

solvency position (Laskina, 2017).

Recommendation on Three Additional Industry Specific Benchmarks

The presence of many additional industry specific performance indicators can be seen in

the hotel industry that Crystal Hotel can use for their comparative analysis. Three of these

benchmarks are discus reresed below:

Liquidity –Both the liquidity ratios that are the current ratio and quick ratio of Crystal Hotel are

lesser than the industry standard which indicates towards major liquidity issues within the hotel.

Significantly lower current ratio than industry demonstrates the presence of key working capital

issues within the hotel. Moreover, the quick ratio is also lower than the industry standard where

it is also less than 1:1; this means the hotel does not have sufficient quick assets for paying off its

current business obligations (Hiran, 2016). Therefore, the recommendation to Crystal Hotel is to

improve its overall liquidity position by increasing the amount of current and quick assets in the

business.

Solvency –The debt to equity ratio of Crystal Hotel is lower than 50% and it means the hotel has

less reliance on the funds of the creditors as it raises majority portion of the capital from

shareholders. The same reflects from the debt ratio of the hotel as low debt ratio shows minimum

overall dependency on the debts. Moreover, Crystal Hotel has high equity ratio shows that the

hotel is worth investing as the business is more sustainable as well as less risky for future loans.

Lastly,Crystal Hotel has an interest coverage ratio of 55 times which makes the hotel able in

paying interests for 55 times in a year from its operating profit. Overall, Crystal Hotel has a good

solvency position (Laskina, 2017).

Recommendation on Three Additional Industry Specific Benchmarks

The presence of many additional industry specific performance indicators can be seen in

the hotel industry that Crystal Hotel can use for their comparative analysis. Three of these

benchmarks are discus reresed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR DECISION MAKING

1. RevPAR – Revenue per available room, commonly known as RevPAR, is a key industry-

specific benchmark that is used in the hotel industry for comparing performance with other

hotels. The formula for calculating RevPAR is shown below:

RevPAR = (The combined total of all revenue ÷ Total available rooms during the period)

The main utilization of this benchmark can be seen in the hotel in order to assess its ability of

filling its available rooms at an average rate (Nieto-Garcia et al., 2019).

2. ADR – Average Daily Rate or ADR is considered as one of the most popular industry specific

benchmarks for hotels for measuring as well as comparing the performance of the hotels. The

formula for calculating ADR is as below”

ADR = (Room revenue ÷ Rooms sold)

ADR helps the hotels in ascertaining the average rate of the rooms sold over a particular period

of time. This duration can be considered as a quarter, a month or a year. Utilization of ADR

provides the hotels with an indication of the overall generated income from every paid and

occupied room for that particular duration (Oses, Gerrikagoitia & Alzua, 2016).

3. Occupancy Rate – Occupancy rate is a key industry specific benchmark that can be used by

the hotels for assessing their performance and comparing the same with other hotels. The

formula for calculating occupancy rate is as below:

Occupancy Rate = (Number of occupied rooms ÷ Total number of available rooms)

This is considered as a major key performance indicator in the hotel industry that assists in

highlighting how much of the available space in a hotel is actually being utilized (Ginindza &

Tichaawa, 2019).

1. RevPAR – Revenue per available room, commonly known as RevPAR, is a key industry-

specific benchmark that is used in the hotel industry for comparing performance with other

hotels. The formula for calculating RevPAR is shown below:

RevPAR = (The combined total of all revenue ÷ Total available rooms during the period)

The main utilization of this benchmark can be seen in the hotel in order to assess its ability of

filling its available rooms at an average rate (Nieto-Garcia et al., 2019).

2. ADR – Average Daily Rate or ADR is considered as one of the most popular industry specific

benchmarks for hotels for measuring as well as comparing the performance of the hotels. The

formula for calculating ADR is as below”

ADR = (Room revenue ÷ Rooms sold)

ADR helps the hotels in ascertaining the average rate of the rooms sold over a particular period

of time. This duration can be considered as a quarter, a month or a year. Utilization of ADR

provides the hotels with an indication of the overall generated income from every paid and

occupied room for that particular duration (Oses, Gerrikagoitia & Alzua, 2016).

3. Occupancy Rate – Occupancy rate is a key industry specific benchmark that can be used by

the hotels for assessing their performance and comparing the same with other hotels. The

formula for calculating occupancy rate is as below:

Occupancy Rate = (Number of occupied rooms ÷ Total number of available rooms)

This is considered as a major key performance indicator in the hotel industry that assists in

highlighting how much of the available space in a hotel is actually being utilized (Ginindza &

Tichaawa, 2019).

11ACCOUNTING FOR DECISION MAKING

Conclusion

The main aim of this report is to assess the financial performance and financial position

of Crystal Hotel. The outcome of the vertical analysis shows that Crystal Hotel does not have

effective financial performance in 2018 as its revenue decreased in that year where the overall

expenses increased. The outcome of the profitability ratio analysis shows that Crystal Hotel does

not have higher profitability ratios as compared to the industry standard except the net profit.

Crystal Hotel does not have efficiency in managing its inventory and receivable as these ratios

are less than the industry standard. The same negative aspect can be seen in case of liquidity

position as Crystal Hotel does not have adequate current and quick assets for paying off its short-

term business obligations. However, Crystal Hotel has an effective solvency position due to the

less dependency of Crystal Hotel on creditors’ funds which makes the company less risky.

Conclusion

The main aim of this report is to assess the financial performance and financial position

of Crystal Hotel. The outcome of the vertical analysis shows that Crystal Hotel does not have

effective financial performance in 2018 as its revenue decreased in that year where the overall

expenses increased. The outcome of the profitability ratio analysis shows that Crystal Hotel does

not have higher profitability ratios as compared to the industry standard except the net profit.

Crystal Hotel does not have efficiency in managing its inventory and receivable as these ratios

are less than the industry standard. The same negative aspect can be seen in case of liquidity

position as Crystal Hotel does not have adequate current and quick assets for paying off its short-

term business obligations. However, Crystal Hotel has an effective solvency position due to the

less dependency of Crystal Hotel on creditors’ funds which makes the company less risky.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.