Analysis of Current Development in Accounting and Economic Trends

VerifiedAdded on 2022/12/18

|16

|3768

|29

Homework Assignment

AI Summary

This assignment analyzes current developments in accounting, focusing on a newspaper article discussing the International Monetary Fund's forecast of a sluggish global economy due to trade tensions and uncertainties. The analysis explores the impact of these economic trends on accounting practices, including the implications of the US-China trade war, Federal Reserve policies, and the Eurozone's economic outlook. The assignment also delves into the IASB exposure draft concerning amendments to IFRS 9 and IAS 39, addressing issues related to benchmark interest rates, cash flow hedges, and fair value hedges. The analysis highlights the draft's views on hedging effectiveness, the treatment of deferred cash flow, and disagreements among market players regarding financial benchmarks and hedging techniques.

Running head : CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Name of the Student

Name of the University

Author Note

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................2

References..................................................................................................................................2

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................2

References..................................................................................................................................2

2CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Question 1

From the newspaper journal Perth Now, there could be found an accounting issue that

relates to the issue of the International Monetary Fund forecasting sluggish Global Economy.

According to the journal dated 23rd July 2019, the Global Trade tensions and continuation of

the uncertainty are weakening the merits of the world economy, that would be facing a

precarious year ahead as said by the International Monetary Fund (2019 PerthNow). As per

the update of the World economic Outlook, the International Monetary Fund had forced the

countries for not using the tariffs in the place of the negotiations. The World Economic

Outlook got update on this regard that the International Monetary Fund shaped the Global

Forecast issued in the month of April, with an expected growth to hit 3.2 per cent in the year

2020 (2019 PerthNow). As per the declaration of the International Monetary Fund, they are

expecting an expansion of the global economy by a sluggish 3.2 per cent in the year 2019,

down from 3.6 per cent in the year 2018 and from a growth rate of 3.3 per cent it forecasted

for this year back in the month of April. The 189 country lending organisation blamed the

lack lustre growth on the heightened trade tensions and it specifically a war of tariff between

the two biggest economies of the world, that is the United States of America and China. The

international Monetary Fund further said that it has an expectation that the United States

economy to grow 2.6 per cent in the year 2019, down from 2.9 per cent last year, but up from

the 2.3 per cent it forecast in the month of April (2019 PerthNow). The Federal Reserve

underwent the process of improvement of the prospects for the growth in the United States by

the help of the restricting the plans to keep the interest rates increased. The policies are being

simplified partly in order to offset the economic fallout from the trade wars of the president

of the United States, Donald Trump (Lea, R. 2019). As per the update of the World economic

Outlook, the International Monetary Fund had forced the countries for not using the tariffs in

the place of the negotiations (2019 PerthNow). The World Economic Outlook got update on

Question 1

From the newspaper journal Perth Now, there could be found an accounting issue that

relates to the issue of the International Monetary Fund forecasting sluggish Global Economy.

According to the journal dated 23rd July 2019, the Global Trade tensions and continuation of

the uncertainty are weakening the merits of the world economy, that would be facing a

precarious year ahead as said by the International Monetary Fund (2019 PerthNow). As per

the update of the World economic Outlook, the International Monetary Fund had forced the

countries for not using the tariffs in the place of the negotiations. The World Economic

Outlook got update on this regard that the International Monetary Fund shaped the Global

Forecast issued in the month of April, with an expected growth to hit 3.2 per cent in the year

2020 (2019 PerthNow). As per the declaration of the International Monetary Fund, they are

expecting an expansion of the global economy by a sluggish 3.2 per cent in the year 2019,

down from 3.6 per cent in the year 2018 and from a growth rate of 3.3 per cent it forecasted

for this year back in the month of April. The 189 country lending organisation blamed the

lack lustre growth on the heightened trade tensions and it specifically a war of tariff between

the two biggest economies of the world, that is the United States of America and China. The

international Monetary Fund further said that it has an expectation that the United States

economy to grow 2.6 per cent in the year 2019, down from 2.9 per cent last year, but up from

the 2.3 per cent it forecast in the month of April (2019 PerthNow). The Federal Reserve

underwent the process of improvement of the prospects for the growth in the United States by

the help of the restricting the plans to keep the interest rates increased. The policies are being

simplified partly in order to offset the economic fallout from the trade wars of the president

of the United States, Donald Trump (Lea, R. 2019). As per the update of the World economic

Outlook, the International Monetary Fund had forced the countries for not using the tariffs in

the place of the negotiations (2019 PerthNow). The World Economic Outlook got update on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

this regard that the International Monetary Fund shaped the Global Forecast issued in the

month of April, with an expected growth to hit 3.2 per cent in the year 2020. There are wide

expectations from the Federal Reserve to cut the rates at its meeting next week. The

International Monetary Fund expects the nineteen country Eurozone to record the modest1.3

per cent growth this year. The main target of the trade actions of the United States is China.

China had already been facing a slowdown. However, according to the reports, the negative

impacts of escalating the tariffs and sapping the external demand have added pressure. A

sudden slowdown in China is a key risk to the economy of the world. There has been a

caution from the side of the International Monetary Fund. There are plenty of triggers that are

potent for the situation to quickly turn negative that is inclusive of the possibilities of more

United States tariffs on China or on the European autos and a no deal Brexit and high levels

of debt in many countries (2019 PerthNow). The international Monetary Fund further said

that it has an expectation that the United States economy to grow 2.6 per cent in the year

2019, down from 2.9 per cent last year, but up from the 2.3 per cent it forecast in the month

of April (2019 PerthNow). The Federal Reserve underwent the process of improvement of the

prospects for the growth in the United States by the help of the restricting the plans to keep

the interest rates increased (Mughal, R. A. 2019). The current forecast was again full of

downgrades with small downward revisions for Germany and Japan. However, larger cracks

for Brazil, Mexico, Russia, India and South Africa (2019 PerthNow). They are the countries

that were the engines for the international growth in the rise of the 2008 financial crisis. The

International Monetary Fund again put emphasis on the resolution of the uncertainty that

remains the most stagnating issue for the global economy and said Government authorities

should avoid the policy missteps that would be having a deliberate impact on the emotions,

growth and the creation of the job (2019 PerthNow). In the reports it was said, “countries

should not use tariffs to target bilateral trade balances.” The President of the United States Mr

this regard that the International Monetary Fund shaped the Global Forecast issued in the

month of April, with an expected growth to hit 3.2 per cent in the year 2020. There are wide

expectations from the Federal Reserve to cut the rates at its meeting next week. The

International Monetary Fund expects the nineteen country Eurozone to record the modest1.3

per cent growth this year. The main target of the trade actions of the United States is China.

China had already been facing a slowdown. However, according to the reports, the negative

impacts of escalating the tariffs and sapping the external demand have added pressure. A

sudden slowdown in China is a key risk to the economy of the world. There has been a

caution from the side of the International Monetary Fund. There are plenty of triggers that are

potent for the situation to quickly turn negative that is inclusive of the possibilities of more

United States tariffs on China or on the European autos and a no deal Brexit and high levels

of debt in many countries (2019 PerthNow). The international Monetary Fund further said

that it has an expectation that the United States economy to grow 2.6 per cent in the year

2019, down from 2.9 per cent last year, but up from the 2.3 per cent it forecast in the month

of April (2019 PerthNow). The Federal Reserve underwent the process of improvement of the

prospects for the growth in the United States by the help of the restricting the plans to keep

the interest rates increased (Mughal, R. A. 2019). The current forecast was again full of

downgrades with small downward revisions for Germany and Japan. However, larger cracks

for Brazil, Mexico, Russia, India and South Africa (2019 PerthNow). They are the countries

that were the engines for the international growth in the rise of the 2008 financial crisis. The

International Monetary Fund again put emphasis on the resolution of the uncertainty that

remains the most stagnating issue for the global economy and said Government authorities

should avoid the policy missteps that would be having a deliberate impact on the emotions,

growth and the creation of the job (2019 PerthNow). In the reports it was said, “countries

should not use tariffs to target bilateral trade balances.” The President of the United States Mr

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Donald Trump and the president of China Xi Jinping in the month of June agreed to an

understanding in their trade hostilities. Several senior officials from Beijing and Washington

had taken two phone calls in the current weeks (2019 PerthNow). However, they had no face

to face meetings that have been scheduled. The International Monetary Fund expects the

nineteen country Eurozone to record the modest1.3 per cent growth this year. The main target

of the trade actions of the United states is China (Guide, G. P. 2019). China had already been

facing a slowdown. However, according to the reports, the negative impacts of escalating the

tariffs and sapping the external demand have added pressure. A sudden slowdown in China is

a key risk to the economy of the world. There has been a caution from the side of the

International Monetary Fund, that there is plenty of triggers (Palley, T. 2019). They are

potent for the situation to quickly turn negative that is inclusive of the possibilities of more

United States tariffs on China or on the European autos and a no deal Brexit and high levels

of debt in many countries (2019 PerthNow). The international Monetary Fund further said

that it has an expectation that the United States economy to grow 2.6 per cent in the year

2019, down from 2.9 per cent last year, but up from the 2.3 per cent it forecast in the month

of April. The Federal Reserve underwent the process of improvement of the prospects for the

growth in the United States by the help of the restricting the plans to keep the interest rates

increased (2019 PerthNow). The International Monetary Fund also added that some major

economies that are inclusive of China and Germany might be in need of taking short term

actions to increase the growth and which a severe downturn would be requiring stimulus

measures that are well coordinated (Kent, C. 2019). The International Monetary Fund further

said that it still has expectations that a steep slowdown in the Europe and some rising market

economies will be giving way to the general reboost in the second half of the year

(2019 PerthNow). However the chances of further cracks to the site are very high is what was

said by the International Monetary Fund. the International Monetary Fund and the World

Donald Trump and the president of China Xi Jinping in the month of June agreed to an

understanding in their trade hostilities. Several senior officials from Beijing and Washington

had taken two phone calls in the current weeks (2019 PerthNow). However, they had no face

to face meetings that have been scheduled. The International Monetary Fund expects the

nineteen country Eurozone to record the modest1.3 per cent growth this year. The main target

of the trade actions of the United states is China (Guide, G. P. 2019). China had already been

facing a slowdown. However, according to the reports, the negative impacts of escalating the

tariffs and sapping the external demand have added pressure. A sudden slowdown in China is

a key risk to the economy of the world. There has been a caution from the side of the

International Monetary Fund, that there is plenty of triggers (Palley, T. 2019). They are

potent for the situation to quickly turn negative that is inclusive of the possibilities of more

United States tariffs on China or on the European autos and a no deal Brexit and high levels

of debt in many countries (2019 PerthNow). The international Monetary Fund further said

that it has an expectation that the United States economy to grow 2.6 per cent in the year

2019, down from 2.9 per cent last year, but up from the 2.3 per cent it forecast in the month

of April. The Federal Reserve underwent the process of improvement of the prospects for the

growth in the United States by the help of the restricting the plans to keep the interest rates

increased (2019 PerthNow). The International Monetary Fund also added that some major

economies that are inclusive of China and Germany might be in need of taking short term

actions to increase the growth and which a severe downturn would be requiring stimulus

measures that are well coordinated (Kent, C. 2019). The International Monetary Fund further

said that it still has expectations that a steep slowdown in the Europe and some rising market

economies will be giving way to the general reboost in the second half of the year

(2019 PerthNow). However the chances of further cracks to the site are very high is what was

said by the International Monetary Fund. the International Monetary Fund and the World

5CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Bank are taking the charge to hold the spring meetings in Washington this week. The

International Monetary Fund chief Economist also said that a steep weakening might be

requiring a well synced fiscal stimulus across the economies and loose the monetary policy

(2019 PerthNow). The Federal Reserve underwent the process of improvement of the

prospects for the growth in the United States by the help of the restricting the plans to keep

the interest rates increased (2019 PerthNow). The International Monetary Fund also added

that some major economies that are inclusive of China and Germany might be in need of

taking short term actions to increase the growth and which a severe downturn would be

requiring stimulus measures that are well coordinated (2019 PerthNow). The International

Monetary Fund further said that it still has expectations that a steep slowdown in the Europe

and some rising market economies will be giving way to the general reboost in the second

half of the year. However the chances of further cracks to the site are very high is what was

said by the International Monetary Fund. the International Monetary Fund and the World

Bank are taking the charge to hold the spring meetings in Washington this week. The

International Monetary Fund chief Economist also said that a steep weakening might be

requiring a well synced fiscal stimulus across the economies and loose the monetary policy

(2019 PerthNow).

Question 2

Major issues covered in the exposure draft

The IASB exposure draft mainly focuses on the proposing amendments resulting in

occurrence to the preparation for the company’s amendments relating to both of the IFRS 9

as well as IAS 39. The exposure draft discusses on the variance of different sort of

uncertainty arising which is caused due to changes in benchmarks associating of the market

interest rates on the requirements causing in due to the risk in cash flow occurrences. It is also

focused in the flow of hedges and it determine about the case of designated risk which is

Bank are taking the charge to hold the spring meetings in Washington this week. The

International Monetary Fund chief Economist also said that a steep weakening might be

requiring a well synced fiscal stimulus across the economies and loose the monetary policy

(2019 PerthNow). The Federal Reserve underwent the process of improvement of the

prospects for the growth in the United States by the help of the restricting the plans to keep

the interest rates increased (2019 PerthNow). The International Monetary Fund also added

that some major economies that are inclusive of China and Germany might be in need of

taking short term actions to increase the growth and which a severe downturn would be

requiring stimulus measures that are well coordinated (2019 PerthNow). The International

Monetary Fund further said that it still has expectations that a steep slowdown in the Europe

and some rising market economies will be giving way to the general reboost in the second

half of the year. However the chances of further cracks to the site are very high is what was

said by the International Monetary Fund. the International Monetary Fund and the World

Bank are taking the charge to hold the spring meetings in Washington this week. The

International Monetary Fund chief Economist also said that a steep weakening might be

requiring a well synced fiscal stimulus across the economies and loose the monetary policy

(2019 PerthNow).

Question 2

Major issues covered in the exposure draft

The IASB exposure draft mainly focuses on the proposing amendments resulting in

occurrence to the preparation for the company’s amendments relating to both of the IFRS 9

as well as IAS 39. The exposure draft discusses on the variance of different sort of

uncertainty arising which is caused due to changes in benchmarks associating of the market

interest rates on the requirements causing in due to the risk in cash flow occurrences. It is also

focused in the flow of hedges and it determine about the case of designated risk which is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

being practiced in the current scenario in association of the cash flow. The fair value hedges

in association to the market level are being discussed in the draft in order to finalize the

amendment for beginning the work on the second phase in recognition to it. The draft also

express concern about the lack of clarity in application to the retrospective hedging

effectiveness, it also focuses on the part of measurement in the version of hedging in

effectiveness in the market association.

Lastly, it mainly discusses on the scenario about the amount of deferred cash flow of

the hedging reserve and it is required to be classified in the effect of profit and loss entity that

is being ceases by applying the amendment structure.

Outline of the view in exposure draft

In the aspect of the agreement for the function of exposure draft it is considered to be

supportive in focusing on the aspect of exceptions which is being provided for exploring

higher probabilistic criterions and also functioning for the hedging effectiveness considering

the assessment. However, it is being considered as the relevant structure for agreeing on the

course of agreement, cash flow hedging and fair value hedging for incurring the issue of

contractual hedging and non-contractual hedging is disclosed on the preference in order to

estimate and measuring the time period. It is also being done by referring the time for

associating the hedging techniques and focusing the measurement by replacing with the

constitution of the risk-free rates. There are different sort of reasoning out the disagreements

in associating with the market players in the company. The financial officers always try to get

into newer sources of constitutional effects in order to review the problems that are being

faced by them and they deserve to change the amendment of the financial benchmarks rates

to affect the marketers to use the things very easily and to undergo with large complexion.

Frequency by which it is being considered is redesigned with various sources of dynamic

being practiced in the current scenario in association of the cash flow. The fair value hedges

in association to the market level are being discussed in the draft in order to finalize the

amendment for beginning the work on the second phase in recognition to it. The draft also

express concern about the lack of clarity in application to the retrospective hedging

effectiveness, it also focuses on the part of measurement in the version of hedging in

effectiveness in the market association.

Lastly, it mainly discusses on the scenario about the amount of deferred cash flow of

the hedging reserve and it is required to be classified in the effect of profit and loss entity that

is being ceases by applying the amendment structure.

Outline of the view in exposure draft

In the aspect of the agreement for the function of exposure draft it is considered to be

supportive in focusing on the aspect of exceptions which is being provided for exploring

higher probabilistic criterions and also functioning for the hedging effectiveness considering

the assessment. However, it is being considered as the relevant structure for agreeing on the

course of agreement, cash flow hedging and fair value hedging for incurring the issue of

contractual hedging and non-contractual hedging is disclosed on the preference in order to

estimate and measuring the time period. It is also being done by referring the time for

associating the hedging techniques and focusing the measurement by replacing with the

constitution of the risk-free rates. There are different sort of reasoning out the disagreements

in associating with the market players in the company. The financial officers always try to get

into newer sources of constitutional effects in order to review the problems that are being

faced by them and they deserve to change the amendment of the financial benchmarks rates

to affect the marketers to use the things very easily and to undergo with large complexion.

Frequency by which it is being considered is redesigned with various sources of dynamic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

hedging and there are some instances where IFRS do not permit the entity to use it for every

resource.

Comment for the purpose of exception which is being identified in the purpose of

uncertainty in relation to the benchmark of the application of interest rate. Several instances

are being focused to apply in order to hedging the purpose. These are referred as the

disagreements where uncertainty is regarded in relation to the assessment of it. There are

different sort if risk that is being associative to it in regard of the pre-reform benchmark of

the forecasting values regarding to it. The disagreement is also concluded due to the floating

issue debt in the current market with a remaining of five years. It is applied because it is

currently focused on hedging with the effective receive of IBOR-pay fixed rate in relation of

the associative skills aggregated to the requirement of market. Cash flow hedging in relation

to the accounting relationship focusing on the variable cash flows of the hedging item is

usually not being effected with uncertainty for the replacing of the next two years. The

effectiveness associated with replacement associative with existence for the respect of

performing the hedging efficiencies (Drechsler,. Savov & Schnabl, 2019). Disagreements are

caused due to optimal uncertainty in the financial resources operating in the market.

However, the amendments which is being associated are usually ceased to apply for

the arising of benchmark rates which are no longer been associated for neither the hedging

instrument nor the hedged item, the requirement in support of hedged item stands to be

uncertainty process for being the higher probable forecasting cash flows of the hedging risk.

Certain proposals are referred to disagreement hedging relationships which is being affected

by reformation of the accounting standards relating to the meaningful information. The

amount of the adjustment that is being stated as the persuasive impact of the reform.

hedging and there are some instances where IFRS do not permit the entity to use it for every

resource.

Comment for the purpose of exception which is being identified in the purpose of

uncertainty in relation to the benchmark of the application of interest rate. Several instances

are being focused to apply in order to hedging the purpose. These are referred as the

disagreements where uncertainty is regarded in relation to the assessment of it. There are

different sort if risk that is being associative to it in regard of the pre-reform benchmark of

the forecasting values regarding to it. The disagreement is also concluded due to the floating

issue debt in the current market with a remaining of five years. It is applied because it is

currently focused on hedging with the effective receive of IBOR-pay fixed rate in relation of

the associative skills aggregated to the requirement of market. Cash flow hedging in relation

to the accounting relationship focusing on the variable cash flows of the hedging item is

usually not being effected with uncertainty for the replacing of the next two years. The

effectiveness associated with replacement associative with existence for the respect of

performing the hedging efficiencies (Drechsler,. Savov & Schnabl, 2019). Disagreements are

caused due to optimal uncertainty in the financial resources operating in the market.

However, the amendments which is being associated are usually ceased to apply for

the arising of benchmark rates which are no longer been associated for neither the hedging

instrument nor the hedged item, the requirement in support of hedged item stands to be

uncertainty process for being the higher probable forecasting cash flows of the hedging risk.

Certain proposals are referred to disagreement hedging relationships which is being affected

by reformation of the accounting standards relating to the meaningful information. The

amount of the adjustment that is being stated as the persuasive impact of the reform.

8CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Analysis of the arguments

In the context of effective date and transition condition based in the paragraph of

BC45-BC47 it is explained that the board is purposed of the amendments that is being made

with standing of effective date for the annual period that is starting from January 1, 2020. The

consideration of the earlier application that is being given permission which is being given to

the board of directors retrospectively. The specific transition, which is being given out in the

market, is being proposed by the provision. However, the comment is considered supportive

for the conditions of accepting the amendments issued by the structural body (Gobet.,

Pimentel., & Warin, 2019). The amendments are considered to be applied successfully in

every context for the consideration of entity being reinstated successfully. There are situation

which is referred in respecting to the exceptions as it is being proposed for highly criterion

and also prospective type of hedging concept. As there are differences between contractual

and the other is non-contractual type of cash flow, hedges, which are being issued for the

interbank rates in order to estimate cash flow risk. However, the approach is not perfect in

relation of what is to be achieved for the proposal to be prepared.

However, there are instances where comment letters are issued in against of the

regulation. It gently, justifies the measurements that consists interest rate benchmarks. The

rates are considered quite higher in nature (PsycNET., 2019). This is the main reason where

marketers are not even satisfied of the implementation occurred, rising amount of interest

rates create a huge problem for the investors who are dealing with the investment in the

market. The measurement of ineffectiveness in the market that is being solicited with the

effective return in the cash flow hedging. Prospective test of hedging is underwent by the

officials to undergo and the design which is being performed by them to render effectiveness

for the forthcoming season (Brehmer et al., 2018). The application of them in order to satisfy

the needs of clients in the market are performed most effectively and it is however generates

Analysis of the arguments

In the context of effective date and transition condition based in the paragraph of

BC45-BC47 it is explained that the board is purposed of the amendments that is being made

with standing of effective date for the annual period that is starting from January 1, 2020. The

consideration of the earlier application that is being given permission which is being given to

the board of directors retrospectively. The specific transition, which is being given out in the

market, is being proposed by the provision. However, the comment is considered supportive

for the conditions of accepting the amendments issued by the structural body (Gobet.,

Pimentel., & Warin, 2019). The amendments are considered to be applied successfully in

every context for the consideration of entity being reinstated successfully. There are situation

which is referred in respecting to the exceptions as it is being proposed for highly criterion

and also prospective type of hedging concept. As there are differences between contractual

and the other is non-contractual type of cash flow, hedges, which are being issued for the

interbank rates in order to estimate cash flow risk. However, the approach is not perfect in

relation of what is to be achieved for the proposal to be prepared.

However, there are instances where comment letters are issued in against of the

regulation. It gently, justifies the measurements that consists interest rate benchmarks. The

rates are considered quite higher in nature (PsycNET., 2019). This is the main reason where

marketers are not even satisfied of the implementation occurred, rising amount of interest

rates create a huge problem for the investors who are dealing with the investment in the

market. The measurement of ineffectiveness in the market that is being solicited with the

effective return in the cash flow hedging. Prospective test of hedging is underwent by the

officials to undergo and the design which is being performed by them to render effectiveness

for the forthcoming season (Brehmer et al., 2018). The application of them in order to satisfy

the needs of clients in the market are performed most effectively and it is however generates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

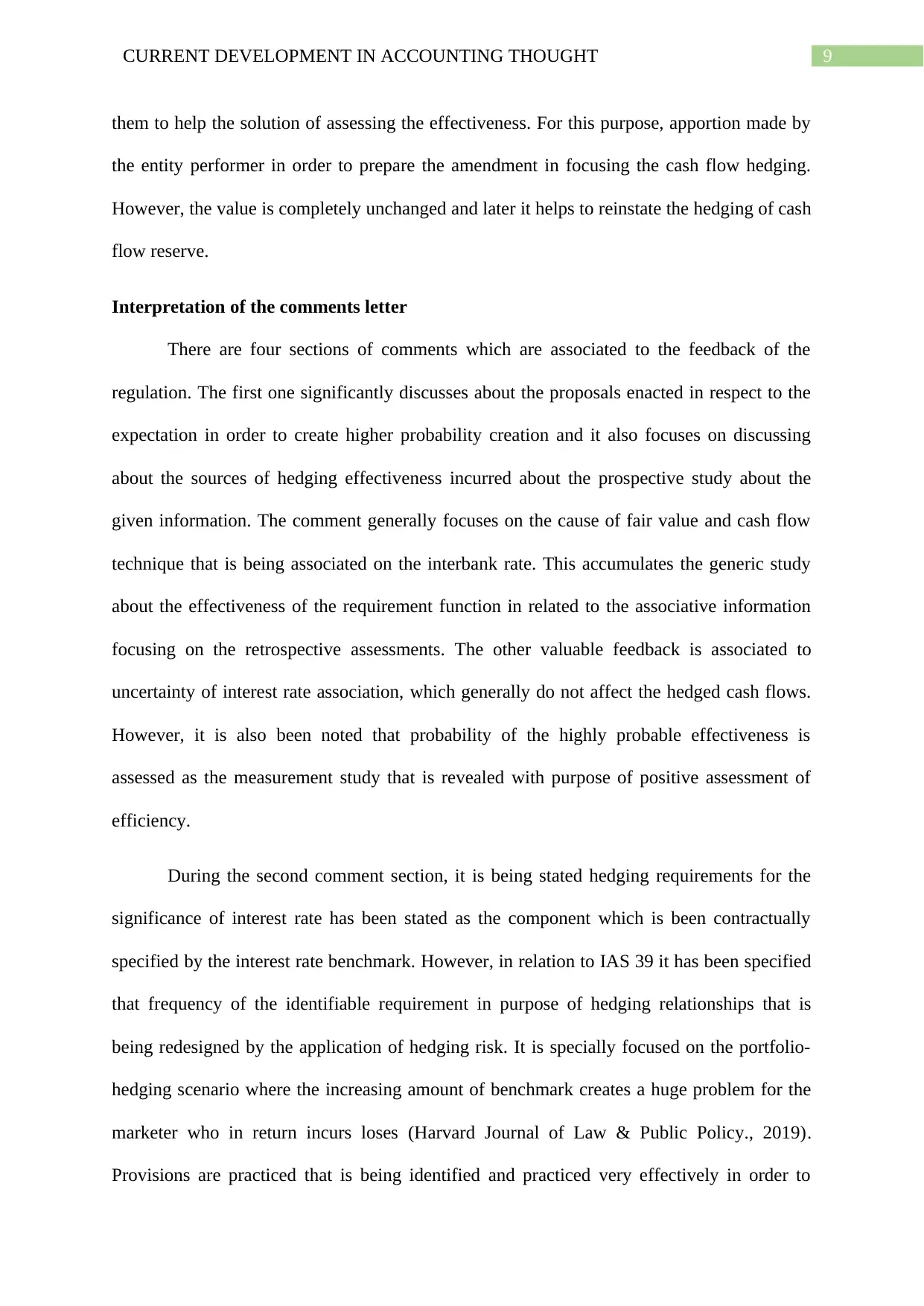

them to help the solution of assessing the effectiveness. For this purpose, apportion made by

the entity performer in order to prepare the amendment in focusing the cash flow hedging.

However, the value is completely unchanged and later it helps to reinstate the hedging of cash

flow reserve.

Interpretation of the comments letter

There are four sections of comments which are associated to the feedback of the

regulation. The first one significantly discusses about the proposals enacted in respect to the

expectation in order to create higher probability creation and it also focuses on discussing

about the sources of hedging effectiveness incurred about the prospective study about the

given information. The comment generally focuses on the cause of fair value and cash flow

technique that is being associated on the interbank rate. This accumulates the generic study

about the effectiveness of the requirement function in related to the associative information

focusing on the retrospective assessments. The other valuable feedback is associated to

uncertainty of interest rate association, which generally do not affect the hedged cash flows.

However, it is also been noted that probability of the highly probable effectiveness is

assessed as the measurement study that is revealed with purpose of positive assessment of

efficiency.

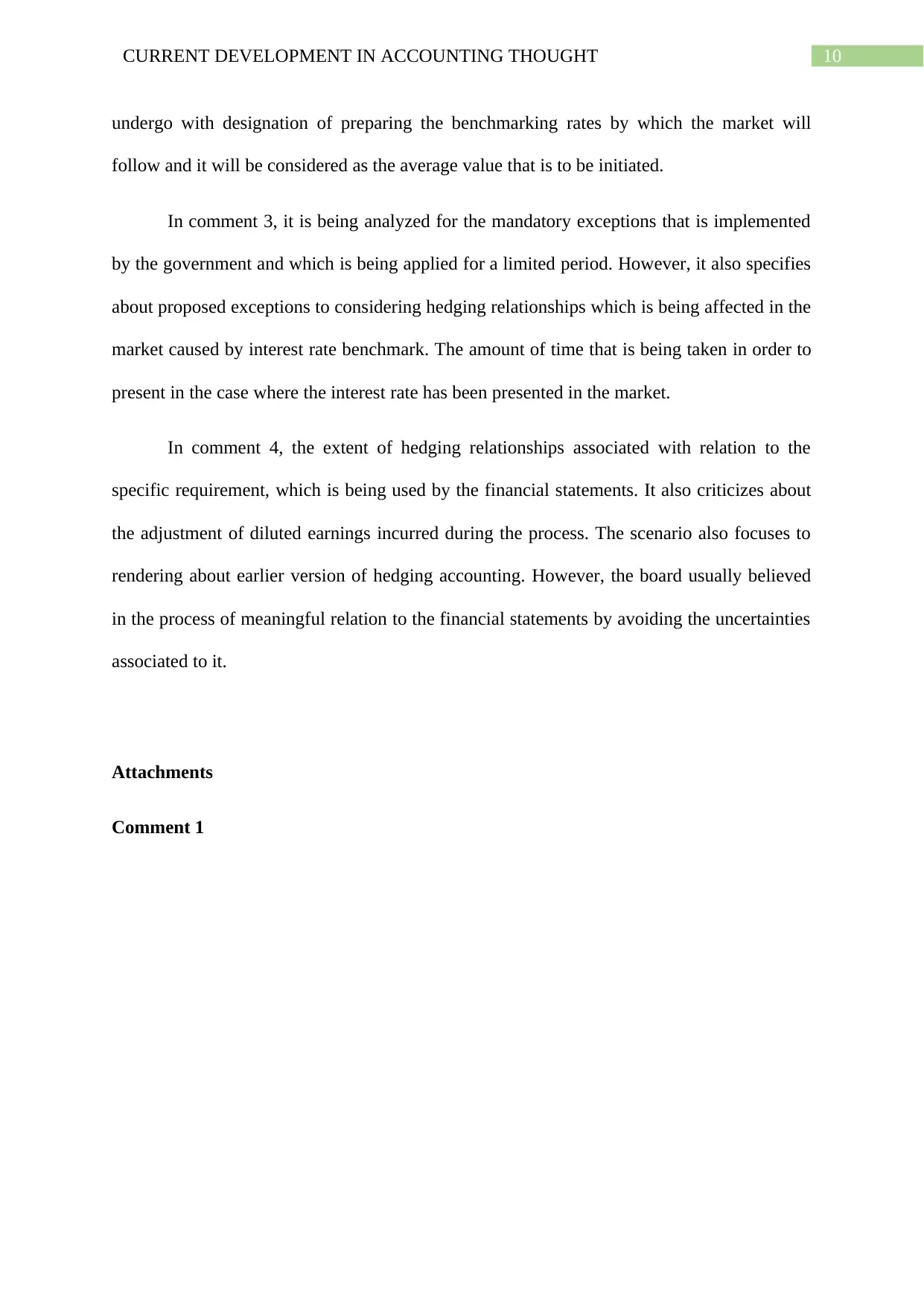

During the second comment section, it is being stated hedging requirements for the

significance of interest rate has been stated as the component which is been contractually

specified by the interest rate benchmark. However, in relation to IAS 39 it has been specified

that frequency of the identifiable requirement in purpose of hedging relationships that is

being redesigned by the application of hedging risk. It is specially focused on the portfolio-

hedging scenario where the increasing amount of benchmark creates a huge problem for the

marketer who in return incurs loses (Harvard Journal of Law & Public Policy., 2019).

Provisions are practiced that is being identified and practiced very effectively in order to

them to help the solution of assessing the effectiveness. For this purpose, apportion made by

the entity performer in order to prepare the amendment in focusing the cash flow hedging.

However, the value is completely unchanged and later it helps to reinstate the hedging of cash

flow reserve.

Interpretation of the comments letter

There are four sections of comments which are associated to the feedback of the

regulation. The first one significantly discusses about the proposals enacted in respect to the

expectation in order to create higher probability creation and it also focuses on discussing

about the sources of hedging effectiveness incurred about the prospective study about the

given information. The comment generally focuses on the cause of fair value and cash flow

technique that is being associated on the interbank rate. This accumulates the generic study

about the effectiveness of the requirement function in related to the associative information

focusing on the retrospective assessments. The other valuable feedback is associated to

uncertainty of interest rate association, which generally do not affect the hedged cash flows.

However, it is also been noted that probability of the highly probable effectiveness is

assessed as the measurement study that is revealed with purpose of positive assessment of

efficiency.

During the second comment section, it is being stated hedging requirements for the

significance of interest rate has been stated as the component which is been contractually

specified by the interest rate benchmark. However, in relation to IAS 39 it has been specified

that frequency of the identifiable requirement in purpose of hedging relationships that is

being redesigned by the application of hedging risk. It is specially focused on the portfolio-

hedging scenario where the increasing amount of benchmark creates a huge problem for the

marketer who in return incurs loses (Harvard Journal of Law & Public Policy., 2019).

Provisions are practiced that is being identified and practiced very effectively in order to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

undergo with designation of preparing the benchmarking rates by which the market will

follow and it will be considered as the average value that is to be initiated.

In comment 3, it is being analyzed for the mandatory exceptions that is implemented

by the government and which is being applied for a limited period. However, it also specifies

about proposed exceptions to considering hedging relationships which is being affected in the

market caused by interest rate benchmark. The amount of time that is being taken in order to

present in the case where the interest rate has been presented in the market.

In comment 4, the extent of hedging relationships associated with relation to the

specific requirement, which is being used by the financial statements. It also criticizes about

the adjustment of diluted earnings incurred during the process. The scenario also focuses to

rendering about earlier version of hedging accounting. However, the board usually believed

in the process of meaningful relation to the financial statements by avoiding the uncertainties

associated to it.

Attachments

Comment 1

undergo with designation of preparing the benchmarking rates by which the market will

follow and it will be considered as the average value that is to be initiated.

In comment 3, it is being analyzed for the mandatory exceptions that is implemented

by the government and which is being applied for a limited period. However, it also specifies

about proposed exceptions to considering hedging relationships which is being affected in the

market caused by interest rate benchmark. The amount of time that is being taken in order to

present in the case where the interest rate has been presented in the market.

In comment 4, the extent of hedging relationships associated with relation to the

specific requirement, which is being used by the financial statements. It also criticizes about

the adjustment of diluted earnings incurred during the process. The scenario also focuses to

rendering about earlier version of hedging accounting. However, the board usually believed

in the process of meaningful relation to the financial statements by avoiding the uncertainties

associated to it.

Attachments

Comment 1

11CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comment 2

Comment 3

Comment 2

Comment 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.