Managerial Accounting: Cost Concepts and Decision Making Analysis

VerifiedAdded on 2023/04/04

|14

|3261

|387

Report

AI Summary

This report analyzes managerial accounting principles through case studies, focusing on cost concepts, decision-making, and strategic management. Part A examines cost types (fixed, variable, semi-variable) in a childcare business, evaluating options for appliance purchases and employee hiring, and analyzing the feasibility of renting space. Part B explores managerial accounting components (strategy, planning, and controlling) within Canon Inc. and Apple Inc., analyzing their innovation processes. The report demonstrates the application of cost analysis, financial calculations, and strategic recommendations to real-world business scenarios. The assignment provides detailed calculations and recommendations, including the evaluation of different laundering options, the impact of hiring additional employees, and the comparison of different accommodation scenarios for the childcare business. The analysis incorporates financial statements, net profit margins, and strategic insights to support decision-making.

Running head: MANAGERIAL ACCOUNTING

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement 1:...........................................................................................................2

Answer to requirement 2:...........................................................................................................2

Answer to requirement 3:...........................................................................................................2

Answer to requirement 4:...........................................................................................................2

Answer to requirement 5:...........................................................................................................2

Part B:.........................................................................................................................................2

Answer to requirement 1:...........................................................................................................2

Answer to requirement 2:...........................................................................................................3

Answer to requirement 3:...........................................................................................................3

References and Bibliography list:..............................................................................................3

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement 1:...........................................................................................................2

Answer to requirement 2:...........................................................................................................2

Answer to requirement 3:...........................................................................................................2

Answer to requirement 4:...........................................................................................................2

Answer to requirement 5:...........................................................................................................2

Part B:.........................................................................................................................................2

Answer to requirement 1:...........................................................................................................2

Answer to requirement 2:...........................................................................................................3

Answer to requirement 3:...........................................................................................................3

References and Bibliography list:..............................................................................................3

MANAGERIAL ACCOUNTING

Part A:

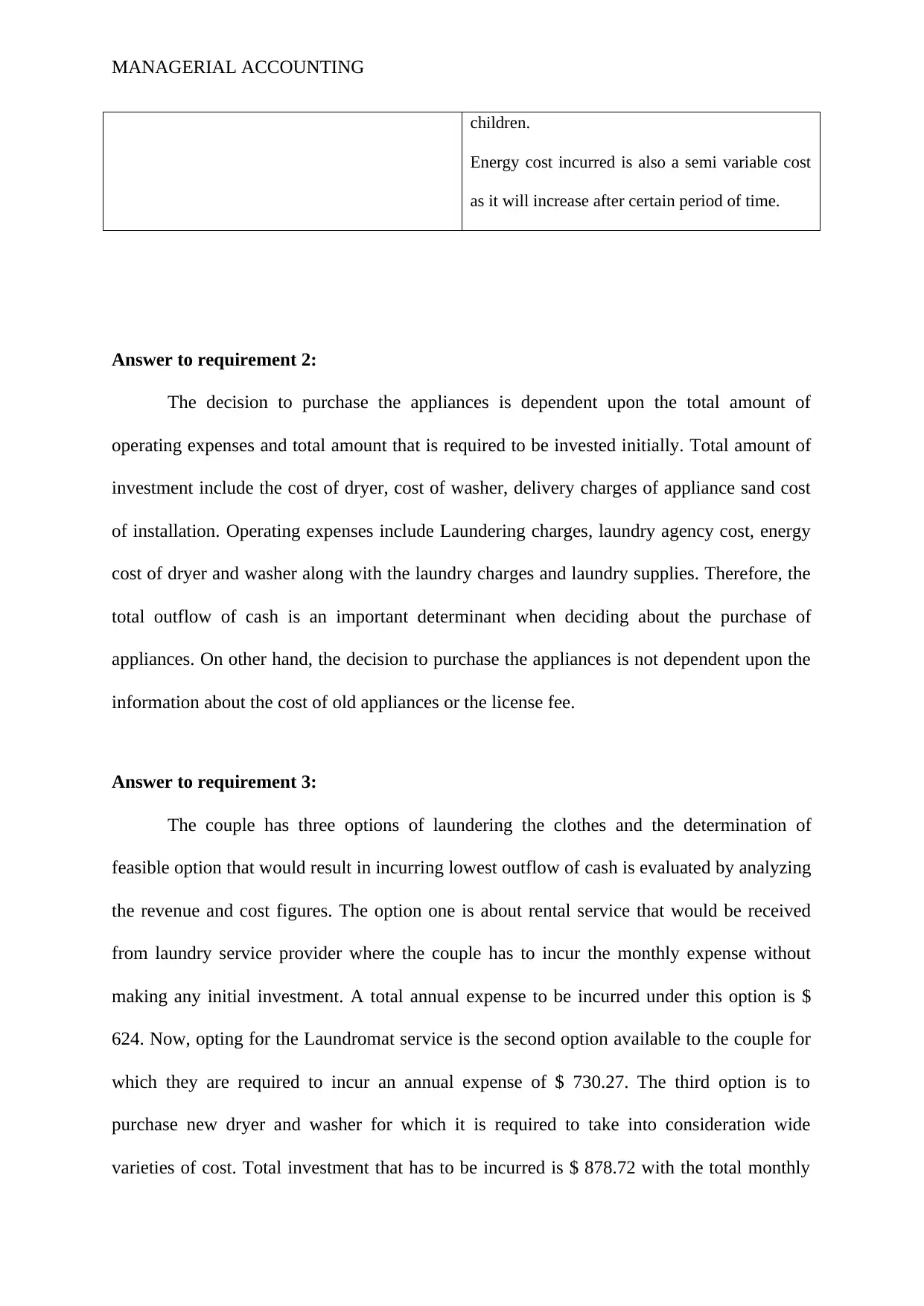

Answer to requirement 1:

There are three types of cost that is discussed in the case study of running the business

of child care. These costs consist of variable costs, semi variable cost and fixed cost. Types of

costs discussed in the case study are listed below:

Different types of costs Example from the case study

Fixed cost

Fixed costs are the costs that are incurred by the

business in a fixed amount and such costs are

independent of the level of output produced or

service provided (Elmassri et al. 2016). For

running the business, it is required to incur this

fixed cost.

The annual fee paid to the state by the couple to

maintain the license for running the business is a

fixed cost. Total amount of fixed cost paid for

annual fee is $ 225. In addition to this, the cost

incurred for insurance on annual basis is also the

fixed cost with an amount of $ 3480.

Variable cost

Variable costs are the cost that is incurred by the

business for the service provided or the output

produced (Albrecht et al. 2017). Such costs

vary with the change in the total number of

services provided or in the given case , it would

vary with the change in the number of children

for which the care is being taken

The utility cost for running the business is a

variable cost.

The cost of snack and meal per day is also

variable and such costs would increase with

increase in the number of children served.

Total salary paid to employees can also be

considered as variable cost.

Semi variable cost

Semi variable cost is the costs that remains fixed

for certain time and it starts increasing thereafter.

License fee in some respect can be considered as

semi variable cost because a fixed amount is

incurred when total of six children is provided

care and increases with the increase in number of

Part A:

Answer to requirement 1:

There are three types of cost that is discussed in the case study of running the business

of child care. These costs consist of variable costs, semi variable cost and fixed cost. Types of

costs discussed in the case study are listed below:

Different types of costs Example from the case study

Fixed cost

Fixed costs are the costs that are incurred by the

business in a fixed amount and such costs are

independent of the level of output produced or

service provided (Elmassri et al. 2016). For

running the business, it is required to incur this

fixed cost.

The annual fee paid to the state by the couple to

maintain the license for running the business is a

fixed cost. Total amount of fixed cost paid for

annual fee is $ 225. In addition to this, the cost

incurred for insurance on annual basis is also the

fixed cost with an amount of $ 3480.

Variable cost

Variable costs are the cost that is incurred by the

business for the service provided or the output

produced (Albrecht et al. 2017). Such costs

vary with the change in the total number of

services provided or in the given case , it would

vary with the change in the number of children

for which the care is being taken

The utility cost for running the business is a

variable cost.

The cost of snack and meal per day is also

variable and such costs would increase with

increase in the number of children served.

Total salary paid to employees can also be

considered as variable cost.

Semi variable cost

Semi variable cost is the costs that remains fixed

for certain time and it starts increasing thereafter.

License fee in some respect can be considered as

semi variable cost because a fixed amount is

incurred when total of six children is provided

care and increases with the increase in number of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

children.

Energy cost incurred is also a semi variable cost

as it will increase after certain period of time.

Answer to requirement 2:

The decision to purchase the appliances is dependent upon the total amount of

operating expenses and total amount that is required to be invested initially. Total amount of

investment include the cost of dryer, cost of washer, delivery charges of appliance sand cost

of installation. Operating expenses include Laundering charges, laundry agency cost, energy

cost of dryer and washer along with the laundry charges and laundry supplies. Therefore, the

total outflow of cash is an important determinant when deciding about the purchase of

appliances. On other hand, the decision to purchase the appliances is not dependent upon the

information about the cost of old appliances or the license fee.

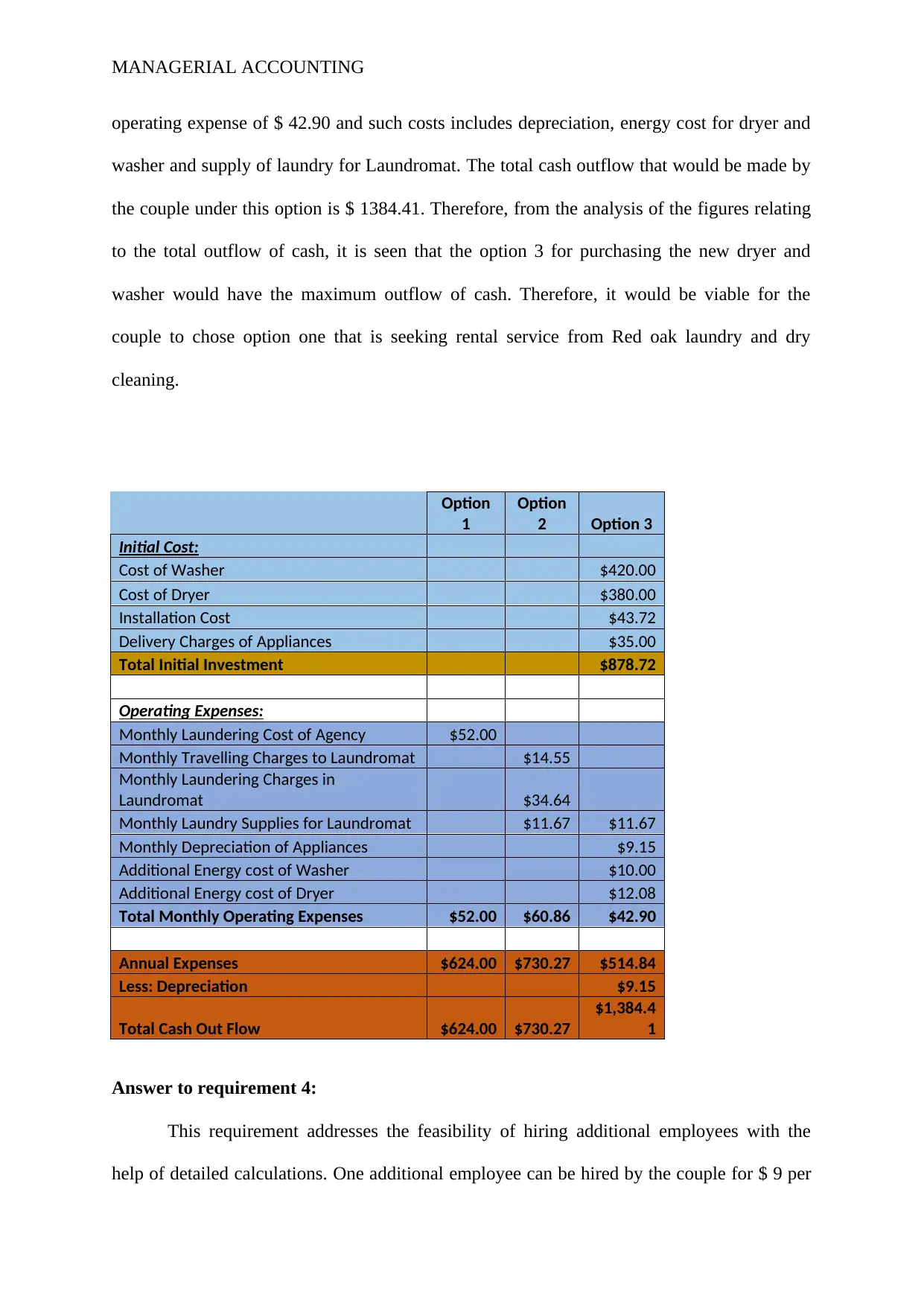

Answer to requirement 3:

The couple has three options of laundering the clothes and the determination of

feasible option that would result in incurring lowest outflow of cash is evaluated by analyzing

the revenue and cost figures. The option one is about rental service that would be received

from laundry service provider where the couple has to incur the monthly expense without

making any initial investment. A total annual expense to be incurred under this option is $

624. Now, opting for the Laundromat service is the second option available to the couple for

which they are required to incur an annual expense of $ 730.27. The third option is to

purchase new dryer and washer for which it is required to take into consideration wide

varieties of cost. Total investment that has to be incurred is $ 878.72 with the total monthly

children.

Energy cost incurred is also a semi variable cost

as it will increase after certain period of time.

Answer to requirement 2:

The decision to purchase the appliances is dependent upon the total amount of

operating expenses and total amount that is required to be invested initially. Total amount of

investment include the cost of dryer, cost of washer, delivery charges of appliance sand cost

of installation. Operating expenses include Laundering charges, laundry agency cost, energy

cost of dryer and washer along with the laundry charges and laundry supplies. Therefore, the

total outflow of cash is an important determinant when deciding about the purchase of

appliances. On other hand, the decision to purchase the appliances is not dependent upon the

information about the cost of old appliances or the license fee.

Answer to requirement 3:

The couple has three options of laundering the clothes and the determination of

feasible option that would result in incurring lowest outflow of cash is evaluated by analyzing

the revenue and cost figures. The option one is about rental service that would be received

from laundry service provider where the couple has to incur the monthly expense without

making any initial investment. A total annual expense to be incurred under this option is $

624. Now, opting for the Laundromat service is the second option available to the couple for

which they are required to incur an annual expense of $ 730.27. The third option is to

purchase new dryer and washer for which it is required to take into consideration wide

varieties of cost. Total investment that has to be incurred is $ 878.72 with the total monthly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

operating expense of $ 42.90 and such costs includes depreciation, energy cost for dryer and

washer and supply of laundry for Laundromat. The total cash outflow that would be made by

the couple under this option is $ 1384.41. Therefore, from the analysis of the figures relating

to the total outflow of cash, it is seen that the option 3 for purchasing the new dryer and

washer would have the maximum outflow of cash. Therefore, it would be viable for the

couple to chose option one that is seeking rental service from Red oak laundry and dry

cleaning.

Option

1

Option

2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Less: Depreciation $9.15

Total Cash Out Flow $624.00 $730.27

$1,384.4

1

Answer to requirement 4:

This requirement addresses the feasibility of hiring additional employees with the

help of detailed calculations. One additional employee can be hired by the couple for $ 9 per

operating expense of $ 42.90 and such costs includes depreciation, energy cost for dryer and

washer and supply of laundry for Laundromat. The total cash outflow that would be made by

the couple under this option is $ 1384.41. Therefore, from the analysis of the figures relating

to the total outflow of cash, it is seen that the option 3 for purchasing the new dryer and

washer would have the maximum outflow of cash. Therefore, it would be viable for the

couple to chose option one that is seeking rental service from Red oak laundry and dry

cleaning.

Option

1

Option

2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Less: Depreciation $9.15

Total Cash Out Flow $624.00 $730.27

$1,384.4

1

Answer to requirement 4:

This requirement addresses the feasibility of hiring additional employees with the

help of detailed calculations. One additional employee can be hired by the couple for $ 9 per

MANAGERIAL ACCOUNTING

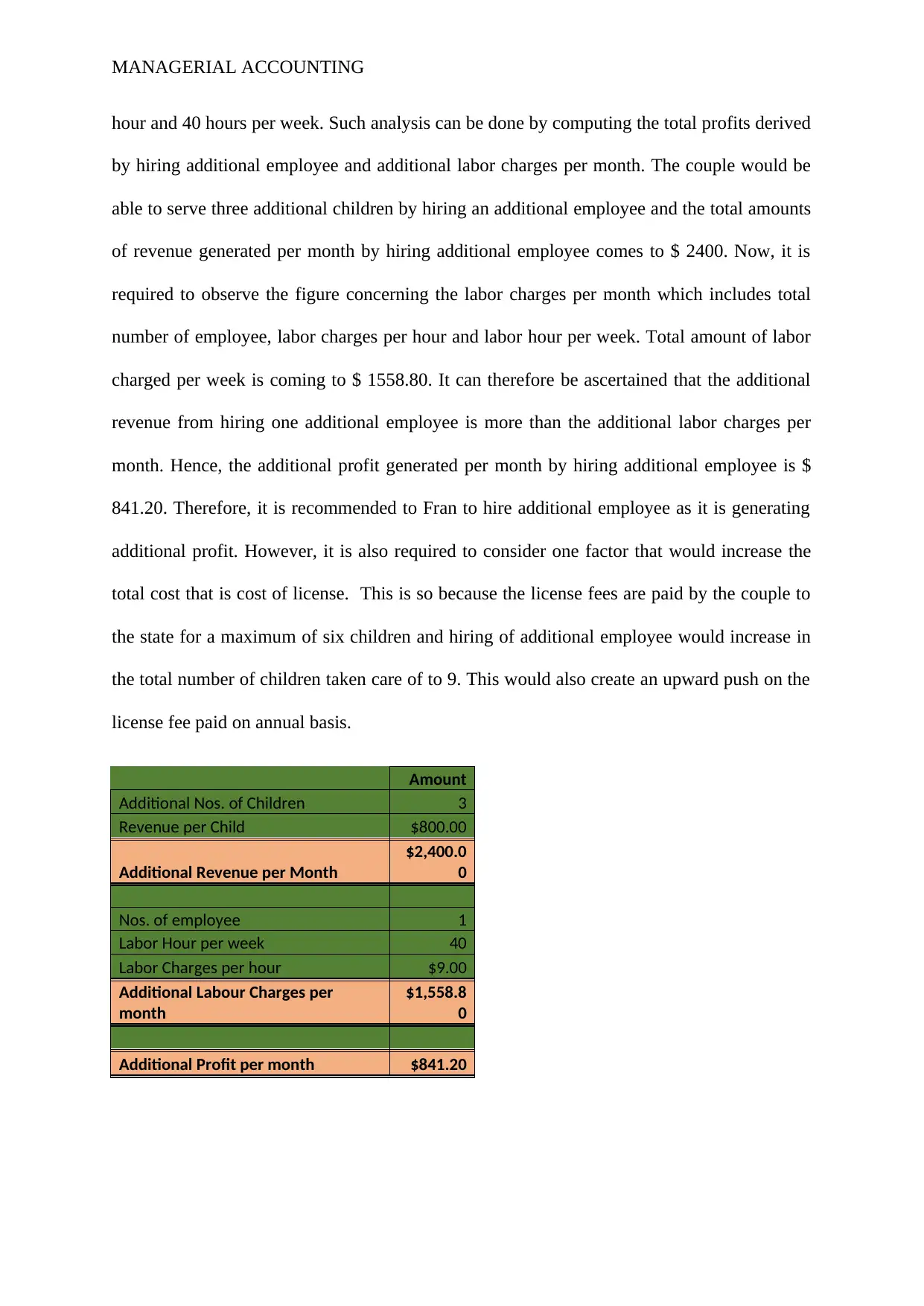

hour and 40 hours per week. Such analysis can be done by computing the total profits derived

by hiring additional employee and additional labor charges per month. The couple would be

able to serve three additional children by hiring an additional employee and the total amounts

of revenue generated per month by hiring additional employee comes to $ 2400. Now, it is

required to observe the figure concerning the labor charges per month which includes total

number of employee, labor charges per hour and labor hour per week. Total amount of labor

charged per week is coming to $ 1558.80. It can therefore be ascertained that the additional

revenue from hiring one additional employee is more than the additional labor charges per

month. Hence, the additional profit generated per month by hiring additional employee is $

841.20. Therefore, it is recommended to Fran to hire additional employee as it is generating

additional profit. However, it is also required to consider one factor that would increase the

total cost that is cost of license. This is so because the license fees are paid by the couple to

the state for a maximum of six children and hiring of additional employee would increase in

the total number of children taken care of to 9. This would also create an upward push on the

license fee paid on annual basis.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labour Charges per

month

$1,558.8

0

Additional Profit per month $841.20

hour and 40 hours per week. Such analysis can be done by computing the total profits derived

by hiring additional employee and additional labor charges per month. The couple would be

able to serve three additional children by hiring an additional employee and the total amounts

of revenue generated per month by hiring additional employee comes to $ 2400. Now, it is

required to observe the figure concerning the labor charges per month which includes total

number of employee, labor charges per hour and labor hour per week. Total amount of labor

charged per week is coming to $ 1558.80. It can therefore be ascertained that the additional

revenue from hiring one additional employee is more than the additional labor charges per

month. Hence, the additional profit generated per month by hiring additional employee is $

841.20. Therefore, it is recommended to Fran to hire additional employee as it is generating

additional profit. However, it is also required to consider one factor that would increase the

total cost that is cost of license. This is so because the license fees are paid by the couple to

the state for a maximum of six children and hiring of additional employee would increase in

the total number of children taken care of to 9. This would also create an upward push on the

license fee paid on annual basis.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labour Charges per

month

$1,558.8

0

Additional Profit per month $841.20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

Answer to requirement 5:

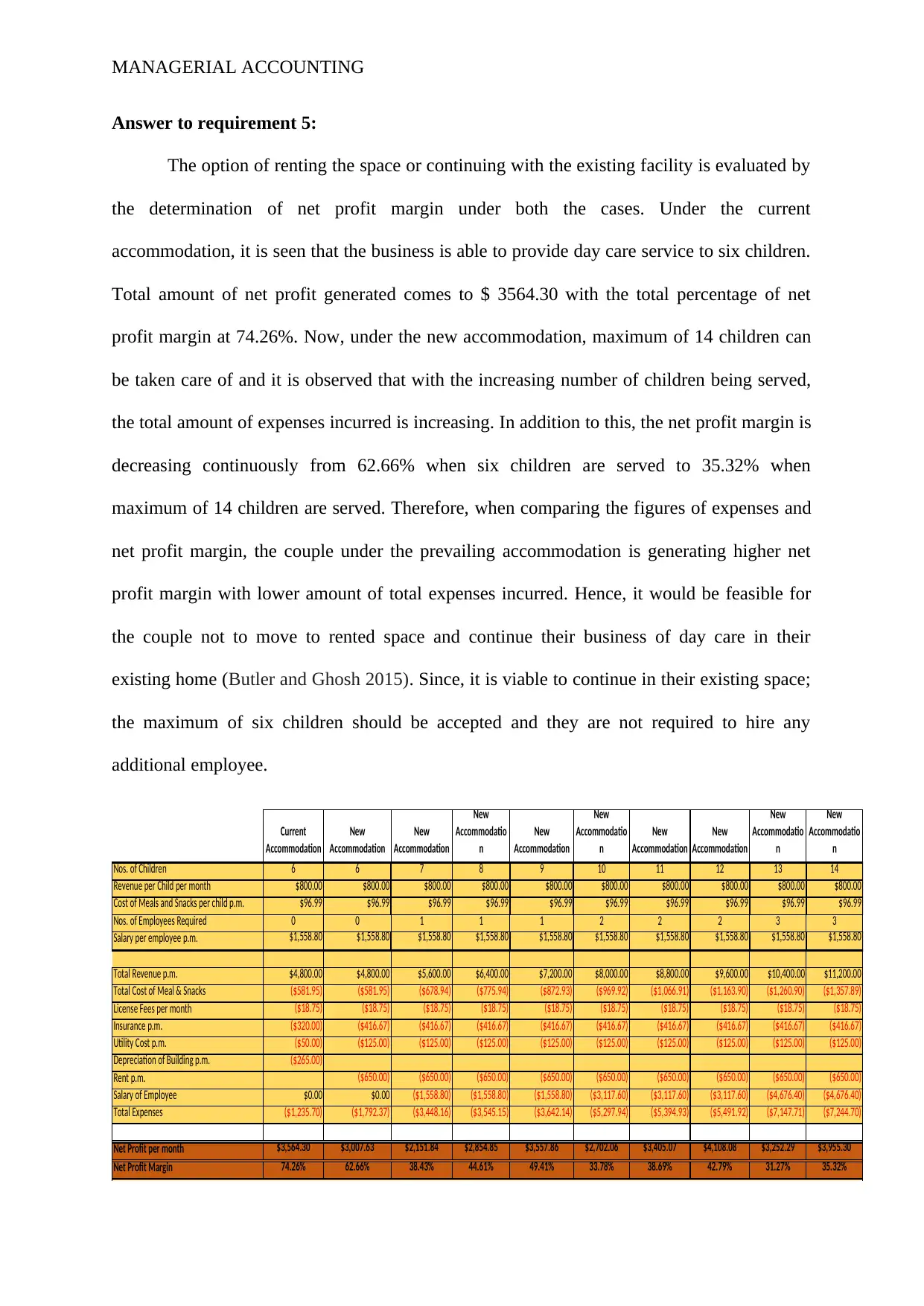

The option of renting the space or continuing with the existing facility is evaluated by

the determination of net profit margin under both the cases. Under the current

accommodation, it is seen that the business is able to provide day care service to six children.

Total amount of net profit generated comes to $ 3564.30 with the total percentage of net

profit margin at 74.26%. Now, under the new accommodation, maximum of 14 children can

be taken care of and it is observed that with the increasing number of children being served,

the total amount of expenses incurred is increasing. In addition to this, the net profit margin is

decreasing continuously from 62.66% when six children are served to 35.32% when

maximum of 14 children are served. Therefore, when comparing the figures of expenses and

net profit margin, the couple under the prevailing accommodation is generating higher net

profit margin with lower amount of total expenses incurred. Hence, it would be feasible for

the couple not to move to rented space and continue their business of day care in their

existing home (Butler and Ghosh 2015). Since, it is viable to continue in their existing space;

the maximum of six children should be accepted and they are not required to hire any

additional employee.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

Answer to requirement 5:

The option of renting the space or continuing with the existing facility is evaluated by

the determination of net profit margin under both the cases. Under the current

accommodation, it is seen that the business is able to provide day care service to six children.

Total amount of net profit generated comes to $ 3564.30 with the total percentage of net

profit margin at 74.26%. Now, under the new accommodation, maximum of 14 children can

be taken care of and it is observed that with the increasing number of children being served,

the total amount of expenses incurred is increasing. In addition to this, the net profit margin is

decreasing continuously from 62.66% when six children are served to 35.32% when

maximum of 14 children are served. Therefore, when comparing the figures of expenses and

net profit margin, the couple under the prevailing accommodation is generating higher net

profit margin with lower amount of total expenses incurred. Hence, it would be feasible for

the couple not to move to rented space and continue their business of day care in their

existing home (Butler and Ghosh 2015). Since, it is viable to continue in their existing space;

the maximum of six children should be accepted and they are not required to hire any

additional employee.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Part B:

Answer to requirement 1:

The firms usually take into accounts strategy, planning and controlling in their

decision making process and these three components forms the part of managerial

accounting. Controlling is the process that helps in evaluation of the object and influencing

the outcome relating to cost and process management whether they are within or outside the

acceptable range. Planning is the components that occur at all the level and it intends to

maximize the profits for the action that is taken. Strategy development helps in creating a

relationship between strategic endeavors and day to day activities (Brewer et al. 2015).

This section demonstrate an understanding of the innovation process of the two

organizations that is canon Inc and Apple Inc by referring to then given case study. From the

analysis of the case study, it was ascertained that the entire paper copier market of Cannon

Inc was reconceptualized. The negative relationship between the reliability and cost for mini

copier was managed by the actualization of mini copier. It was required by the management

to make an improvement in the drum and cleaner durability. Therefore, it intended to develop

the mini copier that would be maintenance free which was done by treating the drum as

module that after making several numbers would be redundant (Nasseri et al. 2016). The

capability of Canon was enhanced due to development of such module.

Assessment of the cost group and quality in the planning stage can be regarded as

another component of management accounting. The process of planning was developed by

setting the standard of quality in terms of fusing, charging and cleaning. Cartridge was the net

technological development which became continuous and spread throughout. The task force

system helped in the planning development and product completion (Apostolou et al. 2015).

Part B:

Answer to requirement 1:

The firms usually take into accounts strategy, planning and controlling in their

decision making process and these three components forms the part of managerial

accounting. Controlling is the process that helps in evaluation of the object and influencing

the outcome relating to cost and process management whether they are within or outside the

acceptable range. Planning is the components that occur at all the level and it intends to

maximize the profits for the action that is taken. Strategy development helps in creating a

relationship between strategic endeavors and day to day activities (Brewer et al. 2015).

This section demonstrate an understanding of the innovation process of the two

organizations that is canon Inc and Apple Inc by referring to then given case study. From the

analysis of the case study, it was ascertained that the entire paper copier market of Cannon

Inc was reconceptualized. The negative relationship between the reliability and cost for mini

copier was managed by the actualization of mini copier. It was required by the management

to make an improvement in the drum and cleaner durability. Therefore, it intended to develop

the mini copier that would be maintenance free which was done by treating the drum as

module that after making several numbers would be redundant (Nasseri et al. 2016). The

capability of Canon was enhanced due to development of such module.

Assessment of the cost group and quality in the planning stage can be regarded as

another component of management accounting. The process of planning was developed by

setting the standard of quality in terms of fusing, charging and cleaning. Cartridge was the net

technological development which became continuous and spread throughout. The task force

system helped in the planning development and product completion (Apostolou et al. 2015).

MANAGERIAL ACCOUNTING

Hence, the enhancement of organization’s capability resulted in bringing benefits and

knowledge based expansion.

The components of managerial accounting were also incorporated in the product

development process at Apple Inc. Apple intended to revolutionized the Mac computers

because of its higher price and its revolutionization was done by incorporating the Xerox parc

technology. The interaction between the software and hardware people was optimized with

an intention to make Mac self organizing (Shields 2015). However, due to lacking technology

and lacking coordination between the Apple member and Mac failed to reverberate some of

the innovations all the way through the company.

Producing the Mac in an inexpensive manner by Apple Inc was the controlling factor

that was to be done by setting low target price in a highly automated factory. Because of

complications in the product development process, the CEO of Apple was to perform critical

role and this helped in enhancing the process of decision making with the organization.

Development of Macintosh resulted from the innovation in the product and the innovations

were made in the base dimension of the product that made the computer with the help of

distinct deign and more compact. Hence, some of the important contributors in the

development process of the product were controlling and decision making.

Answer to requirement 2:

This section of the assignment demonstrates an understanding iof how the

management accounting contributes to the process of innovation. Management accounting

are described a a set of procedures that assist in decision making, planning and monitoring by

providing valuable insights. The control system and tool of management accounting

contributes to the success of process of innovation within an organization. Innovation has

become a way forward with the help of management accounting as it contributes to the

Hence, the enhancement of organization’s capability resulted in bringing benefits and

knowledge based expansion.

The components of managerial accounting were also incorporated in the product

development process at Apple Inc. Apple intended to revolutionized the Mac computers

because of its higher price and its revolutionization was done by incorporating the Xerox parc

technology. The interaction between the software and hardware people was optimized with

an intention to make Mac self organizing (Shields 2015). However, due to lacking technology

and lacking coordination between the Apple member and Mac failed to reverberate some of

the innovations all the way through the company.

Producing the Mac in an inexpensive manner by Apple Inc was the controlling factor

that was to be done by setting low target price in a highly automated factory. Because of

complications in the product development process, the CEO of Apple was to perform critical

role and this helped in enhancing the process of decision making with the organization.

Development of Macintosh resulted from the innovation in the product and the innovations

were made in the base dimension of the product that made the computer with the help of

distinct deign and more compact. Hence, some of the important contributors in the

development process of the product were controlling and decision making.

Answer to requirement 2:

This section of the assignment demonstrates an understanding iof how the

management accounting contributes to the process of innovation. Management accounting

are described a a set of procedures that assist in decision making, planning and monitoring by

providing valuable insights. The control system and tool of management accounting

contributes to the success of process of innovation within an organization. Innovation has

become a way forward with the help of management accounting as it contributes to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

uniqueness of the product, technological competences and competitive pressures (Baldenius

et al. 2015).

From the given case study of Apple and Canon Inc, it has been found that it is the

social interaction created by the team that helps in processing information with the help of

innovation. Development of mini copier by canon Inc and Macintosh by Apple Inc resulted

from the innovation that helped in enhancing the capability of the organizations.

The entire plain paper copier recapitalization was the innovation process at Canon

Inc. The entire project team was gathered outside the workplace that generated new solutions

by brainstorming the contradiction of Copper. Making the mini copier fundamentally

maintenance free was the innovation that arose due to evolvement of innovation resulted

from meeting up of people in a team. Development of photo receptor, toner fuser and

disposable apparatus set within the target cost was another innovation.

For the Apple Inc, development of Macintosh computers due to the incorporation of

new features and ideas due to constant interaction between the team members can be

regarded as one kind of innovation. Innovation accounted for the telephone transformative

role by rethinking on the personal computers features and basing their dimension in the form

of telephone book.

Answer to requirement 3:

In this section, the findings generated from the case study are demonstrated along

with its importance to the management accountants of Australian companies. It was found

that the innovation at both the organizations was quite different. At the Apple Inc, venture

capital creation and constant flow of entrepreneurs are the factors determining the innovation

success and growth. On other hand, for the Japanese firm where the market is considered to

be highly competitive, the constant flow of innovation helps in ensuring growth (Nonala and

uniqueness of the product, technological competences and competitive pressures (Baldenius

et al. 2015).

From the given case study of Apple and Canon Inc, it has been found that it is the

social interaction created by the team that helps in processing information with the help of

innovation. Development of mini copier by canon Inc and Macintosh by Apple Inc resulted

from the innovation that helped in enhancing the capability of the organizations.

The entire plain paper copier recapitalization was the innovation process at Canon

Inc. The entire project team was gathered outside the workplace that generated new solutions

by brainstorming the contradiction of Copper. Making the mini copier fundamentally

maintenance free was the innovation that arose due to evolvement of innovation resulted

from meeting up of people in a team. Development of photo receptor, toner fuser and

disposable apparatus set within the target cost was another innovation.

For the Apple Inc, development of Macintosh computers due to the incorporation of

new features and ideas due to constant interaction between the team members can be

regarded as one kind of innovation. Innovation accounted for the telephone transformative

role by rethinking on the personal computers features and basing their dimension in the form

of telephone book.

Answer to requirement 3:

In this section, the findings generated from the case study are demonstrated along

with its importance to the management accountants of Australian companies. It was found

that the innovation at both the organizations was quite different. At the Apple Inc, venture

capital creation and constant flow of entrepreneurs are the factors determining the innovation

success and growth. On other hand, for the Japanese firm where the market is considered to

be highly competitive, the constant flow of innovation helps in ensuring growth (Nonala and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Kenney 1991). Therefore, the firms are required to create an environment of transmitting new

ideas in an economy that is rapidly changing.

It has been found that new information emerged due to creation of chaos by the

creation of such environment with the help of an involved and careful management. The

innovation process provided the raw material for the theoretical project and the process of

innovation was reconceptualized with the help of such raw material because the deduction or

induction did not form the base of human based activity. Therefore, emergence or synthesis

forms the basis of such emphasis. Moreover, it was also analyzed by evaluating the case of

Canon Inc that the spin offs resulted in revitalization of the new product lines that helped in

the creation of mini copier. The company propelled forward because of the powerful stimulus

due to the transformative capability of the company (Nonala and Kenney 1991).

Management accountants now a day are expected to play the role of information

provider and decision makers resulting from the innovation development process and

growing complexities. Management accounts should be able to generate and create new ideas

that help in transmitting of such information thought the firm. Functioning of the accounts are

made effective by the chaos introduction in the research and development division. In order

to avoid the integrative capabilities of the company, accountants should not be overwhelmed

with the chaos (Phillips 2019).

Management accountants should be aware of the facts that is derived from the case

study that the communication of syntactic information created which the particular channel

creates is not consistent with the semantic information. The boundaries between different

departments of the corporation should be well understood. The role of leader should be well

understood by them and creation of information that acts as the catalyst should b attempted to

be maximized. It is also to be accounted by the management accountants that the use of

Kenney 1991). Therefore, the firms are required to create an environment of transmitting new

ideas in an economy that is rapidly changing.

It has been found that new information emerged due to creation of chaos by the

creation of such environment with the help of an involved and careful management. The

innovation process provided the raw material for the theoretical project and the process of

innovation was reconceptualized with the help of such raw material because the deduction or

induction did not form the base of human based activity. Therefore, emergence or synthesis

forms the basis of such emphasis. Moreover, it was also analyzed by evaluating the case of

Canon Inc that the spin offs resulted in revitalization of the new product lines that helped in

the creation of mini copier. The company propelled forward because of the powerful stimulus

due to the transformative capability of the company (Nonala and Kenney 1991).

Management accountants now a day are expected to play the role of information

provider and decision makers resulting from the innovation development process and

growing complexities. Management accounts should be able to generate and create new ideas

that help in transmitting of such information thought the firm. Functioning of the accounts are

made effective by the chaos introduction in the research and development division. In order

to avoid the integrative capabilities of the company, accountants should not be overwhelmed

with the chaos (Phillips 2019).

Management accountants should be aware of the facts that is derived from the case

study that the communication of syntactic information created which the particular channel

creates is not consistent with the semantic information. The boundaries between different

departments of the corporation should be well understood. The role of leader should be well

understood by them and creation of information that acts as the catalyst should b attempted to

be maximized. It is also to be accounted by the management accountants that the use of

MANAGERIAL ACCOUNTING

analogies and metaphor helps in the creation of understanding and conceptualization (Nonala

and Kenney 1991). Therefore, analysis of the case study generates an useful insights into the

works of management accountants for Australian companies.

analogies and metaphor helps in the creation of understanding and conceptualization (Nonala

and Kenney 1991). Therefore, analysis of the case study generates an useful insights into the

works of management accountants for Australian companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.