Accounting for Decision-Making Report: Hotel, Ethics, and Breakeven

VerifiedAdded on 2020/04/21

|7

|1252

|77

Report

AI Summary

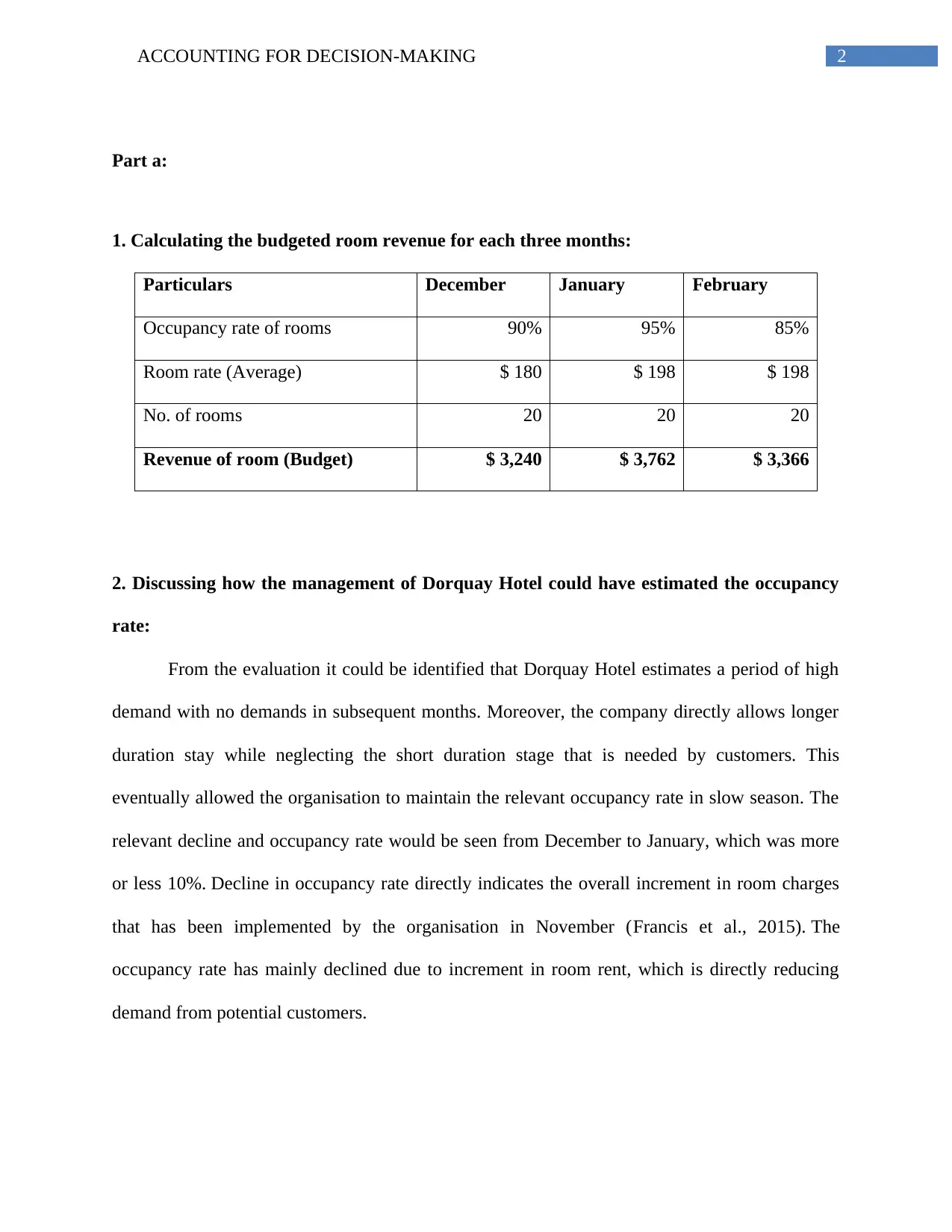

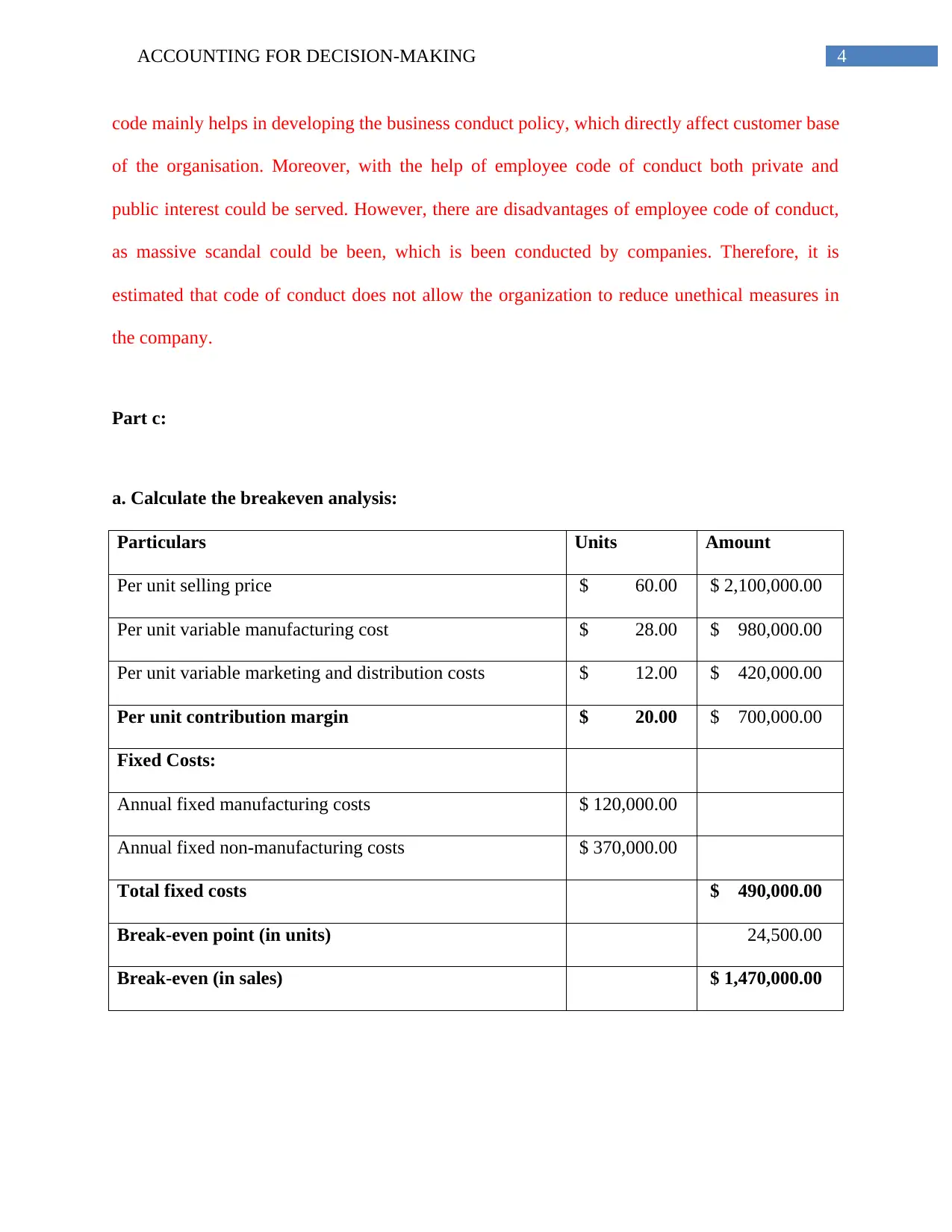

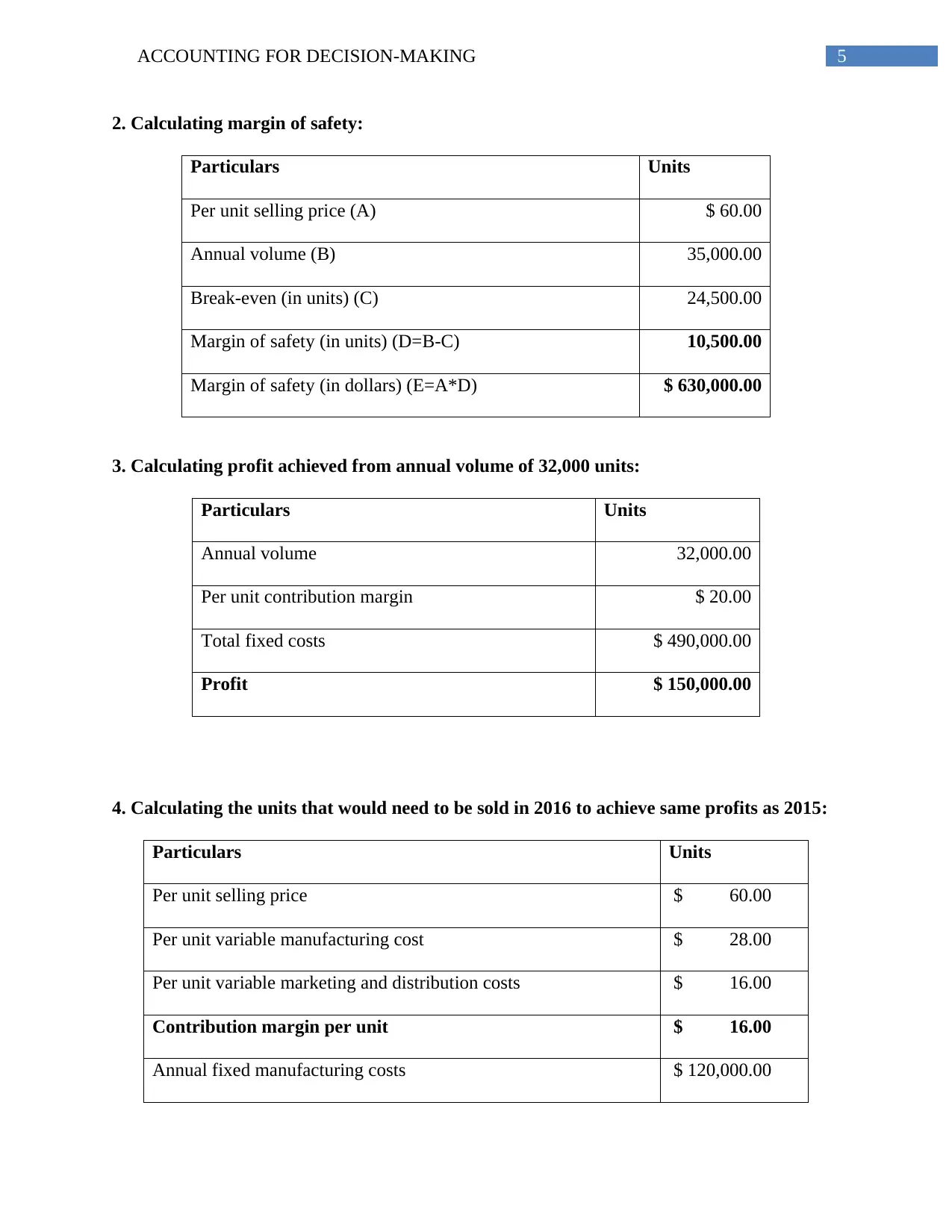

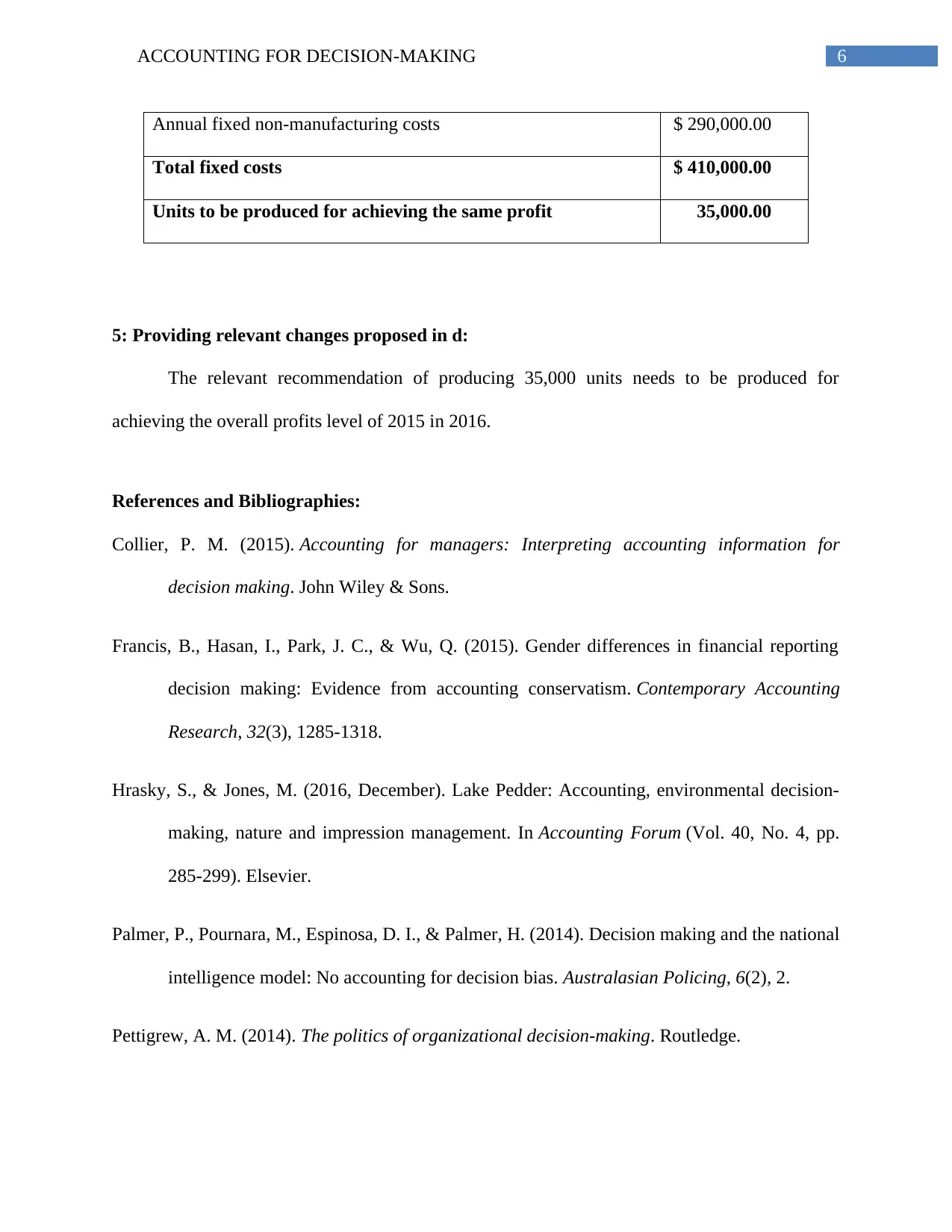

This report, titled "Accounting for Decision-Making," presents a comprehensive analysis of financial concepts and their application in real-world scenarios. Part A focuses on calculating budgeted room revenue for the Dorquay Hotel over three months, examining occupancy rates and room rates. Part B delves into ethical considerations, specifically whether a Mr. Smith should accept a family trip sponsorship and the significance of an employee code of conduct for Practical Solution Ltd. Part C performs a breakeven analysis for a company, calculating the breakeven point, margin of safety, and profit achieved at different sales volumes. Furthermore, the report calculates the units needed to achieve the same profit in a subsequent year, considering changes in costs. The report concludes with references to relevant literature supporting the analysis. The report showcases the practical application of accounting principles in decision-making processes.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.