Accounting Ethics and Professional Conduct: A Comprehensive Analysis

VerifiedAdded on 2020/04/07

|13

|2101

|510

Homework Assignment

AI Summary

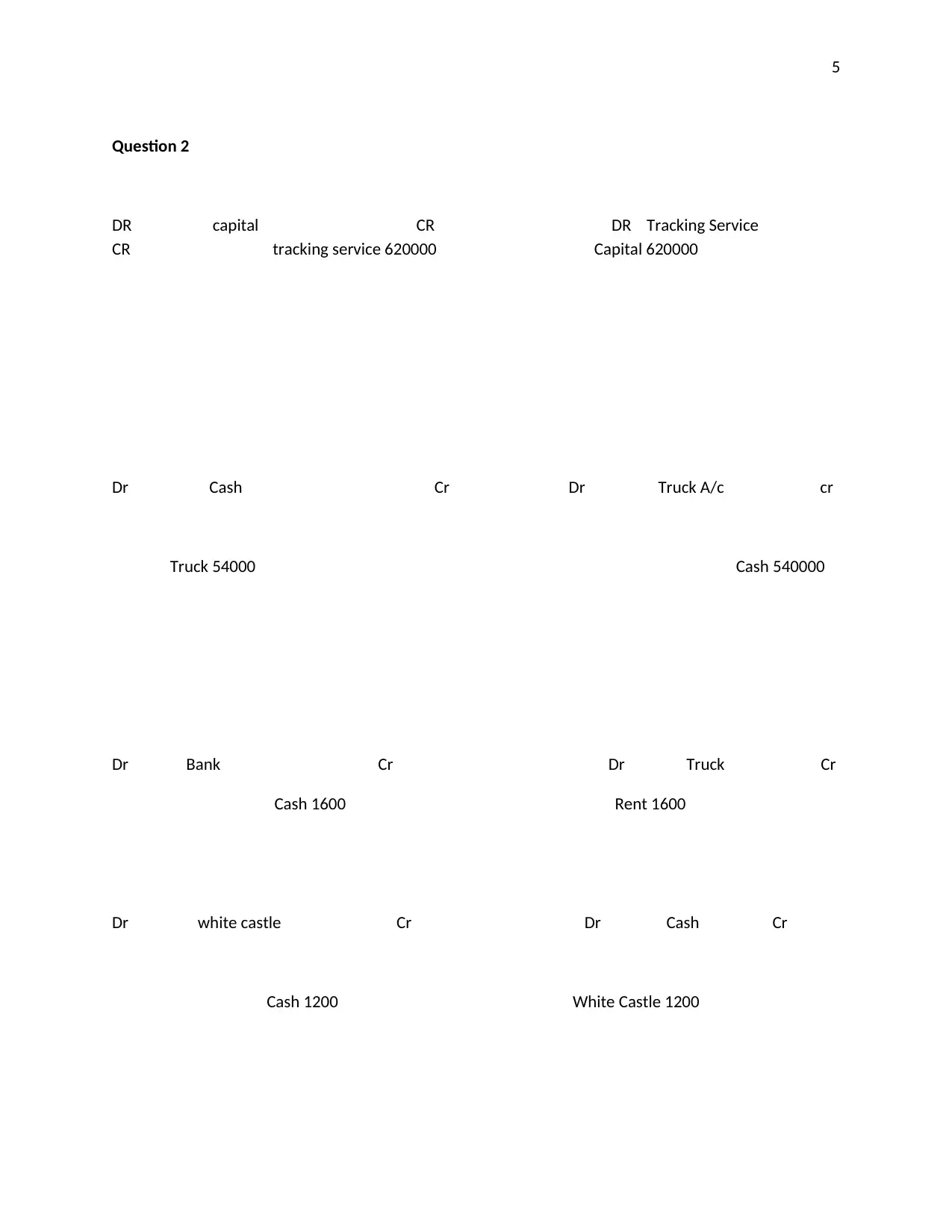

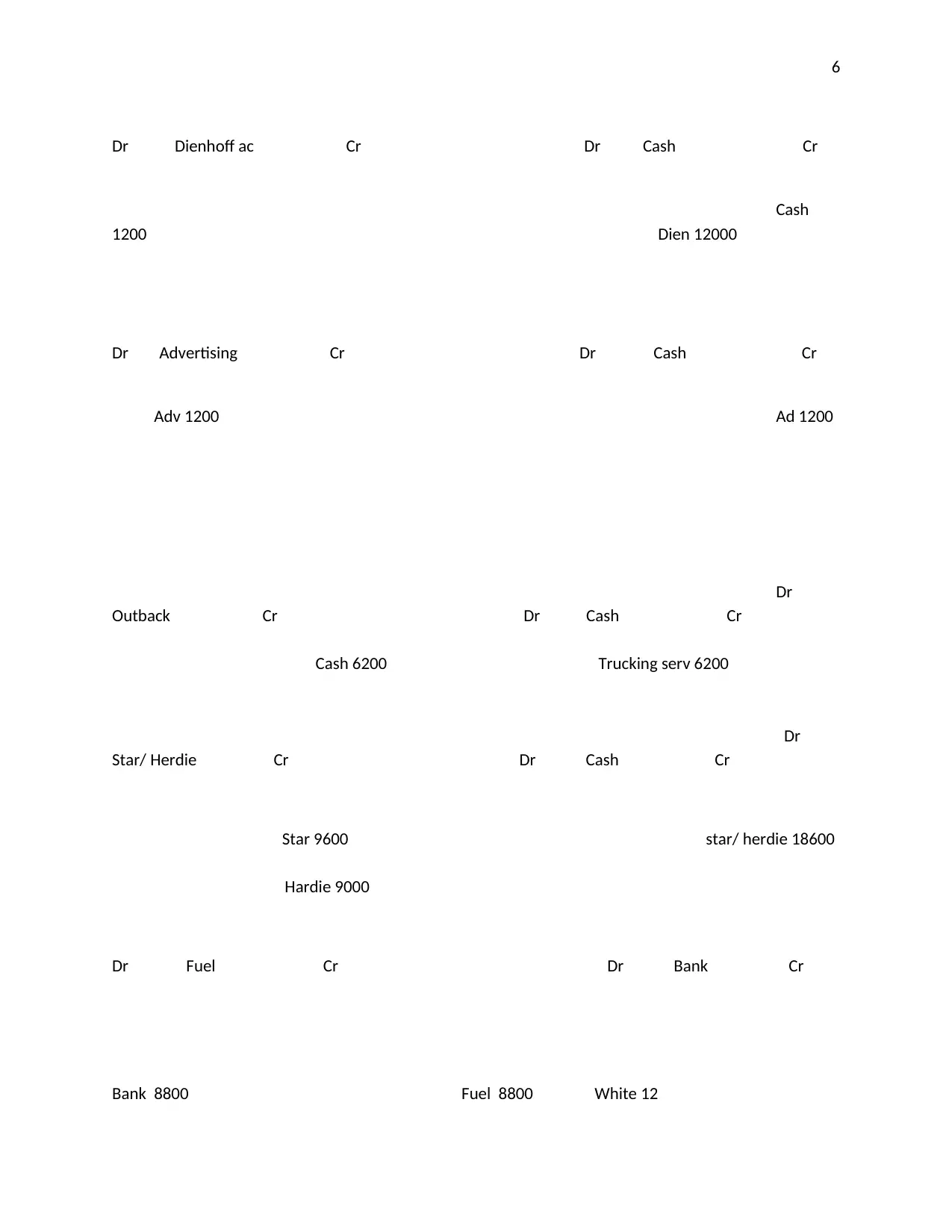

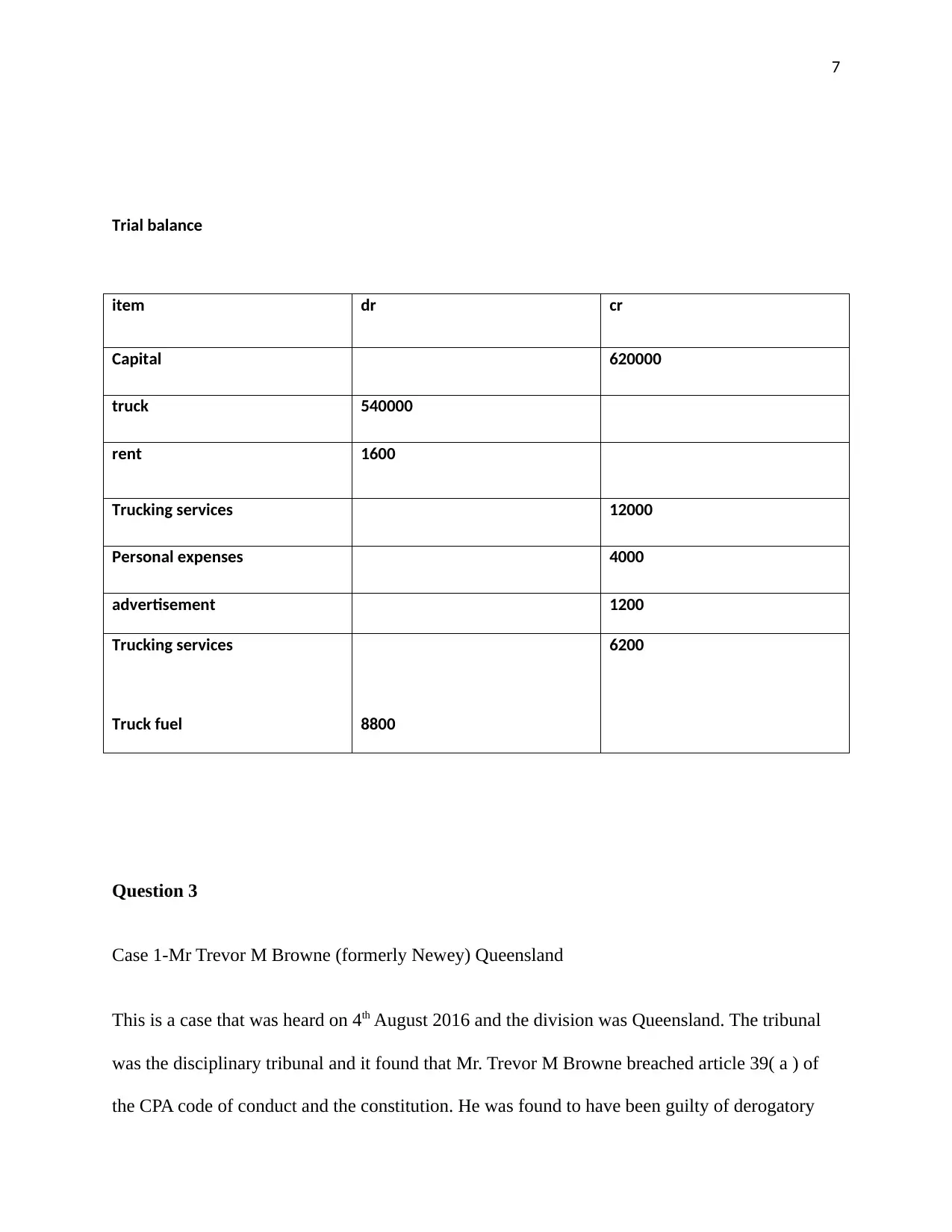

This accounting assignment delves into the ethical considerations within financial reporting, examining a scenario involving potential misrepresentation of financial statements. The assignment identifies key stakeholders, including employees, government, and auditors, and analyzes the motivations behind potential unethical actions, such as deferring profits to obtain grants and bonuses. It explores the ethical issues of fraudulent reporting and omission of financial records, emphasizing the importance of adhering to generally accepted accounting standards. The assignment also includes journal entries and a trial balance, followed by case studies of disciplinary actions taken against accountants who violated ethical codes, and the penalties imposed. The document references APES 110 standards, discussing responsibilities, confidentiality, and the general rules of ethics, and concludes with an assessment of the sufficiency of penalties and costs in the cases presented. The assignment provides a comprehensive overview of ethical challenges in the accounting profession and the consequences of unethical behavior.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.