Accounting for Decision Making: Financial Statement Analysis Report

VerifiedAdded on 2021/06/17

|14

|3224

|148

Report

AI Summary

This report delves into the core principles of accounting for decision-making, emphasizing the evaluation of a company's financial performance through both financial statement analysis and ratio analysis. The report contrasts accounting profits with cash flow, highlighting the preference for cash flow in evaluating a company's true financial position due to its reliability and resistance to manipulation. It examines the roles of internal and external users of financial statements, detailing their specific needs and how they utilize financial information. Furthermore, the report critically assesses the limitations of financial statements, such as their reliance on historical costs and potential for manipulation. Finally, the report includes an analysis of Briscoe Group Limited, evaluating its financial health through key ratios like current ratio, quick ratio, and profitability ratios, along with an examination of its share price performance and recent announcements to aid in an investment decision between purchasing Briscoe Group Limited shares or investing in a term deposit.

RUNNING HEAD: ACCOUNTING

Accounting for decision making

Accounting for decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 2

Question 1

In general, the evaluation of a company involves two aspects, first deals with presentation of

financial statements and second deal with analysis of the same. Normally, while measuring

the performance of an enterprise, two factors on which the analysis is based are net profit and

cash flow. These are the two aspects which clearly reflects financial position of the company

and presents a true and fair view of it (Charifzadeh, & Taschner, 2017).

Accounting profits is the excess amount of total income over total expenses. It is the value

which is derived by deducting all the expenditures from the total revenue earned. (Knight,

2012). On the other hand, cash flow is the inside and outside movement of cash within the

business. The inflow and outflow of cash is represented by cash flow statement and is

recorded on cash basis (Periasamy, 2009). The main difference between the two is the way in

which they are recorded in the books of accounts. Profit is recorded on accrual basis and cash

flow is reported on cash basis.

However, at time of evaluating users generally prefer or rely on cash flow rather than or

profits. Reason being,

Since the profits are recorded and reported on accrual basis, they do not provide a

true representation of actual profits and may prove to be wrong in near future. The

transactions in income statement are reported as per accrual accounting and there is a

possibility of them getting deferred or change in future (Boex, 2015).

The calculation of profit include non-cash items such as depreciation and

amortization while the same are not included in cash flow statement. It is true that the

asset of the company reduces its value over the time and that’s why it is necessary to

record the amount of depreciation. But in actual, such amount is not been paid by the

company and thus it does not affect the profits (Fernandez, 2006).

Question 1

In general, the evaluation of a company involves two aspects, first deals with presentation of

financial statements and second deal with analysis of the same. Normally, while measuring

the performance of an enterprise, two factors on which the analysis is based are net profit and

cash flow. These are the two aspects which clearly reflects financial position of the company

and presents a true and fair view of it (Charifzadeh, & Taschner, 2017).

Accounting profits is the excess amount of total income over total expenses. It is the value

which is derived by deducting all the expenditures from the total revenue earned. (Knight,

2012). On the other hand, cash flow is the inside and outside movement of cash within the

business. The inflow and outflow of cash is represented by cash flow statement and is

recorded on cash basis (Periasamy, 2009). The main difference between the two is the way in

which they are recorded in the books of accounts. Profit is recorded on accrual basis and cash

flow is reported on cash basis.

However, at time of evaluating users generally prefer or rely on cash flow rather than or

profits. Reason being,

Since the profits are recorded and reported on accrual basis, they do not provide a

true representation of actual profits and may prove to be wrong in near future. The

transactions in income statement are reported as per accrual accounting and there is a

possibility of them getting deferred or change in future (Boex, 2015).

The calculation of profit include non-cash items such as depreciation and

amortization while the same are not included in cash flow statement. It is true that the

asset of the company reduces its value over the time and that’s why it is necessary to

record the amount of depreciation. But in actual, such amount is not been paid by the

company and thus it does not affect the profits (Fernandez, 2006).

Accounting 3

Another reason is that the management of an organization can easily manipulate the

accounting profits as compare to cash flow. The figure of the profit can be easily

exaggerated by the mangers by reporting a transaction on accrual basis (CPA. 2018).

The cash flow is a performance measure from the shareholders’ perspective while the

profit only evaluates the outcome of the company’s operations (Fernandez, 2006).

From the above reasons, it can be said that user should rely more on cash flow rather than

accounting profits at time of evaluating or measuring a company’s performance. Also the

cash flows are generally easy to forecast as compare to profits and they reflect the true

liquidity position. Critical evaluation of cash flow helps in knowing about the future trends

that will prevail in the business and also reflects the cash position of the company.

Accounting profits are not reliable and can be modified, thus not reflecting a true position of

the entity. Therefore, it is important to take into account, the cash flow of the company while

evaluating or determining its position and situation within the industry (Berk & DeMarzo,

2010).

Question 2

The financial statements mentioned in the annual report of a company are used by many

people for their own purposes. As these statements clearly represent the financial view of an

organizations, users evaluate them as per their needs and requirements. However, there are

many users of financial statements classified as internal and external. Both the type of users

are as follows:

Internal users

Management: The Company’s managers uses the information for understanding the

profitability, liquidity and efficiency of the business and analyse them to take

Another reason is that the management of an organization can easily manipulate the

accounting profits as compare to cash flow. The figure of the profit can be easily

exaggerated by the mangers by reporting a transaction on accrual basis (CPA. 2018).

The cash flow is a performance measure from the shareholders’ perspective while the

profit only evaluates the outcome of the company’s operations (Fernandez, 2006).

From the above reasons, it can be said that user should rely more on cash flow rather than

accounting profits at time of evaluating or measuring a company’s performance. Also the

cash flows are generally easy to forecast as compare to profits and they reflect the true

liquidity position. Critical evaluation of cash flow helps in knowing about the future trends

that will prevail in the business and also reflects the cash position of the company.

Accounting profits are not reliable and can be modified, thus not reflecting a true position of

the entity. Therefore, it is important to take into account, the cash flow of the company while

evaluating or determining its position and situation within the industry (Berk & DeMarzo,

2010).

Question 2

The financial statements mentioned in the annual report of a company are used by many

people for their own purposes. As these statements clearly represent the financial view of an

organizations, users evaluate them as per their needs and requirements. However, there are

many users of financial statements classified as internal and external. Both the type of users

are as follows:

Internal users

Management: The Company’s managers uses the information for understanding the

profitability, liquidity and efficiency of the business and analyse them to take

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 4

important decisions related to its operations and management (Dick & Missonier-

Piera, 2011).

Employees: They are those people who form an organization and work for it in return

of a compensation. They look up to the statements to know about the profits of the

company so that they can demand for bonus and salary increment.

Owners: They are the people who owned the organization or entity. For analysing and

measuring the viability and profitability of their investment they look up to the

financial statements and the key ratios of the firm (Alexander, Britton & Jorissen,

2007).

External users

Creditors and suppliers: They evaluate the final accounts of a company to know about

its creditworthiness and its ability to pay them back on time.

Investors: For knowing about the feasibility of their investment in a firm, they analyse

the final accounts of that firm. By critically reviewing the statements, they came to

know about the percentage of return offered by the organization and can decide to

continue with the investment or not.

Government: To ensure that the entity complies with all the regulatory requirements

and pay the tax liability on time, the government official require to check its financial

records.

Competitors: Entities generally functions in a competitive environment where a cut

throat competition prevails. In order to evaluate the financial conditions, competing

companies access each other financial data and gain knowledge regarding the same

(Palepu & Healy, 2007).

important decisions related to its operations and management (Dick & Missonier-

Piera, 2011).

Employees: They are those people who form an organization and work for it in return

of a compensation. They look up to the statements to know about the profits of the

company so that they can demand for bonus and salary increment.

Owners: They are the people who owned the organization or entity. For analysing and

measuring the viability and profitability of their investment they look up to the

financial statements and the key ratios of the firm (Alexander, Britton & Jorissen,

2007).

External users

Creditors and suppliers: They evaluate the final accounts of a company to know about

its creditworthiness and its ability to pay them back on time.

Investors: For knowing about the feasibility of their investment in a firm, they analyse

the final accounts of that firm. By critically reviewing the statements, they came to

know about the percentage of return offered by the organization and can decide to

continue with the investment or not.

Government: To ensure that the entity complies with all the regulatory requirements

and pay the tax liability on time, the government official require to check its financial

records.

Competitors: Entities generally functions in a competitive environment where a cut

throat competition prevails. In order to evaluate the financial conditions, competing

companies access each other financial data and gain knowledge regarding the same

(Palepu & Healy, 2007).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 5

However, the financial statements prepared are according to the Generally Accepted

Accounting Principles and only provides limited information. Thus there are some limitation

of them to its users. Following are the limitations of financial statements:

They are been prepared on historical cost concept. Initially, transactions are recorded

on their historical cost (Sinha, 2012). This can create a problem for the government

officials while calculating the tax liability and any other legal charges for the firm.

In GAAP format, treatment of derivatives and securitization is done according to

some specified rules. This implies that they not modified as per the changes taking

place in the market. This give a faulty view of financial position of the business.

The GAAP prepared financial statements record assets at their historical cost and not

on their fair value. This created a problem for the investors to judge the value of

company’s tangible assets.

GAAP requires the company to report all their expenses on accrual basis that is it

should be reported as and when they occur, irrespective of the fact that they are

actually paid or not (Rajasekaran, 2011). Such increased expenses can be a limitation

to the employees of the firm as it may impact their chances of getting bonus or

increment.

It is not always possible to compare the financial statements of different companies

because of the different accounting concepts and policies used by them.

The accounts prepared according to GAAP can be manipulated deliberately by the

managers, as they are rule based which can easily be modified. It is a huge drawback

to the investors and creditors as they can take wrong decisions regarding investment

and lending credit on the basis of manipulated figures.

So, above are the limitations of financial statements that are exposed to both the types of

users.

However, the financial statements prepared are according to the Generally Accepted

Accounting Principles and only provides limited information. Thus there are some limitation

of them to its users. Following are the limitations of financial statements:

They are been prepared on historical cost concept. Initially, transactions are recorded

on their historical cost (Sinha, 2012). This can create a problem for the government

officials while calculating the tax liability and any other legal charges for the firm.

In GAAP format, treatment of derivatives and securitization is done according to

some specified rules. This implies that they not modified as per the changes taking

place in the market. This give a faulty view of financial position of the business.

The GAAP prepared financial statements record assets at their historical cost and not

on their fair value. This created a problem for the investors to judge the value of

company’s tangible assets.

GAAP requires the company to report all their expenses on accrual basis that is it

should be reported as and when they occur, irrespective of the fact that they are

actually paid or not (Rajasekaran, 2011). Such increased expenses can be a limitation

to the employees of the firm as it may impact their chances of getting bonus or

increment.

It is not always possible to compare the financial statements of different companies

because of the different accounting concepts and policies used by them.

The accounts prepared according to GAAP can be manipulated deliberately by the

managers, as they are rule based which can easily be modified. It is a huge drawback

to the investors and creditors as they can take wrong decisions regarding investment

and lending credit on the basis of manipulated figures.

So, above are the limitations of financial statements that are exposed to both the types of

users.

Accounting 6

Question 3

In order to decide between the purchase of Briscoe Group Limited and investment in term

deposit worth $50000, following analysis is been done for Briscoe Limited:

Ratio analysis

Performance of share price

Recent announcements

Ratio Analysis of the company

The key ratios calculated are as follows:

1. Current ratio

It is one of the liquidity ratio that reflects the capability of a company to pay off its current

liabilities with its current assets. It shows the financial health of the business.

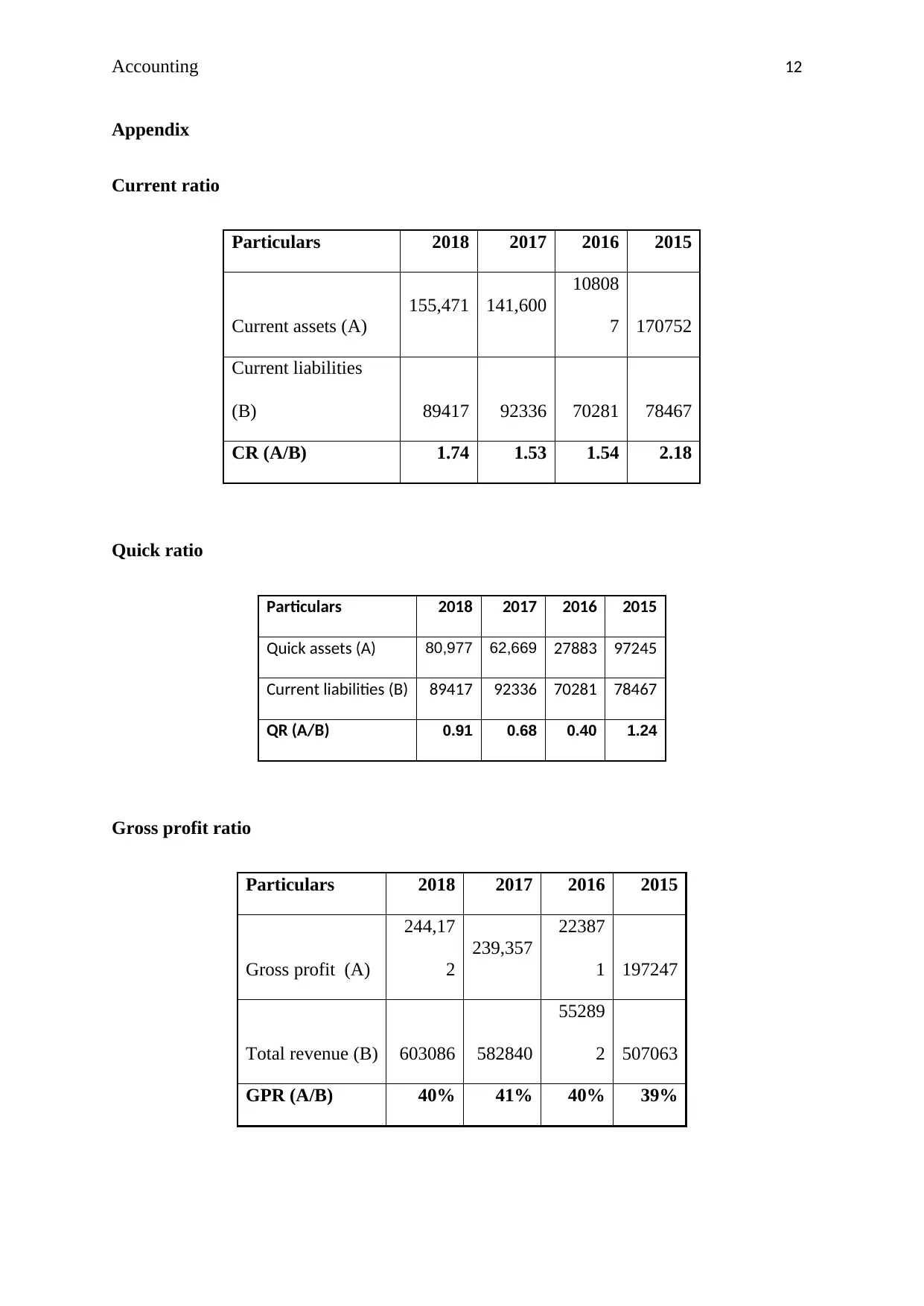

Referring to the Appendix, the current ratio reflects the financial position of a company and is

calculated by dividing the current assets with current liabilities. The CR of Briscoe group has

been continuously increasing after facing a fall in 2016. In 2015, the CR of the company was

2.18 and the same reduces to 1.54 in 2016. After that, it falls further to 1.53 and currently, its

CR is 1.74. This implies that company has improved its performance as a result of which, its

liabilities has reduced in 2018. This boosted up the ratio make Briscoe capable enough to

meet its short term obligations (Tracy, 2012).

2. Quick ratio

It is another financial metric which reflects the same as current ratio does. The only

difference is that it takes into account the value of quick assets which comprises of the most

liquid assets that excludes inventory.

Question 3

In order to decide between the purchase of Briscoe Group Limited and investment in term

deposit worth $50000, following analysis is been done for Briscoe Limited:

Ratio analysis

Performance of share price

Recent announcements

Ratio Analysis of the company

The key ratios calculated are as follows:

1. Current ratio

It is one of the liquidity ratio that reflects the capability of a company to pay off its current

liabilities with its current assets. It shows the financial health of the business.

Referring to the Appendix, the current ratio reflects the financial position of a company and is

calculated by dividing the current assets with current liabilities. The CR of Briscoe group has

been continuously increasing after facing a fall in 2016. In 2015, the CR of the company was

2.18 and the same reduces to 1.54 in 2016. After that, it falls further to 1.53 and currently, its

CR is 1.74. This implies that company has improved its performance as a result of which, its

liabilities has reduced in 2018. This boosted up the ratio make Briscoe capable enough to

meet its short term obligations (Tracy, 2012).

2. Quick ratio

It is another financial metric which reflects the same as current ratio does. The only

difference is that it takes into account the value of quick assets which comprises of the most

liquid assets that excludes inventory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 7

From the calculation done in Appendix, it can be said that Briscoe has the highest quick ratio

in 2015 with 1.24. Post the year, the ratio falls to 0.40 in 2016. Reason was the sudden

decrease in the current assets of the company. However, from 2016 a constant increase was

there in Briscoe’s QR and in 2018 it is reported at 0.91. This implies that company has

improved its current assets by managing them properly for meeting its quick and short term

liabilities.

3. Gross profit ratio

This ratio determoines the amount of profit earned by the firm after paying for its COGS,

expressed as a percentage of total sales (Jenter & Lewellen, 2015). The GPR of Briscoe

remains almost same during the past four years. Comparing between 2017 and 2018, the ratio

has decreased by 1% that is in 2017, it was 41% and in 2018 it was 40%. However, such

minor reduction does not impacted the company as a whole (Refer Appendix).

4. Net Profit ratio

It is also one of the key financial ratio that is used for measuring the profitability of the

company. It represents the amount of net profit in terms of percentage of sales. It shows the

profits made by the company from its total revenue.

Referring to the Appendix, it is observed that the NPR of Briscoe Limited has increased over

the years but with fewer changes. In 2015, its NPR was 8% which increase to 10% in 2018.

The ratio remains same for the past two years because of the minor increase in the revenue

and net profits of the company. This implies that company is able to maintain its profitability

situation over the years and is performing better in financial aspects.

5. Interest coverage ratio

From the calculation done in Appendix, it can be said that Briscoe has the highest quick ratio

in 2015 with 1.24. Post the year, the ratio falls to 0.40 in 2016. Reason was the sudden

decrease in the current assets of the company. However, from 2016 a constant increase was

there in Briscoe’s QR and in 2018 it is reported at 0.91. This implies that company has

improved its current assets by managing them properly for meeting its quick and short term

liabilities.

3. Gross profit ratio

This ratio determoines the amount of profit earned by the firm after paying for its COGS,

expressed as a percentage of total sales (Jenter & Lewellen, 2015). The GPR of Briscoe

remains almost same during the past four years. Comparing between 2017 and 2018, the ratio

has decreased by 1% that is in 2017, it was 41% and in 2018 it was 40%. However, such

minor reduction does not impacted the company as a whole (Refer Appendix).

4. Net Profit ratio

It is also one of the key financial ratio that is used for measuring the profitability of the

company. It represents the amount of net profit in terms of percentage of sales. It shows the

profits made by the company from its total revenue.

Referring to the Appendix, it is observed that the NPR of Briscoe Limited has increased over

the years but with fewer changes. In 2015, its NPR was 8% which increase to 10% in 2018.

The ratio remains same for the past two years because of the minor increase in the revenue

and net profits of the company. This implies that company is able to maintain its profitability

situation over the years and is performing better in financial aspects.

5. Interest coverage ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 8

From the calculation shown in Appendix, ICR shows how many times a company can pay its

interest expense. Briscoe’s ICR in 2018 is 612.97 times which is way more than the ICR of

2017 and 2016. The highest was 8,853.67 times in 2015. This implies that company has

enough earnings to meet its interest expense (Parrino, Kidwell & Bates, 2011).

6. Return on Equity

ROE indicates the amount of return offered by a company to its shareholders (Saleem &

Rehman, 2011). In case of Briscoe, the ROE reduces to 25% in 2018, however it was remain

29% for the two years that is 2017 and 2016. This is because the shareholder equity has

increased over the year (Refer Appendix).

7. Earnings per share

EPS shows the profits available for equity shareholders. Briscoe has positive and increasing

EPS over the years. So, it can be interpreted that the same trend will follow in future also and

the company will offer more profits to its shareholders (Refer Appendix).

8. Price-earnings ratio

The P/E ratio of Briscoe is fluctuating due to the changes in market price. In 2018, it was

11.67 and the market price per share is $3.25. It is reduced as compare to 2017 because of

reduction in the market price of the share (Refer Appendix).

Performance of share price

The graph shown in the Appendix reflects the movements in share price of Briscoe Group

Limited over the past four years. It can be interpreted from the graph that price was

continuously increasing from 2015 and it was reported highest at $4.5 on March 2017. After

that some fluctuations were there due to which the prices reduces by the end of 2017.

From the calculation shown in Appendix, ICR shows how many times a company can pay its

interest expense. Briscoe’s ICR in 2018 is 612.97 times which is way more than the ICR of

2017 and 2016. The highest was 8,853.67 times in 2015. This implies that company has

enough earnings to meet its interest expense (Parrino, Kidwell & Bates, 2011).

6. Return on Equity

ROE indicates the amount of return offered by a company to its shareholders (Saleem &

Rehman, 2011). In case of Briscoe, the ROE reduces to 25% in 2018, however it was remain

29% for the two years that is 2017 and 2016. This is because the shareholder equity has

increased over the year (Refer Appendix).

7. Earnings per share

EPS shows the profits available for equity shareholders. Briscoe has positive and increasing

EPS over the years. So, it can be interpreted that the same trend will follow in future also and

the company will offer more profits to its shareholders (Refer Appendix).

8. Price-earnings ratio

The P/E ratio of Briscoe is fluctuating due to the changes in market price. In 2018, it was

11.67 and the market price per share is $3.25. It is reduced as compare to 2017 because of

reduction in the market price of the share (Refer Appendix).

Performance of share price

The graph shown in the Appendix reflects the movements in share price of Briscoe Group

Limited over the past four years. It can be interpreted from the graph that price was

continuously increasing from 2015 and it was reported highest at $4.5 on March 2017. After

that some fluctuations were there due to which the prices reduces by the end of 2017.

Accounting 9

However, in start of 2018 the prices again rises showing a positive trend for the investors.

Currently the share price of Briscoe is $3.48.

Recent announcements

In April 2018, the company announce about its 1st quarter sales of year 2018. The sales were

worth $146.4 million showing a 3.57% hike as compare to the same quarter of 2017. The

report also discloses that the group sales were 2.03% high and the departmental sales also

increases (Briscoegroup.com. 2018).

As per the article in NZ Herald, Briscoe’s total profit for the year 2017 rose by 25% to $59

million along with the upsurge in the sales. The increase in profit and revenue boosted up the

share price of the company and bring it to the highest if $4.5 per share (NZ Herald. 2017).

Final Decision

As per the analysis, it will be recommended to invest $50,000 in Briscoe Group Limited by

purchasing its shares at $3.55 (price as on April 22, 2018) because it is believed that the

company is doing well and will give more return as compare to the term deposit. Also it has

high profits, reasonable ROE and a good financial health. So, it will be recommended that the

shares of Briscoe’s Limited should be purchased.

However, in start of 2018 the prices again rises showing a positive trend for the investors.

Currently the share price of Briscoe is $3.48.

Recent announcements

In April 2018, the company announce about its 1st quarter sales of year 2018. The sales were

worth $146.4 million showing a 3.57% hike as compare to the same quarter of 2017. The

report also discloses that the group sales were 2.03% high and the departmental sales also

increases (Briscoegroup.com. 2018).

As per the article in NZ Herald, Briscoe’s total profit for the year 2017 rose by 25% to $59

million along with the upsurge in the sales. The increase in profit and revenue boosted up the

share price of the company and bring it to the highest if $4.5 per share (NZ Herald. 2017).

Final Decision

As per the analysis, it will be recommended to invest $50,000 in Briscoe Group Limited by

purchasing its shares at $3.55 (price as on April 22, 2018) because it is believed that the

company is doing well and will give more return as compare to the term deposit. Also it has

high profits, reasonable ROE and a good financial health. So, it will be recommended that the

shares of Briscoe’s Limited should be purchased.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 10

References

Alexander, D., Britton, A., & Jorissen, A. (2007). International financial reporting and

analysis. (3rd ed.). London: Thomson.

Berk, J. B., & DeMarzo, P. M. (2010). Corporate finance. India: Pearson Education.

Boex, A. (2015). Why cash flow is more important than profit. Retrieved from

https://www.unomaha.edu/nebraska-business-development-center/_files/

publications/cash-flow.pdf

Briscoegroup.com. (2018). 1st Quarter Sales to 29 April 2018. Retrieved from

http://briscoegroup.co.nz/wp-content/uploads/1st-Quarter-Sales-May-2018.pdf

Charifzadeh, M., & Taschner, A. (2017). Management accounting and control: tools and

concepts in a Central European context. Germany: John Wiley & Sons.

CPA. (2018). The importance of linking profitability and cash flow when analysing financial

statements. Retrieved from http://www.cpaireland.ie/docs/default-source/business-

resource/profitability-and-cashflow-(2009).pdf?sfvrsn=2

Dick, W., & Missonier-Piera, F. (2011). Financial reporting under IFRS: a topic based

approach (Vol. 1). UK: John Wiley & Sons.

Fernandez, P. (2006). Cash flow is cash and is a fact: Net income is an opinion. Retrieved

from https://www.iese.edu/research/pdfs/di-0629-e.pdf

Jenter, D., & Lewellen, K. (2015). CEO preferences and acquisitions. The Journal of

Finance, 70(6), 2813-2852.

Knight, F.H. (2012). Risk, uncertainty and profit. Courier Corporation.

References

Alexander, D., Britton, A., & Jorissen, A. (2007). International financial reporting and

analysis. (3rd ed.). London: Thomson.

Berk, J. B., & DeMarzo, P. M. (2010). Corporate finance. India: Pearson Education.

Boex, A. (2015). Why cash flow is more important than profit. Retrieved from

https://www.unomaha.edu/nebraska-business-development-center/_files/

publications/cash-flow.pdf

Briscoegroup.com. (2018). 1st Quarter Sales to 29 April 2018. Retrieved from

http://briscoegroup.co.nz/wp-content/uploads/1st-Quarter-Sales-May-2018.pdf

Charifzadeh, M., & Taschner, A. (2017). Management accounting and control: tools and

concepts in a Central European context. Germany: John Wiley & Sons.

CPA. (2018). The importance of linking profitability and cash flow when analysing financial

statements. Retrieved from http://www.cpaireland.ie/docs/default-source/business-

resource/profitability-and-cashflow-(2009).pdf?sfvrsn=2

Dick, W., & Missonier-Piera, F. (2011). Financial reporting under IFRS: a topic based

approach (Vol. 1). UK: John Wiley & Sons.

Fernandez, P. (2006). Cash flow is cash and is a fact: Net income is an opinion. Retrieved

from https://www.iese.edu/research/pdfs/di-0629-e.pdf

Jenter, D., & Lewellen, K. (2015). CEO preferences and acquisitions. The Journal of

Finance, 70(6), 2813-2852.

Knight, F.H. (2012). Risk, uncertainty and profit. Courier Corporation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 11

NZ Herald. (2017). Briscoe Group's full-year profit rose 25pc to about $59 million. Retrieved

from https://www.nzherald.co.nz/business/news/article.cfm?

c_id=3&objectid=11793458

Palepu, K. G., & Healy, P. M. (2007). Business analysis and valuation. USA: Cengage

Learning EMEA.

Parrino, R., Kidwell, D. S., & Bates, T. (2011). Fundamentals of corporate finance. John

Wiley & Sons.

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Rajasekaran, V. (2011). Financial accounting. India: Pearson Education India.

Saleem, Q., & Rehman, R. U. (2011). Impacts of liquidity ratios on

profitability. Interdisciplinary Journal of Research in Business, 1(7), 95-98.

Sinha, G. (2012). Financial statement analysis. (2nd ed.). New Delhi: PHI Learning Pvt. Ltd..

Tracy, A. (2012). Ratio analysis fundamentals: how 17 financial ratios can allow you to

analyse any business on the planet. RatioAnalysis. net.

Yahoo Finance. (2018). BGP.NZ Interactive Chart Briscoe Group Limited Ordinary Stock -

Retrieved from https://finance.yahoo.com/quote/BGP.NZ/financials?p=BGP.NZ

NZ Herald. (2017). Briscoe Group's full-year profit rose 25pc to about $59 million. Retrieved

from https://www.nzherald.co.nz/business/news/article.cfm?

c_id=3&objectid=11793458

Palepu, K. G., & Healy, P. M. (2007). Business analysis and valuation. USA: Cengage

Learning EMEA.

Parrino, R., Kidwell, D. S., & Bates, T. (2011). Fundamentals of corporate finance. John

Wiley & Sons.

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Rajasekaran, V. (2011). Financial accounting. India: Pearson Education India.

Saleem, Q., & Rehman, R. U. (2011). Impacts of liquidity ratios on

profitability. Interdisciplinary Journal of Research in Business, 1(7), 95-98.

Sinha, G. (2012). Financial statement analysis. (2nd ed.). New Delhi: PHI Learning Pvt. Ltd..

Tracy, A. (2012). Ratio analysis fundamentals: how 17 financial ratios can allow you to

analyse any business on the planet. RatioAnalysis. net.

Yahoo Finance. (2018). BGP.NZ Interactive Chart Briscoe Group Limited Ordinary Stock -

Retrieved from https://finance.yahoo.com/quote/BGP.NZ/financials?p=BGP.NZ

Accounting 12

Appendix

Current ratio

Particulars 2018 2017 2016 2015

Current assets (A)

155,471 141,600

10808

7 170752

Current liabilities

(B) 89417 92336 70281 78467

CR (A/B) 1.74 1.53 1.54 2.18

Quick ratio

Particulars 2018 2017 2016 2015

Quick assets (A) 80,977 62,669 27883 97245

Current liabilities (B) 89417 92336 70281 78467

QR (A/B) 0.91 0.68 0.40 1.24

Gross profit ratio

Particulars 2018 2017 2016 2015

Gross profit (A)

244,17

2

239,357

22387

1 197247

Total revenue (B) 603086 582840

55289

2 507063

GPR (A/B) 40% 41% 40% 39%

Appendix

Current ratio

Particulars 2018 2017 2016 2015

Current assets (A)

155,471 141,600

10808

7 170752

Current liabilities

(B) 89417 92336 70281 78467

CR (A/B) 1.74 1.53 1.54 2.18

Quick ratio

Particulars 2018 2017 2016 2015

Quick assets (A) 80,977 62,669 27883 97245

Current liabilities (B) 89417 92336 70281 78467

QR (A/B) 0.91 0.68 0.40 1.24

Gross profit ratio

Particulars 2018 2017 2016 2015

Gross profit (A)

244,17

2

239,357

22387

1 197247

Total revenue (B) 603086 582840

55289

2 507063

GPR (A/B) 40% 41% 40% 39%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.