Accounting Report: Ethics, Ledger Accounts, and Trial Balance Analysis

VerifiedAdded on 2020/07/22

|9

|2425

|71

Report

AI Summary

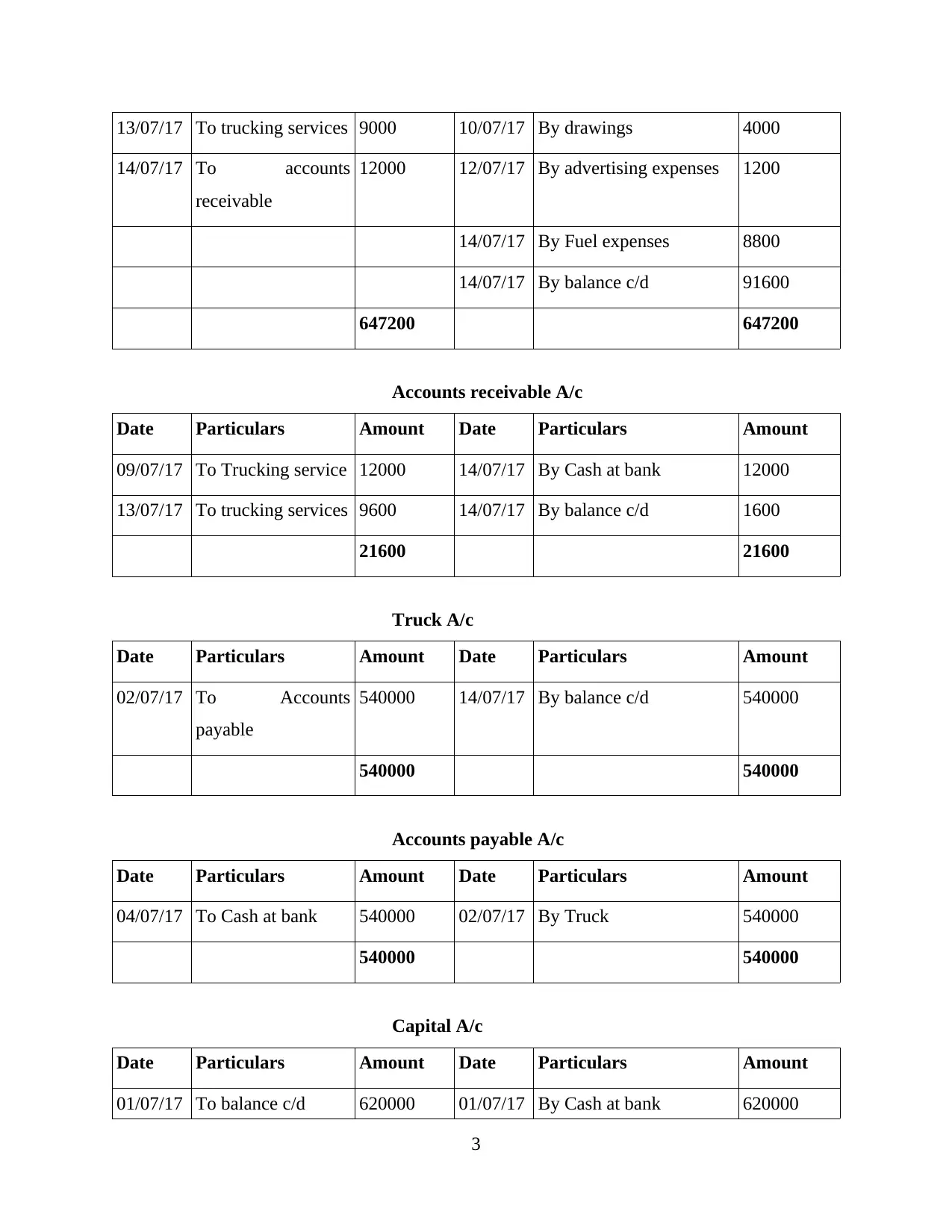

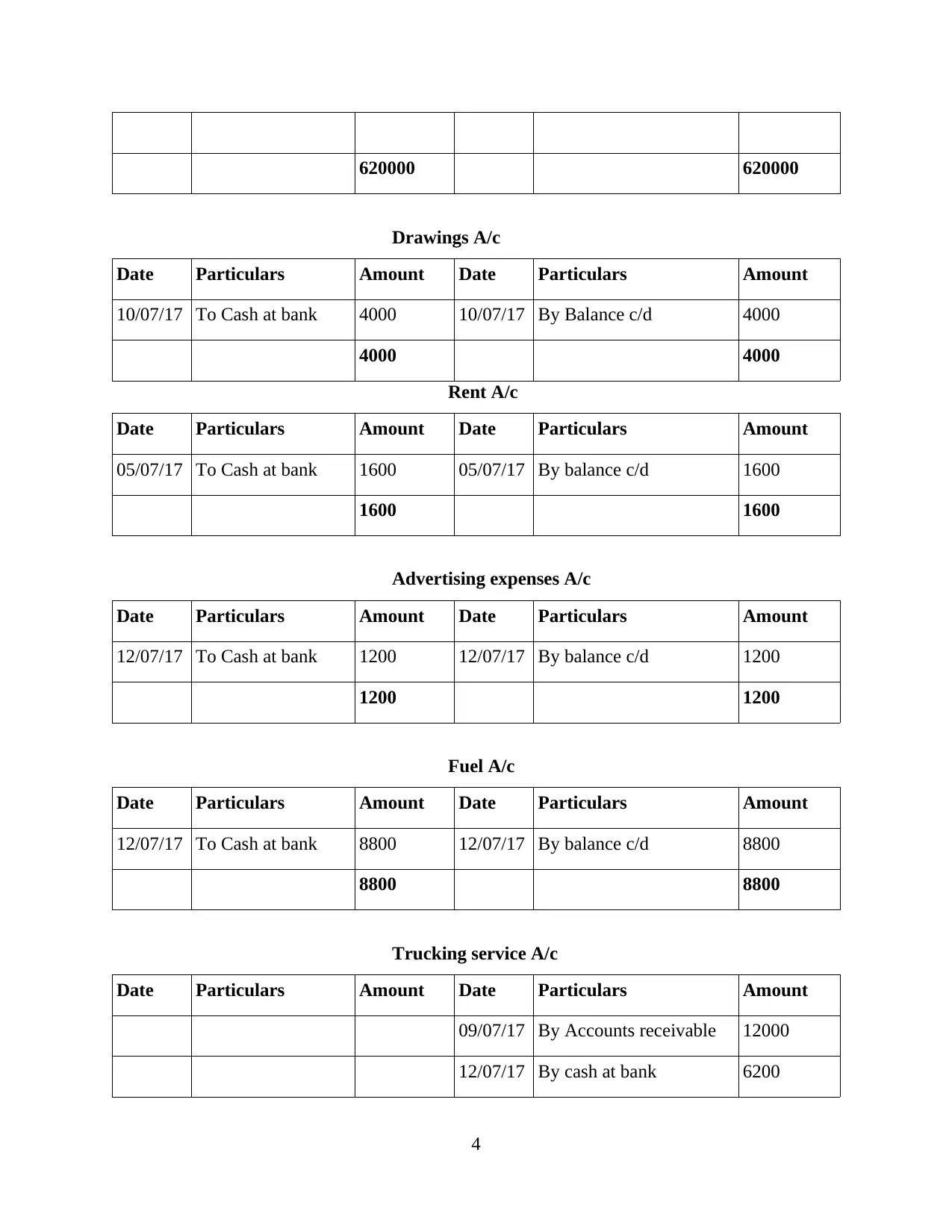

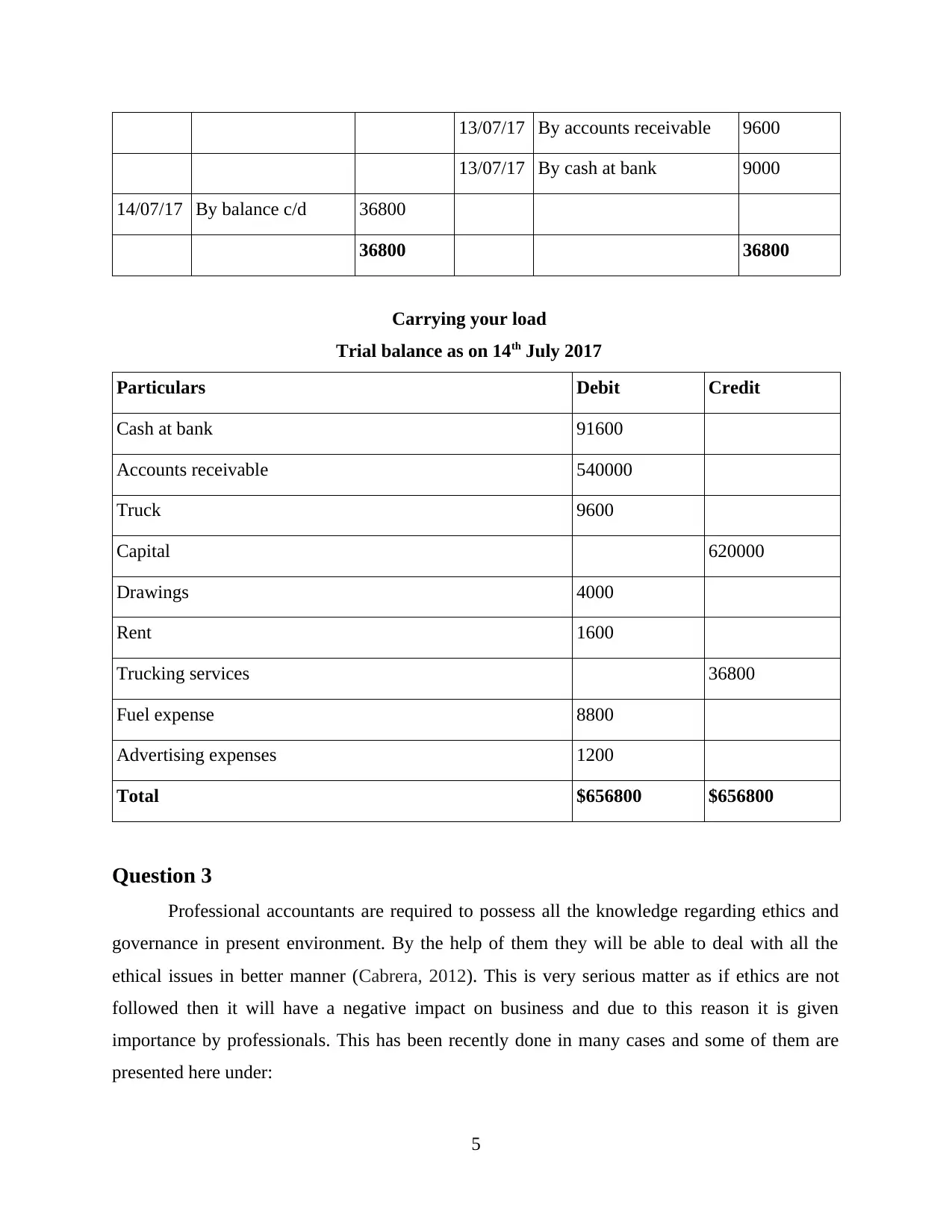

This accounting report addresses ethical considerations, ledger accounts, and trial balance analysis. It begins with an introduction outlining the report's structure, followed by an examination of stakeholder interests, Freda's request to manipulate financial statements, and the ethical issues involved, concluding with whether Lucia can remain ethical. The report then presents ledger accounts for various transactions, including cash at bank, accounts receivable, truck, accounts payable, capital, drawings, rent, advertising expenses, fuel, and trucking services. A trial balance is also provided. Finally, the report discusses professional accountants' ethical responsibilities and reviews cases where accounting laws were breached, detailing penalties imposed for non-compliance. The report concludes by emphasizing the importance of ethical standards in business operations and the correct preparation of financial records.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.