ACC518 Assignment 2: Current Development in Accounting - Analysis

VerifiedAdded on 2022/11/26

|19

|3170

|191

Report

AI Summary

This report provides a detailed analysis of current developments in accounting, addressing two key questions. Question 1 examines an article from the Australian Financial Review regarding ASIC's scrutiny of Pioneer Credit, analyzing the accounting issues, linking them to relevant theories such as standard setting, theories of regulation, and ethics, and deconstructing the issues through these theoretical lenses. Question 2 delves into an exposure draft by FASB, outlining the major issues covered, identifying areas of agreement and disagreement among stakeholders (including Wells Fargo and William Companies Inc.), and assessing the behavior of regulators using public interest theory. The report critically evaluates the underlying assumptions of the applied theories and perspectives of regulation, providing a comprehensive understanding of the subject matter.

Running head: CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Current development in accounting thoughts

Name of the student

Name of the university

Student ID

Author note

Current development in accounting thoughts

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Table of Contents

Answer to Question 1:................................................................................................................2

Introduction:...............................................................................................................................2

Identification of the issues in the article:...................................................................................2

Linkage between the identified issues and accounting theory:..................................................3

Identification and deconstruction of relevant accounting theories that are consistent with the

issues identified:.........................................................................................................................4

Process of setting standard:........................................................................................................5

Ethics and professionalism in accounting:.................................................................................5

Conclusion:................................................................................................................................6

Answer to Question 2:................................................................................................................7

Major issues covered in exposure draft:.....................................................................................7

Identifying areas of agreement and disagreement in the exposure draft:...................................7

Assessing the behavior of regulator in introducing using public interest theory:....................12

References list:.........................................................................................................................14

Appendix:.................................................................................................................................17

Table of Contents

Answer to Question 1:................................................................................................................2

Introduction:...............................................................................................................................2

Identification of the issues in the article:...................................................................................2

Linkage between the identified issues and accounting theory:..................................................3

Identification and deconstruction of relevant accounting theories that are consistent with the

issues identified:.........................................................................................................................4

Process of setting standard:........................................................................................................5

Ethics and professionalism in accounting:.................................................................................5

Conclusion:................................................................................................................................6

Answer to Question 2:................................................................................................................7

Major issues covered in exposure draft:.....................................................................................7

Identifying areas of agreement and disagreement in the exposure draft:...................................7

Assessing the behavior of regulator in introducing using public interest theory:....................12

References list:.........................................................................................................................14

Appendix:.................................................................................................................................17

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Answer to Question 1:

Introduction:

The study intends to conduct an analysis on the accounting issues reported in one of

the articles that have been published in the Australian financial review. The chosen article for

the analysis purpose is “ASIC kept watch on Pioneer Credit for 12 months which will be

evaluated, analyzed and deconstructed by linking with the accounting theories that have been

studied.

Identification of the issues in the article:

The article takes into account two parties namely regulated which is pioneer credits

and regulator which is ASIC which is a regulator of corporate bodies operating in Australia.

For the period of twelve months, the regulator has kept a watch on the pioneer credits. The

accounting standards of pioneer was investigated because the regulator having doubt on it.

ASIC is entrusted with the responsibility of ensuring that all the corporate bodies strictly

complies with all the regulating requirement in relation to the financial and auditor report of

the company (afr.com, 2019).

Pioneer is a company offering financial services in Australia and since the institution

is a member of Securities of exchange commission of Australia, it is required by them to

make submission of their auditing report to the regulatory body. The article outlines the

concern of ASIC regarding the method of valuation that is used by the pioneer credit. The

whistle blower of the organization informed the regulator about the accounting standards

adopted. In addition to this, the article presents the questions that were asked by ASIUC

regarding the accounting practice of pioneer credit. Furthermore, no information regarding

the accounting requirements and the standards were provided by the pioneer credit and

Answer to Question 1:

Introduction:

The study intends to conduct an analysis on the accounting issues reported in one of

the articles that have been published in the Australian financial review. The chosen article for

the analysis purpose is “ASIC kept watch on Pioneer Credit for 12 months which will be

evaluated, analyzed and deconstructed by linking with the accounting theories that have been

studied.

Identification of the issues in the article:

The article takes into account two parties namely regulated which is pioneer credits

and regulator which is ASIC which is a regulator of corporate bodies operating in Australia.

For the period of twelve months, the regulator has kept a watch on the pioneer credits. The

accounting standards of pioneer was investigated because the regulator having doubt on it.

ASIC is entrusted with the responsibility of ensuring that all the corporate bodies strictly

complies with all the regulating requirement in relation to the financial and auditor report of

the company (afr.com, 2019).

Pioneer is a company offering financial services in Australia and since the institution

is a member of Securities of exchange commission of Australia, it is required by them to

make submission of their auditing report to the regulatory body. The article outlines the

concern of ASIC regarding the method of valuation that is used by the pioneer credit. The

whistle blower of the organization informed the regulator about the accounting standards

adopted. In addition to this, the article presents the questions that were asked by ASIUC

regarding the accounting practice of pioneer credit. Furthermore, no information regarding

the accounting requirements and the standards were provided by the pioneer credit and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

something malevolent was ascertained in the model used by them because of inadequacy in

the disclosure of the same. The details of the process used in the model were not provided in

spite the fact that a qualified audit opinion was given by Pwc. The legitimacy of the method

was protected by employing a tax specialist who argued in favor of the method adopted.

Moreover, the property from one of the directors was leased which indicated the failure of the

method implemented (Marti & Scherer, 2016).

It was claimed by the pioneer credit that they employed a customer friendly method of

collecting debt on the ground that it helps in collaborating with them properly and build good

customer relationship (Marti & Scherer, 2016). However, this was criticized by the customers

who were against this method. Therefore, it is indicative of the fact that pioneer credit was

duping the regulators and customers and failed to comply with the required accounting

standards.

Linkage between the identified issues and accounting theory:

The issues identified in the article can be explained in relation to some of the

accounting theories that have been studied. They are as follows:

Standard setting theory- This theory takes into account the concepts of normative

accounting and positive accounting theory.

Theories of regulation- Some of the regulation theories involve public interest

theory, self interest and capture theory.

Ethics and professionalism theory in accounting- Deontological and teleological

are the theories related to ethics and professionalism (Marginson, 2018).

something malevolent was ascertained in the model used by them because of inadequacy in

the disclosure of the same. The details of the process used in the model were not provided in

spite the fact that a qualified audit opinion was given by Pwc. The legitimacy of the method

was protected by employing a tax specialist who argued in favor of the method adopted.

Moreover, the property from one of the directors was leased which indicated the failure of the

method implemented (Marti & Scherer, 2016).

It was claimed by the pioneer credit that they employed a customer friendly method of

collecting debt on the ground that it helps in collaborating with them properly and build good

customer relationship (Marti & Scherer, 2016). However, this was criticized by the customers

who were against this method. Therefore, it is indicative of the fact that pioneer credit was

duping the regulators and customers and failed to comply with the required accounting

standards.

Linkage between the identified issues and accounting theory:

The issues identified in the article can be explained in relation to some of the

accounting theories that have been studied. They are as follows:

Standard setting theory- This theory takes into account the concepts of normative

accounting and positive accounting theory.

Theories of regulation- Some of the regulation theories involve public interest

theory, self interest and capture theory.

Ethics and professionalism theory in accounting- Deontological and teleological

are the theories related to ethics and professionalism (Marginson, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Identification and deconstruction of relevant accounting theories that are consistent

with the issues identified:

The valuation method employed by the pioneer credit has been of the major concern

for ASIC and this places a great importance on understanding the operation of accounting and

financial regulations in Australia. The accounting bodies are provided with an oversight using

accoun6ing regulation for ensuring that they are complying with the regulations, principle

and practices. It is required by ASIC to ensure that the financial sector operates while

maintaining efficiency and fairness. The public accounting theory helps in explaining the

power, functions and role of ASIC and it is believed by the theory that any regulations

introduced are in the public’s best interest.

Business and companies operating in Australia are required to submit their financial

report to ASIC on an annual basis. It is essential for the companies listed on the stock

exchange to comply with the requirements of the accounting standard along with fulfilling

the criteria of making public disclosure.

It has been ascertained from the analysis of the article that valuation method of

pioneer credit did not adhere to the reporting requirements and the applicable accounting

standards. In spite of the failure of the debt collected methods, the model employed generated

positive and favorable results. The company is restraining from changing its current policy

that has created many issues and this particular behavior of pioneer credit can be explained

with the help of self interest theory (Pülzl & Treib, 2017). This is so because they have the

perception that the company or any organization take actions and step taken only when they

provide benefits.

The financial report of pioneer credit was audited by Pwc and it has been stated by the

auditing company that they did not receive adequate information to make professional

Identification and deconstruction of relevant accounting theories that are consistent

with the issues identified:

The valuation method employed by the pioneer credit has been of the major concern

for ASIC and this places a great importance on understanding the operation of accounting and

financial regulations in Australia. The accounting bodies are provided with an oversight using

accoun6ing regulation for ensuring that they are complying with the regulations, principle

and practices. It is required by ASIC to ensure that the financial sector operates while

maintaining efficiency and fairness. The public accounting theory helps in explaining the

power, functions and role of ASIC and it is believed by the theory that any regulations

introduced are in the public’s best interest.

Business and companies operating in Australia are required to submit their financial

report to ASIC on an annual basis. It is essential for the companies listed on the stock

exchange to comply with the requirements of the accounting standard along with fulfilling

the criteria of making public disclosure.

It has been ascertained from the analysis of the article that valuation method of

pioneer credit did not adhere to the reporting requirements and the applicable accounting

standards. In spite of the failure of the debt collected methods, the model employed generated

positive and favorable results. The company is restraining from changing its current policy

that has created many issues and this particular behavior of pioneer credit can be explained

with the help of self interest theory (Pülzl & Treib, 2017). This is so because they have the

perception that the company or any organization take actions and step taken only when they

provide benefits.

The financial report of pioneer credit was audited by Pwc and it has been stated by the

auditing company that they did not receive adequate information to make professional

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

judgment about the accounting matters and therefore, they could not form a decision on

whether the accounting policies implemented by them were correct or false.

Process of setting standard:

The accounting standards are developed by IFRS which provides the reporting entity

with guidance about reporting and preparation of the financial report. Australian Accounting

Standards Board is the regulatory body that is entrusted with the responsibility of developing

the accounting standard which serves the interest of public. The standards of accounting are

formulated by AASB on one hand and standards are enforced by ASIC on other hand. In

addition to this, the accounting standards at the international level are developed and

formulated by IASB (International accounting standard board) which ensure that the

international standards are in confirmation with the locally developed standards. From the

article, it has been found that pioneer credit is not confirming to the international standards

that has resulted in breaching of the standard and thereby banning the operations of company.

Ethics and professionalism in accounting:

Deontological theory of ethics can help in explaining the questions imposed by ASIC

regarding the method of valuation adopted by pioneer credit. It is their moral obligations

about questioning into the accounting matters of organization. The controversial method of

valuation of Pioneer credit was concluded by the auditors by issuing a qualified audit

opinion. This particular event where auditor has expressed favorable opinion on the valuation

method cab be explained by egoistic theory. In addition to this, the hiring of tax specialist by

pioneer credit for protecting their views can also be considered as acting egoistically. The

failure of Pwc to draw adequate and viable conclusion on the matters of the pioneer credit

was because of the inadequate information provided (Marti & Scherer, 2016). Moreover,

conflict of interest arises because of leasing of property of directors into business.

judgment about the accounting matters and therefore, they could not form a decision on

whether the accounting policies implemented by them were correct or false.

Process of setting standard:

The accounting standards are developed by IFRS which provides the reporting entity

with guidance about reporting and preparation of the financial report. Australian Accounting

Standards Board is the regulatory body that is entrusted with the responsibility of developing

the accounting standard which serves the interest of public. The standards of accounting are

formulated by AASB on one hand and standards are enforced by ASIC on other hand. In

addition to this, the accounting standards at the international level are developed and

formulated by IASB (International accounting standard board) which ensure that the

international standards are in confirmation with the locally developed standards. From the

article, it has been found that pioneer credit is not confirming to the international standards

that has resulted in breaching of the standard and thereby banning the operations of company.

Ethics and professionalism in accounting:

Deontological theory of ethics can help in explaining the questions imposed by ASIC

regarding the method of valuation adopted by pioneer credit. It is their moral obligations

about questioning into the accounting matters of organization. The controversial method of

valuation of Pioneer credit was concluded by the auditors by issuing a qualified audit

opinion. This particular event where auditor has expressed favorable opinion on the valuation

method cab be explained by egoistic theory. In addition to this, the hiring of tax specialist by

pioneer credit for protecting their views can also be considered as acting egoistically. The

failure of Pwc to draw adequate and viable conclusion on the matters of the pioneer credit

was because of the inadequate information provided (Marti & Scherer, 2016). Moreover,

conflict of interest arises because of leasing of property of directors into business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Conclusion:

From the detailed evaluation and analysis of the article, it can be inferred that there

were some of the main issues that were identified in relation to the accounting treatment due

to the employment of particular accounting practice. Such issues have resulted in making

concluding remark of existence of conflict of interest between the ASIC and pioneer credit as

the accounting practices of the latter is not in confirmation with the regulatory standards and

practices of former. In light of this, it can be inferred that in order to avoid such conflict, it is

required by the regulated body to comply with the regulations imposed by regulator. This

would help in reducing the conflict to an acceptable level and seamless running of the

organization.

Conclusion:

From the detailed evaluation and analysis of the article, it can be inferred that there

were some of the main issues that were identified in relation to the accounting treatment due

to the employment of particular accounting practice. Such issues have resulted in making

concluding remark of existence of conflict of interest between the ASIC and pioneer credit as

the accounting practices of the latter is not in confirmation with the regulatory standards and

practices of former. In light of this, it can be inferred that in order to avoid such conflict, it is

required by the regulated body to comply with the regulations imposed by regulator. This

would help in reducing the conflict to an acceptable level and seamless running of the

organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Answer to Question 2:

Major issues covered in exposure draft:

A variety of different exposure drafts were issued by FASB that helps in soliciting

input on the activities of standard setting. The exposure draft covers a considerable number of

issues related to accounting treatment of different accounts such as inventory, goodwill,

financial instruments, and lease improvement for lessors. In one of the proposed amendment

of the disclosure is in relation to the lease accounting by lessor. The issue is about

determination of the fair value of the lessor underlying assets and another issue concerning

this is presentation of cash flow statement for direct financing and sales types of leases.

Another issue that has been pointed is in relation to the income tax that is reclassifying

certain tax effects for accumulated comprehensive income (Rosenbloom, 2016). One

accounting standard that has been proposed is to address the issue of debt classification in the

balance sheet. The accounting standards have been progressed and updated on the scope for

modification accounting and stock compensation. All the accounting concerns were

addressed by requesting the stakeholders to comment on the issued identified and whether

they agree with the proposed updating of the standard. It can be inferred from the analysis of

the exposure draft by FASB that the current provisions of the accounting standard are

addressed using such proposal and updating (Vogel, 2018).

Identifying areas of agreement and disagreement in the exposure draft:

Concerning the proposed accounting treatment and standard in relation to the issues

observed, many reporting entities and accounting firms have expressed their opinion whether

they completely or partially agree with the proposal.

Answer to Question 2:

Major issues covered in exposure draft:

A variety of different exposure drafts were issued by FASB that helps in soliciting

input on the activities of standard setting. The exposure draft covers a considerable number of

issues related to accounting treatment of different accounts such as inventory, goodwill,

financial instruments, and lease improvement for lessors. In one of the proposed amendment

of the disclosure is in relation to the lease accounting by lessor. The issue is about

determination of the fair value of the lessor underlying assets and another issue concerning

this is presentation of cash flow statement for direct financing and sales types of leases.

Another issue that has been pointed is in relation to the income tax that is reclassifying

certain tax effects for accumulated comprehensive income (Rosenbloom, 2016). One

accounting standard that has been proposed is to address the issue of debt classification in the

balance sheet. The accounting standards have been progressed and updated on the scope for

modification accounting and stock compensation. All the accounting concerns were

addressed by requesting the stakeholders to comment on the issued identified and whether

they agree with the proposed updating of the standard. It can be inferred from the analysis of

the exposure draft by FASB that the current provisions of the accounting standard are

addressed using such proposal and updating (Vogel, 2018).

Identifying areas of agreement and disagreement in the exposure draft:

Concerning the proposed accounting treatment and standard in relation to the issues

observed, many reporting entities and accounting firms have expressed their opinion whether

they completely or partially agree with the proposal.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

Wells Fargo 2019:

The update on the proposed accounting standard for leases has received response from

the diversified and community based financial services named Well Fargo. The issue relating

to the determination of fair value for the underlying assets is fully supported by the company.

It is so because under the proposal, the leased pricing would be consistent with the reporting

yield on financing lease because the cost of acquisition is treated as the part of net investment

in the lease. Had such cost were not included, the company would have reported artificially

inflated yield because the delivery cost is triggered due to location of delivery (Fasb.org,

Wells Fargo 2019:

The update on the proposed accounting standard for leases has received response from

the diversified and community based financial services named Well Fargo. The issue relating

to the determination of fair value for the underlying assets is fully supported by the company.

It is so because under the proposal, the leased pricing would be consistent with the reporting

yield on financing lease because the cost of acquisition is treated as the part of net investment

in the lease. Had such cost were not included, the company would have reported artificially

inflated yield because the delivery cost is triggered due to location of delivery (Fasb.org,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

2019). In addition to this, the presentation of cash flow statement is also supported as it

provided decision usefulness to users and is operational and therefore, the company is

actively engaged in adopting the revised standard as it is beneficial to both company and

investors or uses at the same time.

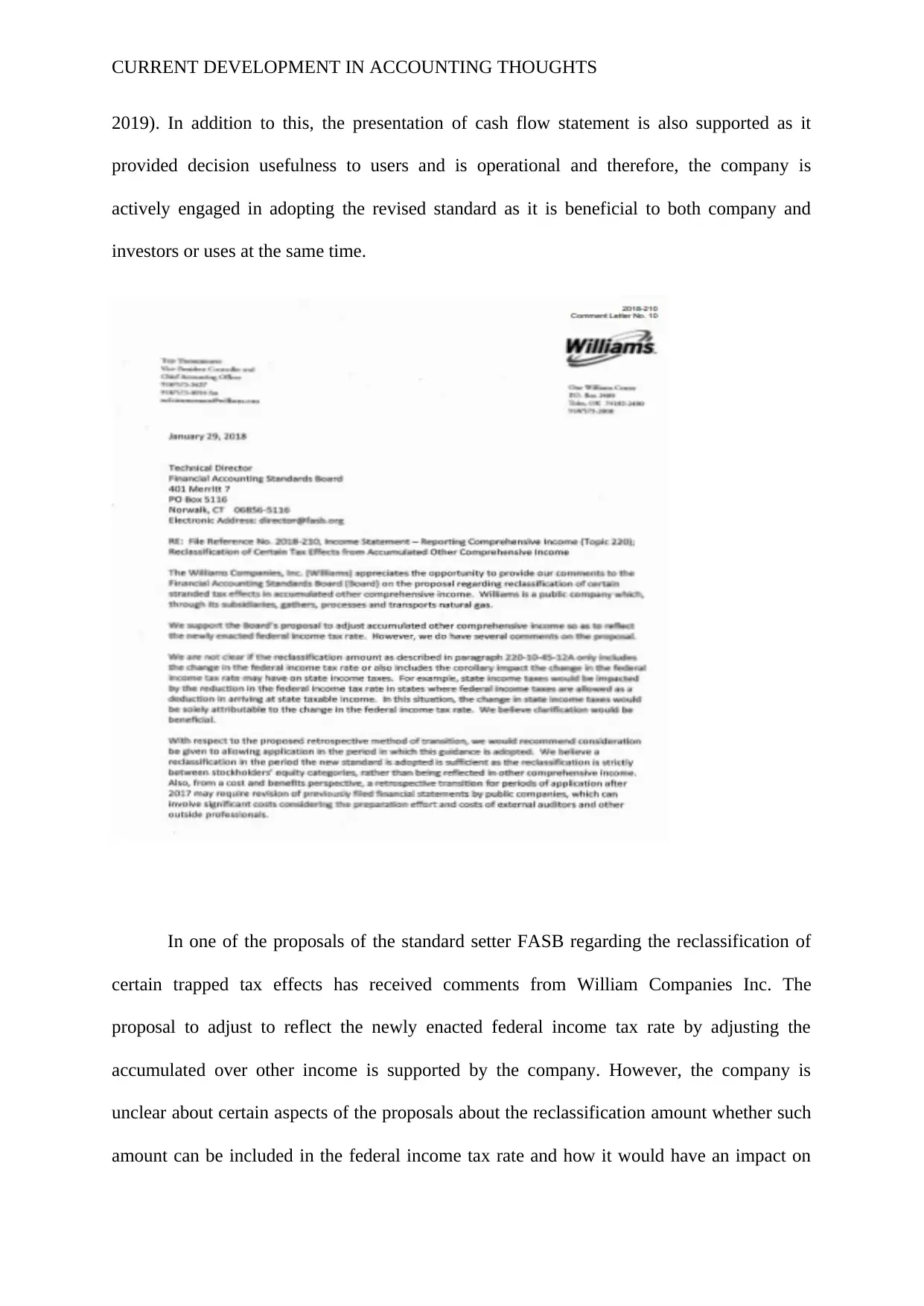

In one of the proposals of the standard setter FASB regarding the reclassification of

certain trapped tax effects has received comments from William Companies Inc. The

proposal to adjust to reflect the newly enacted federal income tax rate by adjusting the

accumulated over other income is supported by the company. However, the company is

unclear about certain aspects of the proposals about the reclassification amount whether such

amount can be included in the federal income tax rate and how it would have an impact on

2019). In addition to this, the presentation of cash flow statement is also supported as it

provided decision usefulness to users and is operational and therefore, the company is

actively engaged in adopting the revised standard as it is beneficial to both company and

investors or uses at the same time.

In one of the proposals of the standard setter FASB regarding the reclassification of

certain trapped tax effects has received comments from William Companies Inc. The

proposal to adjust to reflect the newly enacted federal income tax rate by adjusting the

accumulated over other income is supported by the company. However, the company is

unclear about certain aspects of the proposals about the reclassification amount whether such

amount can be included in the federal income tax rate and how it would have an impact on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

the state income taxes (Fasb.org, 2019). Furthermore, it is also believed by the company that

reclassification for the new adopted standard is sufficient because it is strictly in the

categories of equity stockholder.

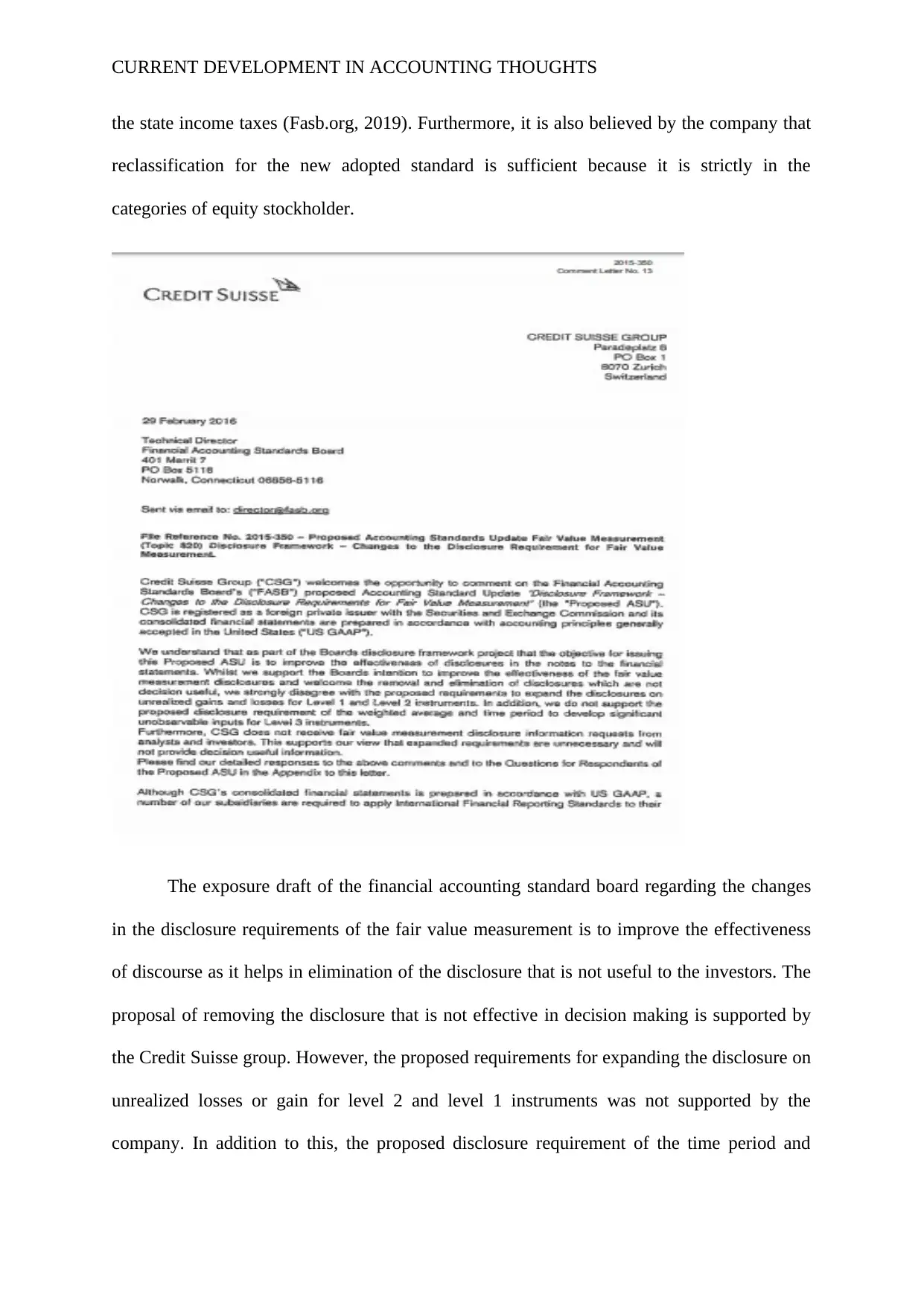

The exposure draft of the financial accounting standard board regarding the changes

in the disclosure requirements of the fair value measurement is to improve the effectiveness

of discourse as it helps in elimination of the disclosure that is not useful to the investors. The

proposal of removing the disclosure that is not effective in decision making is supported by

the Credit Suisse group. However, the proposed requirements for expanding the disclosure on

unrealized losses or gain for level 2 and level 1 instruments was not supported by the

company. In addition to this, the proposed disclosure requirement of the time period and

the state income taxes (Fasb.org, 2019). Furthermore, it is also believed by the company that

reclassification for the new adopted standard is sufficient because it is strictly in the

categories of equity stockholder.

The exposure draft of the financial accounting standard board regarding the changes

in the disclosure requirements of the fair value measurement is to improve the effectiveness

of discourse as it helps in elimination of the disclosure that is not useful to the investors. The

proposal of removing the disclosure that is not effective in decision making is supported by

the Credit Suisse group. However, the proposed requirements for expanding the disclosure on

unrealized losses or gain for level 2 and level 1 instruments was not supported by the

company. In addition to this, the proposed disclosure requirement of the time period and

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHTS

weighted average to develop the observable input for level 3 instruments has not been

supported by the company. The company has also expressed their concern about the

divergence of board with the disclosure requirements that are substantially converged

between IFRS 13 and topic 820 (Fasb.org, 2019).

weighted average to develop the observable input for level 3 instruments has not been

supported by the company. The company has also expressed their concern about the

divergence of board with the disclosure requirements that are substantially converged

between IFRS 13 and topic 820 (Fasb.org, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.