Managerial Accounting: Cost Analysis and Decision-Making Report

VerifiedAdded on 2023/04/03

|17

|3746

|493

Report

AI Summary

This managerial accounting report provides a comprehensive analysis of cost structures and decision-making processes within a child care business context. The report begins by classifying costs into fixed, variable, and semi-variable categories, providing examples from the case study. It then examines relevant and irrelevant information for purchasing appliances, emphasizing the importance of cost accounting in managerial decisions. The report further analyzes three options for laundering clothes, recommending the most cost-effective choice. A feasibility analysis is conducted to determine the profitability of hiring additional employees, followed by an assessment of renting space versus operating from the existing location. The analysis includes detailed financial tables comparing different scenarios and their impact on net profit margins, ultimately recommending that the business continues operating from its current location. The report concludes by examining the application of managerial accounting principles, using case studies from Canon Inc. and Apple Computer Inc. to illustrate the concepts.

Running head: MANAGERIAL ACCOUNTING

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Table of Contents

Part A:...........................................................................................................................2

Answer to requirement 1:.............................................................................................2

Answer to requirement 2:.............................................................................................2

Answer to requirement 3:.............................................................................................2

Answer to requirement 4:.............................................................................................2

Answer to requirement 5:.............................................................................................2

Part B:...........................................................................................................................2

Answer to requirement 1:.............................................................................................2

Answer to requirement 2:.............................................................................................3

Answer to requirement 3:.............................................................................................3

References and Bibliography list:.................................................................................3

Table of Contents

Part A:...........................................................................................................................2

Answer to requirement 1:.............................................................................................2

Answer to requirement 2:.............................................................................................2

Answer to requirement 3:.............................................................................................2

Answer to requirement 4:.............................................................................................2

Answer to requirement 5:.............................................................................................2

Part B:...........................................................................................................................2

Answer to requirement 1:.............................................................................................2

Answer to requirement 2:.............................................................................................3

Answer to requirement 3:.............................................................................................3

References and Bibliography list:.................................................................................3

MANAGERIAL ACCOUNTING

Part A:

Answer to requirement 1:

Depending upon the application and nature, there can be various

classifications of costs. From the analysis of the case study, it can be observed that

the business of child care incurs three different types of cost. These costs include

fixed cost, variable cost and semi variable costs. There are several components of

cash that has been incorporated in the case study. The first cost that has been

observed is the fixed cost. Fixed costs are those costs which remain constant

regardless of the production volume or the service provided. That is they will not vary

with the change in output level and would remain fixed throughout. In the given case

study, for running the child care business, there are two fixed costs that are incurred

such as insurance cost and license fee. The license fees paid by the couple to the

state are $ 225 and they also incur insurance cost of $ 3840 on annual basis. One

point that should be notes is that the license fee paid for running the business is that

it grants the limit of serving 6 children. In case, the business intends to take care of

more than 6 children, then the license fee payable by the business would increase.

Another cost that has been found is the variable cost. Variable cost is the cost

that varies in proportion to the level of output or services provided. It means that the

costs incurred would increase or decrease when there is an increase or decrease in

the level of services provided and output produced. Some of the variable cost that is

incurred by the child care business is utility cost and cost of providing meal and

snacks is also a variable cost. It is so because this cost would increase with increase

in the number of children being served. Another variable cost that can be considered

Part A:

Answer to requirement 1:

Depending upon the application and nature, there can be various

classifications of costs. From the analysis of the case study, it can be observed that

the business of child care incurs three different types of cost. These costs include

fixed cost, variable cost and semi variable costs. There are several components of

cash that has been incorporated in the case study. The first cost that has been

observed is the fixed cost. Fixed costs are those costs which remain constant

regardless of the production volume or the service provided. That is they will not vary

with the change in output level and would remain fixed throughout. In the given case

study, for running the child care business, there are two fixed costs that are incurred

such as insurance cost and license fee. The license fees paid by the couple to the

state are $ 225 and they also incur insurance cost of $ 3840 on annual basis. One

point that should be notes is that the license fee paid for running the business is that

it grants the limit of serving 6 children. In case, the business intends to take care of

more than 6 children, then the license fee payable by the business would increase.

Another cost that has been found is the variable cost. Variable cost is the cost

that varies in proportion to the level of output or services provided. It means that the

costs incurred would increase or decrease when there is an increase or decrease in

the level of services provided and output produced. Some of the variable cost that is

incurred by the child care business is utility cost and cost of providing meal and

snacks is also a variable cost. It is so because this cost would increase with increase

in the number of children being served. Another variable cost that can be considered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

to be the variable cost is the total amount of salary that is payable to employee

(Joshi & Li, 2016).

Semi variable costs are the costs that remain fixed for certain period of time and it

increases thereafter. It means that the semi variable cost is the combination of both

variable and fixed cost. Some of the semi variable cost that is incurred by the child

care business are utility cost, energy cost of running washer and dryer along with the

cost of meal and snacks.

Answer to requirement 2:

This section discusses about the information that is relevant and should be

considered by the couple to purchase the appliances. The managerial decision taken

by the entrepreneur is dependant upon the aspect of cost accounting. It is seen that

for laundering the soiled clothes of babies, the couple is seeking to purchase the

appliances. For purchasing the appliance, the couple is required to take into account

relevant information such as cost of installing the machine, cost of purchasing the

washer and dryer and delivery charges for purchasing the appliances. In addition to

this, Frank is also required to consider the factor such as operating expenses which

include energy cost of running the dryer and washer, travelling charges, laundry

supplies and laundering charge along with the depreciation charges. Such costs help

in accounting for the total outflow of cash and the total annual expenses that would

be required to purchase and install the new appliances. The information that is

considered irrelevant for purchasing the appliances is the cost of old appliances and

the license fees along with the insurance cost (Kianto et al., 2017). This is so

because for purchasing the new appliances, it is not required to consider the cost of

old appliances.

to be the variable cost is the total amount of salary that is payable to employee

(Joshi & Li, 2016).

Semi variable costs are the costs that remain fixed for certain period of time and it

increases thereafter. It means that the semi variable cost is the combination of both

variable and fixed cost. Some of the semi variable cost that is incurred by the child

care business are utility cost, energy cost of running washer and dryer along with the

cost of meal and snacks.

Answer to requirement 2:

This section discusses about the information that is relevant and should be

considered by the couple to purchase the appliances. The managerial decision taken

by the entrepreneur is dependant upon the aspect of cost accounting. It is seen that

for laundering the soiled clothes of babies, the couple is seeking to purchase the

appliances. For purchasing the appliance, the couple is required to take into account

relevant information such as cost of installing the machine, cost of purchasing the

washer and dryer and delivery charges for purchasing the appliances. In addition to

this, Frank is also required to consider the factor such as operating expenses which

include energy cost of running the dryer and washer, travelling charges, laundry

supplies and laundering charge along with the depreciation charges. Such costs help

in accounting for the total outflow of cash and the total annual expenses that would

be required to purchase and install the new appliances. The information that is

considered irrelevant for purchasing the appliances is the cost of old appliances and

the license fees along with the insurance cost (Kianto et al., 2017). This is so

because for purchasing the new appliances, it is not required to consider the cost of

old appliances.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

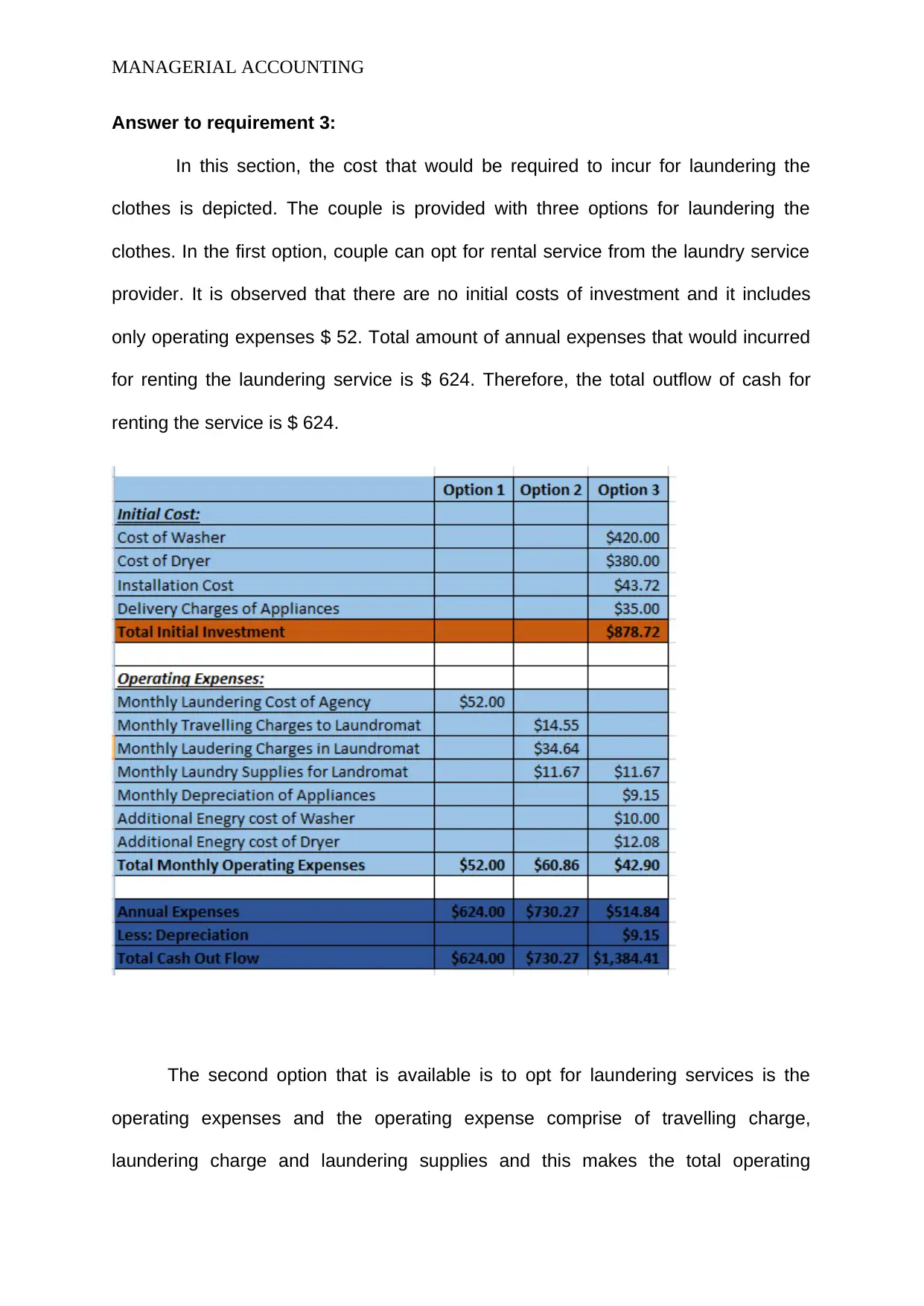

Answer to requirement 3:

In this section, the cost that would be required to incur for laundering the

clothes is depicted. The couple is provided with three options for laundering the

clothes. In the first option, couple can opt for rental service from the laundry service

provider. It is observed that there are no initial costs of investment and it includes

only operating expenses $ 52. Total amount of annual expenses that would incurred

for renting the laundering service is $ 624. Therefore, the total outflow of cash for

renting the service is $ 624.

The second option that is available is to opt for laundering services is the

operating expenses and the operating expense comprise of travelling charge,

laundering charge and laundering supplies and this makes the total operating

Answer to requirement 3:

In this section, the cost that would be required to incur for laundering the

clothes is depicted. The couple is provided with three options for laundering the

clothes. In the first option, couple can opt for rental service from the laundry service

provider. It is observed that there are no initial costs of investment and it includes

only operating expenses $ 52. Total amount of annual expenses that would incurred

for renting the laundering service is $ 624. Therefore, the total outflow of cash for

renting the service is $ 624.

The second option that is available is to opt for laundering services is the

operating expenses and the operating expense comprise of travelling charge,

laundering charge and laundering supplies and this makes the total operating

MANAGERIAL ACCOUNTING

expense to $ 60.86. The total annual expenses and the total outflow of cash that

would be required to incur is $ 730.27. Now, looking at the third option which

requires the couple to purchase dryer and washer, it is observed that the couple

would be required to incur initial investment along with the operating expenses. Total

cost of investment includes installation cost, cost of purchasing dryer and washer

along with the delivery charges of appliances. The total amount that should be

invested at the initial level is $ 878.72. In addition to this, there are other operating

expenses that is to take into account is energy cost of dryer and washer,

depreciation charge and supply if laundry for Laundromat. The annual expenses that

would be incurred are $ 514.84 and the total outflow of cash is $ 1384.41. From the

analysis of above figures, it is ascertained that the maximum outflow of cash is in

third option. However, the couple would have to incur minimal annual expenses of $

514.84 when they are opting to purchaser dryer and washer. When looking at the

option of total cash flow, it is observed that the renting the service from Red oak

laundry and dry cleaning would have the minimal outflow of cash. Therefore, from

the analysis of figures, t is inferred that the couple should consider option one.

Hence, it is recommended that couple should opt for renting the service from Red

oak laundry and dry cleaning.

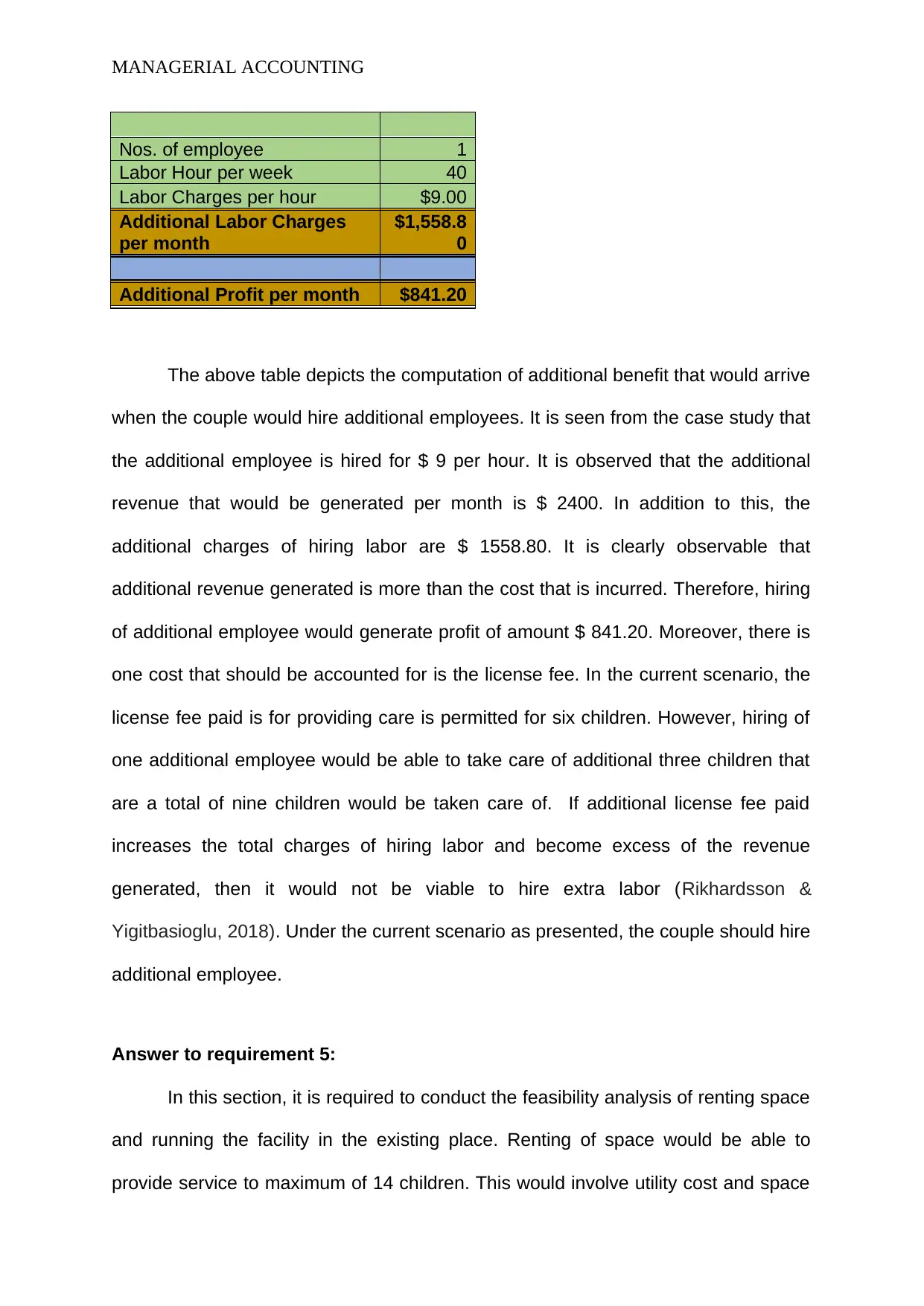

Answer to requirement 4:

This section evaluates the benefits or loss that would occur when the

additional employee is hired for the business to take care of additional children.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

expense to $ 60.86. The total annual expenses and the total outflow of cash that

would be required to incur is $ 730.27. Now, looking at the third option which

requires the couple to purchase dryer and washer, it is observed that the couple

would be required to incur initial investment along with the operating expenses. Total

cost of investment includes installation cost, cost of purchasing dryer and washer

along with the delivery charges of appliances. The total amount that should be

invested at the initial level is $ 878.72. In addition to this, there are other operating

expenses that is to take into account is energy cost of dryer and washer,

depreciation charge and supply if laundry for Laundromat. The annual expenses that

would be incurred are $ 514.84 and the total outflow of cash is $ 1384.41. From the

analysis of above figures, it is ascertained that the maximum outflow of cash is in

third option. However, the couple would have to incur minimal annual expenses of $

514.84 when they are opting to purchaser dryer and washer. When looking at the

option of total cash flow, it is observed that the renting the service from Red oak

laundry and dry cleaning would have the minimal outflow of cash. Therefore, from

the analysis of figures, t is inferred that the couple should consider option one.

Hence, it is recommended that couple should opt for renting the service from Red

oak laundry and dry cleaning.

Answer to requirement 4:

This section evaluates the benefits or loss that would occur when the

additional employee is hired for the business to take care of additional children.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

The above table depicts the computation of additional benefit that would arrive

when the couple would hire additional employees. It is seen from the case study that

the additional employee is hired for $ 9 per hour. It is observed that the additional

revenue that would be generated per month is $ 2400. In addition to this, the

additional charges of hiring labor are $ 1558.80. It is clearly observable that

additional revenue generated is more than the cost that is incurred. Therefore, hiring

of additional employee would generate profit of amount $ 841.20. Moreover, there is

one cost that should be accounted for is the license fee. In the current scenario, the

license fee paid is for providing care is permitted for six children. However, hiring of

one additional employee would be able to take care of additional three children that

are a total of nine children would be taken care of. If additional license fee paid

increases the total charges of hiring labor and become excess of the revenue

generated, then it would not be viable to hire extra labor (Rikhardsson &

Yigitbasioglu, 2018). Under the current scenario as presented, the couple should hire

additional employee.

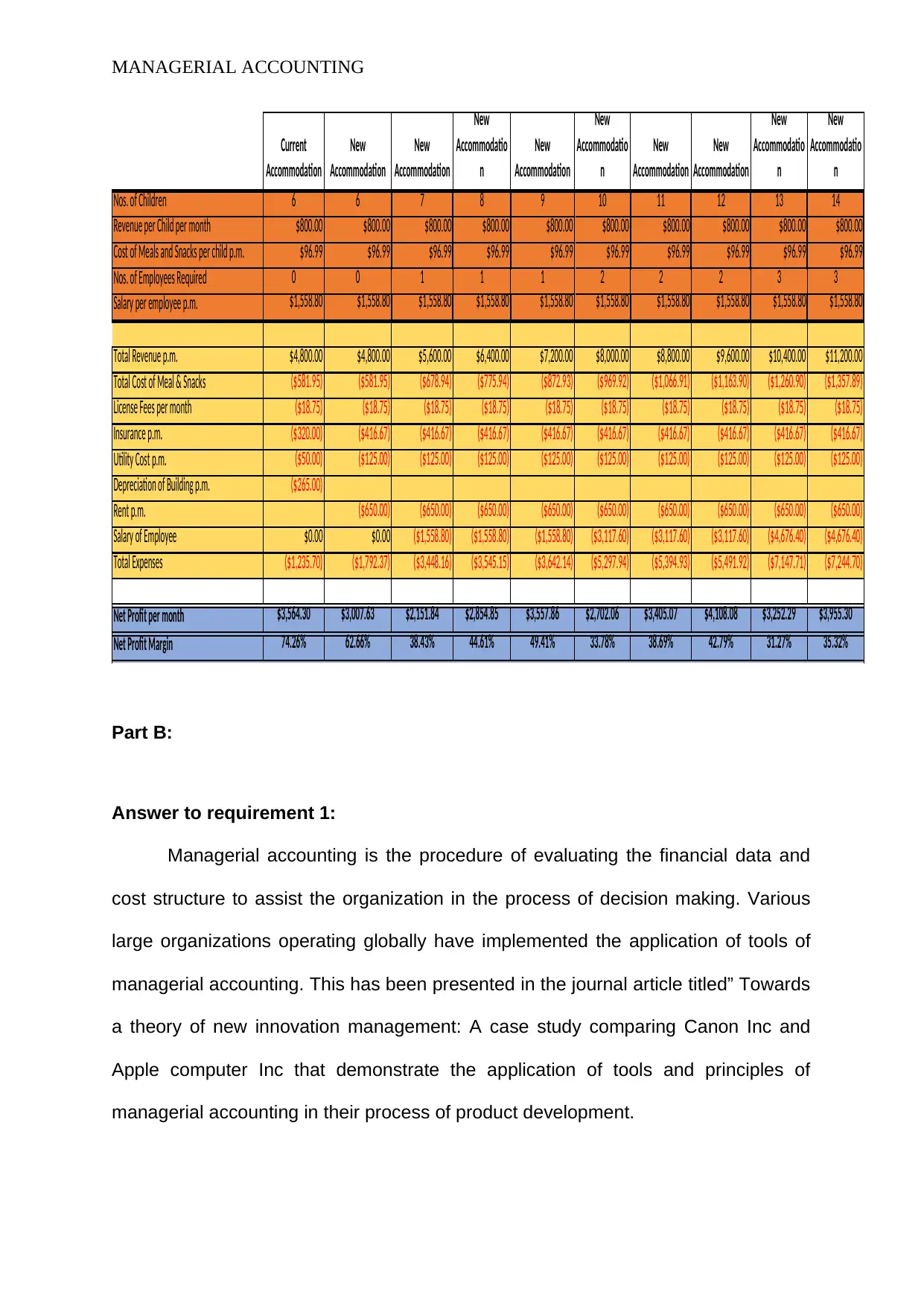

Answer to requirement 5:

In this section, it is required to conduct the feasibility analysis of renting space

and running the facility in the existing place. Renting of space would be able to

provide service to maximum of 14 children. This would involve utility cost and space

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

The above table depicts the computation of additional benefit that would arrive

when the couple would hire additional employees. It is seen from the case study that

the additional employee is hired for $ 9 per hour. It is observed that the additional

revenue that would be generated per month is $ 2400. In addition to this, the

additional charges of hiring labor are $ 1558.80. It is clearly observable that

additional revenue generated is more than the cost that is incurred. Therefore, hiring

of additional employee would generate profit of amount $ 841.20. Moreover, there is

one cost that should be accounted for is the license fee. In the current scenario, the

license fee paid is for providing care is permitted for six children. However, hiring of

one additional employee would be able to take care of additional three children that

are a total of nine children would be taken care of. If additional license fee paid

increases the total charges of hiring labor and become excess of the revenue

generated, then it would not be viable to hire extra labor (Rikhardsson &

Yigitbasioglu, 2018). Under the current scenario as presented, the couple should hire

additional employee.

Answer to requirement 5:

In this section, it is required to conduct the feasibility analysis of renting space

and running the facility in the existing place. Renting of space would be able to

provide service to maximum of 14 children. This would involve utility cost and space

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

cost of amount $ 125 and $ 650 per month. In addition to this, there will be increased

cost of $ 5000. In order to determine which of the two options would be viable, the

net profit margin generated is compared along with the total expenses that are

incurred by the business.

Under the current accommodation, it is seen that the couple has to incur total

expenses of $ 1235.70 with the total net profit generated is at $ 3564.30. The total

net profit margin is 74.26 %. Now, considering the situation under new

accommodation when the maximum of 14 children can be taken care of, it is

observed that the total amount of expenses incurred is increasing with increasing

number of children served. Net profit margin on other hand is decreasing on the

continuous basis from 62.66% in case of serving six children and 35.32% in case of

14 children. Therefore, from the analysis of the figures in both the cases, it is

observed that business under the existing accommodation is generating higher net

profit margin compared to facility under the rented space. Hence, it is recommended

that the couple should continue operating the facility at their home instead of renting

the space. Consequently, it would be viable to serve a total of six children that does

not require hiring of any employees.

cost of amount $ 125 and $ 650 per month. In addition to this, there will be increased

cost of $ 5000. In order to determine which of the two options would be viable, the

net profit margin generated is compared along with the total expenses that are

incurred by the business.

Under the current accommodation, it is seen that the couple has to incur total

expenses of $ 1235.70 with the total net profit generated is at $ 3564.30. The total

net profit margin is 74.26 %. Now, considering the situation under new

accommodation when the maximum of 14 children can be taken care of, it is

observed that the total amount of expenses incurred is increasing with increasing

number of children served. Net profit margin on other hand is decreasing on the

continuous basis from 62.66% in case of serving six children and 35.32% in case of

14 children. Therefore, from the analysis of the figures in both the cases, it is

observed that business under the existing accommodation is generating higher net

profit margin compared to facility under the rented space. Hence, it is recommended

that the couple should continue operating the facility at their home instead of renting

the space. Consequently, it would be viable to serve a total of six children that does

not require hiring of any employees.

MANAGERIAL ACCOUNTING

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

Part B:

Answer to requirement 1:

Managerial accounting is the procedure of evaluating the financial data and

cost structure to assist the organization in the process of decision making. Various

large organizations operating globally have implemented the application of tools of

managerial accounting. This has been presented in the journal article titled” Towards

a theory of new innovation management: A case study comparing Canon Inc and

Apple computer Inc that demonstrate the application of tools and principles of

managerial accounting in their process of product development.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

Part B:

Answer to requirement 1:

Managerial accounting is the procedure of evaluating the financial data and

cost structure to assist the organization in the process of decision making. Various

large organizations operating globally have implemented the application of tools of

managerial accounting. This has been presented in the journal article titled” Towards

a theory of new innovation management: A case study comparing Canon Inc and

Apple computer Inc that demonstrate the application of tools and principles of

managerial accounting in their process of product development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

In the technologies industry, Canon Inc leads the market in photocopier

segment whereas Apple Inc is the market leader in manufacturing of innovative and

premium computers. Competitive advantage of the organization in producing any

product is the success that is dependent on the sound management and the core

competencies of company. It is required by the companies to embrace innovation in

the ever changing technological markets in terms of their costing and managing the

products. It can be cited from the case study that is demonstrating the case of Apple

Inc and Canon Inc that is emphasizing on one of the important aspects of

management accounting that is the process of sharing and creating information.

When studying the case of Canon Inc, it is seen that the development of the new

product that is mini copier has been done by complete restructuring of entire plain

paper copier market (Nonala and Kenney, 1991). It can be observed that the Canon

Inc also incorporated the components in their innovation process of developing mini

copier. For this purpose, a feasibility group was formed by the company by taking

personnel from different departments. The management of the company intended to

make effective and conscious decision by forming the group comprising of

executives from various department of organization (Kastberg & Siverbo, 2016).

Moreover, the manufacturing managers from the integrated part of the team because

Apple intended to build highly automated factory that would be capable of producing

the Macintosh inexpensively by setting lower target price. For the development of

Apple Macintosh, it can be seen that Steve struggled to build the product as building

of Mac separately created conflict and this resulted in the lack of coordination

between group of Mac and other divisions of Apple and due to the lack of transfer of

technology. It was the string management of organization that contributed to the

successful development of product due to continuous interaction between the team

In the technologies industry, Canon Inc leads the market in photocopier

segment whereas Apple Inc is the market leader in manufacturing of innovative and

premium computers. Competitive advantage of the organization in producing any

product is the success that is dependent on the sound management and the core

competencies of company. It is required by the companies to embrace innovation in

the ever changing technological markets in terms of their costing and managing the

products. It can be cited from the case study that is demonstrating the case of Apple

Inc and Canon Inc that is emphasizing on one of the important aspects of

management accounting that is the process of sharing and creating information.

When studying the case of Canon Inc, it is seen that the development of the new

product that is mini copier has been done by complete restructuring of entire plain

paper copier market (Nonala and Kenney, 1991). It can be observed that the Canon

Inc also incorporated the components in their innovation process of developing mini

copier. For this purpose, a feasibility group was formed by the company by taking

personnel from different departments. The management of the company intended to

make effective and conscious decision by forming the group comprising of

executives from various department of organization (Kastberg & Siverbo, 2016).

Moreover, the manufacturing managers from the integrated part of the team because

Apple intended to build highly automated factory that would be capable of producing

the Macintosh inexpensively by setting lower target price. For the development of

Apple Macintosh, it can be seen that Steve struggled to build the product as building

of Mac separately created conflict and this resulted in the lack of coordination

between group of Mac and other divisions of Apple and due to the lack of transfer of

technology. It was the string management of organization that contributed to the

successful development of product due to continuous interaction between the team

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

and transmission of information within the team that resulted in creation of

innovation.

The system of sharing and transmitting information by way of innovation

brought by the application of various tools of management accounting system has

provided opportunities to companies to make their product cost effective and

innovative. Furthermore, it can also be said that excellent innovation in the operating

segment of organization has resulted due to harmonization and collaboration due to

closely working of managers and engineer along with personnel from different

departments (Zott & Amit, 2015). Therefore, from the above discussion, it can be

concluded that the decision making process in the organization can be improved and

become effective due to the application of techniques and tools of managerial

accounting.

Answer to requirement 2:

The management accounting system of the organization has evolved

considerably due to embracing innovation as the accounting system helps in

addressing the challenges faced by the company in uncertain operating settings.

There are no existing reviews that have built upon the development of innovation in

the management accounting system. The current journal article is a contribution to

the literature of managerial accounting by exploring the product development

process at Canon and Apple Inc (Nonala and Kenney, 1991). The process of

innovation has been outlined in the creation and sharing of information in an effective

and efficient manner by the management of the firm. It can be seen that such

proposition is true as the process of management in these firms incorporate analysis

and transmission of information that can be financial as well as non financial. The

and transmission of information within the team that resulted in creation of

innovation.

The system of sharing and transmitting information by way of innovation

brought by the application of various tools of management accounting system has

provided opportunities to companies to make their product cost effective and

innovative. Furthermore, it can also be said that excellent innovation in the operating

segment of organization has resulted due to harmonization and collaboration due to

closely working of managers and engineer along with personnel from different

departments (Zott & Amit, 2015). Therefore, from the above discussion, it can be

concluded that the decision making process in the organization can be improved and

become effective due to the application of techniques and tools of managerial

accounting.

Answer to requirement 2:

The management accounting system of the organization has evolved

considerably due to embracing innovation as the accounting system helps in

addressing the challenges faced by the company in uncertain operating settings.

There are no existing reviews that have built upon the development of innovation in

the management accounting system. The current journal article is a contribution to

the literature of managerial accounting by exploring the product development

process at Canon and Apple Inc (Nonala and Kenney, 1991). The process of

innovation has been outlined in the creation and sharing of information in an effective

and efficient manner by the management of the firm. It can be seen that such

proposition is true as the process of management in these firms incorporate analysis

and transmission of information that can be financial as well as non financial. The

MANAGERIAL ACCOUNTING

information system of business can be utilized efficiently by analyzing the business

activities that takes into account both the relevant financial and non financial

information (Bromwich & Scapens, 2016).

The case study of Canon Inc and Apple Inc has presented innovation as the

process that helps in creating the information that arises from the interacting socially

between the team members. Innovation facilitated the development of product at

both the organizations and it was drawn from controlling and the planning

components of managerial accounting (Nonala and Kenney, 1991). At canon, the

human activity formed the basis of recapitalization of entire plain paper copier and

not on the deduction or any induction. Gathering of personnel outside the workplace

resulted in brainstorming of the solutions for contradicting the copier. The innovation

of making copier maintenance free was made by drum development that would lame

the copier after certain number has been produced (Mancini et al., 2017).

The Macintosh computer was evolved by adding new features and ideas that

was generated due to constant interaction between the development technical team.

The CEO of the company that is Steve played a critical role in the development of

product as he rethought about the existing computer features by accounting for the

telephone transformative role and based the new computer dimension to that of

telephone book (Nonala and Kenney, 1991).

Answer to requirement 3:

From the analysis of the journal articles, some of the relevant findings were

generated that would be useful to the management accountants of Australian

companies. The article has presented the importance of innovation brought by the

transmission and creation of information in the decision making process. It is

information system of business can be utilized efficiently by analyzing the business

activities that takes into account both the relevant financial and non financial

information (Bromwich & Scapens, 2016).

The case study of Canon Inc and Apple Inc has presented innovation as the

process that helps in creating the information that arises from the interacting socially

between the team members. Innovation facilitated the development of product at

both the organizations and it was drawn from controlling and the planning

components of managerial accounting (Nonala and Kenney, 1991). At canon, the

human activity formed the basis of recapitalization of entire plain paper copier and

not on the deduction or any induction. Gathering of personnel outside the workplace

resulted in brainstorming of the solutions for contradicting the copier. The innovation

of making copier maintenance free was made by drum development that would lame

the copier after certain number has been produced (Mancini et al., 2017).

The Macintosh computer was evolved by adding new features and ideas that

was generated due to constant interaction between the development technical team.

The CEO of the company that is Steve played a critical role in the development of

product as he rethought about the existing computer features by accounting for the

telephone transformative role and based the new computer dimension to that of

telephone book (Nonala and Kenney, 1991).

Answer to requirement 3:

From the analysis of the journal articles, some of the relevant findings were

generated that would be useful to the management accountants of Australian

companies. The article has presented the importance of innovation brought by the

transmission and creation of information in the decision making process. It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.