Accounting Research Project: East Energy Financial Performance Report

VerifiedAdded on 2020/07/22

|10

|1429

|52

Report

AI Summary

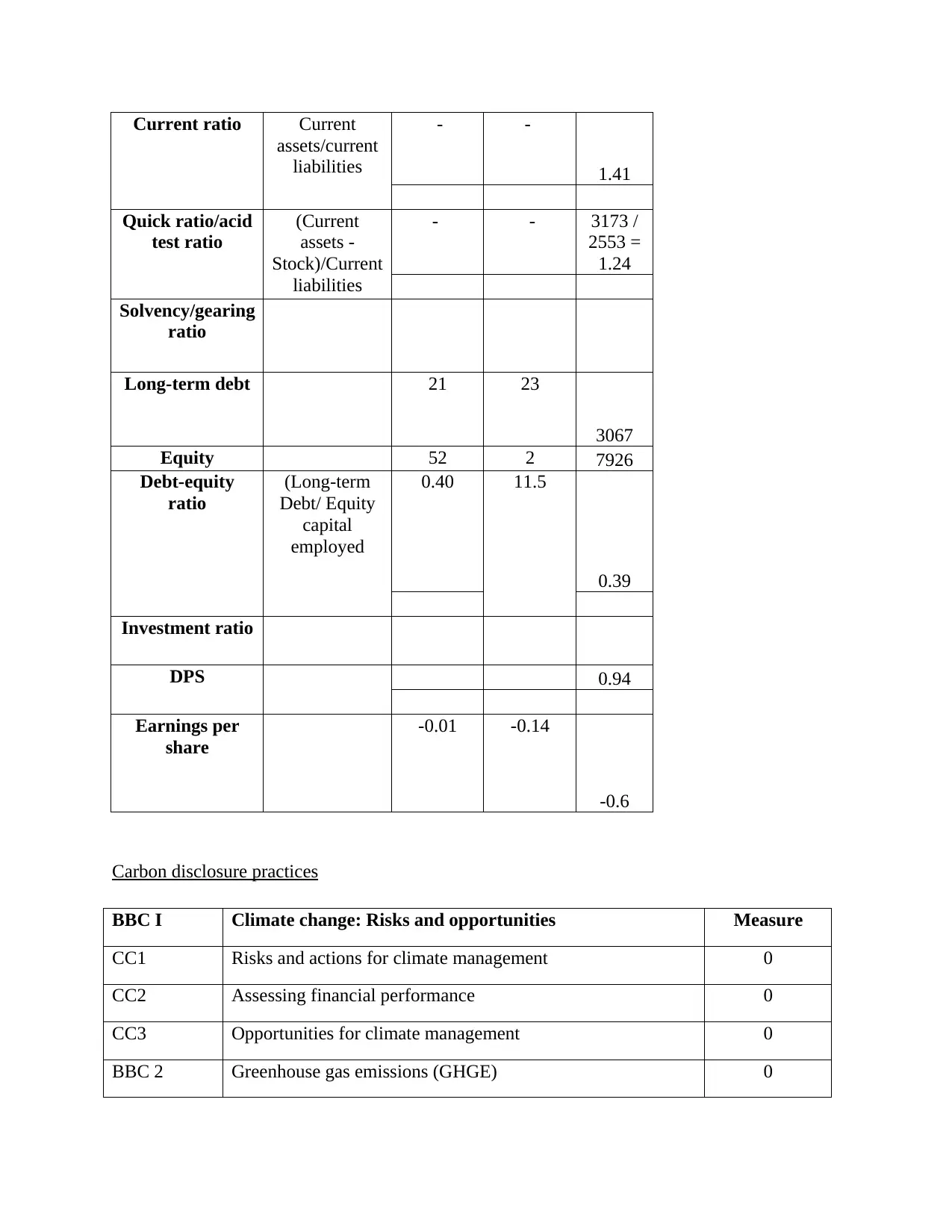

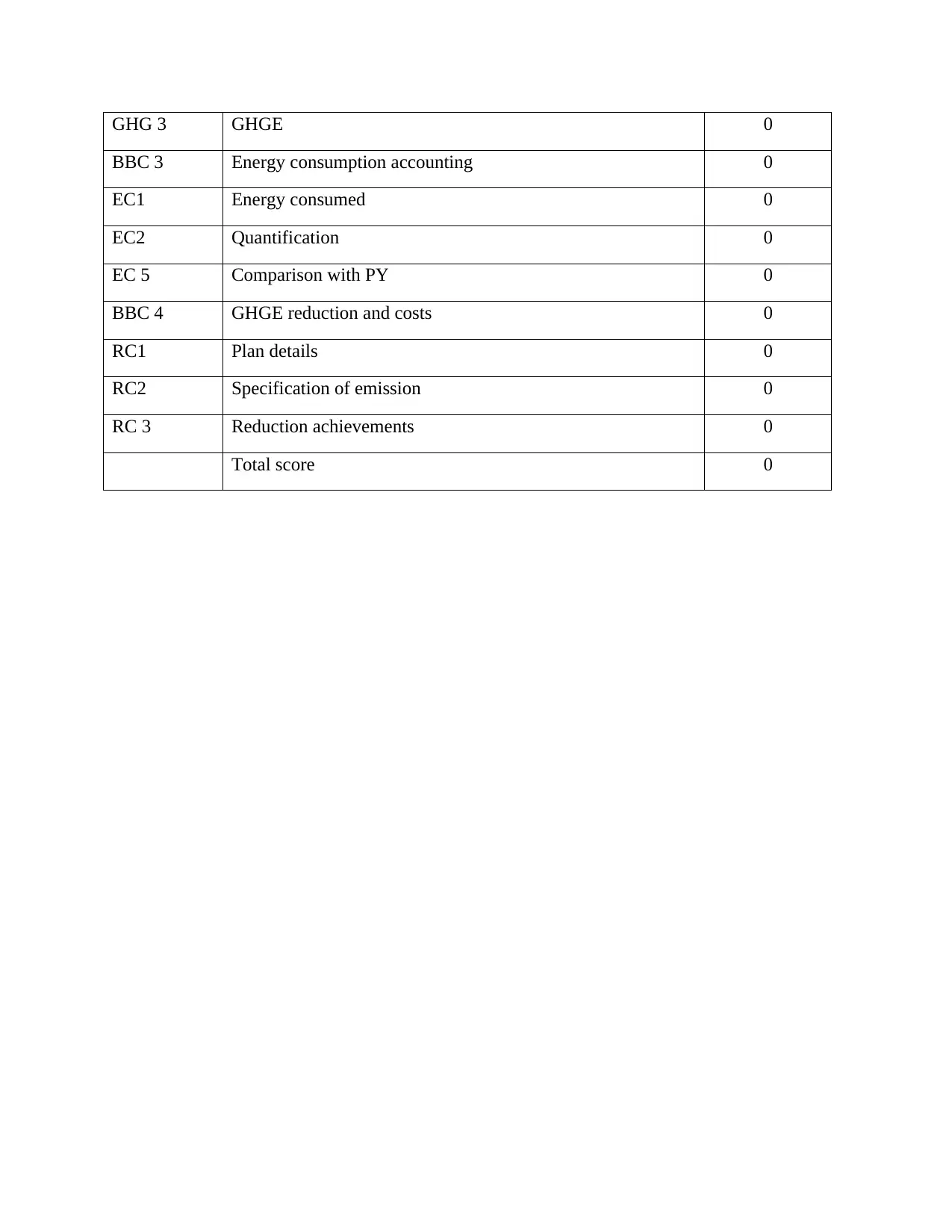

This accounting research project assesses the financial performance of East Energy Resources, focusing on the years 2015 and 2016. The study evaluates corporate governance, financial performance, and sustainability disclosure practices. The financial analysis reveals poor profitability and liquidity positions compared to AGL. Key findings include negative net margins, high debt-equity ratios, and a lack of dividend payments. The report suggests strategic measures to improve performance, such as attracting shareholders and streamlining operations. Additionally, the analysis touches upon carbon disclosure policies and emphasizes the need for East Energy to address environmental concerns. The conclusion highlights the need for technological advancements and improved financial strategies for East Energy to enhance its overall financial health and competitiveness in the market.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.