Accounting Ethics: An Overview of Principles, Issues, and Importance

VerifiedAdded on 2023/04/22

|14

|1258

|183

Presentation

AI Summary

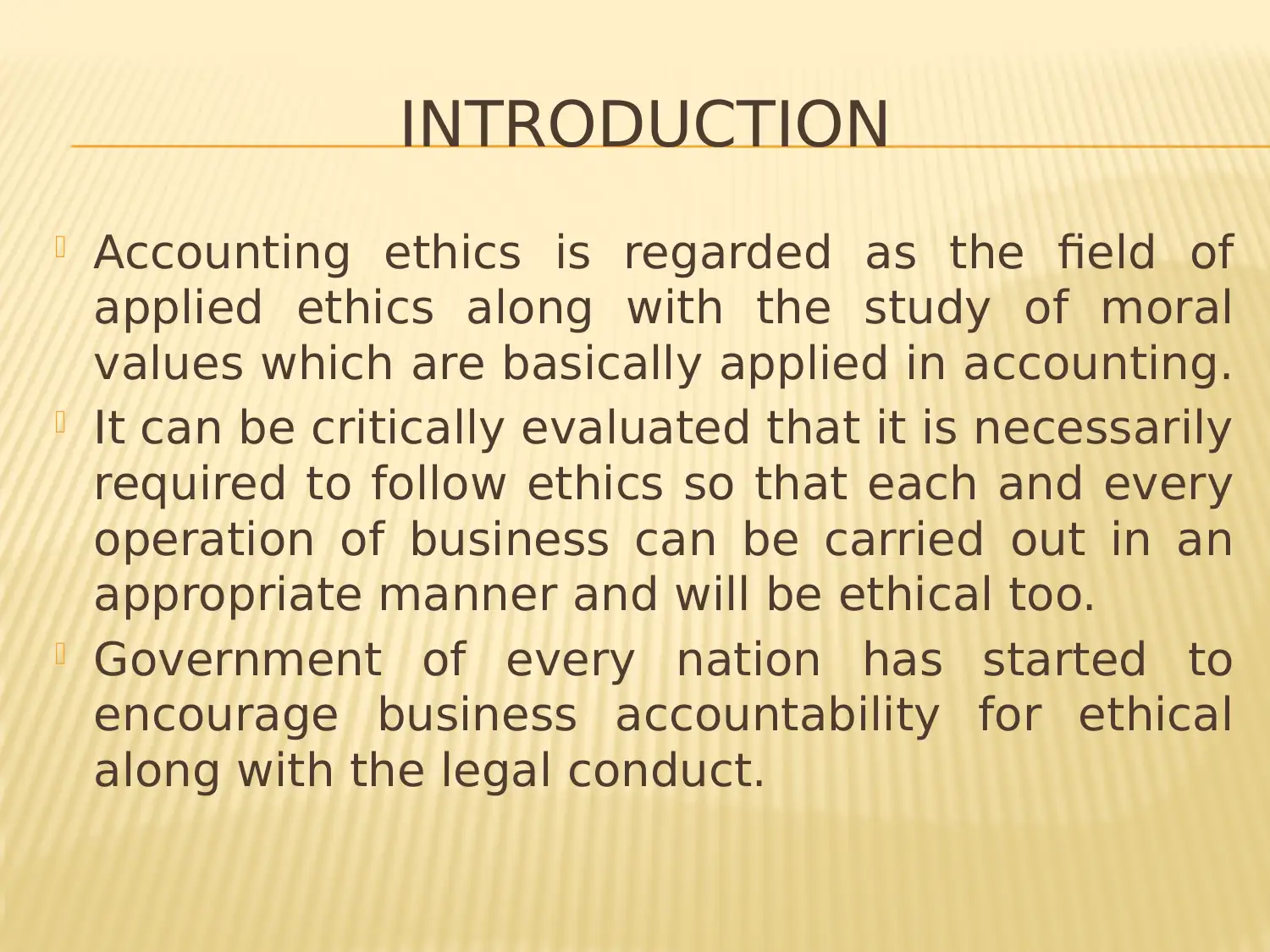

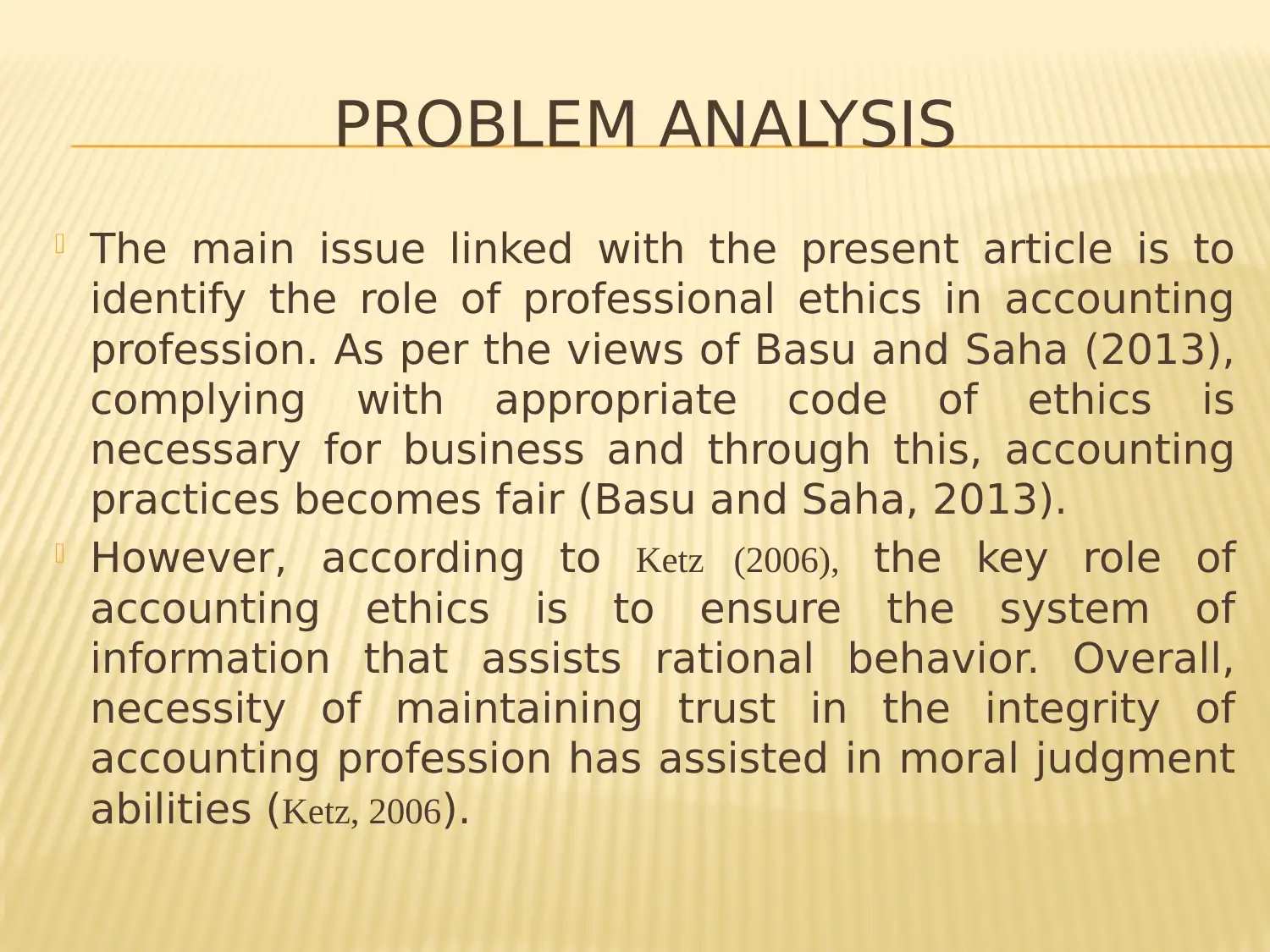

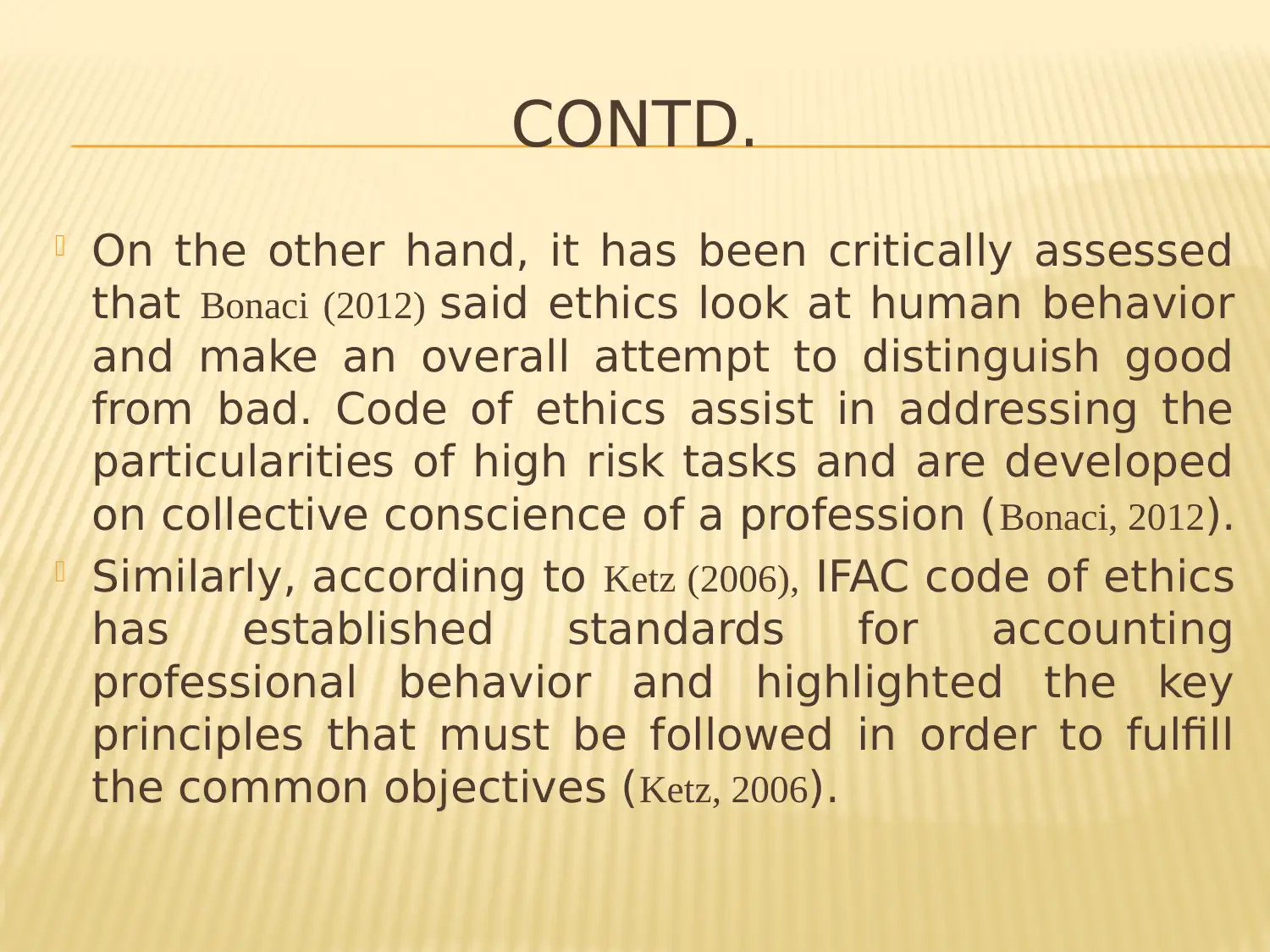

This presentation offers a comprehensive overview of accounting ethics, beginning with an introduction to the field and its importance in ensuring ethical conduct in business operations. It delves into the analysis of ethical problems, emphasizing the necessity of adhering to a code of ethics for fair accounting practices. The presentation outlines the five fundamental principles of accounting ethics: integrity, objectivity, professional competence and due care, confidentiality, and professional behavior. Furthermore, it explores various ethical issues such as fraudulent financial reporting, misappropriation of assets, disclosure problems, and penalties. The conclusion underscores the significance of ethical principles in accounting, highlighting their role in maintaining a company's fair and accurate financial position, and the positive impact of ethical guidelines on a company's image. The presentation is supported by references to relevant research papers and sources.

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.