ACC320: Contemporary Issues in Accounting - Enron Research

VerifiedAdded on 2022/10/13

|14

|2441

|9

Report

AI Summary

This research proposal delves into the Enron scandal, a landmark case of accounting fraud. The study examines the practical and theoretical motivations behind the scandal, exploring its impact on accountants, investors, and stakeholders. It includes a literature review that analyzes the ethical breaches, failures in corporate governance, and the role of auditing misrepresentation. The proposal outlines the strengths and weaknesses associated with the Enron case. The proposal discusses the hypothesis, including both null and alternative hypotheses, focusing on the positive and negative consequences of the scandal. The positive aspects include the implementation of new regulations and the emphasis on independent auditing. The negative aspects highlight the financial losses, loss of investor confidence, and the company's ultimate collapse. The proposal concludes by referencing key academic sources that support the analysis.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary issues in accounting

Research proposal

Student name

Student ID

Title

Submission date

Contemporary issues in accounting

Research proposal

Student name

Student ID

Title

Submission date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction....................................................................................................................2

Discussion......................................................................................................................2

Practical motivation...................................................................................................2

Theoretical motivation...............................................................................................3

Literature review........................................................................................................3

Hypothesis..................................................................................................................6

References......................................................................................................................8

Appendix......................................................................................................................10

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction....................................................................................................................2

Discussion......................................................................................................................2

Practical motivation...................................................................................................2

Theoretical motivation...............................................................................................3

Literature review........................................................................................................3

Hypothesis..................................................................................................................6

References......................................................................................................................8

Appendix......................................................................................................................10

2

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The study assignment deals with the scandals of Enron which is considered as one of

the biggest accounting fraud of the century. On the other hand the study topic also deals with

different other aspects like practical and theoretical motivation techniques. The literature

review of the aspect also deals with the relation between the practical and theoretical aspects

of the scandal of Enron Company. In the context of the literature review the strength and

weakness of the research area is conducted. The study areas also discusses about the key

hypothesis related to the case study overall. These hypothesis are testable and feasible at the

same time (Usikalu et al.2015).

Discussion

Practical motivation

The Enron scandal had opened the eyes of the whole auditing world. Since company

auditing is a very complex part and therefore requires full concentration and the auditors

ensure that truthfulness of the auditing should be maintained. However the scandal of Enron

had affected the accountants, investors and the company shareholders effectively.

Corporate governance

The board had failed to understand what the management is doing or if they had

understood it, they could have prevent it. The company had clearly manipulated the financial

statement by creating many separate purpose entities which had been managed by the

company officers itself.

Investors

The investors are the part and parcel of the company business. They generally be

quite concerned when the qualified group of Enron had shown themselves woefully

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The study assignment deals with the scandals of Enron which is considered as one of

the biggest accounting fraud of the century. On the other hand the study topic also deals with

different other aspects like practical and theoretical motivation techniques. The literature

review of the aspect also deals with the relation between the practical and theoretical aspects

of the scandal of Enron Company. In the context of the literature review the strength and

weakness of the research area is conducted. The study areas also discusses about the key

hypothesis related to the case study overall. These hypothesis are testable and feasible at the

same time (Usikalu et al.2015).

Discussion

Practical motivation

The Enron scandal had opened the eyes of the whole auditing world. Since company

auditing is a very complex part and therefore requires full concentration and the auditors

ensure that truthfulness of the auditing should be maintained. However the scandal of Enron

had affected the accountants, investors and the company shareholders effectively.

Corporate governance

The board had failed to understand what the management is doing or if they had

understood it, they could have prevent it. The company had clearly manipulated the financial

statement by creating many separate purpose entities which had been managed by the

company officers itself.

Investors

The investors are the part and parcel of the company business. They generally be

quite concerned when the qualified group of Enron had shown themselves woefully

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

inadequate to their risk status. Thus by generalizing the board had caused the investors to

doubt the efficiency of the corporate governance in general.

Accountants and auditors

The accountants are also considered as another vital part of this company. The

company clearly had not maintained the company rules and regulations at the time of

auditing. On the other hand the CEO of this company Mr Andersen had looked for some

alternative ways to do the business which had been unethical. Hence this issue is important to

practise since it had stated clearly about the unethical ways adopted by Enron for auditing

and how it affected the investor and stakeholders (Dibra 2016.).

Theoretical motivation

The theoretical motivation deals with the existing factors which are highly related to

the scandal of Enron Company. Here it is seen that the company had fall due to the auditing

misrepresentation. This had effectively cost huge monitory loss to the company and the share

prices from high had fall down drastically. The practical motivation areas had focused on the

effect to the accountants, investors and stakeholders. Hence due to the auditing

misrepresentation as a result the company management had to stop their operation, many

people had lost their jobs, investors lost their faith to the business and the company had

suffered huge financial crisis. It had forced the ASA to implement new auditing standards.

Literature review

The Enron tragedy had also embedded another tricky which had developed very

apparent in the last year which is Wall Street’s loss of detachment. The investment banks

make good money from “underwriting of shares” in relation to the broker fees. Hence there is

a question of loyalty. Therefore here in this context the research had found key obstacles

which had let the business of Enron to stop. Since the company had faced certain ethical

CONTEMPORARY ISSUES IN ACCOUNTING

inadequate to their risk status. Thus by generalizing the board had caused the investors to

doubt the efficiency of the corporate governance in general.

Accountants and auditors

The accountants are also considered as another vital part of this company. The

company clearly had not maintained the company rules and regulations at the time of

auditing. On the other hand the CEO of this company Mr Andersen had looked for some

alternative ways to do the business which had been unethical. Hence this issue is important to

practise since it had stated clearly about the unethical ways adopted by Enron for auditing

and how it affected the investor and stakeholders (Dibra 2016.).

Theoretical motivation

The theoretical motivation deals with the existing factors which are highly related to

the scandal of Enron Company. Here it is seen that the company had fall due to the auditing

misrepresentation. This had effectively cost huge monitory loss to the company and the share

prices from high had fall down drastically. The practical motivation areas had focused on the

effect to the accountants, investors and stakeholders. Hence due to the auditing

misrepresentation as a result the company management had to stop their operation, many

people had lost their jobs, investors lost their faith to the business and the company had

suffered huge financial crisis. It had forced the ASA to implement new auditing standards.

Literature review

The Enron tragedy had also embedded another tricky which had developed very

apparent in the last year which is Wall Street’s loss of detachment. The investment banks

make good money from “underwriting of shares” in relation to the broker fees. Hence there is

a question of loyalty. Therefore here in this context the research had found key obstacles

which had let the business of Enron to stop. Since the company had faced certain ethical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

issues related to the accounting, investors, and stakeholders. These have been discussed one

by one-

Truthfulness

The first mishap that had occurred in this case had affected the well-being of the

corporation. The older directors had whispered that the company had been the best at

everything they did in order to protect their reputations and alleged for a full compensation.

Hence the duties have been related to the good faith and disclosure. Moreover the companies

had not learned about the stock sale. Hence the bankruptcy caused by the company had

forced them to sell of the business (Markham 2015).

“Conflict of interest”

The “conflict of interest” is another part where the failure of the management of

Enron had occurred. Moreover it is also suggested that enrols compensation policy had

engaged in a narrow-minded focus on the company’s growing and earnings overall. Hence

the recent supervisory fluctuations have focused on the enhancement of bookkeeping

technique related to the internal control system. Thus the “conflict of interest” had been

correlated to the consultant of this scandal. The company had also thought of salvaging the

business of various investors. Furthermore the company scandal had different factors related

to the accounting module. These are as follows-

“Mark to market”

Being a communal concern, Enron had been subjected to the source of power

including the market pressure and error by the private beings including the “auditors”,

“equity analysts” and “credit rating agencies” as a whole. Hence this method requires a long

term convention signing and the amount at which the assets can be sold theoretically to the

future market share price as per the financial statements. (Nguyen 2014).

CONTEMPORARY ISSUES IN ACCOUNTING

issues related to the accounting, investors, and stakeholders. These have been discussed one

by one-

Truthfulness

The first mishap that had occurred in this case had affected the well-being of the

corporation. The older directors had whispered that the company had been the best at

everything they did in order to protect their reputations and alleged for a full compensation.

Hence the duties have been related to the good faith and disclosure. Moreover the companies

had not learned about the stock sale. Hence the bankruptcy caused by the company had

forced them to sell of the business (Markham 2015).

“Conflict of interest”

The “conflict of interest” is another part where the failure of the management of

Enron had occurred. Moreover it is also suggested that enrols compensation policy had

engaged in a narrow-minded focus on the company’s growing and earnings overall. Hence

the recent supervisory fluctuations have focused on the enhancement of bookkeeping

technique related to the internal control system. Thus the “conflict of interest” had been

correlated to the consultant of this scandal. The company had also thought of salvaging the

business of various investors. Furthermore the company scandal had different factors related

to the accounting module. These are as follows-

“Mark to market”

Being a communal concern, Enron had been subjected to the source of power

including the market pressure and error by the private beings including the “auditors”,

“equity analysts” and “credit rating agencies” as a whole. Hence this method requires a long

term convention signing and the amount at which the assets can be sold theoretically to the

future market share price as per the financial statements. (Nguyen 2014).

5

CONTEMPORARY ISSUES IN ACCOUNTING

Special purpose entity

Since the companies share had been co-lateral, the SPE had borrowed large amount of money

which is used to evaluate the overvalued contracts of Enron. On the other hand the company

had also enabled the loan and the properties had laden with the liability obligations into

salary. Thus the routine, liability and the monies purchased by the SPE had actually fraught

large amount of assets which had not conveyed on the pecuniary crash. Hence the past

research related to the scandal of Enron had discussed about the strength and the weakness.

These are as follows-

Strength

The company had not believed of being an overnight energy giant serving multiple of clients.

The triumph comes from marketing and value delivery. Market facilitated the company to

recognize and meet the customer requirements. The duty of any corporate is to carry the

customer worth with a return. The company can utilise the value by fine tuning the delivery

progression and choosing the superior value (Eckhaus and Sheaffer 2018).

Weakness

Failed board of directors

The “board of directors” had simply disastrous in managing the business of the company.

They probably had been more concerned about making profits. Nevertheless beyond all

analysis, board of directors stands big errands for not doing the work correctly. Hence the

board of directors had wrongly monitored the developments inside and outside of the

company by bringing to the management’s attention development.

CONTEMPORARY ISSUES IN ACCOUNTING

Special purpose entity

Since the companies share had been co-lateral, the SPE had borrowed large amount of money

which is used to evaluate the overvalued contracts of Enron. On the other hand the company

had also enabled the loan and the properties had laden with the liability obligations into

salary. Thus the routine, liability and the monies purchased by the SPE had actually fraught

large amount of assets which had not conveyed on the pecuniary crash. Hence the past

research related to the scandal of Enron had discussed about the strength and the weakness.

These are as follows-

Strength

The company had not believed of being an overnight energy giant serving multiple of clients.

The triumph comes from marketing and value delivery. Market facilitated the company to

recognize and meet the customer requirements. The duty of any corporate is to carry the

customer worth with a return. The company can utilise the value by fine tuning the delivery

progression and choosing the superior value (Eckhaus and Sheaffer 2018).

Weakness

Failed board of directors

The “board of directors” had simply disastrous in managing the business of the company.

They probably had been more concerned about making profits. Nevertheless beyond all

analysis, board of directors stands big errands for not doing the work correctly. Hence the

board of directors had wrongly monitored the developments inside and outside of the

company by bringing to the management’s attention development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

Evaluation and influence

A board is expected to examine the management offers, decisions, settle or upset with them

by giving advices and offering some submissions and sketch certain objectives. Hence the

company probably had been in need of monitoring the business of the company (Pai. and

Tolleson 2015.).

Hypothesis

There are two types of hypothesis had been considered to demonstrate the case? These are

as follows-

Null hypothesis

Alternate hypothesis

The null hypothesis means void which does not generate any effective outcomes in terms

of discussion. On the other hand the alternative hypothesis is used to deal with the positive

and negative aspects relating to the research study aspect. Here for the case of Enron, the

alternative hypothesis had been used (Hardin et al.2015). The main focus is on the positive

and negative effects on the Enron scandal. The positive areas surely had been related to the

after effects of the scandals. Hence after this scandal many new government rules and

regulations had been implemented so that no such scandals gets to occur again. Secondly the

government had given special attraction to conduct independent auditing. It is the

responsibility of the company to let the auditor to conduct auditing effectively and efficiently

where the auditor could perform the audit as per company rules and regulations as a whole

(Ailon 2015.).

CONTEMPORARY ISSUES IN ACCOUNTING

Evaluation and influence

A board is expected to examine the management offers, decisions, settle or upset with them

by giving advices and offering some submissions and sketch certain objectives. Hence the

company probably had been in need of monitoring the business of the company (Pai. and

Tolleson 2015.).

Hypothesis

There are two types of hypothesis had been considered to demonstrate the case? These are

as follows-

Null hypothesis

Alternate hypothesis

The null hypothesis means void which does not generate any effective outcomes in terms

of discussion. On the other hand the alternative hypothesis is used to deal with the positive

and negative aspects relating to the research study aspect. Here for the case of Enron, the

alternative hypothesis had been used (Hardin et al.2015). The main focus is on the positive

and negative effects on the Enron scandal. The positive areas surely had been related to the

after effects of the scandals. Hence after this scandal many new government rules and

regulations had been implemented so that no such scandals gets to occur again. Secondly the

government had given special attraction to conduct independent auditing. It is the

responsibility of the company to let the auditor to conduct auditing effectively and efficiently

where the auditor could perform the audit as per company rules and regulations as a whole

(Ailon 2015.).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

On the other hand there are also some negative effects related to the auditing of the

company. It is seen that the company had made certain mistakes for which they had lost all

the plot. Further it is also seen that due to this mishap, the company had lost all its potential

investors, stakeholders and most importantly their client market. This had been taken as a big

loss to the company where they had no opportunity to get up from. Thus the share price of the

company had fall down drastically which had also been considered as a major failure to the

company. In this way it can be said that the company had lost their major market of Australia.

Thus this in turn had made the company stop their overall corporate.

CONTEMPORARY ISSUES IN ACCOUNTING

On the other hand there are also some negative effects related to the auditing of the

company. It is seen that the company had made certain mistakes for which they had lost all

the plot. Further it is also seen that due to this mishap, the company had lost all its potential

investors, stakeholders and most importantly their client market. This had been taken as a big

loss to the company where they had no opportunity to get up from. Thus the share price of the

company had fall down drastically which had also been considered as a major failure to the

company. In this way it can be said that the company had lost their major market of Australia.

Thus this in turn had made the company stop their overall corporate.

8

CONTEMPORARY ISSUES IN ACCOUNTING

References

Ailon, G., 2015. From superstars to devils: The ethical discourse on managerial figures

involved in a corporate scandal. Organization, 22(1), pp.78-99.

Broberg, P., Umans, T., Skog, P. and Theodorsson, E., 2018. Auditors’ professional and

organizational identities and commercialization in audit firms. Accounting, Auditing &

Accountability Journal, 31(2), pp.374-399.

Dibra, R., 2016. Corporate Governance failure: the case of Enron and Parmalat. European

Scientific Journal, 12(16).

Eckhaus, E. and Sheaffer, Z., 2018. Managerial hubris detection: the case of Enron. Risk

Management, 20(4), pp.304-325.

Hardin, J.S., Sarkis, G. and Urc, P.C., 2015. Network analysis with the enron email

corpus. Journal of Statistics Education, 23(2).

Markham, J.W., 2015. A financial history of modern US corporate scandals: From Enron to

reform. Routledge.

Mattern, S., 2015. Mission control: A history of the urban dashboard. Places Journal.

Nguyen, T.N., 2014. A different approach to information management by exceptions (toward

the prevention of another Enron). Information & Management, 51(1), pp.165-176.

Pai, K. and Tolleson, T.D., 2015. India's Satyam Scandal: Evidence the Too Large to Indict

Mindset of Accounting Regulators Is a Global Phenomenon. Review of Business & Finance

Studies, 6(2), p.35.

CONTEMPORARY ISSUES IN ACCOUNTING

References

Ailon, G., 2015. From superstars to devils: The ethical discourse on managerial figures

involved in a corporate scandal. Organization, 22(1), pp.78-99.

Broberg, P., Umans, T., Skog, P. and Theodorsson, E., 2018. Auditors’ professional and

organizational identities and commercialization in audit firms. Accounting, Auditing &

Accountability Journal, 31(2), pp.374-399.

Dibra, R., 2016. Corporate Governance failure: the case of Enron and Parmalat. European

Scientific Journal, 12(16).

Eckhaus, E. and Sheaffer, Z., 2018. Managerial hubris detection: the case of Enron. Risk

Management, 20(4), pp.304-325.

Hardin, J.S., Sarkis, G. and Urc, P.C., 2015. Network analysis with the enron email

corpus. Journal of Statistics Education, 23(2).

Markham, J.W., 2015. A financial history of modern US corporate scandals: From Enron to

reform. Routledge.

Mattern, S., 2015. Mission control: A history of the urban dashboard. Places Journal.

Nguyen, T.N., 2014. A different approach to information management by exceptions (toward

the prevention of another Enron). Information & Management, 51(1), pp.165-176.

Pai, K. and Tolleson, T.D., 2015. India's Satyam Scandal: Evidence the Too Large to Indict

Mindset of Accounting Regulators Is a Global Phenomenon. Review of Business & Finance

Studies, 6(2), p.35.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

Roy, M.N., 2015. Statutory Auditors' Independence in the Context of Corporate Accounting

Scandal: A Comparative Study of Enron and Satyam. IUP Journal of Accounting Research &

Audit Practices, 14(2), p.7.

Usikalu, O., Ogunleye, A.J. and Effiong, J., 2015. Organizational Trust, Job Satisfaction and

Job Performance Among Teachers in Ekiti State, Nigeria. British Open Journal of

Psychology, 1(1), pp.1-10.

CONTEMPORARY ISSUES IN ACCOUNTING

Roy, M.N., 2015. Statutory Auditors' Independence in the Context of Corporate Accounting

Scandal: A Comparative Study of Enron and Satyam. IUP Journal of Accounting Research &

Audit Practices, 14(2), p.7.

Usikalu, O., Ogunleye, A.J. and Effiong, J., 2015. Organizational Trust, Job Satisfaction and

Job Performance Among Teachers in Ekiti State, Nigeria. British Open Journal of

Psychology, 1(1), pp.1-10.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

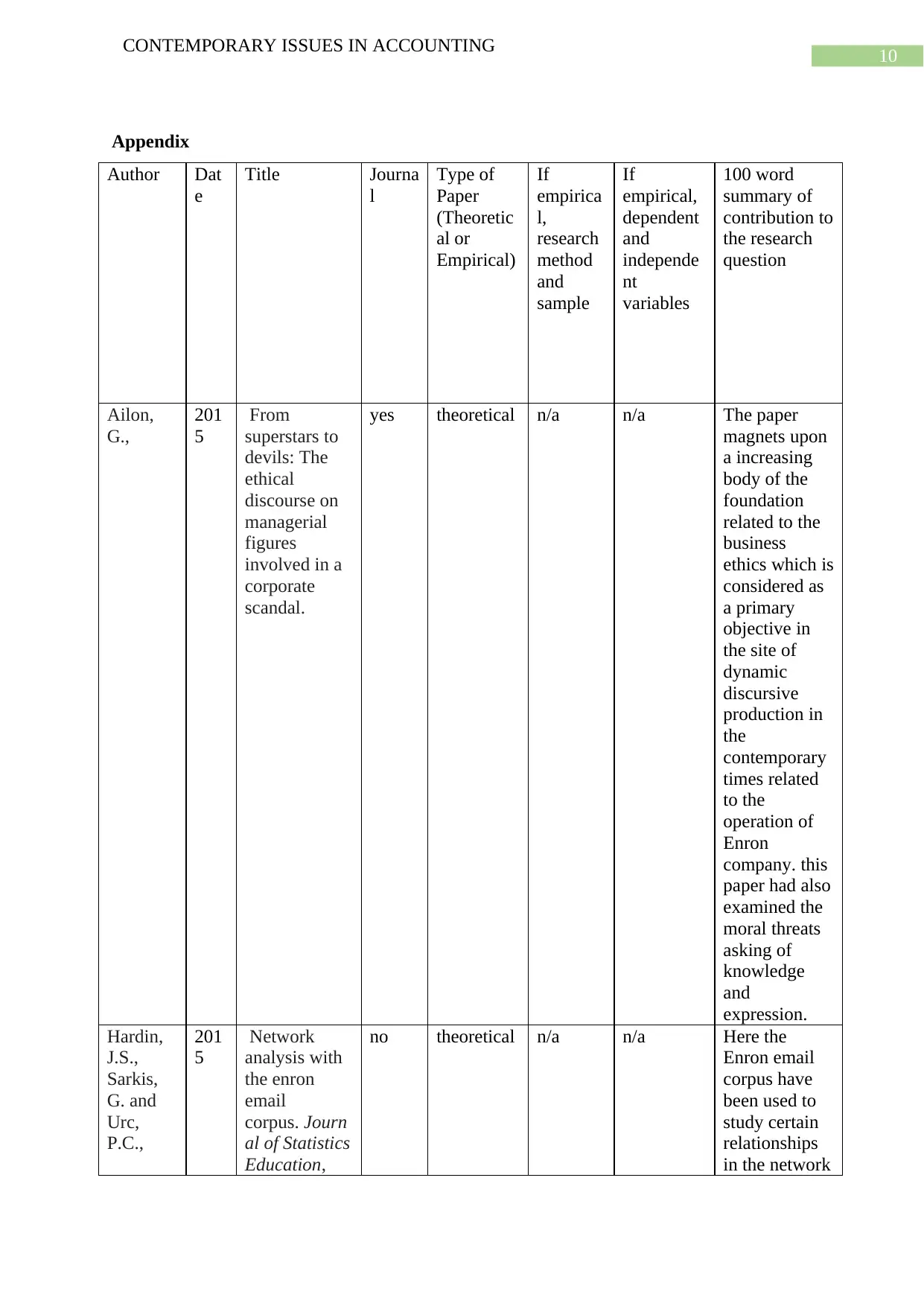

Appendix

Author Dat

e

Title Journa

l

Type of

Paper

(Theoretic

al or

Empirical)

If

empirica

l,

research

method

and

sample

If

empirical,

dependent

and

independe

nt

variables

100 word

summary of

contribution to

the research

question

Ailon,

G.,

201

5

From

superstars to

devils: The

ethical

discourse on

managerial

figures

involved in a

corporate

scandal.

yes theoretical n/a n/a The paper

magnets upon

a increasing

body of the

foundation

related to the

business

ethics which is

considered as

a primary

objective in

the site of

dynamic

discursive

production in

the

contemporary

times related

to the

operation of

Enron

company. this

paper had also

examined the

moral threats

asking of

knowledge

and

expression.

Hardin,

J.S.,

Sarkis,

G. and

Urc,

P.C.,

201

5

Network

analysis with

the enron

email

corpus. Journ

al of Statistics

Education,

no theoretical n/a n/a Here the

Enron email

corpus have

been used to

study certain

relationships

in the network

CONTEMPORARY ISSUES IN ACCOUNTING

Appendix

Author Dat

e

Title Journa

l

Type of

Paper

(Theoretic

al or

Empirical)

If

empirica

l,

research

method

and

sample

If

empirical,

dependent

and

independe

nt

variables

100 word

summary of

contribution to

the research

question

Ailon,

G.,

201

5

From

superstars to

devils: The

ethical

discourse on

managerial

figures

involved in a

corporate

scandal.

yes theoretical n/a n/a The paper

magnets upon

a increasing

body of the

foundation

related to the

business

ethics which is

considered as

a primary

objective in

the site of

dynamic

discursive

production in

the

contemporary

times related

to the

operation of

Enron

company. this

paper had also

examined the

moral threats

asking of

knowledge

and

expression.

Hardin,

J.S.,

Sarkis,

G. and

Urc,

P.C.,

201

5

Network

analysis with

the enron

corpus. Journ

al of Statistics

Education,

no theoretical n/a n/a Here the

Enron email

corpus have

been used to

study certain

relationships

in the network

11

CONTEMPORARY ISSUES IN ACCOUNTING

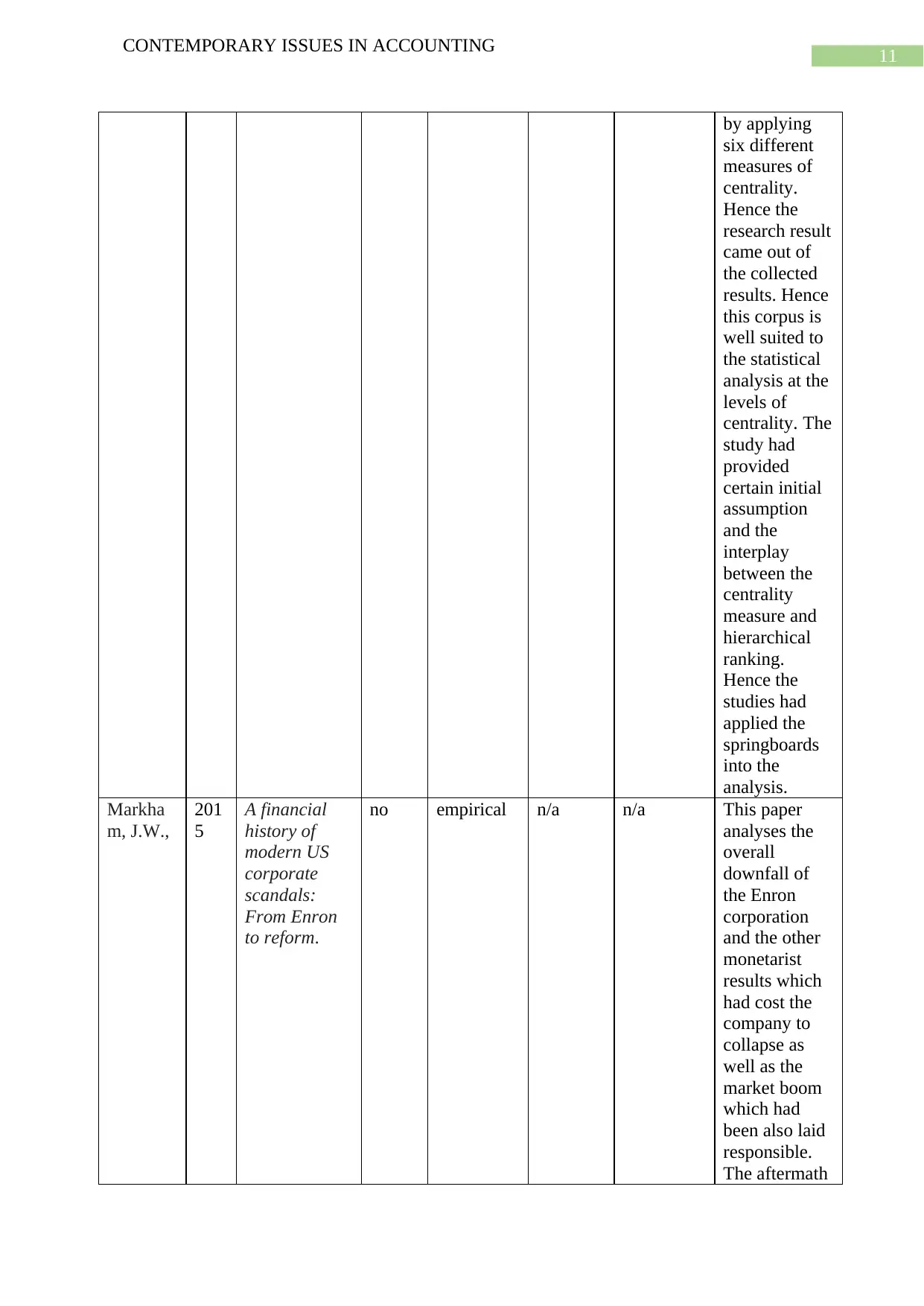

by applying

six different

measures of

centrality.

Hence the

research result

came out of

the collected

results. Hence

this corpus is

well suited to

the statistical

analysis at the

levels of

centrality. The

study had

provided

certain initial

assumption

and the

interplay

between the

centrality

measure and

hierarchical

ranking.

Hence the

studies had

applied the

springboards

into the

analysis.

Markha

m, J.W.,

201

5

A financial

history of

modern US

corporate

scandals:

From Enron

to reform.

no empirical n/a n/a This paper

analyses the

overall

downfall of

the Enron

corporation

and the other

monetarist

results which

had cost the

company to

collapse as

well as the

market boom

which had

been also laid

responsible.

The aftermath

CONTEMPORARY ISSUES IN ACCOUNTING

by applying

six different

measures of

centrality.

Hence the

research result

came out of

the collected

results. Hence

this corpus is

well suited to

the statistical

analysis at the

levels of

centrality. The

study had

provided

certain initial

assumption

and the

interplay

between the

centrality

measure and

hierarchical

ranking.

Hence the

studies had

applied the

springboards

into the

analysis.

Markha

m, J.W.,

201

5

A financial

history of

modern US

corporate

scandals:

From Enron

to reform.

no empirical n/a n/a This paper

analyses the

overall

downfall of

the Enron

corporation

and the other

monetarist

results which

had cost the

company to

collapse as

well as the

market boom

which had

been also laid

responsible.

The aftermath

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.