Taxation Assignment: Analysis of Current and Deferred Tax

VerifiedAdded on 2022/09/16

|6

|446

|21

Homework Assignment

AI Summary

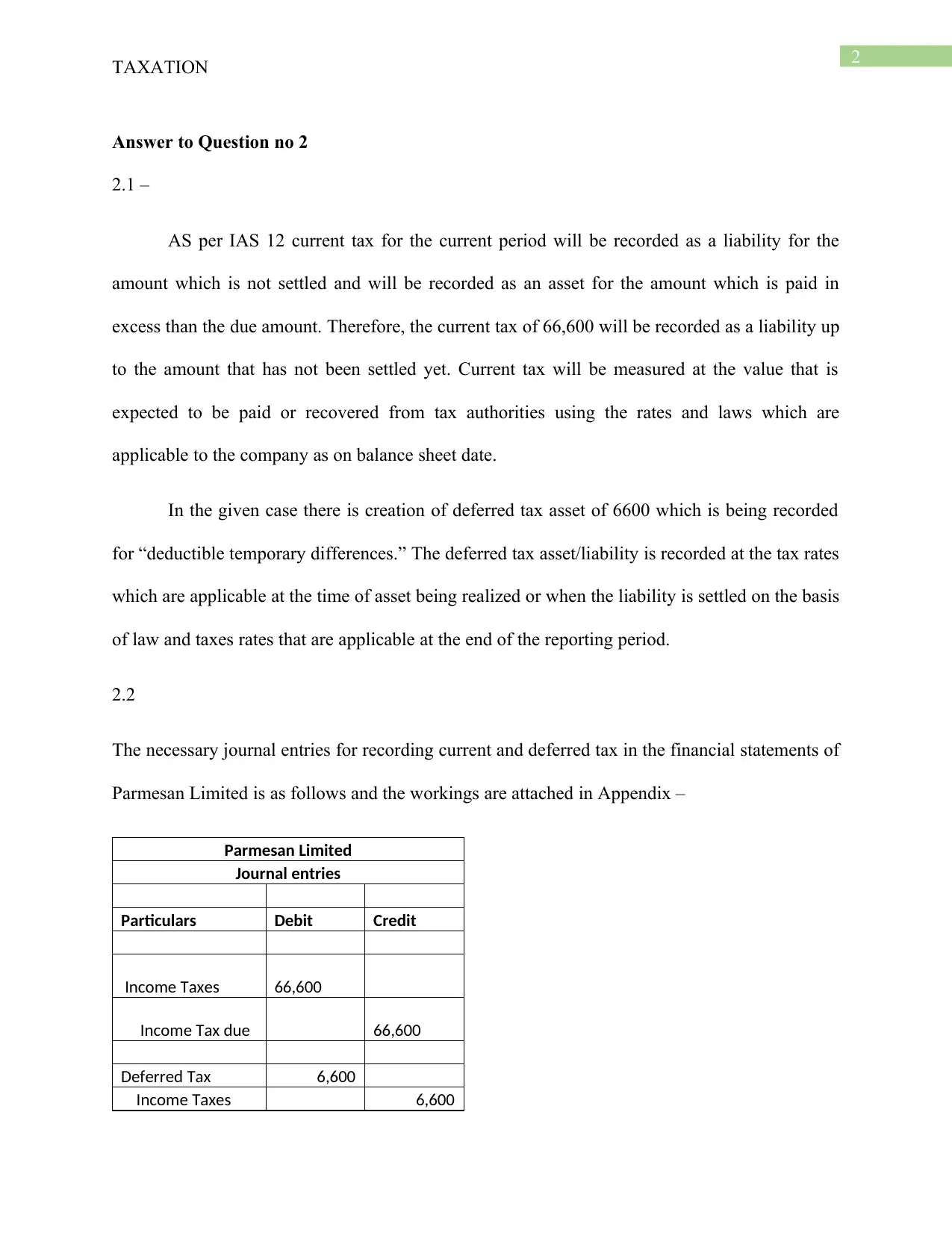

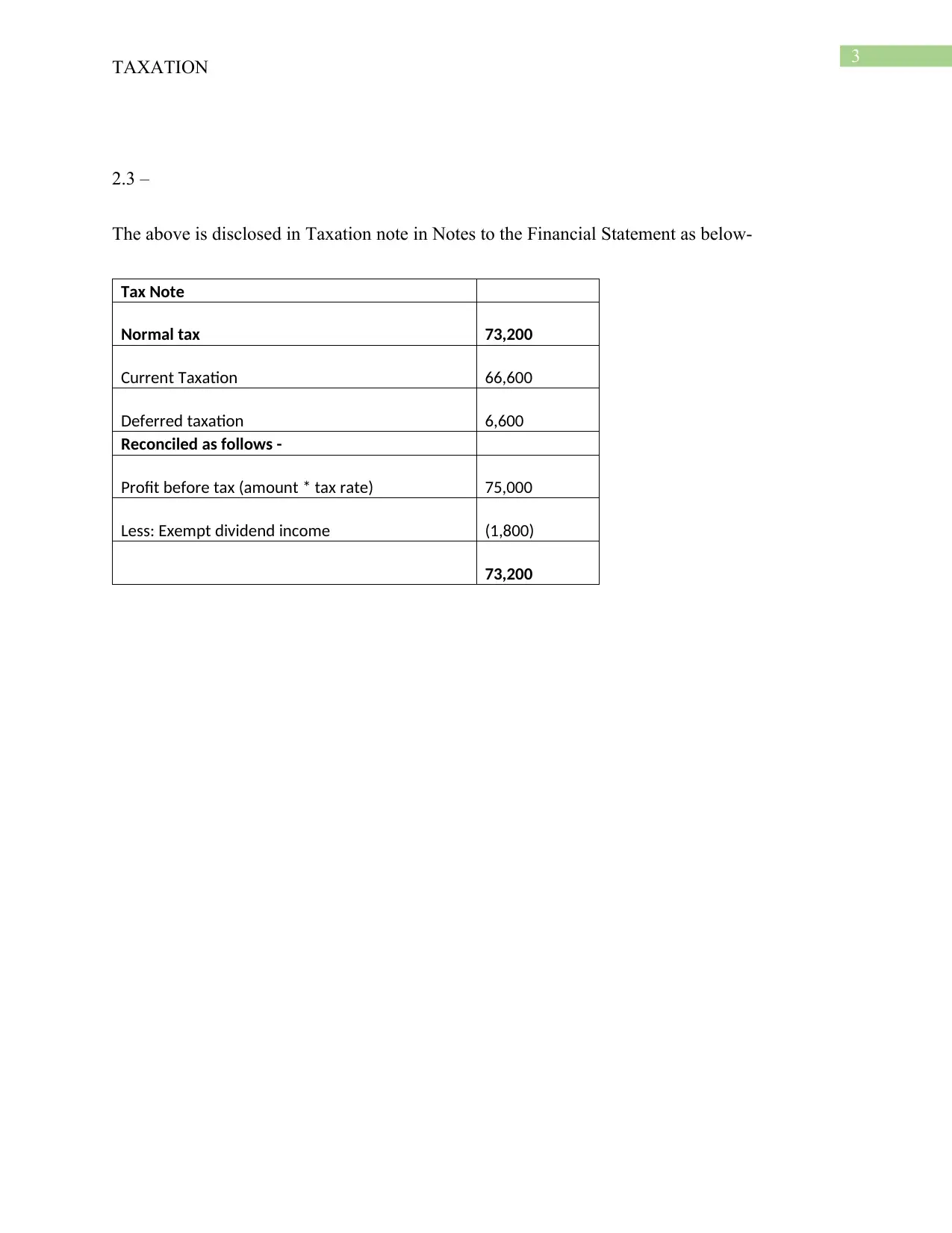

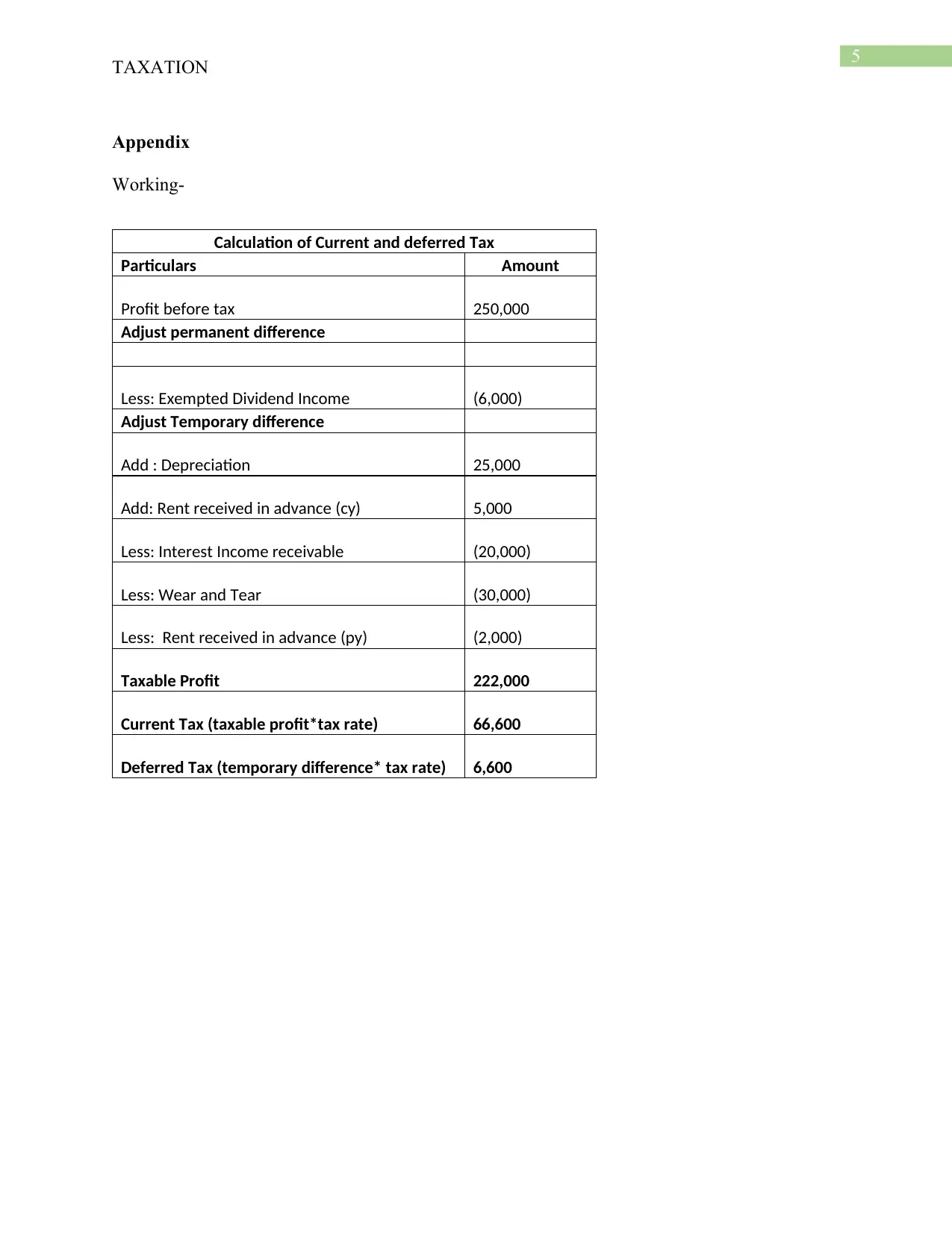

This document provides a comprehensive solution to a taxation assignment, focusing on the accounting treatment of current and deferred taxes. The assignment analyzes the calculation of current tax liability and the recognition of deferred tax assets. It includes detailed journal entries for recording both current and deferred tax, along with explanations of the underlying principles and relevant accounting standards (IAS 12). The solution demonstrates how to reconcile profit before tax with taxable profit, considering temporary and permanent differences. It also presents the required disclosures in the notes to the financial statements, including the breakdown of current and deferred tax components. Furthermore, the document provides a working paper that outlines the detailed calculations of current and deferred tax liabilities, including adjustments for permanent differences, and temporary differences. This assignment provides a thorough understanding of taxation, accounting, and financial reporting.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.