Accounting and Finance for Decision Making: Dividend Policy Analysis

VerifiedAdded on 2022/10/14

|12

|3227

|411

Homework Assignment

AI Summary

This assignment analyzes the dividend policy of Scommine Company, a major electricity provider, in response to a government announcement regarding environmental regulations. The analysis evaluates the market reaction to the announcement, which negatively impacted the company's share price due to anticipated costs of compliance. The assignment then assesses three dividend strategies: paying a cash dividend, paying no dividend, and declaring a scrip dividend. The analysis includes calculations for each strategy, considering the impact on shareholders and the company's financial position. The discussion delves into the arguments for and against the relevancy of dividend policy, exploring models like the Walter model and Modigliani-Miller model. The conclusion recommends a scrip dividend strategy as the most beneficial option, balancing investor needs with the company's financial constraints and compliance requirements. The paper emphasizes the importance of dividend policy in financial decision-making and its effect on share price performance.

Running head: ACCOUNTING AND FINANCE FOR DECISION MAKING

Accounting and Finance for Decision Making

Name of the Student:

Name of the University:

Authors Note:

Accounting and Finance for Decision Making

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE FOR DECISION MAKING

Table of Contents

Introduction:...............................................................................................................................2

a. Evaluating the market reaction to the government announcement:.......................................2

b. Evaluating each of dividend strategies:..................................................................................3

c. Discussing the argument for the relevancy and irrelevancy of dividend policy:...................6

Conclusion:................................................................................................................................8

References and Bibliography:....................................................................................................9

Table of Contents

Introduction:...............................................................................................................................2

a. Evaluating the market reaction to the government announcement:.......................................2

b. Evaluating each of dividend strategies:..................................................................................3

c. Discussing the argument for the relevancy and irrelevancy of dividend policy:...................6

Conclusion:................................................................................................................................8

References and Bibliography:....................................................................................................9

ACCOUNTING AND FINANCE FOR DECISION MAKING

Introduction:

The assessment aims at evaluating the significance of dividend policy, which has been

argued by different researchers all over the world. The report directly evaluates the

significant information’s of the case study that highlights the dividend conditions of

Scommine Company, which are the largest electricity generator and distributor in the country

of Highland. Thus, adequate discussion on the overall announcement from the government is

relatively analyzed for identifying the reaction of the investors on the share price of the

organization. Further evaluation is conducted on the overall different strategies that was

developed by the directors and identify the impact it would hold on the typical shareholder

that has exposure of 120 shares in the organization. Lastly, the adequate arguments are

conducted on the relevancy and irrelevancy of dividend policies that are used for determining

the firm's value. Moreover, the adequate dividend strategy that needs to be implemented by

the company after considering all the relevant factors adequately discussed.

a. Evaluating the market reaction to the government announcement:

The market reaction to the announcement conducted by the government has an

adverse impact on the performance of the company’s share price. The government has mainly

indicated that the electric producing companies need to use environmentally friendly

processes while generating the relevant electricity for the sale. The information delivered by

the government will directly alter the overall production conditions the electric producing

companies, which in turn might initiate high level of cash outflows by the organization. This

announcement came with the deadline, where within the time limit the organizations need to

the improve and develop their current production conditions (Kumar, Kanujiya & Kumar,

2018). Thus, the announcement of the government had negative impact on the share price

moment of Scommine Company, where the share value on the day of the announcement

Introduction:

The assessment aims at evaluating the significance of dividend policy, which has been

argued by different researchers all over the world. The report directly evaluates the

significant information’s of the case study that highlights the dividend conditions of

Scommine Company, which are the largest electricity generator and distributor in the country

of Highland. Thus, adequate discussion on the overall announcement from the government is

relatively analyzed for identifying the reaction of the investors on the share price of the

organization. Further evaluation is conducted on the overall different strategies that was

developed by the directors and identify the impact it would hold on the typical shareholder

that has exposure of 120 shares in the organization. Lastly, the adequate arguments are

conducted on the relevancy and irrelevancy of dividend policies that are used for determining

the firm's value. Moreover, the adequate dividend strategy that needs to be implemented by

the company after considering all the relevant factors adequately discussed.

a. Evaluating the market reaction to the government announcement:

The market reaction to the announcement conducted by the government has an

adverse impact on the performance of the company’s share price. The government has mainly

indicated that the electric producing companies need to use environmentally friendly

processes while generating the relevant electricity for the sale. The information delivered by

the government will directly alter the overall production conditions the electric producing

companies, which in turn might initiate high level of cash outflows by the organization. This

announcement came with the deadline, where within the time limit the organizations need to

the improve and develop their current production conditions (Kumar, Kanujiya & Kumar,

2018). Thus, the announcement of the government had negative impact on the share price

moment of Scommine Company, where the share value on the day of the announcement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE FOR DECISION MAKING

declined from the levels of $2.20 to $1.95. Moreover, after the announcement the company’s

shares have been declining to new lows and is currently trading at the levels of $1.90.

This decline in the share value of Scommine Company was due to the sudden change

in the perspective of the government regarding the environmental conditions of electric

producing companies. This accommodation would have negative impact on their cash

balance, as adequate level of improvements would be required for complying with the new

regulations. Moreover, if the compliance of the movement announcement is not made then

the company would be barred from operating successfully within the organization. Thus, the

information would have negative impact on the performance and financial capability of

Scommine Company. This anticipation of the declining financial performance triggered the

massive selling, which witnessed the decline in share price of the company. Jacob &

Michaely (2017) stated that external factors and policies have direct impact on the share price

performance of the company, as its operation and profitability is hampered due to

government intervention.

b. Evaluating each of dividend strategies:

The board of Scommine Company has directly constructed three dividend strategies

that can be used for adequately reducing the concern for the investors and compensating on

the overall announcement from the government. Dividend policy is considered to be one of

the major attributes of investment that is used by the organizations for effectively improving

their current demand in the capital market. Thus, with the help of dividends the organization

is able to motivate the investors to invest within the organization, which helps in increasing

the share value and market capitalization of the company (Baker & Weigand, 2015). The

adequate analysis of the three different strategies is depicted as follows.

Pay a cash dividend of $200 million:

declined from the levels of $2.20 to $1.95. Moreover, after the announcement the company’s

shares have been declining to new lows and is currently trading at the levels of $1.90.

This decline in the share value of Scommine Company was due to the sudden change

in the perspective of the government regarding the environmental conditions of electric

producing companies. This accommodation would have negative impact on their cash

balance, as adequate level of improvements would be required for complying with the new

regulations. Moreover, if the compliance of the movement announcement is not made then

the company would be barred from operating successfully within the organization. Thus, the

information would have negative impact on the performance and financial capability of

Scommine Company. This anticipation of the declining financial performance triggered the

massive selling, which witnessed the decline in share price of the company. Jacob &

Michaely (2017) stated that external factors and policies have direct impact on the share price

performance of the company, as its operation and profitability is hampered due to

government intervention.

b. Evaluating each of dividend strategies:

The board of Scommine Company has directly constructed three dividend strategies

that can be used for adequately reducing the concern for the investors and compensating on

the overall announcement from the government. Dividend policy is considered to be one of

the major attributes of investment that is used by the organizations for effectively improving

their current demand in the capital market. Thus, with the help of dividends the organization

is able to motivate the investors to invest within the organization, which helps in increasing

the share value and market capitalization of the company (Baker & Weigand, 2015). The

adequate analysis of the three different strategies is depicted as follows.

Pay a cash dividend of $200 million:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE FOR DECISION MAKING

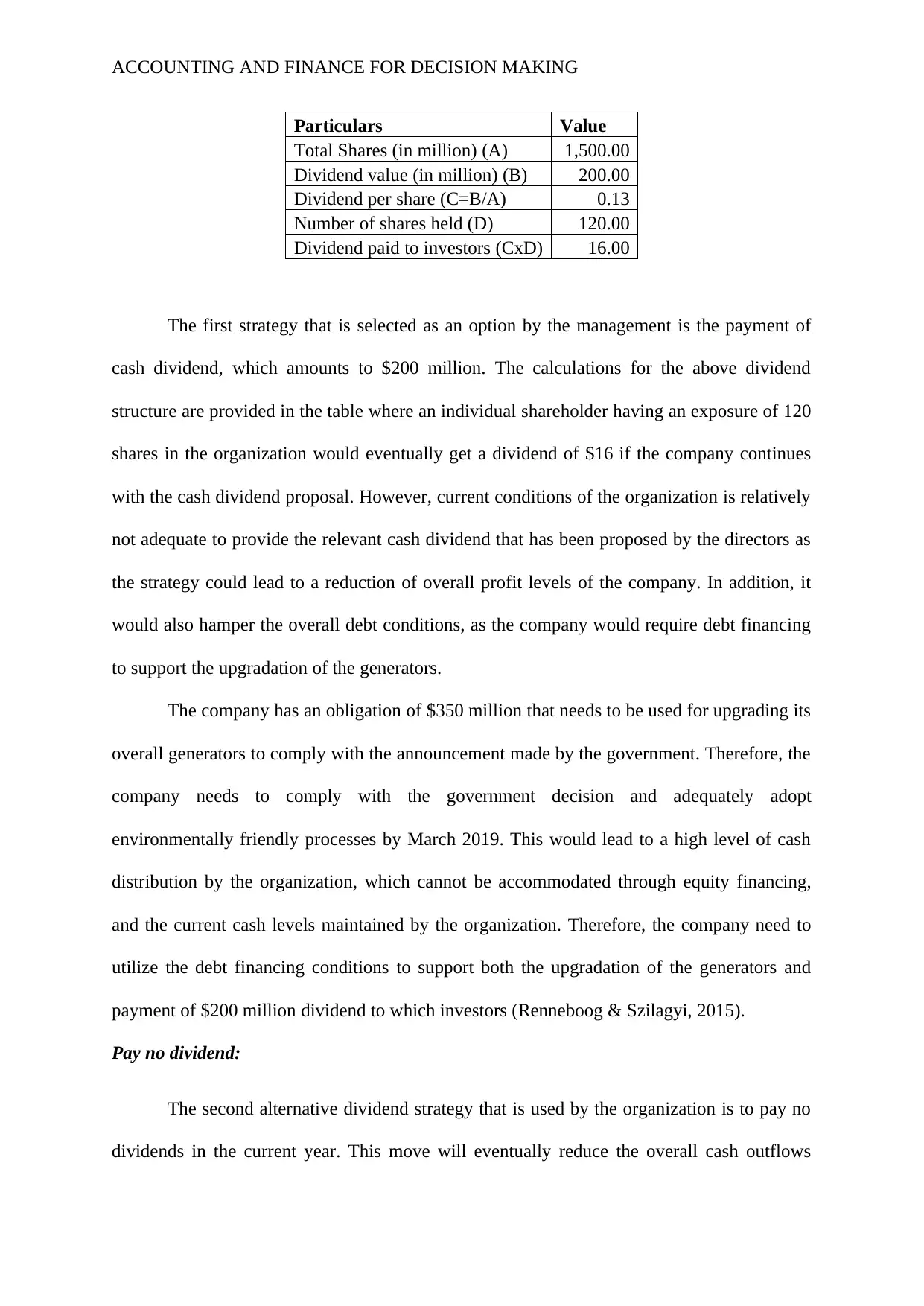

Particulars Value

Total Shares (in million) (A) 1,500.00

Dividend value (in million) (B) 200.00

Dividend per share (C=B/A) 0.13

Number of shares held (D) 120.00

Dividend paid to investors (CxD) 16.00

The first strategy that is selected as an option by the management is the payment of

cash dividend, which amounts to $200 million. The calculations for the above dividend

structure are provided in the table where an individual shareholder having an exposure of 120

shares in the organization would eventually get a dividend of $16 if the company continues

with the cash dividend proposal. However, current conditions of the organization is relatively

not adequate to provide the relevant cash dividend that has been proposed by the directors as

the strategy could lead to a reduction of overall profit levels of the company. In addition, it

would also hamper the overall debt conditions, as the company would require debt financing

to support the upgradation of the generators.

The company has an obligation of $350 million that needs to be used for upgrading its

overall generators to comply with the announcement made by the government. Therefore, the

company needs to comply with the government decision and adequately adopt

environmentally friendly processes by March 2019. This would lead to a high level of cash

distribution by the organization, which cannot be accommodated through equity financing,

and the current cash levels maintained by the organization. Therefore, the company need to

utilize the debt financing conditions to support both the upgradation of the generators and

payment of $200 million dividend to which investors (Renneboog & Szilagyi, 2015).

Pay no dividend:

The second alternative dividend strategy that is used by the organization is to pay no

dividends in the current year. This move will eventually reduce the overall cash outflows

Particulars Value

Total Shares (in million) (A) 1,500.00

Dividend value (in million) (B) 200.00

Dividend per share (C=B/A) 0.13

Number of shares held (D) 120.00

Dividend paid to investors (CxD) 16.00

The first strategy that is selected as an option by the management is the payment of

cash dividend, which amounts to $200 million. The calculations for the above dividend

structure are provided in the table where an individual shareholder having an exposure of 120

shares in the organization would eventually get a dividend of $16 if the company continues

with the cash dividend proposal. However, current conditions of the organization is relatively

not adequate to provide the relevant cash dividend that has been proposed by the directors as

the strategy could lead to a reduction of overall profit levels of the company. In addition, it

would also hamper the overall debt conditions, as the company would require debt financing

to support the upgradation of the generators.

The company has an obligation of $350 million that needs to be used for upgrading its

overall generators to comply with the announcement made by the government. Therefore, the

company needs to comply with the government decision and adequately adopt

environmentally friendly processes by March 2019. This would lead to a high level of cash

distribution by the organization, which cannot be accommodated through equity financing,

and the current cash levels maintained by the organization. Therefore, the company need to

utilize the debt financing conditions to support both the upgradation of the generators and

payment of $200 million dividend to which investors (Renneboog & Szilagyi, 2015).

Pay no dividend:

The second alternative dividend strategy that is used by the organization is to pay no

dividends in the current year. This move will eventually reduce the overall cash outflows

ACCOUNTING AND FINANCE FOR DECISION MAKING

from the company for an amount of $200 million, which is mainly expected by the investors

in April. This mainly indicates that every organization does not pay any kind of dividend to

the investors the overall deteriorating share price of the company from 222 1.9 dollars per

share will shrink more in future due to the nonpayment of adequate dividends to the

investors. Dividend payments are considered to be one of the major attributes, which allows

the organization to deliver more investors and maintain the overall valuation of the share

price.

The nonpayment of adequate dividends to the investors has both advantage and

disadvantage to the organization. One of the major advantages that will be provided to the

organization is the reduction of cash outflows and occur ace of debt financing. This non-

adoption of debt financing would eventually help in improving the solvency conditions of the

company and reduce the overall interest expense that erodes maximum of the profits of the

organization (Al-Najjar & Kilincarslan, 2016). However, the major disadvantage of the

nonpayment of dividend is the decline in the share price of the organization, which has

started after the announcement made by the government. The nonpayment of the dividends

would directly result in the massive selling of shares by the investors who were waiting for

the dividends and value the share price on the basis of dividend payments and growth.

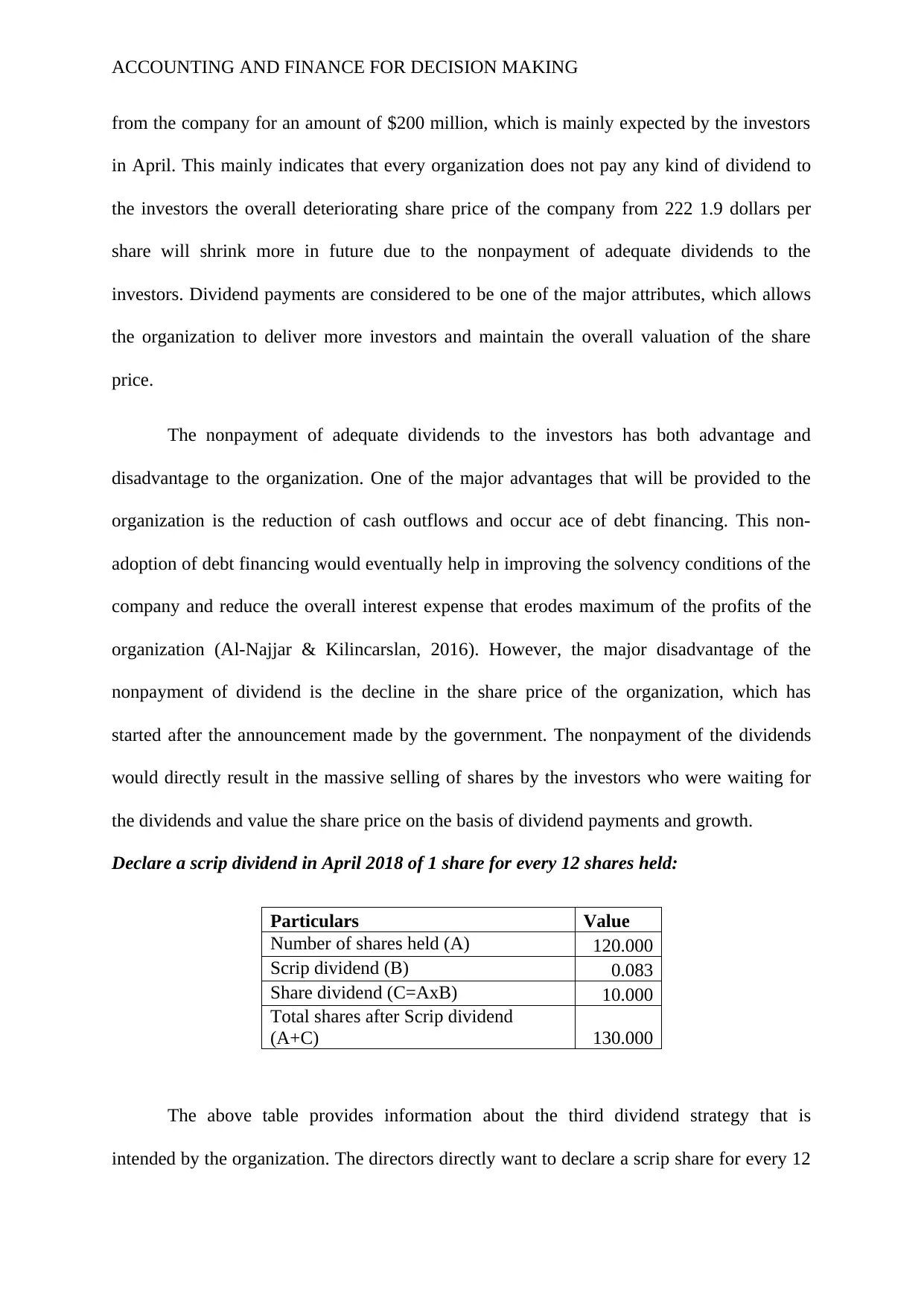

Declare a scrip dividend in April 2018 of 1 share for every 12 shares held:

Particulars Value

Number of shares held (A) 120.000

Scrip dividend (B) 0.083

Share dividend (C=AxB) 10.000

Total shares after Scrip dividend

(A+C) 130.000

The above table provides information about the third dividend strategy that is

intended by the organization. The directors directly want to declare a scrip share for every 12

from the company for an amount of $200 million, which is mainly expected by the investors

in April. This mainly indicates that every organization does not pay any kind of dividend to

the investors the overall deteriorating share price of the company from 222 1.9 dollars per

share will shrink more in future due to the nonpayment of adequate dividends to the

investors. Dividend payments are considered to be one of the major attributes, which allows

the organization to deliver more investors and maintain the overall valuation of the share

price.

The nonpayment of adequate dividends to the investors has both advantage and

disadvantage to the organization. One of the major advantages that will be provided to the

organization is the reduction of cash outflows and occur ace of debt financing. This non-

adoption of debt financing would eventually help in improving the solvency conditions of the

company and reduce the overall interest expense that erodes maximum of the profits of the

organization (Al-Najjar & Kilincarslan, 2016). However, the major disadvantage of the

nonpayment of dividend is the decline in the share price of the organization, which has

started after the announcement made by the government. The nonpayment of the dividends

would directly result in the massive selling of shares by the investors who were waiting for

the dividends and value the share price on the basis of dividend payments and growth.

Declare a scrip dividend in April 2018 of 1 share for every 12 shares held:

Particulars Value

Number of shares held (A) 120.000

Scrip dividend (B) 0.083

Share dividend (C=AxB) 10.000

Total shares after Scrip dividend

(A+C) 130.000

The above table provides information about the third dividend strategy that is

intended by the organization. The directors directly want to declare a scrip share for every 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE FOR DECISION MAKING

shares held by the shareholder. This type of dividend would eventually increase the level of

shares that is currently being floated in the market, as more shares would be provided to the

investors in form of dividends. The analysis of the above table has directly indicated that after

the overall declaration of dividend the overall shares of an individual will increase from 120

to 130. This increment eventually affects the overall valuation of the companies share and

reduces its market capitalization and share price.

Therefore, the continuous decline in the share price after the announcement from the

government would not hold after the dividend declaration, which would result in the erosion

of adequate market capitalization and capability of the company to ensure the investors with

future growth possibilities. However, the overall move of scrip dividend is relatively

beneficial for the investors and organization, as the company will only go through a small

change in their overall operations where the upgradation of the generators would ensure the

legality of their process (Jabbouri, 2016).

The implementation of the script dividend would eventually help the organization to

conduct its overall expenses on the generators while ensuring the investors to provide

adequate level of returns in the next dividend payment cycle. Furthermore, with the help of

the above decision the organization will eventually help to minimize the level of debt

exposure and increase its valuation after the upgradation announcement by the directors.

c. Discussing the argument for the relevancy and irrelevancy of dividend policy:

The relevancy and irrelevancy of the dividend policy have direct impact on the shar

price performance of the organization. Dividend policy of a firm is considered to be the major

factor in shaping the valuation of the organization that is conducted by the investors.

Investors making rely on the relevancy models and irrelevancy models for determining the

share price valuation of the organization. Baker & Jabbouri (2016) stated that investors use

shares held by the shareholder. This type of dividend would eventually increase the level of

shares that is currently being floated in the market, as more shares would be provided to the

investors in form of dividends. The analysis of the above table has directly indicated that after

the overall declaration of dividend the overall shares of an individual will increase from 120

to 130. This increment eventually affects the overall valuation of the companies share and

reduces its market capitalization and share price.

Therefore, the continuous decline in the share price after the announcement from the

government would not hold after the dividend declaration, which would result in the erosion

of adequate market capitalization and capability of the company to ensure the investors with

future growth possibilities. However, the overall move of scrip dividend is relatively

beneficial for the investors and organization, as the company will only go through a small

change in their overall operations where the upgradation of the generators would ensure the

legality of their process (Jabbouri, 2016).

The implementation of the script dividend would eventually help the organization to

conduct its overall expenses on the generators while ensuring the investors to provide

adequate level of returns in the next dividend payment cycle. Furthermore, with the help of

the above decision the organization will eventually help to minimize the level of debt

exposure and increase its valuation after the upgradation announcement by the directors.

c. Discussing the argument for the relevancy and irrelevancy of dividend policy:

The relevancy and irrelevancy of the dividend policy have direct impact on the shar

price performance of the organization. Dividend policy of a firm is considered to be the major

factor in shaping the valuation of the organization that is conducted by the investors.

Investors making rely on the relevancy models and irrelevancy models for determining the

share price valuation of the organization. Baker & Jabbouri (2016) stated that investors use

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE FOR DECISION MAKING

the dividend policy for determining the appropriate level of share price for the organization

and detect whether they are undervalued or overvalued. Dividends are mainly detected as the

portion of the profits that is shared by the organization with their shareholders, which is

considered as the appropriate way of wealth distribution. Therefore, it would be understood

that the decisions of the dividends are a crucial endeavor for the organization, as it might

have direct impact on the share price performance condition of the company.

Therefore, from the relevant evaluation it has been detected that financial managers

utilize the dividend decisions to the organization for improving their current investment

exposure. The financial manager makes the investment exposure on the basis of long term

financing decisions and wealth maximization decisions. The dividend policy of the

organization is mainly segregated under the two sections by the financial managers while

conducting relevant investment decisions. The dividend valuation of the company is mainly

dependent on the relevant theory and irrelevant theory that is used by the company for

securing their investment conditions (Cheung, Hu & Schwiebert, 2018).

The relevancy theory mainly comprises of models such as Walter model, Gordon

Model and Bird in hand argument. These models are mainly used by the organization for

appropriately utilizing the dividend information, which could help in depicting the current

valuation of the company. On the other hand, the irrelevancy theory mainly comprises of

Modigliani-Miller Model, which mainly evaluates the dividends conditions of the

organization, which indicates that the dividend is irrelevant for the valuation of the

organization. Thus, it could be understood that relevancy theory is much more beneficial for

detecting the appropriate valuation of the organization.

From the relevant evaluation of the three options, it has been detected that choosing

the third option of ‘Declaring a scrip dividend in April 2018 of 1 share for every 12 shares

the dividend policy for determining the appropriate level of share price for the organization

and detect whether they are undervalued or overvalued. Dividends are mainly detected as the

portion of the profits that is shared by the organization with their shareholders, which is

considered as the appropriate way of wealth distribution. Therefore, it would be understood

that the decisions of the dividends are a crucial endeavor for the organization, as it might

have direct impact on the share price performance condition of the company.

Therefore, from the relevant evaluation it has been detected that financial managers

utilize the dividend decisions to the organization for improving their current investment

exposure. The financial manager makes the investment exposure on the basis of long term

financing decisions and wealth maximization decisions. The dividend policy of the

organization is mainly segregated under the two sections by the financial managers while

conducting relevant investment decisions. The dividend valuation of the company is mainly

dependent on the relevant theory and irrelevant theory that is used by the company for

securing their investment conditions (Cheung, Hu & Schwiebert, 2018).

The relevancy theory mainly comprises of models such as Walter model, Gordon

Model and Bird in hand argument. These models are mainly used by the organization for

appropriately utilizing the dividend information, which could help in depicting the current

valuation of the company. On the other hand, the irrelevancy theory mainly comprises of

Modigliani-Miller Model, which mainly evaluates the dividends conditions of the

organization, which indicates that the dividend is irrelevant for the valuation of the

organization. Thus, it could be understood that relevancy theory is much more beneficial for

detecting the appropriate valuation of the organization.

From the relevant evaluation of the three options, it has been detected that choosing

the third option of ‘Declaring a scrip dividend in April 2018 of 1 share for every 12 shares

ACCOUNTING AND FINANCE FOR DECISION MAKING

held’ will be most beneficial for the organization. The accommodation of the scrip dividend

would be beneficial for Scommine Company, as the management will be able to reduce the

level of cash outflow. This would eventually help in reducing the comprising cash outflow

and maintaining adequate financial performance. However, other decisions that was proposed

by the directors would instigate massive selling, as investors with no dividends would reduce

the share value of the company. In the similar prices the increment in debt would also

increase the change of insolvency and reduce the share price of the origination. Therefore,

using the scrip dividend would eventually allow the organization to provide additional

benefits to the investors, while compensating for the expenses on the upgradation of the

generators (Florackis, Kanas & Kostakis, 2015).

Conclusion:

From the relevant evaluation of the above assessment the measure that needs to be

taken by Scommine Company is adequately depicted. The case study has indicated that after

the announcement from the government the share price conditions of the company was

deteriorating, while the decisions also needs to be made regarding the dividends that was due

in April. The analysis and dissection of the three measures proposed by the directors have

directly indicated that decision three the ‘Declaring a scrip dividend in April 2018 of 1 share

for every 12 shares held’ is the most appropriate decision for the organization and investors.

The analysis of the relevancy and irrelevancy theories is also conducted, which helps the

investors to value the organization’s current position, which helps in making adequate

investment decisions. Therefore, the directors need to declare scrip dividends, as which will

have no impact on the current debt levels, as the company would be paying dividends in form

of shares and accommodate the upgradation required for complying with the government

decisions.

held’ will be most beneficial for the organization. The accommodation of the scrip dividend

would be beneficial for Scommine Company, as the management will be able to reduce the

level of cash outflow. This would eventually help in reducing the comprising cash outflow

and maintaining adequate financial performance. However, other decisions that was proposed

by the directors would instigate massive selling, as investors with no dividends would reduce

the share value of the company. In the similar prices the increment in debt would also

increase the change of insolvency and reduce the share price of the origination. Therefore,

using the scrip dividend would eventually allow the organization to provide additional

benefits to the investors, while compensating for the expenses on the upgradation of the

generators (Florackis, Kanas & Kostakis, 2015).

Conclusion:

From the relevant evaluation of the above assessment the measure that needs to be

taken by Scommine Company is adequately depicted. The case study has indicated that after

the announcement from the government the share price conditions of the company was

deteriorating, while the decisions also needs to be made regarding the dividends that was due

in April. The analysis and dissection of the three measures proposed by the directors have

directly indicated that decision three the ‘Declaring a scrip dividend in April 2018 of 1 share

for every 12 shares held’ is the most appropriate decision for the organization and investors.

The analysis of the relevancy and irrelevancy theories is also conducted, which helps the

investors to value the organization’s current position, which helps in making adequate

investment decisions. Therefore, the directors need to declare scrip dividends, as which will

have no impact on the current debt levels, as the company would be paying dividends in form

of shares and accommodate the upgradation required for complying with the government

decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE FOR DECISION MAKING

References and Bibliography:

Al-Najjar, B., & Kilincarslan, E. (2016). The effect of ownership structure on dividend

policy: evidence from Turkey. Corporate Governance: The international journal of

business in society, 16(1), 135-161.

Attig, N., Boubakri, N., El Ghoul, S., & Guedhami, O. (2016). The global financial crisis,

family control, and dividend policy. Financial Management, 45(2), 291-313.

Baker, H. K., & Jabbouri, I. (2016). How Moroccan managers view dividend

policy. Managerial Finance, 42(3), 270-288.

Baker, H. K., & Weigand, R. (2015). Corporate dividend policy revisited. Managerial

Finance, 41(2), 126-144.

Baker, H. K., Kilincarslan, E., & Arsal, A. H. (2018). Dividend policy in Turkey: Survey

evidence from Borsa Istanbul firms. Global Finance Journal, 35, 43-57.

Bremberger, F., Cambini, C., Gugler, K., & Rondi, L. (2016). Dividend policy in regulated

network industries: Evidence from the EU. Economic Inquiry, 54(1), 408-432.

Cheung, A., Hu, M., & Schwiebert, J. (2018). Corporate social responsibility and dividend

policy. Accounting & Finance, 58(3), 787-816.

Florackis, C., Kanas, A., & Kostakis, A. (2015). Dividend policy, managerial ownership and

debt financing: A non-parametric perspective. European Journal of Operational

Research, 241(3), 783-795.

He, W., Ng, L., Zaiats, N., & Zhang, B. (2017). Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, 267-286.

References and Bibliography:

Al-Najjar, B., & Kilincarslan, E. (2016). The effect of ownership structure on dividend

policy: evidence from Turkey. Corporate Governance: The international journal of

business in society, 16(1), 135-161.

Attig, N., Boubakri, N., El Ghoul, S., & Guedhami, O. (2016). The global financial crisis,

family control, and dividend policy. Financial Management, 45(2), 291-313.

Baker, H. K., & Jabbouri, I. (2016). How Moroccan managers view dividend

policy. Managerial Finance, 42(3), 270-288.

Baker, H. K., & Weigand, R. (2015). Corporate dividend policy revisited. Managerial

Finance, 41(2), 126-144.

Baker, H. K., Kilincarslan, E., & Arsal, A. H. (2018). Dividend policy in Turkey: Survey

evidence from Borsa Istanbul firms. Global Finance Journal, 35, 43-57.

Bremberger, F., Cambini, C., Gugler, K., & Rondi, L. (2016). Dividend policy in regulated

network industries: Evidence from the EU. Economic Inquiry, 54(1), 408-432.

Cheung, A., Hu, M., & Schwiebert, J. (2018). Corporate social responsibility and dividend

policy. Accounting & Finance, 58(3), 787-816.

Florackis, C., Kanas, A., & Kostakis, A. (2015). Dividend policy, managerial ownership and

debt financing: A non-parametric perspective. European Journal of Operational

Research, 241(3), 783-795.

He, W., Ng, L., Zaiats, N., & Zhang, B. (2017). Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, 267-286.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE FOR DECISION MAKING

Huang, T., Wu, F., Yu, J., & Zhang, B. (2015). Political risk and dividend policy: Evidence

from international political crises. Journal of International Business Studies, 46(5),

574-595.

Jabbouri, I. (2016). Determinants of corporate dividend policy in emerging markets:

Evidence from MENA stock markets. Research in International Business and

Finance, 37, 283-298.

Jacob, M., & Michaely, R. (2017). Taxation and dividend policy: the muting effect of agency

issues and shareholder conflicts. The Review of Financial Studies, 30(9), 3176-3222.

Kajola, S. O., Adewumi, A. A., & Oworu, O. O. (2015). Dividend pay-out policy and firm

financial performance: Evidence from Nigerian listed non-financial

firms. International Journal of Economics, Commerce and Management, 3(4), 1-12.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality

on corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Kumar, A., Kanujiya, P. K., & Kumar, P. (2018). Impact of profitability on dividend policy

of public and private sector bank in India. Asian Man (The)-An International

Journal, 12(1), 43-47.

Lin, T. J., Chen, Y. P., & Tsai, H. F. (2017). The relationship among information asymmetry,

dividend policy and ownership structure. Finance Research Letters, 20, 1-12.

Renneboog, L., & Szilagyi, P. G. (2015). How relevant is dividend policy under low

shareholder protection?. Journal of International Financial Markets, Institutions and

Money.

Setiawan, D., Bandi, B., Kee Phua, L., & Trinugroho, I. (2016). Ownership structure and

dividend policy in Indonesia. Journal of Asia Business Studies, 10(3), 230-252.

Huang, T., Wu, F., Yu, J., & Zhang, B. (2015). Political risk and dividend policy: Evidence

from international political crises. Journal of International Business Studies, 46(5),

574-595.

Jabbouri, I. (2016). Determinants of corporate dividend policy in emerging markets:

Evidence from MENA stock markets. Research in International Business and

Finance, 37, 283-298.

Jacob, M., & Michaely, R. (2017). Taxation and dividend policy: the muting effect of agency

issues and shareholder conflicts. The Review of Financial Studies, 30(9), 3176-3222.

Kajola, S. O., Adewumi, A. A., & Oworu, O. O. (2015). Dividend pay-out policy and firm

financial performance: Evidence from Nigerian listed non-financial

firms. International Journal of Economics, Commerce and Management, 3(4), 1-12.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality

on corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Kumar, A., Kanujiya, P. K., & Kumar, P. (2018). Impact of profitability on dividend policy

of public and private sector bank in India. Asian Man (The)-An International

Journal, 12(1), 43-47.

Lin, T. J., Chen, Y. P., & Tsai, H. F. (2017). The relationship among information asymmetry,

dividend policy and ownership structure. Finance Research Letters, 20, 1-12.

Renneboog, L., & Szilagyi, P. G. (2015). How relevant is dividend policy under low

shareholder protection?. Journal of International Financial Markets, Institutions and

Money.

Setiawan, D., Bandi, B., Kee Phua, L., & Trinugroho, I. (2016). Ownership structure and

dividend policy in Indonesia. Journal of Asia Business Studies, 10(3), 230-252.

ACCOUNTING AND FINANCE FOR DECISION MAKING

Taofeek, O., Kajola, S. O., & AKINBOLA, O. А. (2019). Influence of Dividend Policy on

Stock Price Volatility of Non-Financial Firms Listed Nigerian Stock

Exchange. Journal of Varna University of Economics, 63(1), 35-49.

Yusof, Y., & Ismail, S. (2016). Determinants of dividend policy of public listed companies in

Malaysia. Review of International Business and Strategy, 26(1), 88-99.

Taofeek, O., Kajola, S. O., & AKINBOLA, O. А. (2019). Influence of Dividend Policy on

Stock Price Volatility of Non-Financial Firms Listed Nigerian Stock

Exchange. Journal of Varna University of Economics, 63(1), 35-49.

Yusof, Y., & Ismail, S. (2016). Determinants of dividend policy of public listed companies in

Malaysia. Review of International Business and Strategy, 26(1), 88-99.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.