Ethics and Financial Reporting Case Study: NZZ Limited Analysis

VerifiedAdded on 2023/06/08

|10

|627

|250

Case Study

AI Summary

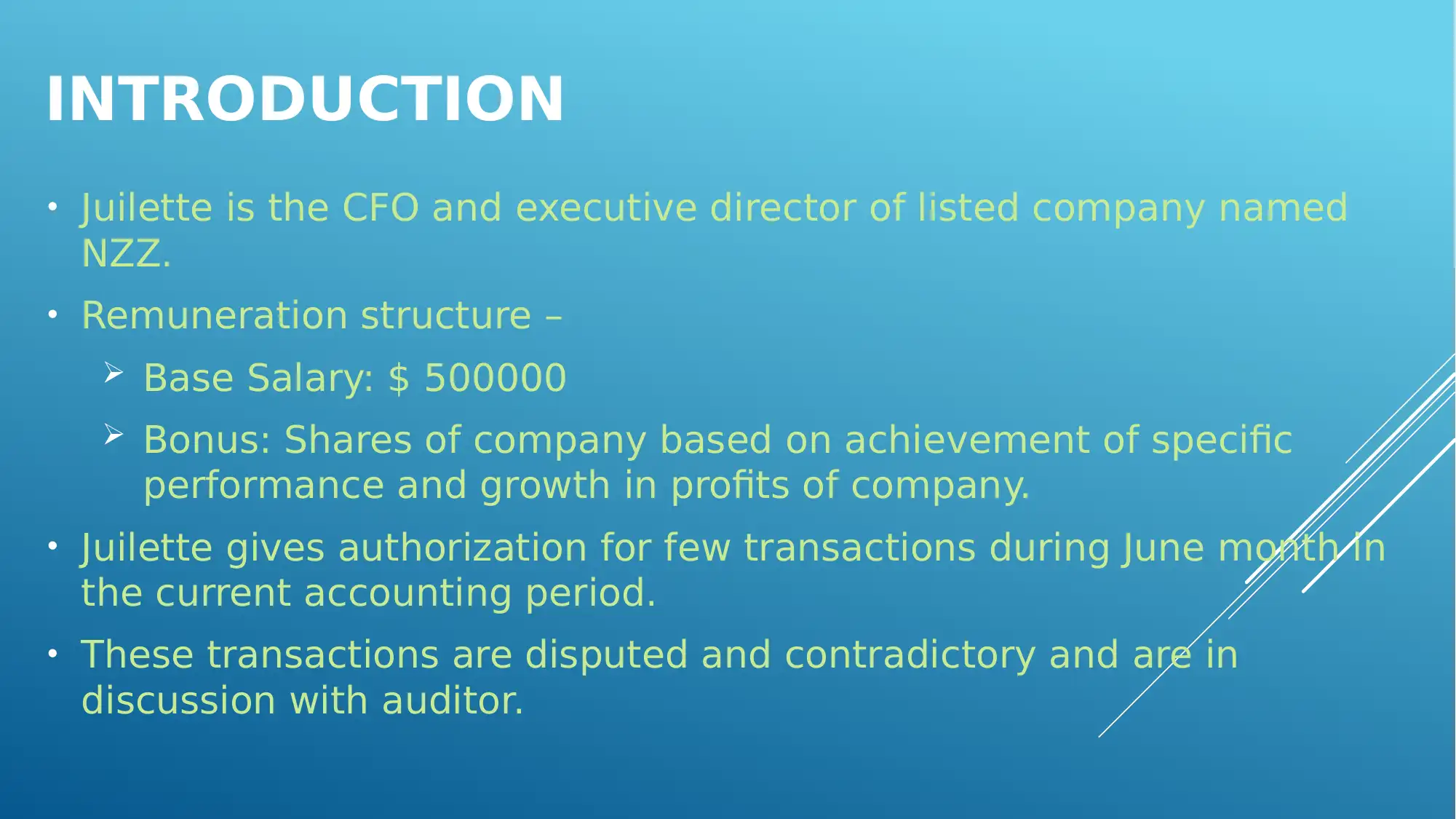

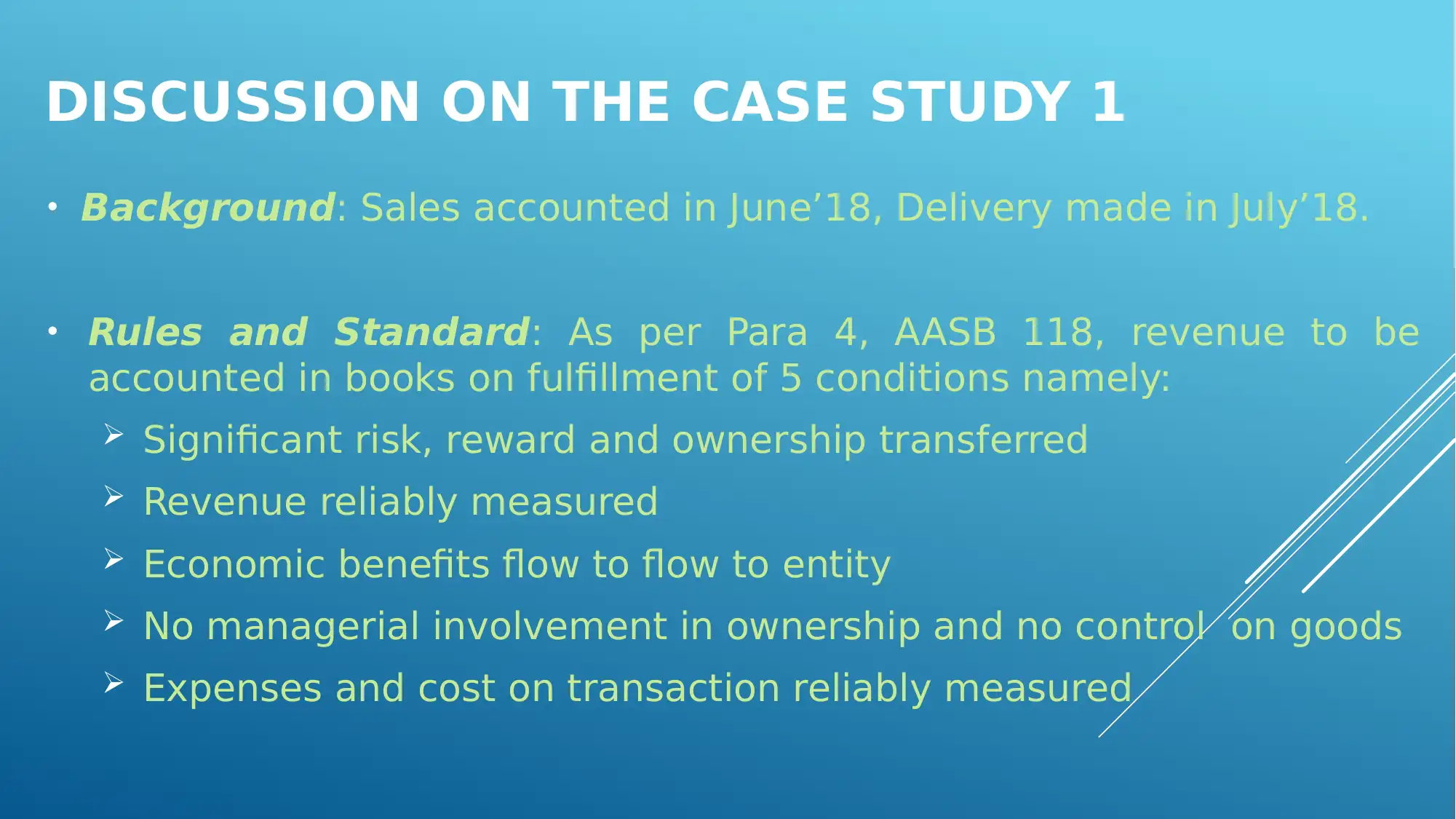

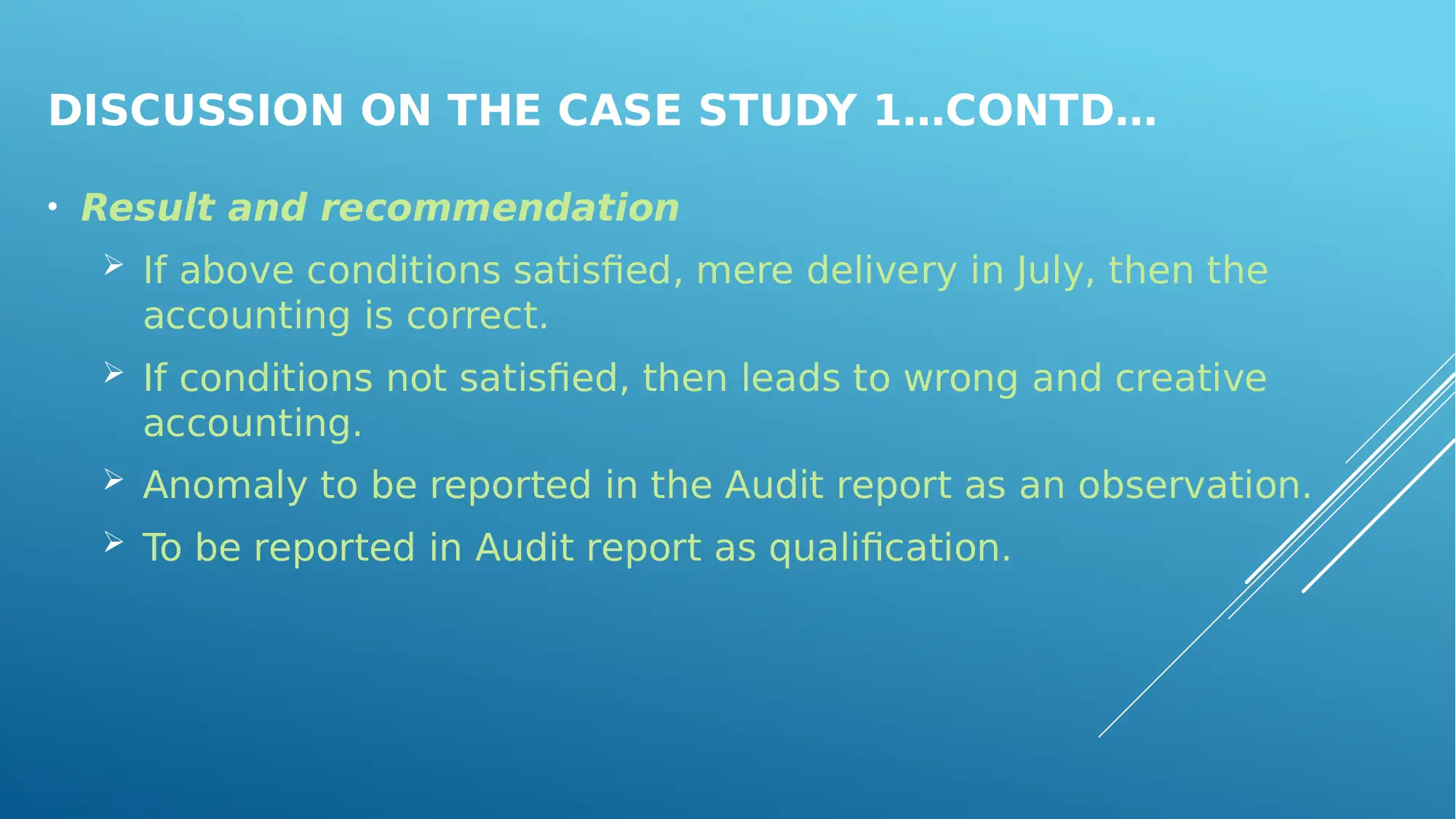

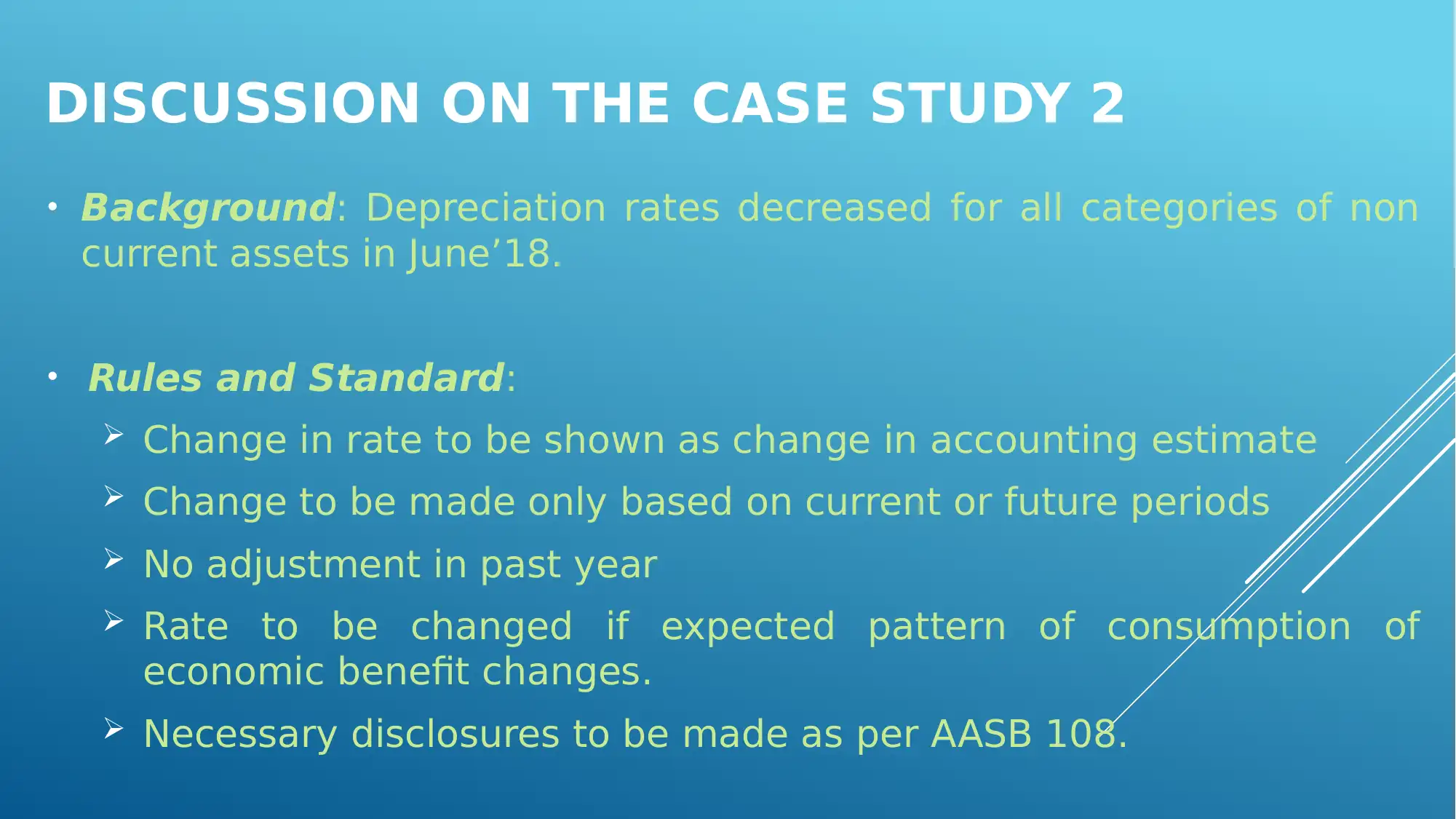

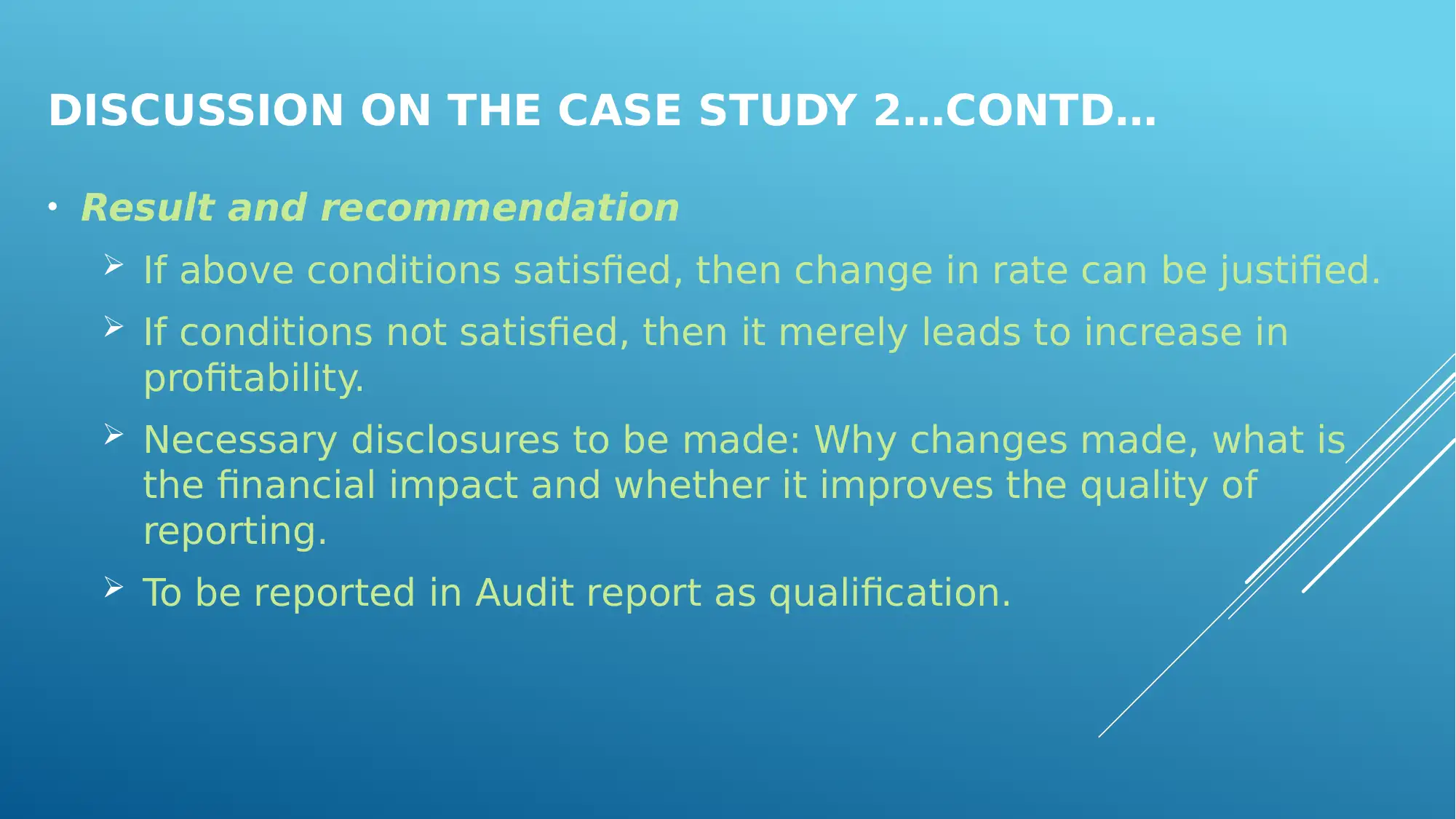

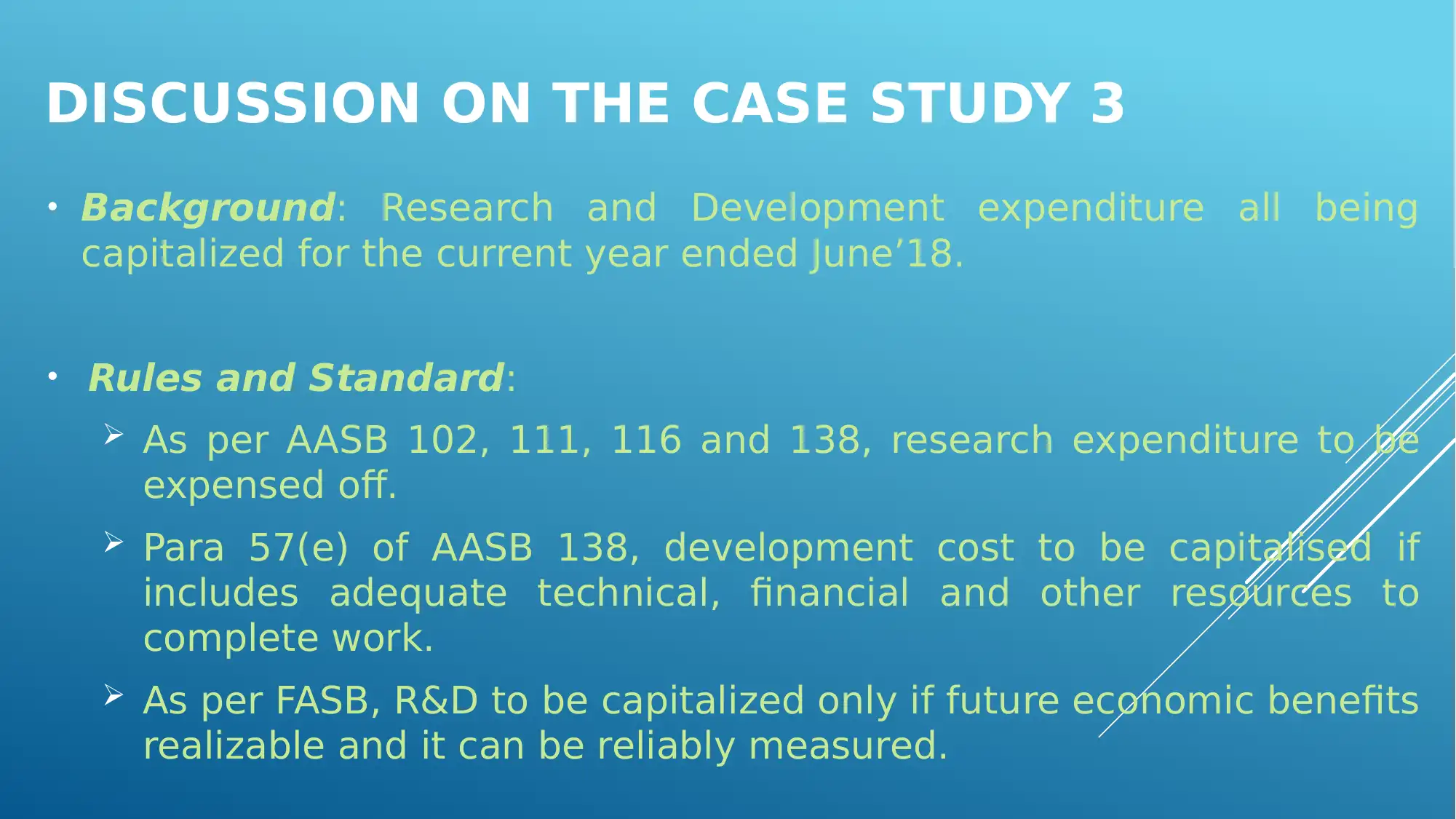

This case study examines ethical issues in accounting and financial reporting, focusing on the actions of Juliette, the CFO and executive director of NZZ Limited. The case presents three key issues: the premature recognition of sales revenue, the manipulation of depreciation rates, and the improper capitalization of research and development expenditures. The analysis evaluates these actions against relevant accounting standards, including AASB and FASB, and considers their implications for the audit report. The remuneration structure, which links bonuses to profit growth, is identified as a potential driver of creative accounting practices. The case concludes by highlighting the need for proper justification of transactions and the importance of transparent financial reporting, with recommendations for audit qualifications and improved ethical conduct.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.