Accounting Aspects of Emission Allowances in the EU ETS

VerifiedAdded on 2020/10/01

|16

|7290

|291

Report

AI Summary

This paper provides an in-depth analysis of the accounting perspectives of emission allowances within the European Union Emissions Trading Scheme (EU ETS), focusing on the application of International Financial Reporting Standards (IFRS). The study examines the recognition, capitalization, classification, measurement, and derecognition of emission allowances, as well as the treatment of fees and penalties. The paper highlights how various accounting treatments can significantly impact a company's profit or loss and equity, emphasizing the need for comprehensive accounting guidance to aid financial statement users in making informed economic decisions. The report delves into the EU ETS, discusses the recognition of emission allowances as intangible assets or non-current assets held for sale, and explores different measurement models, including cost and revaluation. It also addresses the issues of amortization, impairment, and fair value determination. Furthermore, the paper examines the derecognition of allowances through transfer or cancellation and offers alternative accounting interpretations. An illustrative example is also included to clarify the practical implications of the discussed accounting treatments, providing a valuable resource for understanding the financial reporting of emission allowances.

Accounting Aspects of Emissions Trading

Abstract

This paper is one of the first attempts to analyze the accounting perspectives of emission allowances

introduced by the European Union Emissions Trading Scheme, operating since January 1, 2005. Entities

subjected to the trading system face the growing challenge of calculating and reducing greenhouse gas

emissions; emission allowances are recognized into their books.

This study first introduces the European Union Emissions Trading Scheme. In the frame of the accounting

rules of International Financial Reporting Standards (IFRS), the authors look at the recognition,

capitalization and classification of emission allowances, their measurement, derecognition and also at fees

and penalties as administrative burden related to the trading system. The paper finds that the various

acceptable accounting treatments may affect the entity's profit or loss and equity quite differently.

Therefore a comprehensive accounting guidance is desirable for CO2 emission allowances that helps

readers of financial statements make better-informed economic decisions.

- 1 -

Abstract

This paper is one of the first attempts to analyze the accounting perspectives of emission allowances

introduced by the European Union Emissions Trading Scheme, operating since January 1, 2005. Entities

subjected to the trading system face the growing challenge of calculating and reducing greenhouse gas

emissions; emission allowances are recognized into their books.

This study first introduces the European Union Emissions Trading Scheme. In the frame of the accounting

rules of International Financial Reporting Standards (IFRS), the authors look at the recognition,

capitalization and classification of emission allowances, their measurement, derecognition and also at fees

and penalties as administrative burden related to the trading system. The paper finds that the various

acceptable accounting treatments may affect the entity's profit or loss and equity quite differently.

Therefore a comprehensive accounting guidance is desirable for CO2 emission allowances that helps

readers of financial statements make better-informed economic decisions.

- 1 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction..................................................................................................................................3

1. The European Union Emissions Trading Scheme...........................................................4

2. Interpretation of accounting on emission allowances....................................................5

3. Recognition into the balance sheet......................................................................................6

4. Capitalization...........................................................................................................................7

5. Measurement............................................................................................................................8

5.1. Emission allowances recognized as intangible assets...........................................................8

5.1.1. Cost model or revaluation model......................................................................................................8

5.1.2. Amortisation.........................................................................................................................................8

5.1.3. Impairment............................................................................................................................................8

5.2. Emission allowances recognized as non-current assets held for sale .................................9

5.3. Fair value of emission allowances..........................................................................................10

6. Provision..................................................................................................................................10

7. Derecognition.........................................................................................................................10

7.1. Transfer.......................................................................................................................................10

7.2. Cancellation................................................................................................................................11

8. Alternative accounting interpretation on emission allowances.................................11

9. Fees and penalties.................................................................................................................12

10. An illustrative example......................................................................................................12

Summary......................................................................................................................................14

List of references.......................................................................................................................15

List of tables

Table 1. Alternative accounting treatments for emission allowances.........................................................11

List of figures

Figure 1. A simplified model for the operation of allowance trading..........................................................4

- 2 -

Introduction..................................................................................................................................3

1. The European Union Emissions Trading Scheme...........................................................4

2. Interpretation of accounting on emission allowances....................................................5

3. Recognition into the balance sheet......................................................................................6

4. Capitalization...........................................................................................................................7

5. Measurement............................................................................................................................8

5.1. Emission allowances recognized as intangible assets...........................................................8

5.1.1. Cost model or revaluation model......................................................................................................8

5.1.2. Amortisation.........................................................................................................................................8

5.1.3. Impairment............................................................................................................................................8

5.2. Emission allowances recognized as non-current assets held for sale .................................9

5.3. Fair value of emission allowances..........................................................................................10

6. Provision..................................................................................................................................10

7. Derecognition.........................................................................................................................10

7.1. Transfer.......................................................................................................................................10

7.2. Cancellation................................................................................................................................11

8. Alternative accounting interpretation on emission allowances.................................11

9. Fees and penalties.................................................................................................................12

10. An illustrative example......................................................................................................12

Summary......................................................................................................................................14

List of references.......................................................................................................................15

List of tables

Table 1. Alternative accounting treatments for emission allowances.........................................................11

List of figures

Figure 1. A simplified model for the operation of allowance trading..........................................................4

- 2 -

Introduction

This paper calls attention to the area of environmental protection where it is not the environmental experts

and green NGOs that make efforts to achieve results most of all. The emissions trading system relating to

greenhouse gases offers the promise of additional revenue to businesses, this article addresses managers

and operators covered by the regulation of the EU ETS. This paper focuses on the accounting aspects of

emission allowances and their book keeping rather than discussing related theories. This study presents

evidence that it is worth analysing emission allowances as assets from an accounting perspective as they

are recognized in the financial statements of companies.

The CO2 allowance system entered into force in the European Union on January 1, 2005. The revision of

National Allocation Plans establishing the conditions of the operation was completed by the middle of

2006. The system has finished its first, trial phase with the end of 2007. Events of the last three years were

the establishment of the conditions and details of introduction, operation and sustainable operation, market

creation, and the foundation of its technical and technological basis. It can be stated that this area requires

a shift in attitudes and is sensitive to economic factors.

The system is quite revolutionary and not just because of the exact level of emission reduction achieved.

Similar incentive systems have already been present both in Europe and around the world (e.g., eco-taxes,

environmental burden fees, environmental pollution fines). However, no such system has been present to

encourage participants within a public stock exchange framework, allowing for an almost full enforcement

of market mechanisms, at the same time, attracting capital investors to this area.

As a result of the Directive on CO2 emissions trading of the European Union the emissions of CO2 have

become a new factor in the production costs of companies covered. CO2 emission allowances are intended

to become scarcities, similar to capital, labour force, land or other natural resources. Scarcity creates

value, that is, allowances for carbon emissions become material rights of business value, its ownership

bear benefits.

- 3 -

This paper calls attention to the area of environmental protection where it is not the environmental experts

and green NGOs that make efforts to achieve results most of all. The emissions trading system relating to

greenhouse gases offers the promise of additional revenue to businesses, this article addresses managers

and operators covered by the regulation of the EU ETS. This paper focuses on the accounting aspects of

emission allowances and their book keeping rather than discussing related theories. This study presents

evidence that it is worth analysing emission allowances as assets from an accounting perspective as they

are recognized in the financial statements of companies.

The CO2 allowance system entered into force in the European Union on January 1, 2005. The revision of

National Allocation Plans establishing the conditions of the operation was completed by the middle of

2006. The system has finished its first, trial phase with the end of 2007. Events of the last three years were

the establishment of the conditions and details of introduction, operation and sustainable operation, market

creation, and the foundation of its technical and technological basis. It can be stated that this area requires

a shift in attitudes and is sensitive to economic factors.

The system is quite revolutionary and not just because of the exact level of emission reduction achieved.

Similar incentive systems have already been present both in Europe and around the world (e.g., eco-taxes,

environmental burden fees, environmental pollution fines). However, no such system has been present to

encourage participants within a public stock exchange framework, allowing for an almost full enforcement

of market mechanisms, at the same time, attracting capital investors to this area.

As a result of the Directive on CO2 emissions trading of the European Union the emissions of CO2 have

become a new factor in the production costs of companies covered. CO2 emission allowances are intended

to become scarcities, similar to capital, labour force, land or other natural resources. Scarcity creates

value, that is, allowances for carbon emissions become material rights of business value, its ownership

bear benefits.

- 3 -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

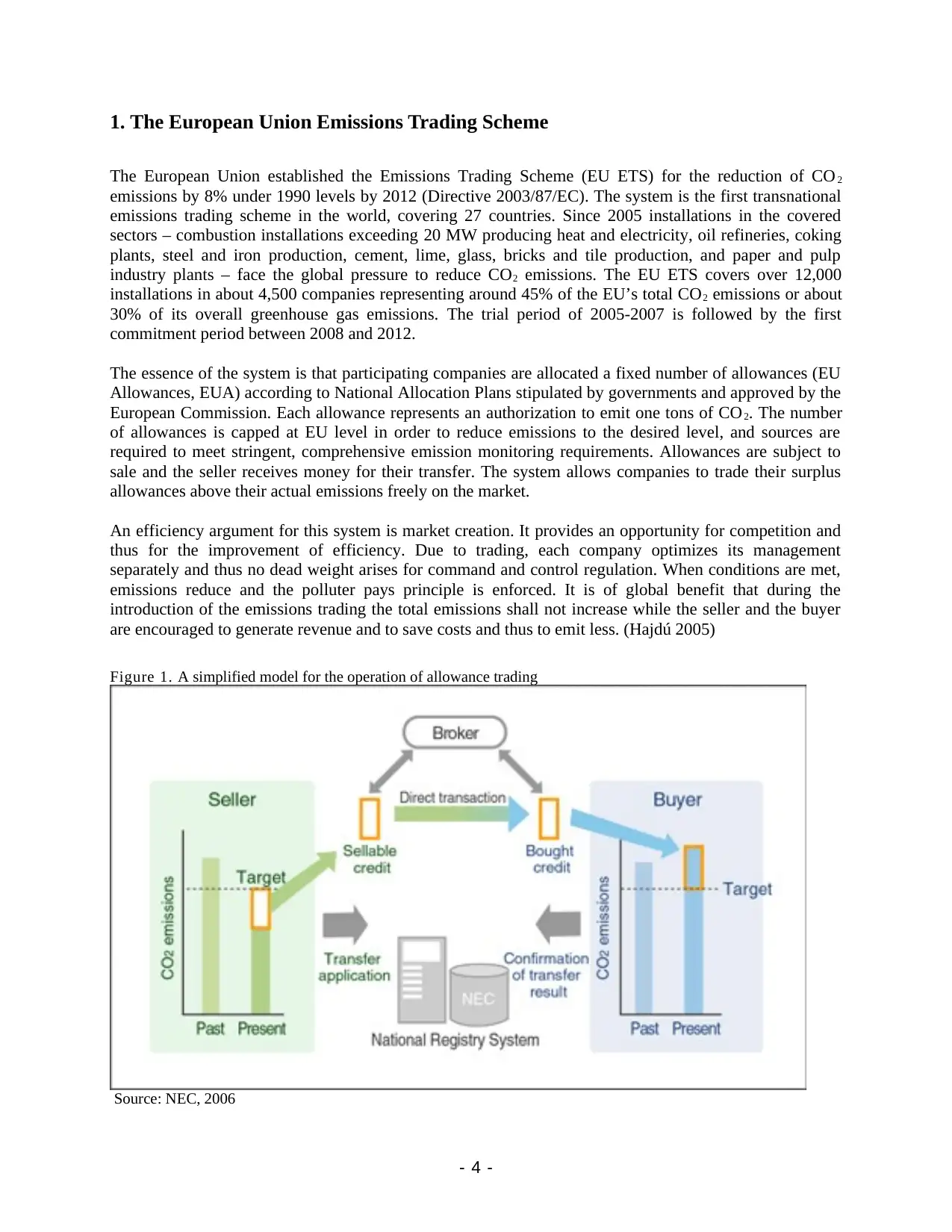

1. The European Union Emissions Trading Scheme

The European Union established the Emissions Trading Scheme (EU ETS) for the reduction of CO 2

emissions by 8% under 1990 levels by 2012 (Directive 2003/87/EC). The system is the first transnational

emissions trading scheme in the world, covering 27 countries. Since 2005 installations in the covered

sectors – combustion installations exceeding 20 MW producing heat and electricity, oil refineries, coking

plants, steel and iron production, cement, lime, glass, bricks and tile production, and paper and pulp

industry plants – face the global pressure to reduce CO2 emissions. The EU ETS covers over 12,000

installations in about 4,500 companies representing around 45% of the EU’s total CO2 emissions or about

30% of its overall greenhouse gas emissions. The trial period of 2005-2007 is followed by the first

commitment period between 2008 and 2012.

The essence of the system is that participating companies are allocated a fixed number of allowances (EU

Allowances, EUA) according to National Allocation Plans stipulated by governments and approved by the

European Commission. Each allowance represents an authorization to emit one tons of CO2. The number

of allowances is capped at EU level in order to reduce emissions to the desired level, and sources are

required to meet stringent, comprehensive emission monitoring requirements. Allowances are subject to

sale and the seller receives money for their transfer. The system allows companies to trade their surplus

allowances above their actual emissions freely on the market.

An efficiency argument for this system is market creation. It provides an opportunity for competition and

thus for the improvement of efficiency. Due to trading, each company optimizes its management

separately and thus no dead weight arises for command and control regulation. When conditions are met,

emissions reduce and the polluter pays principle is enforced. It is of global benefit that during the

introduction of the emissions trading the total emissions shall not increase while the seller and the buyer

are encouraged to generate revenue and to save costs and thus to emit less. (Hajdú 2005)

Figure 1. A simplified model for the operation of allowance trading

Source: NEC, 2006

- 4 -

The European Union established the Emissions Trading Scheme (EU ETS) for the reduction of CO 2

emissions by 8% under 1990 levels by 2012 (Directive 2003/87/EC). The system is the first transnational

emissions trading scheme in the world, covering 27 countries. Since 2005 installations in the covered

sectors – combustion installations exceeding 20 MW producing heat and electricity, oil refineries, coking

plants, steel and iron production, cement, lime, glass, bricks and tile production, and paper and pulp

industry plants – face the global pressure to reduce CO2 emissions. The EU ETS covers over 12,000

installations in about 4,500 companies representing around 45% of the EU’s total CO2 emissions or about

30% of its overall greenhouse gas emissions. The trial period of 2005-2007 is followed by the first

commitment period between 2008 and 2012.

The essence of the system is that participating companies are allocated a fixed number of allowances (EU

Allowances, EUA) according to National Allocation Plans stipulated by governments and approved by the

European Commission. Each allowance represents an authorization to emit one tons of CO2. The number

of allowances is capped at EU level in order to reduce emissions to the desired level, and sources are

required to meet stringent, comprehensive emission monitoring requirements. Allowances are subject to

sale and the seller receives money for their transfer. The system allows companies to trade their surplus

allowances above their actual emissions freely on the market.

An efficiency argument for this system is market creation. It provides an opportunity for competition and

thus for the improvement of efficiency. Due to trading, each company optimizes its management

separately and thus no dead weight arises for command and control regulation. When conditions are met,

emissions reduce and the polluter pays principle is enforced. It is of global benefit that during the

introduction of the emissions trading the total emissions shall not increase while the seller and the buyer

are encouraged to generate revenue and to save costs and thus to emit less. (Hajdú 2005)

Figure 1. A simplified model for the operation of allowance trading

Source: NEC, 2006

- 4 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Interpretation of accounting on emission allowances

Market-based programs, like CO2 allowance trading systems, “raise a plethora of new accounting, tax and

liability issues with little in the way of precedent." (Hopp 1994:487) “The issues for accountants are how

to account for the emission rights received, any surplus or shortfall of rights at the balance sheet date and

how to measure the expense associated with CO2 emissions.” (Riley 2007:48)

From 2005 many companies in the EU are required to report their financial performance according to

International Financial Reporting Standards (IFRS). This paper focuses on the accounting principals of

IFRS. However it should be noted that in the US, the Emerging Issues Task Force (EITF) also attempted

to summarise the related accounting issues in Participants’ Accounting for Emissions Allowances under a

“Cap and Trade” Program. This regulation is beyond the scope of this paper.

The International Accounting Standards Board’s (IASB) International Financial Reporting Interpretations

Committee (IFRIC) has decided to standardise the accounting for emission rights and has issued its

interpretation how to account for emission allowances. IFRIC 3 Emission Rights was published by IFRIC

on 2 December 2004. The objective was to provide guidance on accounting for a cap and trade emission

right scheme that is operational. It would have become effective for annual periods beginning on or after 1

March 2005.

Several organisations submitted comments on IFRIC 3 Emission Rights. For example the concerns of the

European Financial Reporting Advisory Group (EFRAG) were the followings: “applying IFRIC 3 will not

always result in economic reality being reflected and relevant information being provided. That is because

the accounting required by IFRIC is constrained by the existing standards. ... This creates a measurement

mismatch [whereby some items are measured at cost (IAS 38 and IAS 20) and others at fair value (IAS

37)] and a reporting mismatch [whereby some gains and losses are reported in profit or loss (IAS 37 and

IAS 20) and others in equity (IAS 38)]. These accounting mismatches are all the more critical because of

the fact that there is an economic interdependency between the assets and liability involved in the

scheme.” (EFRAG 2005) That was why EFRAG recommended that IFRIC 3 should not be endorsed for

use in the EU. According to the opinion of EFRAG “the disadvantages that would arise from endorsing

the interpretation outweigh the advantages of guidance on the accounting on the emission right schemes.”

(EFRAG 2005)

After a long and vigorous debate, during which several alternative treatments were proposed, the IASB

withdrew IFRIC 3 at its meeting in June 2005. The reasons were the unsatisfactory measurement of the

interpretation, the reporting mismatches and reduced urgency for an accounting guidance on emission

allowances. IFRIC is now reconsidering IFRIC 3 Emission Rights to improve the accounting quality of the

financial information resulting from the interpretation and it is studying whether and how IFRIC 3 might

be appropriate to amend existing standards to reduce or eliminate some of the mismatches.

“But the issues associated with emission rights accounting, as with CO2 emissions, have not disappeared

as easily as IFRIC 3. So, in this post-IFRIC 3 vacuum, how should entities that participate in an emissions

trading scheme account for the rights?” (Riley 2007:48) So thus a guidance should be revealed how to

apply existing International Accounting Standards to cap and trade emission rights schemes. An emission

allowance reported in financial statements and accounts is considered as a special case of the following

accounting standards:

IAS 20 – Accounting for Government Grants and Disclosure of Government Assistance

IAS 36 – Impairment of Assets

IAS 37 – Provisions, Contingent Liabilities and Contingent Assets

IAS 38 – Intangible Assets

IFRS 5 – Non-current Assets Held for Sale and Discontinued Operations.

This paper provides an accounting guidance according to the above mentioned accounting standards.

- 5 -

Market-based programs, like CO2 allowance trading systems, “raise a plethora of new accounting, tax and

liability issues with little in the way of precedent." (Hopp 1994:487) “The issues for accountants are how

to account for the emission rights received, any surplus or shortfall of rights at the balance sheet date and

how to measure the expense associated with CO2 emissions.” (Riley 2007:48)

From 2005 many companies in the EU are required to report their financial performance according to

International Financial Reporting Standards (IFRS). This paper focuses on the accounting principals of

IFRS. However it should be noted that in the US, the Emerging Issues Task Force (EITF) also attempted

to summarise the related accounting issues in Participants’ Accounting for Emissions Allowances under a

“Cap and Trade” Program. This regulation is beyond the scope of this paper.

The International Accounting Standards Board’s (IASB) International Financial Reporting Interpretations

Committee (IFRIC) has decided to standardise the accounting for emission rights and has issued its

interpretation how to account for emission allowances. IFRIC 3 Emission Rights was published by IFRIC

on 2 December 2004. The objective was to provide guidance on accounting for a cap and trade emission

right scheme that is operational. It would have become effective for annual periods beginning on or after 1

March 2005.

Several organisations submitted comments on IFRIC 3 Emission Rights. For example the concerns of the

European Financial Reporting Advisory Group (EFRAG) were the followings: “applying IFRIC 3 will not

always result in economic reality being reflected and relevant information being provided. That is because

the accounting required by IFRIC is constrained by the existing standards. ... This creates a measurement

mismatch [whereby some items are measured at cost (IAS 38 and IAS 20) and others at fair value (IAS

37)] and a reporting mismatch [whereby some gains and losses are reported in profit or loss (IAS 37 and

IAS 20) and others in equity (IAS 38)]. These accounting mismatches are all the more critical because of

the fact that there is an economic interdependency between the assets and liability involved in the

scheme.” (EFRAG 2005) That was why EFRAG recommended that IFRIC 3 should not be endorsed for

use in the EU. According to the opinion of EFRAG “the disadvantages that would arise from endorsing

the interpretation outweigh the advantages of guidance on the accounting on the emission right schemes.”

(EFRAG 2005)

After a long and vigorous debate, during which several alternative treatments were proposed, the IASB

withdrew IFRIC 3 at its meeting in June 2005. The reasons were the unsatisfactory measurement of the

interpretation, the reporting mismatches and reduced urgency for an accounting guidance on emission

allowances. IFRIC is now reconsidering IFRIC 3 Emission Rights to improve the accounting quality of the

financial information resulting from the interpretation and it is studying whether and how IFRIC 3 might

be appropriate to amend existing standards to reduce or eliminate some of the mismatches.

“But the issues associated with emission rights accounting, as with CO2 emissions, have not disappeared

as easily as IFRIC 3. So, in this post-IFRIC 3 vacuum, how should entities that participate in an emissions

trading scheme account for the rights?” (Riley 2007:48) So thus a guidance should be revealed how to

apply existing International Accounting Standards to cap and trade emission rights schemes. An emission

allowance reported in financial statements and accounts is considered as a special case of the following

accounting standards:

IAS 20 – Accounting for Government Grants and Disclosure of Government Assistance

IAS 36 – Impairment of Assets

IAS 37 – Provisions, Contingent Liabilities and Contingent Assets

IAS 38 – Intangible Assets

IFRS 5 – Non-current Assets Held for Sale and Discontinued Operations.

This paper provides an accounting guidance according to the above mentioned accounting standards.

- 5 -

3. Recognition into the balance sheet

An emission allowance scheme gives rise to:

(a) an asset for allowances held;

(b) a government grant;

(c) a liability for the obligation to deliver allowances equal to emissions that have been made.

On one hand an emission allowance meets the definition of an asset in the Framework for the Preparation

and Presentation of Financial Statements. Assets are resources controlled by the entity as a result of past

events and from which future economic benefits are expected to flow to the entity. An entity controls an

asset in case it is capable of gaining the earnings deriving of the asset or restricting others in it. Future

economic benefits may arise from cost savings realized by the asset or direct increase in incomes or from

any economic events related to the use of the asset. On the other hand once emissions have occurred, the

entity has the liability to deliver allowances equal to emissions that have been made.

“A comparison of the characteristics of ecological resources and of traditional intangible resources shows

points of similarity that may cause an equivalent treatment in the annual accounts.” (Edeltraud 2006:235)

Accordingly emission allowances are to be considered as intangible assets. The recognition of an item as

an intangible asset requires an entity to demonstrate that the item meets:

(a) the definition of an intangible asset; and

(b) the recognition criteria.

An emission allowance meets the definition of an intangible asset, namely it is an identifiable non-

monetary asset without physical substance. An asset meets the identifiability criterion in the definition of

an intangible asset when it:

(a) is separable, i.e. is capable of being separated or divided from the entity and sold, transferred,

licensed, rented or exchanged, either individually or together with a related contract, asset or

liability; or

(b) arises from contractual or other legal rights, regardless of whether those rights are transferable

or separable from the entity or from other rights and obligations.

An intangible asset shall be recognized if, and only if:

(a) it is probable that the expected future economic benefits that are attributable to the asset will

flow to the entity; and

(b) the cost of the asset can be measured reliably.

Emission allowances are basic rights, which permanently serve the operation of the entity. The emission

permit and the pollution rights obtained are fundamental requirements for the continued operation of the

entity. Operation of enterprises under Directive 2003/87/EC requires a greenhouse gas emission permit:

“Member States shall ensure that, from 1 January 2005, no installation undertakes any activity listed in

Annex I resulting in emissions specified in relation to that activity unless its operator holds a permit issued

by a competent authority in accordance with Articles 5 and 6” (Article 4). Emission allowances to be

allocated in the given calendar year shall be allocated by February 28 of each trading year. Entities are

obliged to deliver allowances corresponding to their emissions by April 30 of the following year at the

latest. These are then deleted from the Transaction Log.

Entities are free to buy and sell allowances. Thus an entity has three options:

1. it can emit equal to its initial allocation;

2. it can emit less than its initial allocation, and sell or bank excess allowances;

3. it can emit more than its initial allocation, in which case it must buy additional allowances for

the excess emissions or borrow from next year’s allocation or pay a penalty.

- 6 -

An emission allowance scheme gives rise to:

(a) an asset for allowances held;

(b) a government grant;

(c) a liability for the obligation to deliver allowances equal to emissions that have been made.

On one hand an emission allowance meets the definition of an asset in the Framework for the Preparation

and Presentation of Financial Statements. Assets are resources controlled by the entity as a result of past

events and from which future economic benefits are expected to flow to the entity. An entity controls an

asset in case it is capable of gaining the earnings deriving of the asset or restricting others in it. Future

economic benefits may arise from cost savings realized by the asset or direct increase in incomes or from

any economic events related to the use of the asset. On the other hand once emissions have occurred, the

entity has the liability to deliver allowances equal to emissions that have been made.

“A comparison of the characteristics of ecological resources and of traditional intangible resources shows

points of similarity that may cause an equivalent treatment in the annual accounts.” (Edeltraud 2006:235)

Accordingly emission allowances are to be considered as intangible assets. The recognition of an item as

an intangible asset requires an entity to demonstrate that the item meets:

(a) the definition of an intangible asset; and

(b) the recognition criteria.

An emission allowance meets the definition of an intangible asset, namely it is an identifiable non-

monetary asset without physical substance. An asset meets the identifiability criterion in the definition of

an intangible asset when it:

(a) is separable, i.e. is capable of being separated or divided from the entity and sold, transferred,

licensed, rented or exchanged, either individually or together with a related contract, asset or

liability; or

(b) arises from contractual or other legal rights, regardless of whether those rights are transferable

or separable from the entity or from other rights and obligations.

An intangible asset shall be recognized if, and only if:

(a) it is probable that the expected future economic benefits that are attributable to the asset will

flow to the entity; and

(b) the cost of the asset can be measured reliably.

Emission allowances are basic rights, which permanently serve the operation of the entity. The emission

permit and the pollution rights obtained are fundamental requirements for the continued operation of the

entity. Operation of enterprises under Directive 2003/87/EC requires a greenhouse gas emission permit:

“Member States shall ensure that, from 1 January 2005, no installation undertakes any activity listed in

Annex I resulting in emissions specified in relation to that activity unless its operator holds a permit issued

by a competent authority in accordance with Articles 5 and 6” (Article 4). Emission allowances to be

allocated in the given calendar year shall be allocated by February 28 of each trading year. Entities are

obliged to deliver allowances corresponding to their emissions by April 30 of the following year at the

latest. These are then deleted from the Transaction Log.

Entities are free to buy and sell allowances. Thus an entity has three options:

1. it can emit equal to its initial allocation;

2. it can emit less than its initial allocation, and sell or bank excess allowances;

3. it can emit more than its initial allocation, in which case it must buy additional allowances for

the excess emissions or borrow from next year’s allocation or pay a penalty.

- 6 -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

An entity can also sell some or even all of its allowances in the expectation of later buying allowances

equal to actual emissions.

Entities generally have two opportunities with regards to the recognition of emission allowances. If the

allowance is expected to be settled more than 12 months after the balance sheet date, it shall be recognized

as an intangible asset under IAS 38 Intangible Assets among the non-current assets. In a given trading

period the allowance not used in the current year can be transferred to the following year. If the allowance

is expected to hold primarily for trading, it shall be recognized as non-current asset held for sale under

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations.

An entity shall classify the emission allowance as non-current asset held for sale if its carrying amount

will be recovered principally through a sale transaction rather than through continuing use. For this to be

the case, the asset must be available for immediate sale in its present condition subject only to terms that

are usual and customary for sales of such assets and its sale must be highly probable. For the sale to be

highly probable, the appropriate level of management must be committed to a plan to sell the asset, and an

active programme to locate a buyer and complete the plan must have been initiated. Further, the asset must

be actively marketed for sale at a price that is reasonable in relation to its current fair value. In addition,

the sale should be expected to qualify for recognition as a completed sale within one year from the date of

classification.

The three options of an entity are linked to the following accounting recognition:

1. emission allowances shall be recognized as intangible assets;

2. emission allowances shall be recognized partly as intangible assets and partly as non-current

assets held for sale;

3. emission allowances shall be recognized as non-current assets held for sale.

4. Capitalization

On initial recognition an intangible asset shall be measured at fair value or at cost. Capitalization of

emission allowances has two major types: allocation by government and purchase.

(a) Allocation by government

According to the Directive 2003/87/EC Member States shall allocate at least 90 % of the allowances

free of charge for the five-year period beginning 1 January 2008. Allowances that are allocated free of

charge or for less than fair value by the government shall be measured initially at their fair value. Fair

value is the amount for which the allowance could be exchanged between knowledgeable, willing

parties in an arm’s length transaction. In these cases the difference between the amount paid and fair

value is a government grant that shall be accounted under IAS 20 Accounting for Government Grants

and Disclosure of Government Assistance. In accordance to IAS 20 such a grant should be measured

at fair or nominal value. “The IFRIC agreed that the estimation at nominal value should not be

permitted for emission rights, since this would not enable the equal treatment of allowances allocated

free of charge and sold allowances.” (Edeltraud 2006:232) Accordingly, the grant is initially

recognized as deferred income in the balance sheet and subsequently recognized as income on a

systematic basis over the compliance period for which the allowances were allocated.

(b) Purchase

In case an entity has fewer permits than the emissions it generates, it should either finance an anti-

pollution investment or purchase allowances at OTC markets, auctions or at the stock exchange.

Allowances purchased shall be measured initially at cost. The cost of a separately acquired intangible

asset comprises its purchase price and any directly attributable cost of preparing the asset for its

intended use.

- 7 -

equal to actual emissions.

Entities generally have two opportunities with regards to the recognition of emission allowances. If the

allowance is expected to be settled more than 12 months after the balance sheet date, it shall be recognized

as an intangible asset under IAS 38 Intangible Assets among the non-current assets. In a given trading

period the allowance not used in the current year can be transferred to the following year. If the allowance

is expected to hold primarily for trading, it shall be recognized as non-current asset held for sale under

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations.

An entity shall classify the emission allowance as non-current asset held for sale if its carrying amount

will be recovered principally through a sale transaction rather than through continuing use. For this to be

the case, the asset must be available for immediate sale in its present condition subject only to terms that

are usual and customary for sales of such assets and its sale must be highly probable. For the sale to be

highly probable, the appropriate level of management must be committed to a plan to sell the asset, and an

active programme to locate a buyer and complete the plan must have been initiated. Further, the asset must

be actively marketed for sale at a price that is reasonable in relation to its current fair value. In addition,

the sale should be expected to qualify for recognition as a completed sale within one year from the date of

classification.

The three options of an entity are linked to the following accounting recognition:

1. emission allowances shall be recognized as intangible assets;

2. emission allowances shall be recognized partly as intangible assets and partly as non-current

assets held for sale;

3. emission allowances shall be recognized as non-current assets held for sale.

4. Capitalization

On initial recognition an intangible asset shall be measured at fair value or at cost. Capitalization of

emission allowances has two major types: allocation by government and purchase.

(a) Allocation by government

According to the Directive 2003/87/EC Member States shall allocate at least 90 % of the allowances

free of charge for the five-year period beginning 1 January 2008. Allowances that are allocated free of

charge or for less than fair value by the government shall be measured initially at their fair value. Fair

value is the amount for which the allowance could be exchanged between knowledgeable, willing

parties in an arm’s length transaction. In these cases the difference between the amount paid and fair

value is a government grant that shall be accounted under IAS 20 Accounting for Government Grants

and Disclosure of Government Assistance. In accordance to IAS 20 such a grant should be measured

at fair or nominal value. “The IFRIC agreed that the estimation at nominal value should not be

permitted for emission rights, since this would not enable the equal treatment of allowances allocated

free of charge and sold allowances.” (Edeltraud 2006:232) Accordingly, the grant is initially

recognized as deferred income in the balance sheet and subsequently recognized as income on a

systematic basis over the compliance period for which the allowances were allocated.

(b) Purchase

In case an entity has fewer permits than the emissions it generates, it should either finance an anti-

pollution investment or purchase allowances at OTC markets, auctions or at the stock exchange.

Allowances purchased shall be measured initially at cost. The cost of a separately acquired intangible

asset comprises its purchase price and any directly attributable cost of preparing the asset for its

intended use.

- 7 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date of recognition is the day on which the Member State credits the emission allowances in the

Transaction Log for the entity and, in other cases, the day of the contractual performance.

5. Measurement

5.1. Emission allowances recognized as intangible assets

5.1.1. Cost model or revaluation model

If emission allowances are recognized as intangible assets, an entity shall choose either the cost model or

the revaluation model as its accounting policy. If an emission allowance is accounted for using the

revaluation model, all the others shall also be accounted for using the same model.

Cost model: After initial recognition, an emission allowance shall be carried at its cost less any

accumulated impairment losses.

Revaluation model: After initial recognition, an emission allowance shall be carried at a revalued amount,

being its fair value at the date of the revaluation less any subsequent accumulated impairment losses. Fair

value shall be determined by reference to an active market. Revaluations shall be made with such

regularity that at the balance sheet date the carrying amount of the asset does not differ materially from its

fair value. An active market is a market in which all the following conditions exist:

(a) the items traded in the market are homogeneous;

(b) willing buyers and sellers can normally be found at any time; and

(c) prices are available to the public.

If an allowance’s carrying amount is increased as a result of a revaluation, the increase shall be credited

directly to equity under the heading of revaluation surplus. However, the increase shall be recognized in

profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognized in

profit or loss. If an allowance’s carrying amount is decreased as a result of a revaluation, the decrease shall

be recognized in profit or loss. However, the decrease shall be debited directly to equity under the heading

of revaluation surplus to the extent of any credit balance in the revaluation surplus in respect of that

allowance. The carrying amount modification of the revalued allowance can be accounted by gross or by

net method. The gross method reaccounts the accumulated amortisation proportionally to the change in

gross value and both the gross value and the accumulated amortisation are modified by this ratio. The net

method carries the accumulated amortisation and the gross value together. So thus the net value is

modified to the revalued amount. Considering that emission allowances shall not be amortised, the net

method shall be regarded as adaptable method.

5.1.2. Amortisation

Amortisation is difficult to interpret for emission allowances. The expected usage of emission allowances

is not followed by physical consumption or moral obsolescence. Allowances allocated and not used in the

first year of the trading period can be transferred to the following years and considered as a performance

in the given year.

5.1.3. Impairment

The objective of impairment is to ensure that an entity’s assets are carried at no more than their

recoverable amount. An asset is carried at more than its recoverable amount if its carrying amount exceeds

- 8 -

Transaction Log for the entity and, in other cases, the day of the contractual performance.

5. Measurement

5.1. Emission allowances recognized as intangible assets

5.1.1. Cost model or revaluation model

If emission allowances are recognized as intangible assets, an entity shall choose either the cost model or

the revaluation model as its accounting policy. If an emission allowance is accounted for using the

revaluation model, all the others shall also be accounted for using the same model.

Cost model: After initial recognition, an emission allowance shall be carried at its cost less any

accumulated impairment losses.

Revaluation model: After initial recognition, an emission allowance shall be carried at a revalued amount,

being its fair value at the date of the revaluation less any subsequent accumulated impairment losses. Fair

value shall be determined by reference to an active market. Revaluations shall be made with such

regularity that at the balance sheet date the carrying amount of the asset does not differ materially from its

fair value. An active market is a market in which all the following conditions exist:

(a) the items traded in the market are homogeneous;

(b) willing buyers and sellers can normally be found at any time; and

(c) prices are available to the public.

If an allowance’s carrying amount is increased as a result of a revaluation, the increase shall be credited

directly to equity under the heading of revaluation surplus. However, the increase shall be recognized in

profit or loss to the extent that it reverses a revaluation decrease of the same asset previously recognized in

profit or loss. If an allowance’s carrying amount is decreased as a result of a revaluation, the decrease shall

be recognized in profit or loss. However, the decrease shall be debited directly to equity under the heading

of revaluation surplus to the extent of any credit balance in the revaluation surplus in respect of that

allowance. The carrying amount modification of the revalued allowance can be accounted by gross or by

net method. The gross method reaccounts the accumulated amortisation proportionally to the change in

gross value and both the gross value and the accumulated amortisation are modified by this ratio. The net

method carries the accumulated amortisation and the gross value together. So thus the net value is

modified to the revalued amount. Considering that emission allowances shall not be amortised, the net

method shall be regarded as adaptable method.

5.1.2. Amortisation

Amortisation is difficult to interpret for emission allowances. The expected usage of emission allowances

is not followed by physical consumption or moral obsolescence. Allowances allocated and not used in the

first year of the trading period can be transferred to the following years and considered as a performance

in the given year.

5.1.3. Impairment

The objective of impairment is to ensure that an entity’s assets are carried at no more than their

recoverable amount. An asset is carried at more than its recoverable amount if its carrying amount exceeds

- 8 -

the amount to be recovered through use or sale of the asset. If this is the case, the asset is described as

impaired and the entity shall recognise an impairment loss. An entity shall assess at each reporting date

whether there is any indication that an allowance may be impaired.

External sources of information are, for example, decline in the market value, significant changes that

have an adverse effect on the entity, increases in market interest rates, and so on. Internal sources of

information are, for example, significant changes in the extent to which or the manner in which the

allowances are used or are expected to be used, and evidence from internal reporting indicating an

allowance is performing worse then expected. If any such indication exists, the entity shall estimate the

recoverable amount of the allowance.

The recoverable amount of an asset is the higher of its fair value less costs to sell and its value in use. Fair

value less costs to sell is the amount obtainable from the sale of an allowance in an arm’s length

transaction between knowledgeable, willing parties, less the costs of disposal. Value in use is the present

value of the future cash flows expected to be derived from an allowance. The following elements shall be

reflected in the calculation of an allowance’s value in use:

(a) an estimate of the future cash flows the entity expects to derive from the allowance;

(b) expectations about possible variations in the amount or timing of those future cash flows;

(c) the time value of money, represented by the current market risk-free rate of interest;

(d) the price for bearing the uncertainty inherent in the allowance; and

(e) other factors, such as illiquidity, that market participants would reflect in pricing the future cash

flows the entity expects to derive from the allowance.

If the recoverable amount of the allowance accounted for using the cost model is less than its carrying

amount, the carrying amount of the allowance shall be reduced to its recoverable amount. That reduction

is an impairment loss. An impairment loss shall be recognized in profit or loss. An impairment loss

recognized in prior periods for an allowance shall be reversed if there has been a change in the estimates

used to determine the allowance’s recoverable amount since the last impairment loss was recognized. The

increased carrying amount of the allowance attributable to a reversal of the impairment loss shall not

exceed the initial carrying amount of the allowance. A reversal of an impairment loss shall be recognized

in profit or loss.

If the allowance is accounted for using the revaluation model any impairment loss shall be treated as a

decrease in the equity under the heading of revaluation surplus to the extent of any credit balance in the

revaluation surplus in respect of that allowance. The remaining amount of decrease shall be recognized in

profit or loss. Any reversal of an impairment loss shall be treated as an increase in the equity under the

heading of revaluation surplus. If any impairment loss was accounted before, the increase shall be

recognized in profit or loss in the extent of the previous impairment loss. The remaining amount of

increase shall be recognized in the equity under the heading of revaluation surplus.

5.2. Emission allowances recognized as non-current assets held for sale

If emission allowances are recognized as non-current assets held for sale, they shall be measured at the

lower of carrying amount or fair value less costs to sell. An entity shall recognize an impairment loss for

any initial or subsequent write-down of an allowance to fair value less costs to sell. An entity shall

recognize a gain for any subsequent increase in fair value less costs to sell of an allowance, but not in

excess of the cumulative impairment loss that has been previously recognized. When the sale is expected

to occur beyond 1 year, the entity shall measure the costs to sell at their present value. Any increase in the

present value of the costs to sell shall be presented in profit or loss as a financing cost. It can happen that

the circumstances of allowances recognized as non-current assets held for sale change in such a way that

the criteria of recognition as non-current asset held for sale are not realized any more. For instance the

- 9 -

impaired and the entity shall recognise an impairment loss. An entity shall assess at each reporting date

whether there is any indication that an allowance may be impaired.

External sources of information are, for example, decline in the market value, significant changes that

have an adverse effect on the entity, increases in market interest rates, and so on. Internal sources of

information are, for example, significant changes in the extent to which or the manner in which the

allowances are used or are expected to be used, and evidence from internal reporting indicating an

allowance is performing worse then expected. If any such indication exists, the entity shall estimate the

recoverable amount of the allowance.

The recoverable amount of an asset is the higher of its fair value less costs to sell and its value in use. Fair

value less costs to sell is the amount obtainable from the sale of an allowance in an arm’s length

transaction between knowledgeable, willing parties, less the costs of disposal. Value in use is the present

value of the future cash flows expected to be derived from an allowance. The following elements shall be

reflected in the calculation of an allowance’s value in use:

(a) an estimate of the future cash flows the entity expects to derive from the allowance;

(b) expectations about possible variations in the amount or timing of those future cash flows;

(c) the time value of money, represented by the current market risk-free rate of interest;

(d) the price for bearing the uncertainty inherent in the allowance; and

(e) other factors, such as illiquidity, that market participants would reflect in pricing the future cash

flows the entity expects to derive from the allowance.

If the recoverable amount of the allowance accounted for using the cost model is less than its carrying

amount, the carrying amount of the allowance shall be reduced to its recoverable amount. That reduction

is an impairment loss. An impairment loss shall be recognized in profit or loss. An impairment loss

recognized in prior periods for an allowance shall be reversed if there has been a change in the estimates

used to determine the allowance’s recoverable amount since the last impairment loss was recognized. The

increased carrying amount of the allowance attributable to a reversal of the impairment loss shall not

exceed the initial carrying amount of the allowance. A reversal of an impairment loss shall be recognized

in profit or loss.

If the allowance is accounted for using the revaluation model any impairment loss shall be treated as a

decrease in the equity under the heading of revaluation surplus to the extent of any credit balance in the

revaluation surplus in respect of that allowance. The remaining amount of decrease shall be recognized in

profit or loss. Any reversal of an impairment loss shall be treated as an increase in the equity under the

heading of revaluation surplus. If any impairment loss was accounted before, the increase shall be

recognized in profit or loss in the extent of the previous impairment loss. The remaining amount of

increase shall be recognized in the equity under the heading of revaluation surplus.

5.2. Emission allowances recognized as non-current assets held for sale

If emission allowances are recognized as non-current assets held for sale, they shall be measured at the

lower of carrying amount or fair value less costs to sell. An entity shall recognize an impairment loss for

any initial or subsequent write-down of an allowance to fair value less costs to sell. An entity shall

recognize a gain for any subsequent increase in fair value less costs to sell of an allowance, but not in

excess of the cumulative impairment loss that has been previously recognized. When the sale is expected

to occur beyond 1 year, the entity shall measure the costs to sell at their present value. Any increase in the

present value of the costs to sell shall be presented in profit or loss as a financing cost. It can happen that

the circumstances of allowances recognized as non-current assets held for sale change in such a way that

the criteria of recognition as non-current asset held for sale are not realized any more. For instance the

- 9 -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

entity can not or does not want to sell these allowances. In this case the entity shall reclassify the

allowances initially recognized as non-current assets held for sale. These allowances shall be measured at

the lower of the followings amounts:

(a) carrying amount modified by any impairment losses or revaluations which would have been

accounted if the allowance has not been recognized as non-current asset held for sale; or

(b) fair value less costs to sell at the date of reclassification.

The difference deriving from reclassification shall be recognized in profit or loss.

5.3. Fair value of emission allowances

As opposed to other rights of financial value, the value of emission allowances is not determined by

benefits and expected future revenue arising from their possession. In reality, it is only the relative market

supply and demand and their situation and volume that influence market prices of allowances. As a result,

the price of allowances has fallen under €1 from the original unit price of €15 to €20. In April 2006 it

became evident that Member States allocated too many allowances and thus there is surplus, and there are

only few companies in scarcity wanting to purchase them. The commitments of the Kyoto Protocol

amount to real objectives only when entities receive allowances in a quantity which corresponds to their

actual production and, what’s more, it is actually the reduction of emissions that has to be achieved on the

long term.

6. Provision

According to the Directive 2003/87/EC “Member States shall ensure that, by 30 April each year at the

latest, the entity of each installation surrenders a number of allowances equal to the total emissions from

that installation during the preceding calendar year and that these are subsequently cancelled”. (Article 12)

“At the start of the compliance period when allowances are allocated, there is no liability yet in agreement

with IAS 37 Provisions, Contingent Liabilities and Contingent Assets, since obligations can only arise

from past events.” (Edeltraud 2006:232) Once emissions are made, a liability is recognized for the

obligation to deliver allowances equal to emissions that have been made. This liability shall be accounted

as provision. The liability is settled by delivering allowances, incurring a penalty or a combination of both.

The liability shall be measured at the best estimate of the expenditure required to settle the present

obligation at the balance sheet date. This will normally be the present market price of the number of

allowances required to cover emissions made up to the balance sheet date. However, if the entity’s best

estimate is that some or all of the obligation will be settled by incurring a cash penalty, it shall measure

that part of its obligation at the cost of the penalty rather than at the market price of the relevant number of

allowances. At the balance sheet date or at interim reporting date the liability to return allowances is

recognized as an expense in the income statement. When the entity delivers emission allowances equal to

emissions that have been made in the previous year, the allowances shall be derecognized over against the

liability to return allowances. The remaining amount of the provision shall be derecognized as income.

7. Derecognition

7.1. Transfer

Emission allowances are subject to free trading. “Member States shall ensure that allowances can be

transferred between:

(a) persons within the Community;

(b) persons within the Community and persons in third countries, where such allowances are

recognized in accordance with the procedure referred to in Article 25 without restrictions other

- 10 -

allowances initially recognized as non-current assets held for sale. These allowances shall be measured at

the lower of the followings amounts:

(a) carrying amount modified by any impairment losses or revaluations which would have been

accounted if the allowance has not been recognized as non-current asset held for sale; or

(b) fair value less costs to sell at the date of reclassification.

The difference deriving from reclassification shall be recognized in profit or loss.

5.3. Fair value of emission allowances

As opposed to other rights of financial value, the value of emission allowances is not determined by

benefits and expected future revenue arising from their possession. In reality, it is only the relative market

supply and demand and their situation and volume that influence market prices of allowances. As a result,

the price of allowances has fallen under €1 from the original unit price of €15 to €20. In April 2006 it

became evident that Member States allocated too many allowances and thus there is surplus, and there are

only few companies in scarcity wanting to purchase them. The commitments of the Kyoto Protocol

amount to real objectives only when entities receive allowances in a quantity which corresponds to their

actual production and, what’s more, it is actually the reduction of emissions that has to be achieved on the

long term.

6. Provision

According to the Directive 2003/87/EC “Member States shall ensure that, by 30 April each year at the

latest, the entity of each installation surrenders a number of allowances equal to the total emissions from

that installation during the preceding calendar year and that these are subsequently cancelled”. (Article 12)

“At the start of the compliance period when allowances are allocated, there is no liability yet in agreement

with IAS 37 Provisions, Contingent Liabilities and Contingent Assets, since obligations can only arise

from past events.” (Edeltraud 2006:232) Once emissions are made, a liability is recognized for the

obligation to deliver allowances equal to emissions that have been made. This liability shall be accounted

as provision. The liability is settled by delivering allowances, incurring a penalty or a combination of both.

The liability shall be measured at the best estimate of the expenditure required to settle the present

obligation at the balance sheet date. This will normally be the present market price of the number of

allowances required to cover emissions made up to the balance sheet date. However, if the entity’s best

estimate is that some or all of the obligation will be settled by incurring a cash penalty, it shall measure

that part of its obligation at the cost of the penalty rather than at the market price of the relevant number of

allowances. At the balance sheet date or at interim reporting date the liability to return allowances is

recognized as an expense in the income statement. When the entity delivers emission allowances equal to

emissions that have been made in the previous year, the allowances shall be derecognized over against the

liability to return allowances. The remaining amount of the provision shall be derecognized as income.

7. Derecognition

7.1. Transfer

Emission allowances are subject to free trading. “Member States shall ensure that allowances can be

transferred between:

(a) persons within the Community;

(b) persons within the Community and persons in third countries, where such allowances are

recognized in accordance with the procedure referred to in Article 25 without restrictions other

- 10 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

than those contained in, or adopted pursuant to, this Directive.” (Article 12 of Directive

2003/87/EC)

The national regulation may specify some restrictions on transfer as penalty. The Hungarian Act on the

trading of emission allowances of greenhouse gases orders for example the following: “Without regard to

the payment of penalties when the entity partly or completely fails to comply with its reporting and

auditing obligations and with its obligation to surrender emission allowances by the deadline, it shall not

be entitled to sell emission allowances until the submission of its properly audited report.”

Gains or losses arising from the transfer of an emission allowance shall be determined as the difference

between the net sale proceeds and the carrying amount of the allowance. It shall be recognized as income

or expense in profit or loss in the period in which the transfer occurs. The consideration receivable on

transfer of an emission allowance is recognized initially at fair value. If payment for an allowance is

deferred, the consideration received is recognized initially at the cash price equivalent. The difference

between the nominal amount of the consideration and the cash price equivalent is recognized as interest

revenue.

7.2. Cancellation

Member States shall cancel emission allowances:

(a) any time under the declaration of an entity submitted to the keeper of the Transaction Log;

(b) every year after delivering allowances equal to emissions that have been made;

(c) four months after the beginning of each subsequent five-year period those allowances which are

no longer valid and have not been surrendered and cancelled.

It is worth mentioning that Member States are allowed to issue allowances to entities for the current period

to replace any allowances held by them which are cancelled in accordance with point (c).

8. Alternative accounting interpretation on emission allowances

The above described accounting treatment of emission allowances follows the main principles of IFRIC 3

Emission Rights. However, the entity is allowed to choose other accounting treatment in the frame of

IFRS. (see Table 1.) It is a challenge for companies to decide which method is appropriate and acceptable.

Table 1. Alternative accounting treatments for emission allowances

ALTERNATIVE I. ALTERNATIVE II. ALTERNATIVE III.

Adaptation of IFRIC

3 in its entirety.

Recognition as intangible asset initially

at fair value, together with a government

grant in line with IFRIC 3, but

recognition a provision on the following

basis:

No recognition of an asset or deferred

income (if IAS 20’s accounting policy

choice of recognising the grant at

nominal amount is applied).

▪ to the extent that the entity holds a

sufficient number of allowances, the

provision should be recognised based

on the carrying value of those

allowances;

In case of shortfall in allowances, a

provision should be made for the best

estimate of the cost to be incurred to

meet the emission obligation, i.e. at the

present market price.

▪ to the extent that the entity does not

hold a sufficient number of allowances,

the provision should be recognised

based on the market value of emission

- 11 -

2003/87/EC)

The national regulation may specify some restrictions on transfer as penalty. The Hungarian Act on the

trading of emission allowances of greenhouse gases orders for example the following: “Without regard to

the payment of penalties when the entity partly or completely fails to comply with its reporting and

auditing obligations and with its obligation to surrender emission allowances by the deadline, it shall not

be entitled to sell emission allowances until the submission of its properly audited report.”

Gains or losses arising from the transfer of an emission allowance shall be determined as the difference

between the net sale proceeds and the carrying amount of the allowance. It shall be recognized as income

or expense in profit or loss in the period in which the transfer occurs. The consideration receivable on

transfer of an emission allowance is recognized initially at fair value. If payment for an allowance is

deferred, the consideration received is recognized initially at the cash price equivalent. The difference

between the nominal amount of the consideration and the cash price equivalent is recognized as interest

revenue.

7.2. Cancellation

Member States shall cancel emission allowances:

(a) any time under the declaration of an entity submitted to the keeper of the Transaction Log;

(b) every year after delivering allowances equal to emissions that have been made;

(c) four months after the beginning of each subsequent five-year period those allowances which are

no longer valid and have not been surrendered and cancelled.

It is worth mentioning that Member States are allowed to issue allowances to entities for the current period

to replace any allowances held by them which are cancelled in accordance with point (c).

8. Alternative accounting interpretation on emission allowances

The above described accounting treatment of emission allowances follows the main principles of IFRIC 3

Emission Rights. However, the entity is allowed to choose other accounting treatment in the frame of

IFRS. (see Table 1.) It is a challenge for companies to decide which method is appropriate and acceptable.

Table 1. Alternative accounting treatments for emission allowances

ALTERNATIVE I. ALTERNATIVE II. ALTERNATIVE III.

Adaptation of IFRIC

3 in its entirety.

Recognition as intangible asset initially

at fair value, together with a government

grant in line with IFRIC 3, but

recognition a provision on the following

basis:

No recognition of an asset or deferred

income (if IAS 20’s accounting policy

choice of recognising the grant at

nominal amount is applied).

▪ to the extent that the entity holds a

sufficient number of allowances, the

provision should be recognised based

on the carrying value of those

allowances;

In case of shortfall in allowances, a

provision should be made for the best

estimate of the cost to be incurred to

meet the emission obligation, i.e. at the

present market price.

▪ to the extent that the entity does not

hold a sufficient number of allowances,

the provision should be recognised

based on the market value of emission

- 11 -

ALTERNATIVE I. ALTERNATIVE II. ALTERNATIVE III.

rights required to cover the shortfall;

▪ to the extent of the penalty that will be

incurred.

Source: Deloitte, 2008

9. Fees and penalties

Entities are obliged to pay fees as determined by national regulations for the operation of the system of

emission allowances. The Hungarian regulation orders the following fees.

(a) An entity is obliged to pay an annual supervisory fee as of the effective date of its emission

permit. The environmental authority shall spend the amount generated from the supervisory

fees on its activities relating to the operation of the emissions trading system.

(b) An administration service provision fee shall be paid for the permit procedure of greenhouse gas

emissions and for the entry into the National Registry of Auditors and the European Community

Registry of Auditors.

(c) An account management fee shall be paid for the publicly authenticated registering and

managing of emission allowances (Transaction Log).

Entities are obliged to pay penalty in case of non-compliance with statutory obligations.

(a) At the end of the compliance period an entity is required to deliver allowances equal to its

actual emissions. If an entity does not deliver sufficient allowances, it will incur a penalty. The

penalty may take a variety of forms, including a cash payment, reductions in the allowances

allocated to the entity for subsequent periods and restrictions on its operations. The Directive

2003/87/EC specifies an excess emissions penalty which shall be EUR 100 for each ton of

carbon dioxide equivalent emitted for which the entity has not surrendered allowances. Payment

of the excess emissions penalty does not release the entity from the obligation to surrender an

amount of allowances equal to those excess emissions when surrendering allowances in relation

to the following calendar year.

(b) If an entity fails to perform monitoring and reporting on greenhouse gas emissions in

compliance with the regulation or the content of the emission permit, or it operates without an

emission permit, the entity has to pay penalty.

(c) If an entity fails to comply with its reporting compliance or change notification obligations, the

entity is obliged to pay penalty.

(d) If an entity fails to comply with its obligation to pay the fee for the account by the deadline, it

has to pay interest on arrears.

- 12 -

rights required to cover the shortfall;

▪ to the extent of the penalty that will be

incurred.

Source: Deloitte, 2008

9. Fees and penalties

Entities are obliged to pay fees as determined by national regulations for the operation of the system of

emission allowances. The Hungarian regulation orders the following fees.

(a) An entity is obliged to pay an annual supervisory fee as of the effective date of its emission

permit. The environmental authority shall spend the amount generated from the supervisory

fees on its activities relating to the operation of the emissions trading system.

(b) An administration service provision fee shall be paid for the permit procedure of greenhouse gas

emissions and for the entry into the National Registry of Auditors and the European Community

Registry of Auditors.

(c) An account management fee shall be paid for the publicly authenticated registering and

managing of emission allowances (Transaction Log).

Entities are obliged to pay penalty in case of non-compliance with statutory obligations.

(a) At the end of the compliance period an entity is required to deliver allowances equal to its

actual emissions. If an entity does not deliver sufficient allowances, it will incur a penalty. The

penalty may take a variety of forms, including a cash payment, reductions in the allowances

allocated to the entity for subsequent periods and restrictions on its operations. The Directive

2003/87/EC specifies an excess emissions penalty which shall be EUR 100 for each ton of