FINANCE 10: Corporate and Financial Accounting Equity and Liabilities

VerifiedAdded on 2022/11/17

|16

|2769

|210

Report

AI Summary

This report delves into the concepts of equity and liabilities within corporate and financial accounting. It examines the fluctuations in equity and liabilities over a three-year period, focusing on the ANZ Bank and Commonwealth Bank. The report is divided into two parts: Part A analyzes equity and liabilities, including ordinary share capital, retained earnings, and non-controlling interests. It also covers key items reported under liabilities, such as deposits, payables, and debt issues. Part B discusses the characteristics and compliance requirements of small and large proprietary companies, along with the concept of a reporting entity. The analysis includes the advantages of debt, equity, and cash equivalents as funding sources. The report highlights key financial aspects, providing insights into the financial positions of the companies and the importance of financial reporting for understanding the business's performance. The report concludes with a summary of the findings and their implications.

Corporate and Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 1

Executive Summary

The main aim of this paper is to understand the concept of equity and liabilities. In this paper, the

fluctuation of equity and liabilities in three years will be discussed. This paper is divided in two

parts such as Part A and Part B. In Part A, the liabilities and equity has been discussed in the last

three years. According to analysis of ANZ Bank and Common wealth Bank will be discussed. In

Part B, small proprietary, large proprietary are the terms that are discussed in the report.

Executive Summary

The main aim of this paper is to understand the concept of equity and liabilities. In this paper, the

fluctuation of equity and liabilities in three years will be discussed. This paper is divided in two

parts such as Part A and Part B. In Part A, the liabilities and equity has been discussed in the last

three years. According to analysis of ANZ Bank and Common wealth Bank will be discussed. In

Part B, small proprietary, large proprietary are the terms that are discussed in the report.

FINANCE 2

Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Part B.............................................................................................................................................10

Small proprietary........................................................................................................................10

Compliance................................................................................................................................10

Large proprietary........................................................................................................................11

Reporting entity..........................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Part B.............................................................................................................................................10

Small proprietary........................................................................................................................10

Compliance................................................................................................................................10

Large proprietary........................................................................................................................11

Reporting entity..........................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 3

Introduction

In this paper, the discussion is made on the concept “corporate and financial accounting”. The

report is divided into two parts such as Part A and Part B. In Part A, there are five 5 questions

that has been attempted related to the equities and liabilities. In Part B, the concept of small

proprietary and large proprietary company has been discussed.

Part A

1. Ordinary share capital, retained earnings, reserves and non-controlling interests are contained

under the heading of owner’s heading. Reserves defines the credit balance which is set aside for

a specific purpose and that cannot be used for further reasons. Retained earnings are the profits

an organization earned on date, by subtracting the dividends or other distributions payments to

external parties such as investors (Geddes, 2017). Ordinary share capital is the amount of money

that is raised by a corporate from public and private sources through the issues of its common

shares. Non-controlling interests is an ownership position in which the shareholders have less

than 50% of outstanding shares and those also not have any control over decision.

2. ANZ Bank is the Australia and New Zealand Banking Group Limited which is commonly

called ANZ. It is Australian multinational banking and financial services firm which is

established in Australia (ANZ, 2018).

The Commonwealth Bank is an Australian Bank which operates at the international level. It is an

multinational bank which operates across New Zealand, the United States, Asia and the United

Kingdom (The Commonwealth, 2018).

Introduction

In this paper, the discussion is made on the concept “corporate and financial accounting”. The

report is divided into two parts such as Part A and Part B. In Part A, there are five 5 questions

that has been attempted related to the equities and liabilities. In Part B, the concept of small

proprietary and large proprietary company has been discussed.

Part A

1. Ordinary share capital, retained earnings, reserves and non-controlling interests are contained

under the heading of owner’s heading. Reserves defines the credit balance which is set aside for

a specific purpose and that cannot be used for further reasons. Retained earnings are the profits

an organization earned on date, by subtracting the dividends or other distributions payments to

external parties such as investors (Geddes, 2017). Ordinary share capital is the amount of money

that is raised by a corporate from public and private sources through the issues of its common

shares. Non-controlling interests is an ownership position in which the shareholders have less

than 50% of outstanding shares and those also not have any control over decision.

2. ANZ Bank is the Australia and New Zealand Banking Group Limited which is commonly

called ANZ. It is Australian multinational banking and financial services firm which is

established in Australia (ANZ, 2018).

The Commonwealth Bank is an Australian Bank which operates at the international level. It is an

multinational bank which operates across New Zealand, the United States, Asia and the United

Kingdom (The Commonwealth, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 4

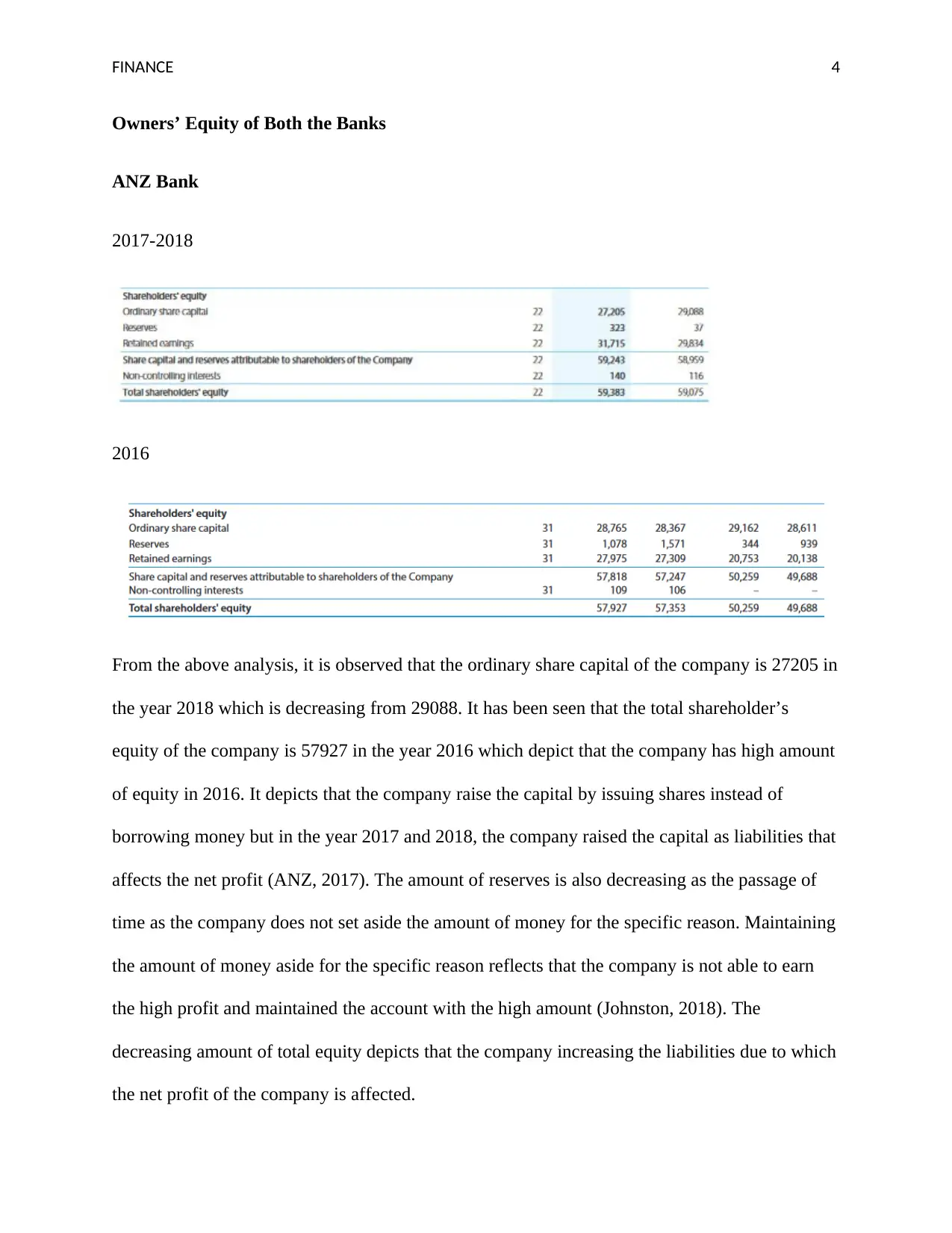

Owners’ Equity of Both the Banks

ANZ Bank

2017-2018

2016

From the above analysis, it is observed that the ordinary share capital of the company is 27205 in

the year 2018 which is decreasing from 29088. It has been seen that the total shareholder’s

equity of the company is 57927 in the year 2016 which depict that the company has high amount

of equity in 2016. It depicts that the company raise the capital by issuing shares instead of

borrowing money but in the year 2017 and 2018, the company raised the capital as liabilities that

affects the net profit (ANZ, 2017). The amount of reserves is also decreasing as the passage of

time as the company does not set aside the amount of money for the specific reason. Maintaining

the amount of money aside for the specific reason reflects that the company is not able to earn

the high profit and maintained the account with the high amount (Johnston, 2018). The

decreasing amount of total equity depicts that the company increasing the liabilities due to which

the net profit of the company is affected.

Owners’ Equity of Both the Banks

ANZ Bank

2017-2018

2016

From the above analysis, it is observed that the ordinary share capital of the company is 27205 in

the year 2018 which is decreasing from 29088. It has been seen that the total shareholder’s

equity of the company is 57927 in the year 2016 which depict that the company has high amount

of equity in 2016. It depicts that the company raise the capital by issuing shares instead of

borrowing money but in the year 2017 and 2018, the company raised the capital as liabilities that

affects the net profit (ANZ, 2017). The amount of reserves is also decreasing as the passage of

time as the company does not set aside the amount of money for the specific reason. Maintaining

the amount of money aside for the specific reason reflects that the company is not able to earn

the high profit and maintained the account with the high amount (Johnston, 2018). The

decreasing amount of total equity depicts that the company increasing the liabilities due to which

the net profit of the company is affected.

FINANCE 5

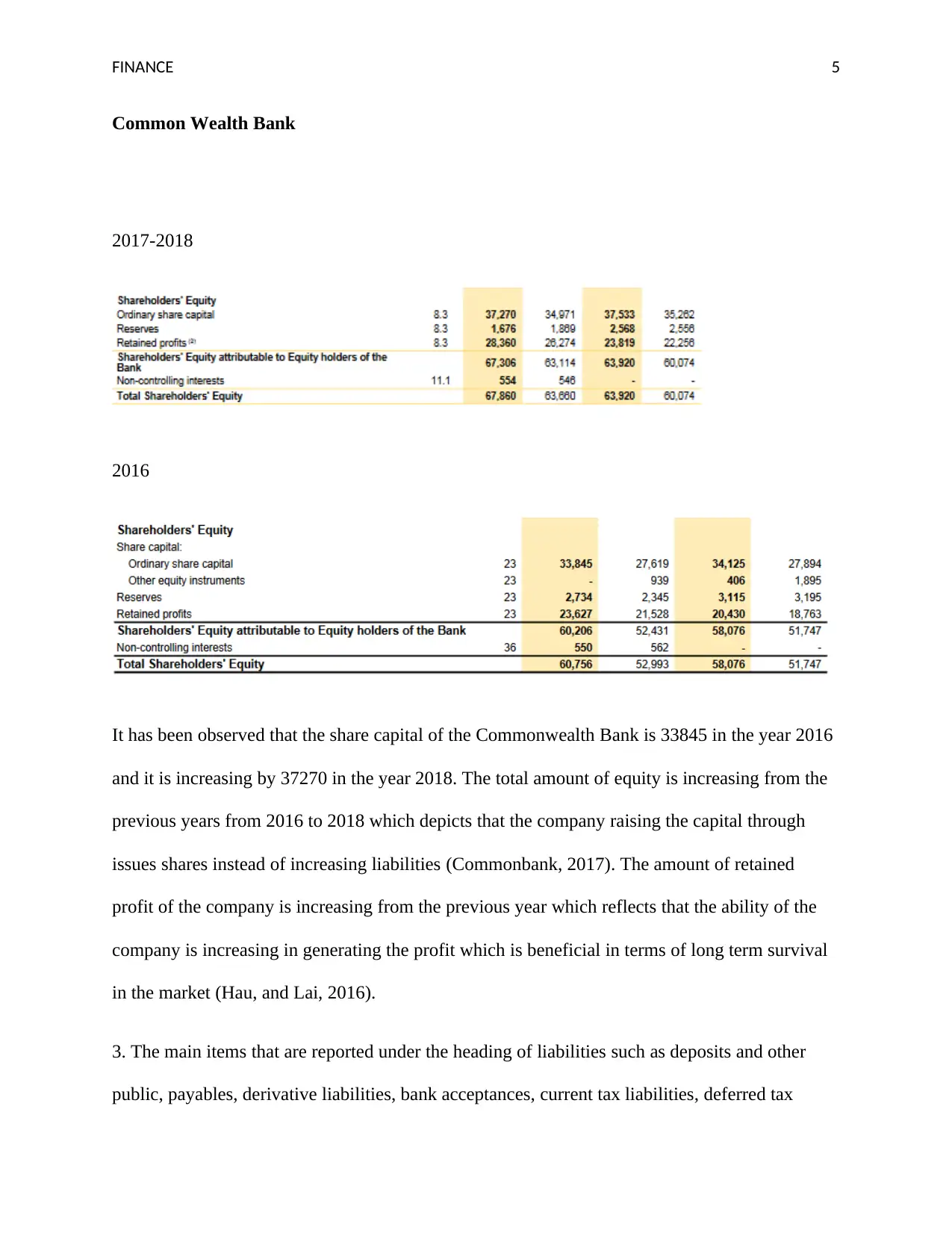

Common Wealth Bank

2017-2018

2016

It has been observed that the share capital of the Commonwealth Bank is 33845 in the year 2016

and it is increasing by 37270 in the year 2018. The total amount of equity is increasing from the

previous years from 2016 to 2018 which depicts that the company raising the capital through

issues shares instead of increasing liabilities (Commonbank, 2017). The amount of retained

profit of the company is increasing from the previous year which reflects that the ability of the

company is increasing in generating the profit which is beneficial in terms of long term survival

in the market (Hau, and Lai, 2016).

3. The main items that are reported under the heading of liabilities such as deposits and other

public, payables, derivative liabilities, bank acceptances, current tax liabilities, deferred tax

Common Wealth Bank

2017-2018

2016

It has been observed that the share capital of the Commonwealth Bank is 33845 in the year 2016

and it is increasing by 37270 in the year 2018. The total amount of equity is increasing from the

previous years from 2016 to 2018 which depicts that the company raising the capital through

issues shares instead of increasing liabilities (Commonbank, 2017). The amount of retained

profit of the company is increasing from the previous year which reflects that the ability of the

company is increasing in generating the profit which is beneficial in terms of long term survival

in the market (Hau, and Lai, 2016).

3. The main items that are reported under the heading of liabilities such as deposits and other

public, payables, derivative liabilities, bank acceptances, current tax liabilities, deferred tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 6

liabilities, insurance policy liabilities, debt issues, bills payable and the others. Derivative

Liabilities means the net liabilities of the borrowers under all derivatives which is determined on

a mark to market basis. Deferred Tax Liabilities defines the income tax expense which is greater

than the taxes payable and the differences are expected to reverse in the future. Debt issues

define the financial obligation that allows the issuers to arise the funds by promising to repay the

lender at the initial stage in the future. Bills Payable is a paper which shows the amount owed for

goods or services that are received on credit. Liability insurance is a part of the general insurance

system which is risk facing to protect the purchaser from the risk of liabilities.

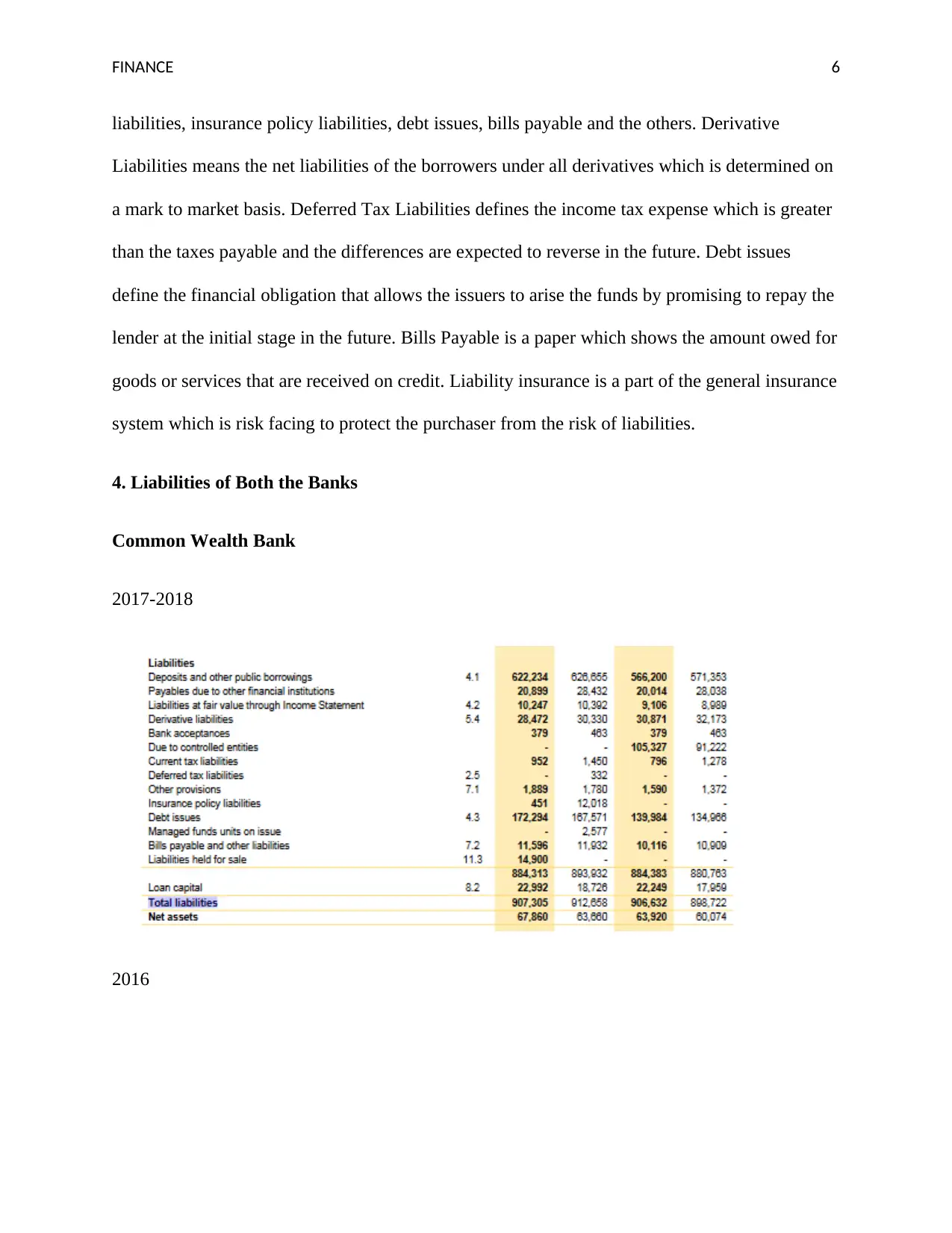

4. Liabilities of Both the Banks

Common Wealth Bank

2017-2018

2016

liabilities, insurance policy liabilities, debt issues, bills payable and the others. Derivative

Liabilities means the net liabilities of the borrowers under all derivatives which is determined on

a mark to market basis. Deferred Tax Liabilities defines the income tax expense which is greater

than the taxes payable and the differences are expected to reverse in the future. Debt issues

define the financial obligation that allows the issuers to arise the funds by promising to repay the

lender at the initial stage in the future. Bills Payable is a paper which shows the amount owed for

goods or services that are received on credit. Liability insurance is a part of the general insurance

system which is risk facing to protect the purchaser from the risk of liabilities.

4. Liabilities of Both the Banks

Common Wealth Bank

2017-2018

2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 7

The liabilities side of balance sheet of the company depicts that the liabilities of the company is

increasing in the year 2017 and 2018 from the previous year 2016 (Commonbank, 2018). The

total liability of the company is increasing as the company raises the capital by borrowing the

amount on liabilities. As per the analysis, it has been seen that the company has to mainly focus

on its liabilities. The amount of total liabilities of the bank is increasing due to increasing the

deposits and the other public borrowings. The liabilities such as derivative liabilities and the

others are the major liabilities that directly increasing the liabilities of the company. It is

observed that the derivative liability of the company is decreasing from 2016 to 2018 such as

39921 to 28472 (Commonbank, 2016). The amount of total liabilities is 60756 in the year 2018

but in the year 2016, the total liability of the company is 872322. Decreasing liabilities in the

financial report depicts the positive sign for the company.

ANZ Bank

2017-2018

The liabilities side of balance sheet of the company depicts that the liabilities of the company is

increasing in the year 2017 and 2018 from the previous year 2016 (Commonbank, 2018). The

total liability of the company is increasing as the company raises the capital by borrowing the

amount on liabilities. As per the analysis, it has been seen that the company has to mainly focus

on its liabilities. The amount of total liabilities of the bank is increasing due to increasing the

deposits and the other public borrowings. The liabilities such as derivative liabilities and the

others are the major liabilities that directly increasing the liabilities of the company. It is

observed that the derivative liability of the company is decreasing from 2016 to 2018 such as

39921 to 28472 (Commonbank, 2016). The amount of total liabilities is 60756 in the year 2018

but in the year 2016, the total liability of the company is 872322. Decreasing liabilities in the

financial report depicts the positive sign for the company.

ANZ Bank

2017-2018

FINANCE 8

2016

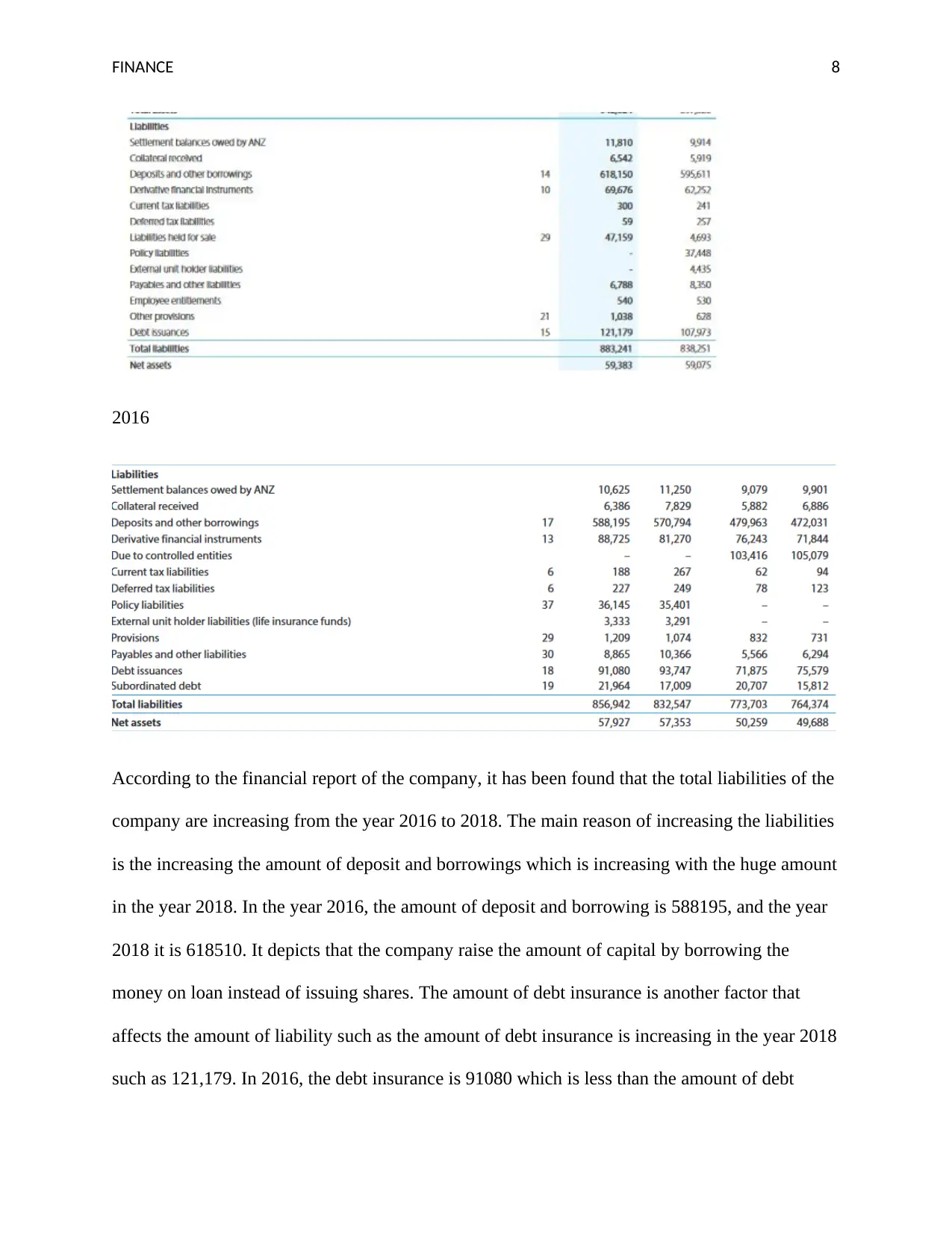

According to the financial report of the company, it has been found that the total liabilities of the

company are increasing from the year 2016 to 2018. The main reason of increasing the liabilities

is the increasing the amount of deposit and borrowings which is increasing with the huge amount

in the year 2018. In the year 2016, the amount of deposit and borrowing is 588195, and the year

2018 it is 618510. It depicts that the company raise the amount of capital by borrowing the

money on loan instead of issuing shares. The amount of debt insurance is another factor that

affects the amount of liability such as the amount of debt insurance is increasing in the year 2018

such as 121,179. In 2016, the debt insurance is 91080 which is less than the amount of debt

2016

According to the financial report of the company, it has been found that the total liabilities of the

company are increasing from the year 2016 to 2018. The main reason of increasing the liabilities

is the increasing the amount of deposit and borrowings which is increasing with the huge amount

in the year 2018. In the year 2016, the amount of deposit and borrowing is 588195, and the year

2018 it is 618510. It depicts that the company raise the amount of capital by borrowing the

money on loan instead of issuing shares. The amount of debt insurance is another factor that

affects the amount of liability such as the amount of debt insurance is increasing in the year 2018

such as 121,179. In 2016, the debt insurance is 91080 which is less than the amount of debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 9

insurance in the year 2018. Increasing debt insurance reflects that the company takes the money

from the different financial institutions. The liability of Common Wealth Bank is increasing

which indicates that the company faces the challenges due to financial crisis as the amount of

debt is increasing (ANZ, 2018).

As per the above analysis of movements in liabilities, it is observed the liabilities of both the

companies are increasing which reflects the negative sign for the companies. But it can be said

that the ANZ banks has less liability as compare to the Commonwealth Bank.

5.

Advantages of Funds

It has been found that both the companies use the debts, equity, and cash and cash equivalents.

These are the funds that the companies use to raise the capital that helps to operate the business

smoothly in the market. These funds are very essential for the companies to raise the capital and

these are:

Debts: It is observed that the company takes the loan from outside or also borrow the money on

liabilities. This fund helps the organization to raise the capital in order to purchase the fixed

assets and current assets. It helps to operate smoothly in the market (Merz, and Overesch, 2016).

Equity: Equity is also a type of fund that helps to raise the capital. It is suggesting that the

company has to raise the capital by issuing shares so that the liabilities of the company are

reducing and it can easily operate the business. It is a fact that the company can pay the dividend

amount as per their profit and it is not liable to pay the amount which is invested by the

shareholders (Boquist, Racette, and Schlarbaum, 2017).

insurance in the year 2018. Increasing debt insurance reflects that the company takes the money

from the different financial institutions. The liability of Common Wealth Bank is increasing

which indicates that the company faces the challenges due to financial crisis as the amount of

debt is increasing (ANZ, 2018).

As per the above analysis of movements in liabilities, it is observed the liabilities of both the

companies are increasing which reflects the negative sign for the companies. But it can be said

that the ANZ banks has less liability as compare to the Commonwealth Bank.

5.

Advantages of Funds

It has been found that both the companies use the debts, equity, and cash and cash equivalents.

These are the funds that the companies use to raise the capital that helps to operate the business

smoothly in the market. These funds are very essential for the companies to raise the capital and

these are:

Debts: It is observed that the company takes the loan from outside or also borrow the money on

liabilities. This fund helps the organization to raise the capital in order to purchase the fixed

assets and current assets. It helps to operate smoothly in the market (Merz, and Overesch, 2016).

Equity: Equity is also a type of fund that helps to raise the capital. It is suggesting that the

company has to raise the capital by issuing shares so that the liabilities of the company are

reducing and it can easily operate the business. It is a fact that the company can pay the dividend

amount as per their profit and it is not liable to pay the amount which is invested by the

shareholders (Boquist, Racette, and Schlarbaum, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 10

Cash and Cash Equivalent: Cash and cash equivalent is the amount which the company always

maintained in their hands in order to pay all short term liabilities or expenses during the period. It

helps the organization to pay the daily routine or short term expenses which is essential to pay

while operating the business.

Part B

Small proprietary

Small proprietary define the organizations that operate the business in the small area with the

limited people. Small proprietary should be followed some areas in order to consider the small

organization. There are several rules which are to be followed or complied with in order to

classify the proprietary company into a small one. The criteria have been listed below and the

rules have been outlined below.

The first criteria of considering the organization as small enterprises are the money. It has

been evaluated that the amount assets of the company should be less than $12.5 million

are there at the end of the financial year.

The second criteria are based on the staff members. The company should have the

maximum 50 number of employees or fewer than 50 at the end of the accounting period

The third criteria are based on operating revenue. The gross operating revenue of the

company is not more than $25 million for the financial year (Berisha, and Pula, 2015).

Compliance

The compliance that is required to be followed by small proprietary company starts with the

preparation of the financial report, which is prepared in accordance with the rules listed in Pt

Cash and Cash Equivalent: Cash and cash equivalent is the amount which the company always

maintained in their hands in order to pay all short term liabilities or expenses during the period. It

helps the organization to pay the daily routine or short term expenses which is essential to pay

while operating the business.

Part B

Small proprietary

Small proprietary define the organizations that operate the business in the small area with the

limited people. Small proprietary should be followed some areas in order to consider the small

organization. There are several rules which are to be followed or complied with in order to

classify the proprietary company into a small one. The criteria have been listed below and the

rules have been outlined below.

The first criteria of considering the organization as small enterprises are the money. It has

been evaluated that the amount assets of the company should be less than $12.5 million

are there at the end of the financial year.

The second criteria are based on the staff members. The company should have the

maximum 50 number of employees or fewer than 50 at the end of the accounting period

The third criteria are based on operating revenue. The gross operating revenue of the

company is not more than $25 million for the financial year (Berisha, and Pula, 2015).

Compliance

The compliance that is required to be followed by small proprietary company starts with the

preparation of the financial report, which is prepared in accordance with the rules listed in Pt

FINANCE 11

2M.3 of the Corporations Act 2001 under section 294(1). It is also required to audit if ASIC

requests

Large proprietary

The large proprietary companies are defined as large companies who operate at the global level

or large area. There are three areas or criteria are that the large company has to be satisfied for

the consideration of large proprietary and these are below:

The first one is based on the total revenue of the company. When the sales for the

financial year exceeds the entities and it controls the $50 million or more, the value of the

consolidated gross assets are more than $25 million or more in case of the company or

the entity.

Another factor that should be fulfilled for considering the company as the large

proprietary and that is based on number of employees. It has been evaluated that the

company and any other entity should have the 100 staff members at the end of the

reporting period.

The last factor that should the company has to fulfill for considering the large company

and that is compliance. Compliance: As per ASIC, the large proprietary companies are

required to file a financial report and the report of the directors for every accounting year.

These accounts must also be audited until the grant is received from ASIC (Dias,

Rodrigues, Craig, and Neves, 2019).

Reporting entity

The reporting entity is an entity that is considered as the entity which is having different users

which are relying on the general purpose financial statements to gain an understanding of the

2M.3 of the Corporations Act 2001 under section 294(1). It is also required to audit if ASIC

requests

Large proprietary

The large proprietary companies are defined as large companies who operate at the global level

or large area. There are three areas or criteria are that the large company has to be satisfied for

the consideration of large proprietary and these are below:

The first one is based on the total revenue of the company. When the sales for the

financial year exceeds the entities and it controls the $50 million or more, the value of the

consolidated gross assets are more than $25 million or more in case of the company or

the entity.

Another factor that should be fulfilled for considering the company as the large

proprietary and that is based on number of employees. It has been evaluated that the

company and any other entity should have the 100 staff members at the end of the

reporting period.

The last factor that should the company has to fulfill for considering the large company

and that is compliance. Compliance: As per ASIC, the large proprietary companies are

required to file a financial report and the report of the directors for every accounting year.

These accounts must also be audited until the grant is received from ASIC (Dias,

Rodrigues, Craig, and Neves, 2019).

Reporting entity

The reporting entity is an entity that is considered as the entity which is having different users

which are relying on the general purpose financial statements to gain an understanding of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.