ACC210: Enron's Fair-Value Accounting and Financial Reporting, 2006

VerifiedAdded on 2022/09/16

|20

|10944

|21

Report

AI Summary

This report analyzes the role of fair-value accounting in Enron's demise, focusing on the misuse of level 3 estimates. The study details how Enron initially used fair-value accounting for energy contracts and merchant investments, later manipulating these valuations to inflate reported earnings and compensate managers. The analysis, based on Benston's 2006 journal article, chronicles Enron's adoption and eventual abuse of fair-value accounting, highlighting the incentives created by linking management compensation to estimated fair values and the failure of internal controls and Arthur Andersen to prevent misleading financial statements. The report underscores the importance of understanding the limitations and potential pitfalls of fair-value accounting, particularly the challenges associated with level 3 estimates that are not based on market prices, and how this led to the downfall of Enron.

Fair-value accounting: A cautionary

tale from Enron

George J. Benston*

Goizueta Business School, Emory University, Atlanta, GA 30322, United States

Abstract

The FASB’s 2004 Exposure Draft, Fair-Value Measurements, would have companie

determine fair values by reference to market prices on the same assets (level 1), sim

assets (level2) and,where these prices are not available or appropriate,present value

and other internally generated estimated values (level3). Enron extensively used level

three estimates and,in some instances,level2 estimates,for its externaland internal

reporting. A description of it’s use and misuse of fair-value accounting should provide

some insights into the problems that auditors and financial statement users might fa

when companies use level 2 and, more importantly, level 3 fair valuations. Enron firs

used level 3 fair-value accounting for energy contracts, then for trading activities gen

ally and undertakings designated as ‘‘merchant’’ investments. Simultaneously, these

values were used to evaluate and compensate senior employees.Enron’s accountants

(with Andersen’s approval) used accounting devices to report cash flow from operati

rather than financing and to otherwise cover up fair-value overstatements and losses

projects undertaken by managers whose compensation was based on fair values. Ba

on a chronologically ordered analysis of its activities and investments,I believe that

Enron’s use of fair-value accounting is substantially responsible for its demise.

Ó 2006 Elsevier Inc. All rights reserved.

0278-4254/$ - see front matter Ó 2006 Elsevier Inc. All rights reserved.

doi:10.1016/j.jaccpubpol.2006.05.003

* Tel.: +1 404 727 7831; fax: +1 404 727 6313.

E-mail address: george_benston@bus.emory.edu

Journal of Accounting and Public Policy 25 (2006) 465–484

www.elsevier.com/locate/jaccpubpol

tale from Enron

George J. Benston*

Goizueta Business School, Emory University, Atlanta, GA 30322, United States

Abstract

The FASB’s 2004 Exposure Draft, Fair-Value Measurements, would have companie

determine fair values by reference to market prices on the same assets (level 1), sim

assets (level2) and,where these prices are not available or appropriate,present value

and other internally generated estimated values (level3). Enron extensively used level

three estimates and,in some instances,level2 estimates,for its externaland internal

reporting. A description of it’s use and misuse of fair-value accounting should provide

some insights into the problems that auditors and financial statement users might fa

when companies use level 2 and, more importantly, level 3 fair valuations. Enron firs

used level 3 fair-value accounting for energy contracts, then for trading activities gen

ally and undertakings designated as ‘‘merchant’’ investments. Simultaneously, these

values were used to evaluate and compensate senior employees.Enron’s accountants

(with Andersen’s approval) used accounting devices to report cash flow from operati

rather than financing and to otherwise cover up fair-value overstatements and losses

projects undertaken by managers whose compensation was based on fair values. Ba

on a chronologically ordered analysis of its activities and investments,I believe that

Enron’s use of fair-value accounting is substantially responsible for its demise.

Ó 2006 Elsevier Inc. All rights reserved.

0278-4254/$ - see front matter Ó 2006 Elsevier Inc. All rights reserved.

doi:10.1016/j.jaccpubpol.2006.05.003

* Tel.: +1 404 727 7831; fax: +1 404 727 6313.

E-mail address: george_benston@bus.emory.edu

Journal of Accounting and Public Policy 25 (2006) 465–484

www.elsevier.com/locate/jaccpubpol

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Keywords:Fair-value accounting; Enron

1. Introduction

The US and International Financial Accounting Standards Boards (FASB

and IASB) have been moving towards replacing historical-cost with fair-value

accounting. In general, fair values have been limited to financial assets and l

bilities,at least in the financialstatements proper.1 A Proposed Statement of

FinancialAccounting Standards,Fair-Value Measurements (FASB,2005,p.

5), specifies a ‘‘fair-value hierarchy.’’Level 1 bases fair values on ‘‘quoted

prices for identicalassets and liabilities in active reference markets whenever

that information is available.’’If such prices are not available,level2 would

prevail, for which ‘‘quoted prices on similar assets and liabilities in active ma

kets,adjusted as appropriate for differences’’would be used (FASB,2005,p.

6). Level 3 estimates ‘‘require judgment in the selection and application of va

uation techniques and relevant inputs.’’ The exposure draft discusses measu

mentproblems that complicate application of allthree levels.For example,

with respect to levels 1 and 2,how should prices that vary by quantity pur-

chased or sold be applied and, where transactions costs are significant, shou

entry or exit prices be used? As difficult as are these problems,at least many

independent public accountants and auditors have dealt with them extensive

and are aware ofmeasurementand verification pitfalls.However,company

accountants and external auditors have had less experience with the third le

(at least for external reporting), which use estimates based on discounted ca

flows and other valuation techniques produced by company managers rather

than by reference to market prices.

Indeed, there are few situations that have revealed the problems encounte

when companies use third levelestimates for their public financialreports.

Instances in which transaction-based historical-based numbers have been mi

leadingly and/or fraudulently reported abound,such as companies reporting

revenue before it is earned (and sometimes not ever earned), inventories mi

ported and mispriced, and expenditures capitalized rather than expensed. M

ford and Comiskey (2002) and Schilit (2002) provide many illustrations of suc

‘‘schenanigans’’ (as Schilit characterizes them). But they (and to my knowled

few,if any,others) do not describe how fair-value numbers not grounded on

actual market prices have been misused and abused. Enron’s bankruptcy an

the subsequent investigations and public revelations of how their managers u

level3 fair-value estimates for both internaland externalaccounting and the

1 The exceptions include goodwillimpairment and,in Europe,appraisals of other assets under

specified conditions.

466 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

1. Introduction

The US and International Financial Accounting Standards Boards (FASB

and IASB) have been moving towards replacing historical-cost with fair-value

accounting. In general, fair values have been limited to financial assets and l

bilities,at least in the financialstatements proper.1 A Proposed Statement of

FinancialAccounting Standards,Fair-Value Measurements (FASB,2005,p.

5), specifies a ‘‘fair-value hierarchy.’’Level 1 bases fair values on ‘‘quoted

prices for identicalassets and liabilities in active reference markets whenever

that information is available.’’If such prices are not available,level2 would

prevail, for which ‘‘quoted prices on similar assets and liabilities in active ma

kets,adjusted as appropriate for differences’’would be used (FASB,2005,p.

6). Level 3 estimates ‘‘require judgment in the selection and application of va

uation techniques and relevant inputs.’’ The exposure draft discusses measu

mentproblems that complicate application of allthree levels.For example,

with respect to levels 1 and 2,how should prices that vary by quantity pur-

chased or sold be applied and, where transactions costs are significant, shou

entry or exit prices be used? As difficult as are these problems,at least many

independent public accountants and auditors have dealt with them extensive

and are aware ofmeasurementand verification pitfalls.However,company

accountants and external auditors have had less experience with the third le

(at least for external reporting), which use estimates based on discounted ca

flows and other valuation techniques produced by company managers rather

than by reference to market prices.

Indeed, there are few situations that have revealed the problems encounte

when companies use third levelestimates for their public financialreports.

Instances in which transaction-based historical-based numbers have been mi

leadingly and/or fraudulently reported abound,such as companies reporting

revenue before it is earned (and sometimes not ever earned), inventories mi

ported and mispriced, and expenditures capitalized rather than expensed. M

ford and Comiskey (2002) and Schilit (2002) provide many illustrations of suc

‘‘schenanigans’’ (as Schilit characterizes them). But they (and to my knowled

few,if any,others) do not describe how fair-value numbers not grounded on

actual market prices have been misused and abused. Enron’s bankruptcy an

the subsequent investigations and public revelations of how their managers u

level3 fair-value estimates for both internaland externalaccounting and the

1 The exceptions include goodwillimpairment and,in Europe,appraisals of other assets under

specified conditions.

466 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

effect of those measurements on their operations and performance should pr

vide some usefulinsights into the problems thatauditors are likely to face

should the proposed SFAS Fair-Value Measurements be adopted.

Although Enron’s failure in December 2001 had many causes,2 both imme-

diate (admissions of massive accounting misstatements) and proximate (mor

complicated, as described below), there is strong reason to believe that Enro

early and continuing use of level 3 fair-value accounting played an important

role in its demise.It appears that Enron initially used level3 fair-value esti-

mates (predominantly present value estimates) without any intent to mislead

investors, but rather to motivate and reward managers for the economic ben

efits they achieved for shareholders.Enron first revalued energy contracts,

reflecting an innovation in how these contractswere structured,with the

increase in value reported as current period earnings. Then level 3 revaluatio

were applied to otherassets,particularly whatEnron termed ‘‘merchant’’

investments.Increasingly,as Enron’s operations were not as profitable as its

managers predicted to the stock market, these upward revaluations were us

opportunistically to inflate reported netincome.This tendency was exacer-

bated by Enron’s basing managers’ compensation on the estimated fair-valu

of their merchant investment projects. This gave those managers strong ince

tives to over-invest resources in often costly, poorly devised, and poorly impl

mented projectsthat could garnera high ‘‘fair’’ valuation.Initially, some

contracts and merchant investments may have had value beyond their costs

But, contrary to the way fair-value accounting should be used,reductions in

value rarely were recognized and recorded because they either were ignored

or were assumed to be temporary. Market prices, specified as level 2 estimat

in Fair-Value Measurements(FASB, 2005),were used by Enron to value

restricted stock, although in most instances they were not adjusted to accou

for differences in value between Enron’s holdings and publicly traded stock, a

specified by the FASB.Market prices were also used by Enron’s traders in

models to value their positions. In almost all of these applications, the numbe

used tended to overstate the value of Enron’s assets and reported net incom

As the following largely chronologicaldescription of Enron’s adoption of

level3 fair-value accounting shows,its abuse by Enron’s managers occurred

gradually until it dominated their decisions, reports to the public, and accoun

ing procedures. Although, technically, fair-value accounting under GAAP was

limited to financialassets,Enron’s accountants were able to get around this

restriction and record present-value-estimates of other assets using procedu

that were accepted and possibly designed by itsexternalauditor,Arthur

Andersen.

2 See Partnoy (2002), who blames Enron’s use of derivatives, and Coffee (2002),who points to

inadequate ‘‘gatekeepers,’’ particularly external auditors and attorneys.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484467

vide some usefulinsights into the problems thatauditors are likely to face

should the proposed SFAS Fair-Value Measurements be adopted.

Although Enron’s failure in December 2001 had many causes,2 both imme-

diate (admissions of massive accounting misstatements) and proximate (mor

complicated, as described below), there is strong reason to believe that Enro

early and continuing use of level 3 fair-value accounting played an important

role in its demise.It appears that Enron initially used level3 fair-value esti-

mates (predominantly present value estimates) without any intent to mislead

investors, but rather to motivate and reward managers for the economic ben

efits they achieved for shareholders.Enron first revalued energy contracts,

reflecting an innovation in how these contractswere structured,with the

increase in value reported as current period earnings. Then level 3 revaluatio

were applied to otherassets,particularly whatEnron termed ‘‘merchant’’

investments.Increasingly,as Enron’s operations were not as profitable as its

managers predicted to the stock market, these upward revaluations were us

opportunistically to inflate reported netincome.This tendency was exacer-

bated by Enron’s basing managers’ compensation on the estimated fair-valu

of their merchant investment projects. This gave those managers strong ince

tives to over-invest resources in often costly, poorly devised, and poorly impl

mented projectsthat could garnera high ‘‘fair’’ valuation.Initially, some

contracts and merchant investments may have had value beyond their costs

But, contrary to the way fair-value accounting should be used,reductions in

value rarely were recognized and recorded because they either were ignored

or were assumed to be temporary. Market prices, specified as level 2 estimat

in Fair-Value Measurements(FASB, 2005),were used by Enron to value

restricted stock, although in most instances they were not adjusted to accou

for differences in value between Enron’s holdings and publicly traded stock, a

specified by the FASB.Market prices were also used by Enron’s traders in

models to value their positions. In almost all of these applications, the numbe

used tended to overstate the value of Enron’s assets and reported net incom

As the following largely chronologicaldescription of Enron’s adoption of

level3 fair-value accounting shows,its abuse by Enron’s managers occurred

gradually until it dominated their decisions, reports to the public, and accoun

ing procedures. Although, technically, fair-value accounting under GAAP was

limited to financialassets,Enron’s accountants were able to get around this

restriction and record present-value-estimates of other assets using procedu

that were accepted and possibly designed by itsexternalauditor,Arthur

Andersen.

2 See Partnoy (2002), who blames Enron’s use of derivatives, and Coffee (2002),who points to

inadequate ‘‘gatekeepers,’’ particularly external auditors and attorneys.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484467

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the following section, I describe Enron’s initial and then widespread use

and abuse of level 3 fair-value in its accounting for energy and other commo

ity-trading contracts, energy production facilities, ‘‘merchant’’ investments, i

major international projects and energy management contracts, investments

broadband (including particularly egregious accounting for its Braveheart pro

ject with Blockbuster), and derivatives trading.3 This is followed by a descrip-

tion of the incentives from basing managementcompensation on fair-value

estimates. I then show how Enron, by structuring transactions so as to report

cash flows from operations, ‘‘validated’’ the profits it reported. Finally, I con-

sider why Enron’s internalcontrolsystem and its externalauditor,Arthur

Andersen, did not prevent Enron’s using fair-value estimates to produce mis-

leading financial statements.

2. Enron’s adoption and use of fair-value accounting4

Enron’s initial substantial success and later failure was the result of a succ

sion of decisions. Fair-value accounting played an important role in these dec

sions because it affected indicators of success and managerial incentives. Th

led to accounting cover-ups and, I believe, to Enron’s subsequent bankruptcy

presentthese developments essentially in chronologicalorder,which shows

how Enron’s initial‘‘reasonable’’use of fair-value accounting evolved and

eventually dominated its accounting and corrupted its operations and report

ing to shareholders.

2.1. Energy contracts

Enron developed from the merger of several pipeline companies that made

the largest natural gas distribution system in the United States. In 1990, Jeffr

Skilling joined Enron after having been a McKinsey consultant to the com-

pany. He had developed a method of trading natural gas contracts called the

Gas Bank.Enron’s CEO, Kenneth Lay, persuaded him to join the company.

Skilling became chairman and CEO of a new division,Enron Finance,with

the mandate to make the Gas Bank work, for which he would be richly com-

pensated with ‘‘phantom’’equity (wherein he received additionalpay in pro-

portion to increases in the market price of Enron stock). Enron Finance sold

long-term contracts for gas to utilities and manufacturers. Skilling’s innovatio

3 Although Enron used the term ‘‘mark-to-market’’ accounting, it rarely based the valuations on

actualmarket prices. Hereafter, ‘‘fair value’’refers to level3 valuations,those based on present-

value and other estimates that are not taken from market prices.

4 This description is largely derived from and documented in McLean and Elkind (2003) and (to

much less extent) Bryce (2002) and Eichenwald (2005), as well as other sources, as noted.

468 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

and abuse of level 3 fair-value in its accounting for energy and other commo

ity-trading contracts, energy production facilities, ‘‘merchant’’ investments, i

major international projects and energy management contracts, investments

broadband (including particularly egregious accounting for its Braveheart pro

ject with Blockbuster), and derivatives trading.3 This is followed by a descrip-

tion of the incentives from basing managementcompensation on fair-value

estimates. I then show how Enron, by structuring transactions so as to report

cash flows from operations, ‘‘validated’’ the profits it reported. Finally, I con-

sider why Enron’s internalcontrolsystem and its externalauditor,Arthur

Andersen, did not prevent Enron’s using fair-value estimates to produce mis-

leading financial statements.

2. Enron’s adoption and use of fair-value accounting4

Enron’s initial substantial success and later failure was the result of a succ

sion of decisions. Fair-value accounting played an important role in these dec

sions because it affected indicators of success and managerial incentives. Th

led to accounting cover-ups and, I believe, to Enron’s subsequent bankruptcy

presentthese developments essentially in chronologicalorder,which shows

how Enron’s initial‘‘reasonable’’use of fair-value accounting evolved and

eventually dominated its accounting and corrupted its operations and report

ing to shareholders.

2.1. Energy contracts

Enron developed from the merger of several pipeline companies that made

the largest natural gas distribution system in the United States. In 1990, Jeffr

Skilling joined Enron after having been a McKinsey consultant to the com-

pany. He had developed a method of trading natural gas contracts called the

Gas Bank.Enron’s CEO, Kenneth Lay, persuaded him to join the company.

Skilling became chairman and CEO of a new division,Enron Finance,with

the mandate to make the Gas Bank work, for which he would be richly com-

pensated with ‘‘phantom’’equity (wherein he received additionalpay in pro-

portion to increases in the market price of Enron stock). Enron Finance sold

long-term contracts for gas to utilities and manufacturers. Skilling’s innovatio

3 Although Enron used the term ‘‘mark-to-market’’ accounting, it rarely based the valuations on

actualmarket prices. Hereafter, ‘‘fair value’’refers to level3 valuations,those based on present-

value and other estimates that are not taken from market prices.

4 This description is largely derived from and documented in McLean and Elkind (2003) and (to

much less extent) Bryce (2002) and Eichenwald (2005), as well as other sources, as noted.

468 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

was to give natural gas producers up-front cash payments, which induced th

to sign long-term supply contracts.He insisted on use of ‘‘mark-to-market’’

(actually ‘‘fair-value,’’as there was no market for the contracts) accounting

to measure his division’s net profit. In 1991 Enron’s board of directors, audit

committee and its external auditor, Arthur Andersen, approved the use of thi

‘‘mark-to-market’’accounting.In January 1992 the SEC approved it for gas

contracts beginning that year. Enron, though, used mark-to-market accountin

for its not-as-yet-filed 1991 statements (withoutobjection by the SEC)and

booked $242 million in earnings. Thereafter, Enron recorded gains (earnings)

when gas contracts were signed, based on its estimates of gas prices project

over many (e.g., 10 and 20) years.

In 1991,Enron created a new division thatmerged Enron Finance with

Enron Gas Marketing (which sold naturalgas to wholesale customers)and

Houston Pipeline to form Enron Capitaland Trade Resources (ECT),all of

which were managed by Skilling.He adopted fair-value accounting for ECT

and he compensated the division’s managers with percentages of internally g

erated estimates of the fair values of contracts they developed. An early (199

example was a 20-year contract to supply naturalgas to the developer of a

large electric generating plant under construction, Sithe Energies. ECT imme

diately recorded the estimated netpresentvalue ofthat contractas current

earnings. During the 1990s, as changes in energy prices indicated that the co

tract was more valuable,additionalgains resulting from revaluations to fair

value were recorded,which allowed Enron to meet its internaland external

quarterly net income projections. By the late 1990s, Sithe owed Enron $1.5 b

lion. However,even though Enron’s internalRisk Assessmentand Control

(RAC) group estimated that Sithe’s only asset (worth just over $400 million)

was inadequate to pay its obligation,the fair value of the contract was not

reduced and,consequently,a loss was not recorded.In fact, the loss was not

recorded until after Enron declared bankruptcy.

2.2. Energy production facilities

Enron International (EI), another major division of Enron, developed and

constructed naturalgas power plants and other projects around the world.

Enron’s developer, John Wing, had previously (in 1987) developed a gas-fired

electricity plant in Texas City, Texas. It was financed almost entirely with hig

yield, high-return (junk) bonds and was very profitable as measured by histor

ical cost accounting.In 1990,Wing completed a dealfor a giant plant in

Teesside (UK) that could produce 4% of the United Kingdom’s entire energy

demands. Enron put up almost no cash and still owned half the plant valued

$1.6 billion in exchange for its role in conceiving and constructing the plant.

the early 1990s, Enron booked more than $100 million in profits from develo

ment and construction fees. Wing received at least $18 million in Enron stock

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484469

to sign long-term supply contracts.He insisted on use of ‘‘mark-to-market’’

(actually ‘‘fair-value,’’as there was no market for the contracts) accounting

to measure his division’s net profit. In 1991 Enron’s board of directors, audit

committee and its external auditor, Arthur Andersen, approved the use of thi

‘‘mark-to-market’’accounting.In January 1992 the SEC approved it for gas

contracts beginning that year. Enron, though, used mark-to-market accountin

for its not-as-yet-filed 1991 statements (withoutobjection by the SEC)and

booked $242 million in earnings. Thereafter, Enron recorded gains (earnings)

when gas contracts were signed, based on its estimates of gas prices project

over many (e.g., 10 and 20) years.

In 1991,Enron created a new division thatmerged Enron Finance with

Enron Gas Marketing (which sold naturalgas to wholesale customers)and

Houston Pipeline to form Enron Capitaland Trade Resources (ECT),all of

which were managed by Skilling.He adopted fair-value accounting for ECT

and he compensated the division’s managers with percentages of internally g

erated estimates of the fair values of contracts they developed. An early (199

example was a 20-year contract to supply naturalgas to the developer of a

large electric generating plant under construction, Sithe Energies. ECT imme

diately recorded the estimated netpresentvalue ofthat contractas current

earnings. During the 1990s, as changes in energy prices indicated that the co

tract was more valuable,additionalgains resulting from revaluations to fair

value were recorded,which allowed Enron to meet its internaland external

quarterly net income projections. By the late 1990s, Sithe owed Enron $1.5 b

lion. However,even though Enron’s internalRisk Assessmentand Control

(RAC) group estimated that Sithe’s only asset (worth just over $400 million)

was inadequate to pay its obligation,the fair value of the contract was not

reduced and,consequently,a loss was not recorded.In fact, the loss was not

recorded until after Enron declared bankruptcy.

2.2. Energy production facilities

Enron International (EI), another major division of Enron, developed and

constructed naturalgas power plants and other projects around the world.

Enron’s developer, John Wing, had previously (in 1987) developed a gas-fired

electricity plant in Texas City, Texas. It was financed almost entirely with hig

yield, high-return (junk) bonds and was very profitable as measured by histor

ical cost accounting.In 1990,Wing completed a dealfor a giant plant in

Teesside (UK) that could produce 4% of the United Kingdom’s entire energy

demands. Enron put up almost no cash and still owned half the plant valued

$1.6 billion in exchange for its role in conceiving and constructing the plant.

the early 1990s, Enron booked more than $100 million in profits from develo

ment and construction fees. Wing received at least $18 million in Enron stock

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484469

plus several million dollars in salary and bonuses for his work on the project,

establishing performance-based compensation. Such rewards were later agg

sively demanded by and used to reward Enron’s senior managers, but with o

major difference – unlike Wing’s compensation that was based on his project

profitable completion and operation as measured by historicalcost numbers,

their rewards were based on the projected future benefits from (or fair values

of) projects.

To provide gas for the Teesside plant, Enron signed a long-term ‘‘take-or-

pay’’contract in 1993 for North Sea J-Block gas.After gas prices decreased

instead of increasing as Enron had expected, the contract became increasing

costly. Nevertheless, the contract was not marked down to fair value to refle

the losses until 1997. That year, Enron was able to change the contract to on

where the price of gas floated with the market, at which point it had to recor

$675 million pre-tax loss.

2.3. ‘‘Merchant’’ investments

Enron also used fair-value accounting for its ‘‘merchant’’ investments–part

nership interests and stock in untraded or thinly traded companies it started

in which it invested. As was the situation for the energy contracts, the fair va

ues were not based on actual market prices, because no market prices existe

for the merchant investments. Although the SEC and FASB require fair-value

accounting for energy contracts,FAS 115 limits revaluations of securities to

those traded on a recognized exchange and for which there were reliable sha

prices, and valuation increases in non-financial assets are not permitted. Enr

(and possibly other corporations) used the following procedure to avoid these

limitations.Enron incorporated major projects into subsidiaries,the stock of

which it designated as ‘‘merchant’’investments,and declared that it was in

the investment company business,for which the AICPA’s Investment Com-

pany Guide applies. This Guide requires these companies to revalue financial

assets held (presumably)for trading to fair values,even when these values

are not determined from arm’s-length market transactions. In such instances

the values may be determined by discounted expected cash flow models,as

are level3 fair values.5 The models allowed Enron’s managers to manipulate

net income by making ‘‘reasonable’’assumptions thatwould give them the

gains they wanted to record. (Some notable examples are provided below.)

Enron chiefaccounting officer,Rick Causey,used revaluations ofthese

investments to meetthe earnings goals announced by Skilling and Enron’s

5 ‘‘Real’’ investment companies, which often are limited partnerships, tend to value investment

conservatively and values are notchanged untila materialeventoccurs to change the value

(National Venture Capital Association, undated and unpaginated, under valuation), apparently to

limit the amount that would be paid out to investors who take out their investments.

470 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

establishing performance-based compensation. Such rewards were later agg

sively demanded by and used to reward Enron’s senior managers, but with o

major difference – unlike Wing’s compensation that was based on his project

profitable completion and operation as measured by historicalcost numbers,

their rewards were based on the projected future benefits from (or fair values

of) projects.

To provide gas for the Teesside plant, Enron signed a long-term ‘‘take-or-

pay’’contract in 1993 for North Sea J-Block gas.After gas prices decreased

instead of increasing as Enron had expected, the contract became increasing

costly. Nevertheless, the contract was not marked down to fair value to refle

the losses until 1997. That year, Enron was able to change the contract to on

where the price of gas floated with the market, at which point it had to recor

$675 million pre-tax loss.

2.3. ‘‘Merchant’’ investments

Enron also used fair-value accounting for its ‘‘merchant’’ investments–part

nership interests and stock in untraded or thinly traded companies it started

in which it invested. As was the situation for the energy contracts, the fair va

ues were not based on actual market prices, because no market prices existe

for the merchant investments. Although the SEC and FASB require fair-value

accounting for energy contracts,FAS 115 limits revaluations of securities to

those traded on a recognized exchange and for which there were reliable sha

prices, and valuation increases in non-financial assets are not permitted. Enr

(and possibly other corporations) used the following procedure to avoid these

limitations.Enron incorporated major projects into subsidiaries,the stock of

which it designated as ‘‘merchant’’investments,and declared that it was in

the investment company business,for which the AICPA’s Investment Com-

pany Guide applies. This Guide requires these companies to revalue financial

assets held (presumably)for trading to fair values,even when these values

are not determined from arm’s-length market transactions. In such instances

the values may be determined by discounted expected cash flow models,as

are level3 fair values.5 The models allowed Enron’s managers to manipulate

net income by making ‘‘reasonable’’assumptions thatwould give them the

gains they wanted to record. (Some notable examples are provided below.)

Enron chiefaccounting officer,Rick Causey,used revaluations ofthese

investments to meetthe earnings goals announced by Skilling and Enron’s

5 ‘‘Real’’ investment companies, which often are limited partnerships, tend to value investment

conservatively and values are notchanged untila materialeventoccurs to change the value

(National Venture Capital Association, undated and unpaginated, under valuation), apparently to

limit the amount that would be paid out to investors who take out their investments.

470 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CEO and Chairman of the Board, Kenneth Lay. ‘‘By the end of the decade,’’

McLean and Elkind (2003, p. 127) report, ‘‘some 35 percent of Enron’s assets

were being given mark-to-market treatment.’’ When additional earnings were

required,contracts were revisited and reinterpreted,if increases in their fair

values could be recorded. However, recording of losses was delayed if any po

sibility existed that the investment might turn around.

An example is Mariner Energy,a privately owned Houston oil-and-gas

company that did deepwater exploration in which Enron invested and which

it boughtout for $185 million in 1996.Enron’s accountantsperiodically

marked-up its investment as needed to report increases in earnings until,by

the second quarter 2001,it was on the books for $367.4 million.Analyses in

the second and third quarters of 2001 by Enron’s Risk Assessment and Contr

department (RAC) that valued the investment at between $47 and $196 milli

did not result in accounting revaluations. After Enron’s bankruptcy, Mariner

Energy was written down to $110.5 million.

Enron’s investmentin RhythmsNet Connections(Rhythms)is another

example, except that the valuation was based on an actual market price. Enr

April 1999 investment of $10 million before Rhythms went public in April 199

had an estimated market value of $90 million following its initial public offeri

(IPO). However, Enron could not realize this gain because it had signed a lock

up agreement that precluded sale of the stock until November. Not surprising

Enron could not purchase a reasonably priced hedge.With the approvalof

Enron’s board of directors,a specialpurpose entity (SPE),LJM1, controlled

by Enron’s Chief FinancialOfficer,Andrew Fastow,was created to provide

the hedge through an SPE itcreated,LJM Swap Sub. 6 LJM1 was almost

entirely funded with Enron’s own stock purchased with a promissory note at

a 39% discount (because it was restricted). LJM Swap Sub was funded with ha

the stock and a promissory note from LJM1. In effect, Enron was writing the

option on itself, for a substantial fee paid to Fastow. It was not really hedging

against a possible economic loss on the Rhythms stock, but against having to

recognize the loss in its accounts. Thus, Enron’s accounting ‘‘shenanigans’’ w

not limited to booking income from increasing estimated fair values.

2.4. Dabhol, other Enron International projects, and Azurix

In 1996 Rebecca Mark became CEO of Enron International, having previ-

ously been head of Enron Development.She developed projects around the

world at a frenetic pace.She and her managers were given bonuses for each

project they developed of about 9% of the present value of its expected net c

6 The transaction is very complicated.See Benston and Hartgraves (2002,pp. 109–110) for a

much more complete description.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484471

McLean and Elkind (2003, p. 127) report, ‘‘some 35 percent of Enron’s assets

were being given mark-to-market treatment.’’ When additional earnings were

required,contracts were revisited and reinterpreted,if increases in their fair

values could be recorded. However, recording of losses was delayed if any po

sibility existed that the investment might turn around.

An example is Mariner Energy,a privately owned Houston oil-and-gas

company that did deepwater exploration in which Enron invested and which

it boughtout for $185 million in 1996.Enron’s accountantsperiodically

marked-up its investment as needed to report increases in earnings until,by

the second quarter 2001,it was on the books for $367.4 million.Analyses in

the second and third quarters of 2001 by Enron’s Risk Assessment and Contr

department (RAC) that valued the investment at between $47 and $196 milli

did not result in accounting revaluations. After Enron’s bankruptcy, Mariner

Energy was written down to $110.5 million.

Enron’s investmentin RhythmsNet Connections(Rhythms)is another

example, except that the valuation was based on an actual market price. Enr

April 1999 investment of $10 million before Rhythms went public in April 199

had an estimated market value of $90 million following its initial public offeri

(IPO). However, Enron could not realize this gain because it had signed a lock

up agreement that precluded sale of the stock until November. Not surprising

Enron could not purchase a reasonably priced hedge.With the approvalof

Enron’s board of directors,a specialpurpose entity (SPE),LJM1, controlled

by Enron’s Chief FinancialOfficer,Andrew Fastow,was created to provide

the hedge through an SPE itcreated,LJM Swap Sub. 6 LJM1 was almost

entirely funded with Enron’s own stock purchased with a promissory note at

a 39% discount (because it was restricted). LJM Swap Sub was funded with ha

the stock and a promissory note from LJM1. In effect, Enron was writing the

option on itself, for a substantial fee paid to Fastow. It was not really hedging

against a possible economic loss on the Rhythms stock, but against having to

recognize the loss in its accounts. Thus, Enron’s accounting ‘‘shenanigans’’ w

not limited to booking income from increasing estimated fair values.

2.4. Dabhol, other Enron International projects, and Azurix

In 1996 Rebecca Mark became CEO of Enron International, having previ-

ously been head of Enron Development.She developed projects around the

world at a frenetic pace.She and her managers were given bonuses for each

project they developed of about 9% of the present value of its expected net c

6 The transaction is very complicated.See Benston and Hartgraves (2002,pp. 109–110) for a

much more complete description.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484471

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flows, one half paid at the financial close and the other half when the project

became operational. The costs of projects that did not come on line but were

not officially declared to be dead were recorded as assets, if the amounts we

under $200 million. Mark’s largest project, begun in 1992 when she managed

Enron Development,was a giantelectricity power plantin Dabhol, India.

To be economically viable, the government of the Indian state of Maharashtr

would have to purchase a fixed amount of electricity at a high price, despite

fact that it was unable to collect for electricity sold at lower prices. The proje

was severely criticized in India, and the contract was renegotiated several tim

Eventually,Enron invested and lost about $900 million in the project,which

now stands idle.Nevertheless,Mark and her team received $20 million in

bonuses for the project, based on their estimates of its present value.

Relatively few of Enron International projects actually became operational

and few were profitable according to traditional accounting standards after t

became operational. Some pre-bankruptcy evidence is available as a result o

dispute between Skilling and Mark. In 1998, Skilling had an in-house accoun-

tant value Enron International’sprojects.He calculated thatthe division

returned only a 2% return on equity, excluding Enron’s substantial contingen

liability for project debts it guaranteed. Mark’s accountant, though, estimated

that her division returned an average of 12% on equity. After Enron declared

bankruptcy, few of the division’s projects were found to have any value.

In May 1998 Skilling forced Mark out of her post as CEO of Enron Inter-

national. (In December 1996, Lay had appointed Skilling, rather than Mark, a

Enron’s President and Chief Operating Officer.) Perhaps as a consolation prize

in July 1998 the board of directors (with Skilling’s blessing) allowed Mark to

establish a new Enron subsidiary,Azurix, which would develop water-supply

projects around the world.The business began with a $2.4 billion purchase

of a British water utility, Wessex Water Services, for a 28% premium.7 The pur-

chase was largely financed with debt sold by an off-balance-sheet partnershi

Marlin, which itself was financed with debt that Enron guaranteed.Enron’s

obligation on that debt was not reported on its financial statements. Most of

the balance came from public sales of Azurix shares for $700 million. Azurix

then successfully bid for a Buenos Aires, Argentina water utility that was priv

atized,paying three times more than the nexthighestbidder.Azurix later

learned that the dealdid not include the utility’s headquarters and records,

making it difficult (often impossible) to collect past-due and present account

balances.8 By year-end 2000, $402 million had to be written off on the project.

Other disastrous projects were undertaken,Azurix stock declined to $3.50 a

share and Enron had to repurchase the publicly held shares for $8.375. Mark

7 Eichenwald (2005, p. 191) reports the purchase as costing $2.25 billion.

8 Eichenwald (2005, p. 231) reports that Azurix paid twice the next bid and that computers and

records were trashed by the former employees.

472 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

became operational. The costs of projects that did not come on line but were

not officially declared to be dead were recorded as assets, if the amounts we

under $200 million. Mark’s largest project, begun in 1992 when she managed

Enron Development,was a giantelectricity power plantin Dabhol, India.

To be economically viable, the government of the Indian state of Maharashtr

would have to purchase a fixed amount of electricity at a high price, despite

fact that it was unable to collect for electricity sold at lower prices. The proje

was severely criticized in India, and the contract was renegotiated several tim

Eventually,Enron invested and lost about $900 million in the project,which

now stands idle.Nevertheless,Mark and her team received $20 million in

bonuses for the project, based on their estimates of its present value.

Relatively few of Enron International projects actually became operational

and few were profitable according to traditional accounting standards after t

became operational. Some pre-bankruptcy evidence is available as a result o

dispute between Skilling and Mark. In 1998, Skilling had an in-house accoun-

tant value Enron International’sprojects.He calculated thatthe division

returned only a 2% return on equity, excluding Enron’s substantial contingen

liability for project debts it guaranteed. Mark’s accountant, though, estimated

that her division returned an average of 12% on equity. After Enron declared

bankruptcy, few of the division’s projects were found to have any value.

In May 1998 Skilling forced Mark out of her post as CEO of Enron Inter-

national. (In December 1996, Lay had appointed Skilling, rather than Mark, a

Enron’s President and Chief Operating Officer.) Perhaps as a consolation prize

in July 1998 the board of directors (with Skilling’s blessing) allowed Mark to

establish a new Enron subsidiary,Azurix, which would develop water-supply

projects around the world.The business began with a $2.4 billion purchase

of a British water utility, Wessex Water Services, for a 28% premium.7 The pur-

chase was largely financed with debt sold by an off-balance-sheet partnershi

Marlin, which itself was financed with debt that Enron guaranteed.Enron’s

obligation on that debt was not reported on its financial statements. Most of

the balance came from public sales of Azurix shares for $700 million. Azurix

then successfully bid for a Buenos Aires, Argentina water utility that was priv

atized,paying three times more than the nexthighestbidder.Azurix later

learned that the dealdid not include the utility’s headquarters and records,

making it difficult (often impossible) to collect past-due and present account

balances.8 By year-end 2000, $402 million had to be written off on the project.

Other disastrous projects were undertaken,Azurix stock declined to $3.50 a

share and Enron had to repurchase the publicly held shares for $8.375. Mark

7 Eichenwald (2005, p. 191) reports the purchase as costing $2.25 billion.

8 Eichenwald (2005, p. 231) reports that Azurix paid twice the next bid and that computers and

records were trashed by the former employees.

472 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

resigned, receiving the balance of her $710,000 Azurix contract, based on th

projected (mark to fair value) benefits to Enron of the enterprise.

2.5. Energy management contracts

In December 2000,after Skilling became president of Enron,he created a

separate business,Enron Energy Services (EES),with Lou Pai as its CEO.

EES expected to sellpower to retailcustomers,based on assumptions that

the market would be deregulated and that the existing utilities could be unde

sold. Enron sold 7% of EES to institutional investors for $130 million. Based

on this sale (which might have qualified as a level 2 estimate), Enron valued

company at $1.9 billion, which allowed it to record a $61 million profit. How-

ever, EES’s efforts were unsuccessful, in part because retail energy was gene

ally not deregulated.Losses on the retail operationswere not reported

separately, but were combined with the wholesale operations.

Pai then concentrated on selling contracts to companies and institutions to

provide them with energy over long periods with guaranteed savings over th

present costs. Customers often were given up-front cash payments in advanc

the promised savings.These contracts were accounted for on a mark-to-fair-

value basis as of the date the contracts were signed. Sales personnel and ma

ers (especially Pai) were paid bonuses based on those values. Not surprisingl

this compensation scheme generated a lot of bad contracts. A particularly co

(to Enron) contract was signed in February 2001 with Eli Lilly to make improv

ments in its energy supply and use over 15 years. Discounting these amount

8.25–8.50%, Enron valued the contract at $1.3 billion and recorded a $38 mi

gain.9 Within two years, this contract was considered to be worthless.

In 2001, after Pai left EES and Enron, a long-time in-house Enron accoun-

tant, Wanda Curry, was asked to evaluate the EES contracts. Her group exam

ined 13 (of 90) contracts that comprised 80% of the business. Each of them h

been recorded as profitable.Nevertheless,Curry found that the 13 contracts

had a totalnegative value of at least $500 million.For example,a dealfor

which the company had booked $20 million in profits, actually was $70 millio

under water. Although, accordingto mark-to-fair-valueaccountingthe

decrease in value documented by Curry should have been recorded,no such

entry was made and Curry was reassigned.

2.6. Enron broadband services

Enron Broadband Services (EBS)was another major portion ofEnron’s

business. Skilling established it in April 1999 to develop a fiber-optic network

9 See Batson (2003a, pp. 32–33) for details.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484473

projected (mark to fair value) benefits to Enron of the enterprise.

2.5. Energy management contracts

In December 2000,after Skilling became president of Enron,he created a

separate business,Enron Energy Services (EES),with Lou Pai as its CEO.

EES expected to sellpower to retailcustomers,based on assumptions that

the market would be deregulated and that the existing utilities could be unde

sold. Enron sold 7% of EES to institutional investors for $130 million. Based

on this sale (which might have qualified as a level 2 estimate), Enron valued

company at $1.9 billion, which allowed it to record a $61 million profit. How-

ever, EES’s efforts were unsuccessful, in part because retail energy was gene

ally not deregulated.Losses on the retail operationswere not reported

separately, but were combined with the wholesale operations.

Pai then concentrated on selling contracts to companies and institutions to

provide them with energy over long periods with guaranteed savings over th

present costs. Customers often were given up-front cash payments in advanc

the promised savings.These contracts were accounted for on a mark-to-fair-

value basis as of the date the contracts were signed. Sales personnel and ma

ers (especially Pai) were paid bonuses based on those values. Not surprisingl

this compensation scheme generated a lot of bad contracts. A particularly co

(to Enron) contract was signed in February 2001 with Eli Lilly to make improv

ments in its energy supply and use over 15 years. Discounting these amount

8.25–8.50%, Enron valued the contract at $1.3 billion and recorded a $38 mi

gain.9 Within two years, this contract was considered to be worthless.

In 2001, after Pai left EES and Enron, a long-time in-house Enron accoun-

tant, Wanda Curry, was asked to evaluate the EES contracts. Her group exam

ined 13 (of 90) contracts that comprised 80% of the business. Each of them h

been recorded as profitable.Nevertheless,Curry found that the 13 contracts

had a totalnegative value of at least $500 million.For example,a dealfor

which the company had booked $20 million in profits, actually was $70 millio

under water. Although, accordingto mark-to-fair-valueaccountingthe

decrease in value documented by Curry should have been recorded,no such

entry was made and Curry was reassigned.

2.6. Enron broadband services

Enron Broadband Services (EBS)was another major portion ofEnron’s

business. Skilling established it in April 1999 to develop a fiber-optic network

9 See Batson (2003a, pp. 32–33) for details.

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484473

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and trade capacity in its and other firms’ networks. Skilling announced the ne

venture to stock analysts on January 20,2000,together with Scott McNealy,

CEO of Sun Microsystems,who said that Enron would purchase 18,000 of

Sun’s best servers for use in its network. By day end, Enron’s stock increased

by 26%. Enron, though, did not then or ever have software that could provide

bandwidth on demand by and for alternative networks. Rather, Enron’s busi-

ness involved swapping the right to use surplus (dark) fiber on its own netwo

for the right to use surplus on other networks.Overall,Enron invested more

than $1 billion on broadband and reported revenue of $408 million in 2000,

much ofit from sales to Fastow-controlled SPEs.For example,in the first

quarter 2000, EBS recorded a mark-to-fair-value-determined gain of $58 mil-

lion from revaluing and then swapping dark fiber,which was designated a

‘‘sale.’’In the second quarter 2000 EBS revalued and ‘‘sold’’that assetto

LJM2, a SPE controlled by Fastow,and recorded another $53 million pre-

tax gain.Based on mark-to-fair-value accounting,EBS booked a $110.9 mil-

lion profit in the fourth quarter 2000 and first quarter 2001.

In the third quarter 2000 EBS recorded a $150 million fair-value gain on its

$15 million investmentin a tech start-up (AviciSystems)that wentpublic,

using the public IPO price as the basis for the transaction even though Enron

stock could not be sold for 180 days. Enron ‘‘locked in’’ the gain with a hedge

provided by another SPE (Talon),even though Talon would not have been

able to meet its obligation if the stock price declined. Before year-end, the st

price declined by 90%. Talon and other similar SPEs (collectively called ‘‘Pro-

ject Raptor’’) could not cover this loss and other losses amounting to $500 m

lion. Nevertheless,the losses were notrecorded,based on Enron’s (invalid)

assertion thatthe SPEs’obligations could be cross-collateralized with other

SPEs that were claimed (incorrectly) to have sufficient assets. Those assets w

Enron shares and rights to shares obtained from Enron for which the Raptors

had not paid. Consequently, for Enron the assets did not exist, because if the

SPEs had to pay Enron their obligations for the hedges by selling the shares,

they would be unable to pay their other debt to Enron.Andersen’s partner-

in-charge, David Duncan, agreed to this procedure despite an objection from

Carl Bass,a member of the firm’s ProfessionalStandards Group who previ-

ously was on the audit team. At Enron’s request, Bass was excluded from com

menting on issues related to Enron.Andersen was paid $1.3 million for its

Raptor-related work. When the Raptors were terminated in 2001 a $710 mil-

lion pre-tax loss was booked.

2.7. Braveheart partnership with Blockbuster

In the fourth quarter 2000 EBS announced a 20-year project (Braveheart)

with Blockbuster to broadcast movies on demand to television viewers. How-

ever, Enron did not have the technology to deliver the movies and Blockbust

474 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

venture to stock analysts on January 20,2000,together with Scott McNealy,

CEO of Sun Microsystems,who said that Enron would purchase 18,000 of

Sun’s best servers for use in its network. By day end, Enron’s stock increased

by 26%. Enron, though, did not then or ever have software that could provide

bandwidth on demand by and for alternative networks. Rather, Enron’s busi-

ness involved swapping the right to use surplus (dark) fiber on its own netwo

for the right to use surplus on other networks.Overall,Enron invested more

than $1 billion on broadband and reported revenue of $408 million in 2000,

much ofit from sales to Fastow-controlled SPEs.For example,in the first

quarter 2000, EBS recorded a mark-to-fair-value-determined gain of $58 mil-

lion from revaluing and then swapping dark fiber,which was designated a

‘‘sale.’’In the second quarter 2000 EBS revalued and ‘‘sold’’that assetto

LJM2, a SPE controlled by Fastow,and recorded another $53 million pre-

tax gain.Based on mark-to-fair-value accounting,EBS booked a $110.9 mil-

lion profit in the fourth quarter 2000 and first quarter 2001.

In the third quarter 2000 EBS recorded a $150 million fair-value gain on its

$15 million investmentin a tech start-up (AviciSystems)that wentpublic,

using the public IPO price as the basis for the transaction even though Enron

stock could not be sold for 180 days. Enron ‘‘locked in’’ the gain with a hedge

provided by another SPE (Talon),even though Talon would not have been

able to meet its obligation if the stock price declined. Before year-end, the st

price declined by 90%. Talon and other similar SPEs (collectively called ‘‘Pro-

ject Raptor’’) could not cover this loss and other losses amounting to $500 m

lion. Nevertheless,the losses were notrecorded,based on Enron’s (invalid)

assertion thatthe SPEs’obligations could be cross-collateralized with other

SPEs that were claimed (incorrectly) to have sufficient assets. Those assets w

Enron shares and rights to shares obtained from Enron for which the Raptors

had not paid. Consequently, for Enron the assets did not exist, because if the

SPEs had to pay Enron their obligations for the hedges by selling the shares,

they would be unable to pay their other debt to Enron.Andersen’s partner-

in-charge, David Duncan, agreed to this procedure despite an objection from

Carl Bass,a member of the firm’s ProfessionalStandards Group who previ-

ously was on the audit team. At Enron’s request, Bass was excluded from com

menting on issues related to Enron.Andersen was paid $1.3 million for its

Raptor-related work. When the Raptors were terminated in 2001 a $710 mil-

lion pre-tax loss was booked.

2.7. Braveheart partnership with Blockbuster

In the fourth quarter 2000 EBS announced a 20-year project (Braveheart)

with Blockbuster to broadcast movies on demand to television viewers. How-

ever, Enron did not have the technology to deliver the movies and Blockbust

474 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

did not have the rights to the movies to be broadcast.Nevertheless,as of

December31, 2000,Enron assigned a fair value of $125 million to its

Braveheart investment and a profit of $53 million from increasing the invest-

ment to its fair value,even though no sales had been made.Enron recorded

additionalrevenue of$53 million from the venture in the firstquarterof

2001,although Blockbuster did not record any income from the venture and

dissolved the partnership in March 2001.In October 2001 Enron had to

announce publicly that it reversed the $110.9 million in profit it had earlier

claimed,which contributedto its loss of public trust and subsequent

bankruptcy.

How could Enron have so massively misestimated the fair value of its Brav

heart investment, and how could Andersen have allowed Enron to report thes

values and their increases as profits? Indeed, the Examiner in Bankruptcy (Ba

son, 2003a, pp. 30–31) finds that Andersen prepared the appraisal of the pro

ject’svalue.Andersen assumed thefollowing:(1) the businesswould be

established in 10 major metro areas within 12 months;(2) eightnew areas

would be added per year until 2010 and these would each grow at 1% a year

(3) digitalsubscriber lines (DSLs)would be used by 5% of the households,

increasing to 32% by 2010,and these would increase in speed sufficientto

accept the broadcasts;and (4) Braveheart would garner 50% of this market.

After determining (somehow) a net cash flow from each of these households

and discounting by 31–34%, the project was assigned a fair value. I suggest t

this calculation illustrates an essentialweakness of level3 fair-value calcula-

tions that necessarily are not grounded on actualmarket transactions.How

can one determine whether or not such assumptions about a ‘‘first-time’’ pro

ject are ‘‘reasonable’’?

2.8. Derivatives trading

Enron’s (derivatives)trading activities expanded beyond naturalgas and

power contracts to contracts in metals, paper, credit derivatives, and commo

ities.Much of this trading was done over an Internetsystem itdeveloped,

Enron On Line (EOL), which enabled Enron to dominate severalmarkets.

Enron often established the prices on those markets, prices that were used to

mark its trades to fair values. Thus, Enron’s traders could establish the prices

at which positions would be valued and, as described below, their compensa-

tion was determined.10

10 As the dominantplayer, Enron took large positions,which made maintaining market

participants’perception that its credit standing was solid absolutely necessary,which is a major

reason that Enron’s accountants went to great lengths to hide its debt obligations, as documente

by Batson (2003a, Appendix Q).

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484475

December31, 2000,Enron assigned a fair value of $125 million to its

Braveheart investment and a profit of $53 million from increasing the invest-

ment to its fair value,even though no sales had been made.Enron recorded

additionalrevenue of$53 million from the venture in the firstquarterof

2001,although Blockbuster did not record any income from the venture and

dissolved the partnership in March 2001.In October 2001 Enron had to

announce publicly that it reversed the $110.9 million in profit it had earlier

claimed,which contributedto its loss of public trust and subsequent

bankruptcy.

How could Enron have so massively misestimated the fair value of its Brav

heart investment, and how could Andersen have allowed Enron to report thes

values and their increases as profits? Indeed, the Examiner in Bankruptcy (Ba

son, 2003a, pp. 30–31) finds that Andersen prepared the appraisal of the pro

ject’svalue.Andersen assumed thefollowing:(1) the businesswould be

established in 10 major metro areas within 12 months;(2) eightnew areas

would be added per year until 2010 and these would each grow at 1% a year

(3) digitalsubscriber lines (DSLs)would be used by 5% of the households,

increasing to 32% by 2010,and these would increase in speed sufficientto

accept the broadcasts;and (4) Braveheart would garner 50% of this market.

After determining (somehow) a net cash flow from each of these households

and discounting by 31–34%, the project was assigned a fair value. I suggest t

this calculation illustrates an essentialweakness of level3 fair-value calcula-

tions that necessarily are not grounded on actualmarket transactions.How

can one determine whether or not such assumptions about a ‘‘first-time’’ pro

ject are ‘‘reasonable’’?

2.8. Derivatives trading

Enron’s (derivatives)trading activities expanded beyond naturalgas and

power contracts to contracts in metals, paper, credit derivatives, and commo

ities.Much of this trading was done over an Internetsystem itdeveloped,

Enron On Line (EOL), which enabled Enron to dominate severalmarkets.

Enron often established the prices on those markets, prices that were used to

mark its trades to fair values. Thus, Enron’s traders could establish the prices

at which positions would be valued and, as described below, their compensa-

tion was determined.10

10 As the dominantplayer, Enron took large positions,which made maintaining market

participants’perception that its credit standing was solid absolutely necessary,which is a major

reason that Enron’s accountants went to great lengths to hide its debt obligations, as documente

by Batson (2003a, Appendix Q).

G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484475

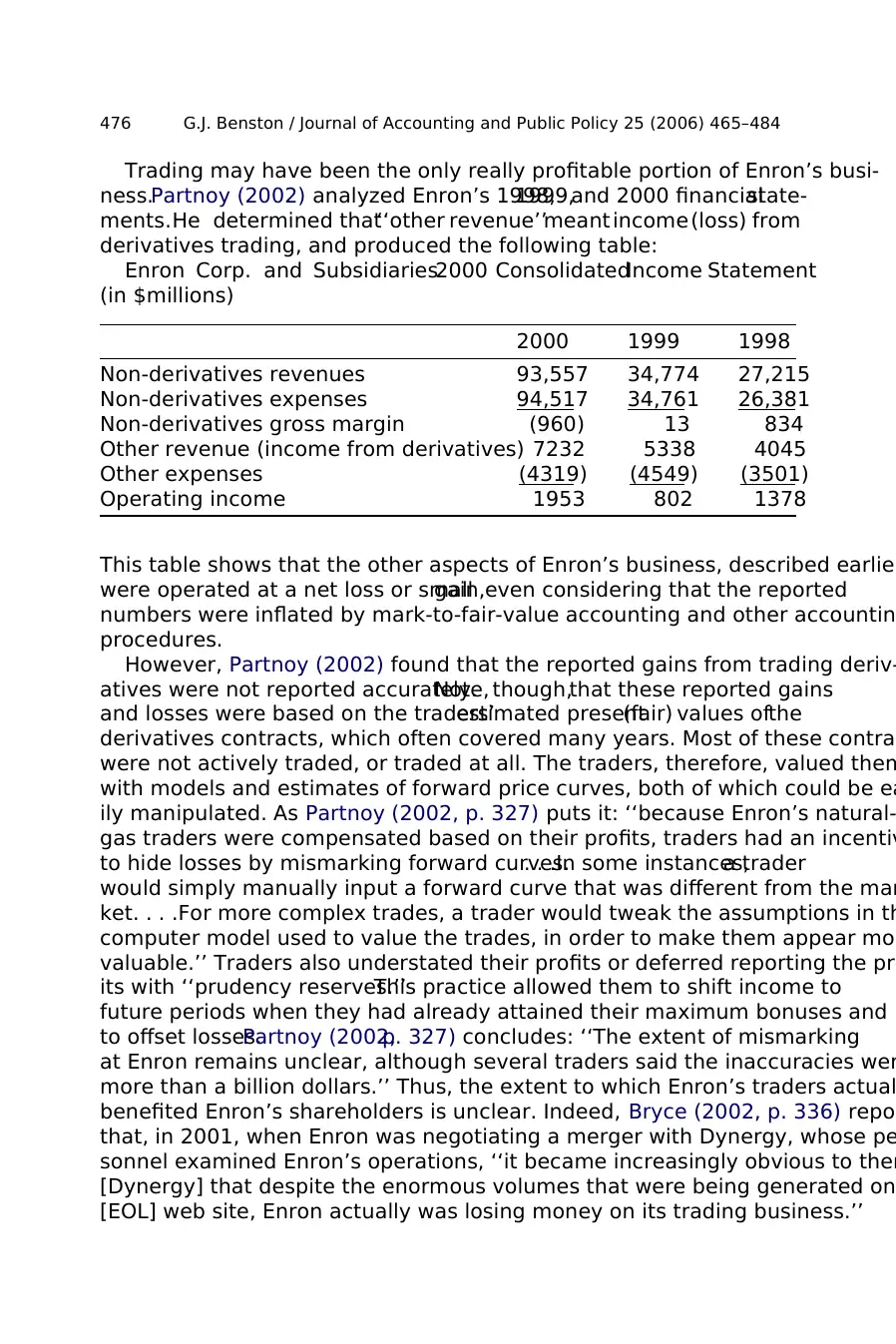

Trading may have been the only really profitable portion of Enron’s busi-

ness.Partnoy (2002) analyzed Enron’s 1998,1999,and 2000 financialstate-

ments.He determined that‘‘other revenue’’meant income (loss) from

derivatives trading, and produced the following table:

Enron Corp. and Subsidiaries2000 ConsolidatedIncome Statement

(in $millions)

2000 1999 1998

Non-derivatives revenues 93,557 34,774 27,215

Non-derivatives expenses 94,517 34,761 26,381

Non-derivatives gross margin (960) 13 834

Other revenue (income from derivatives) 7232 5338 4045

Other expenses (4319) (4549) (3501)

Operating income 1953 802 1378

This table shows that the other aspects of Enron’s business, described earlier

were operated at a net loss or smallgain,even considering that the reported

numbers were inflated by mark-to-fair-value accounting and other accountin

procedures.

However, Partnoy (2002) found that the reported gains from trading deriv-

atives were not reported accurately.Note, though,that these reported gains

and losses were based on the traders’estimated present(fair) values ofthe

derivatives contracts, which often covered many years. Most of these contrac

were not actively traded, or traded at all. The traders, therefore, valued them

with models and estimates of forward price curves, both of which could be ea

ily manipulated. As Partnoy (2002, p. 327) puts it: ‘‘because Enron’s natural-

gas traders were compensated based on their profits, traders had an incentiv

to hide losses by mismarking forward curves.. . .In some instances,a trader

would simply manually input a forward curve that was different from the mar

ket. . . .For more complex trades, a trader would tweak the assumptions in th

computer model used to value the trades, in order to make them appear mor

valuable.’’ Traders also understated their profits or deferred reporting the pro

its with ‘‘prudency reserves.’’This practice allowed them to shift income to

future periods when they had already attained their maximum bonuses and

to offset losses.Partnoy (2002,p. 327) concludes: ‘‘The extent of mismarking

at Enron remains unclear, although several traders said the inaccuracies wer

more than a billion dollars.’’ Thus, the extent to which Enron’s traders actual

benefited Enron’s shareholders is unclear. Indeed, Bryce (2002, p. 336) repor

that, in 2001, when Enron was negotiating a merger with Dynergy, whose pe

sonnel examined Enron’s operations, ‘‘it became increasingly obvious to them

[Dynergy] that despite the enormous volumes that were being generated on

[EOL] web site, Enron actually was losing money on its trading business.’’

476 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

ness.Partnoy (2002) analyzed Enron’s 1998,1999,and 2000 financialstate-

ments.He determined that‘‘other revenue’’meant income (loss) from

derivatives trading, and produced the following table:

Enron Corp. and Subsidiaries2000 ConsolidatedIncome Statement

(in $millions)

2000 1999 1998

Non-derivatives revenues 93,557 34,774 27,215

Non-derivatives expenses 94,517 34,761 26,381

Non-derivatives gross margin (960) 13 834

Other revenue (income from derivatives) 7232 5338 4045

Other expenses (4319) (4549) (3501)

Operating income 1953 802 1378

This table shows that the other aspects of Enron’s business, described earlier

were operated at a net loss or smallgain,even considering that the reported

numbers were inflated by mark-to-fair-value accounting and other accountin

procedures.

However, Partnoy (2002) found that the reported gains from trading deriv-

atives were not reported accurately.Note, though,that these reported gains

and losses were based on the traders’estimated present(fair) values ofthe

derivatives contracts, which often covered many years. Most of these contrac

were not actively traded, or traded at all. The traders, therefore, valued them

with models and estimates of forward price curves, both of which could be ea

ily manipulated. As Partnoy (2002, p. 327) puts it: ‘‘because Enron’s natural-

gas traders were compensated based on their profits, traders had an incentiv

to hide losses by mismarking forward curves.. . .In some instances,a trader

would simply manually input a forward curve that was different from the mar

ket. . . .For more complex trades, a trader would tweak the assumptions in th

computer model used to value the trades, in order to make them appear mor

valuable.’’ Traders also understated their profits or deferred reporting the pro

its with ‘‘prudency reserves.’’This practice allowed them to shift income to

future periods when they had already attained their maximum bonuses and

to offset losses.Partnoy (2002,p. 327) concludes: ‘‘The extent of mismarking

at Enron remains unclear, although several traders said the inaccuracies wer

more than a billion dollars.’’ Thus, the extent to which Enron’s traders actual

benefited Enron’s shareholders is unclear. Indeed, Bryce (2002, p. 336) repor

that, in 2001, when Enron was negotiating a merger with Dynergy, whose pe

sonnel examined Enron’s operations, ‘‘it became increasingly obvious to them

[Dynergy] that despite the enormous volumes that were being generated on

[EOL] web site, Enron actually was losing money on its trading business.’’

476 G.J. Benston / Journal of Accounting and Public Policy 25 (2006) 465–484

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.