Analysis of Consolidated Financial Accounts and Group Evaluation

VerifiedAdded on 2023/06/11

|6

|1300

|323

Report

AI Summary

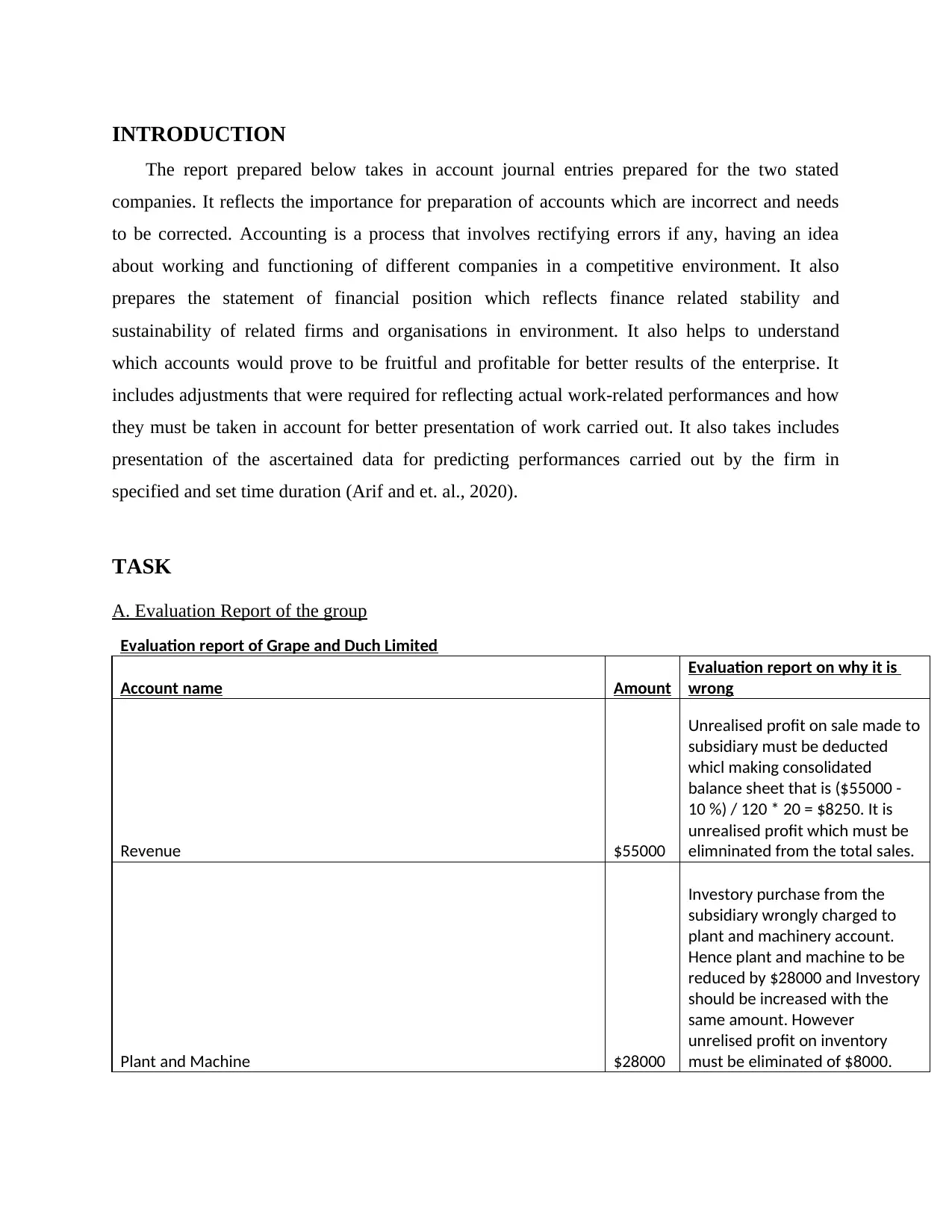

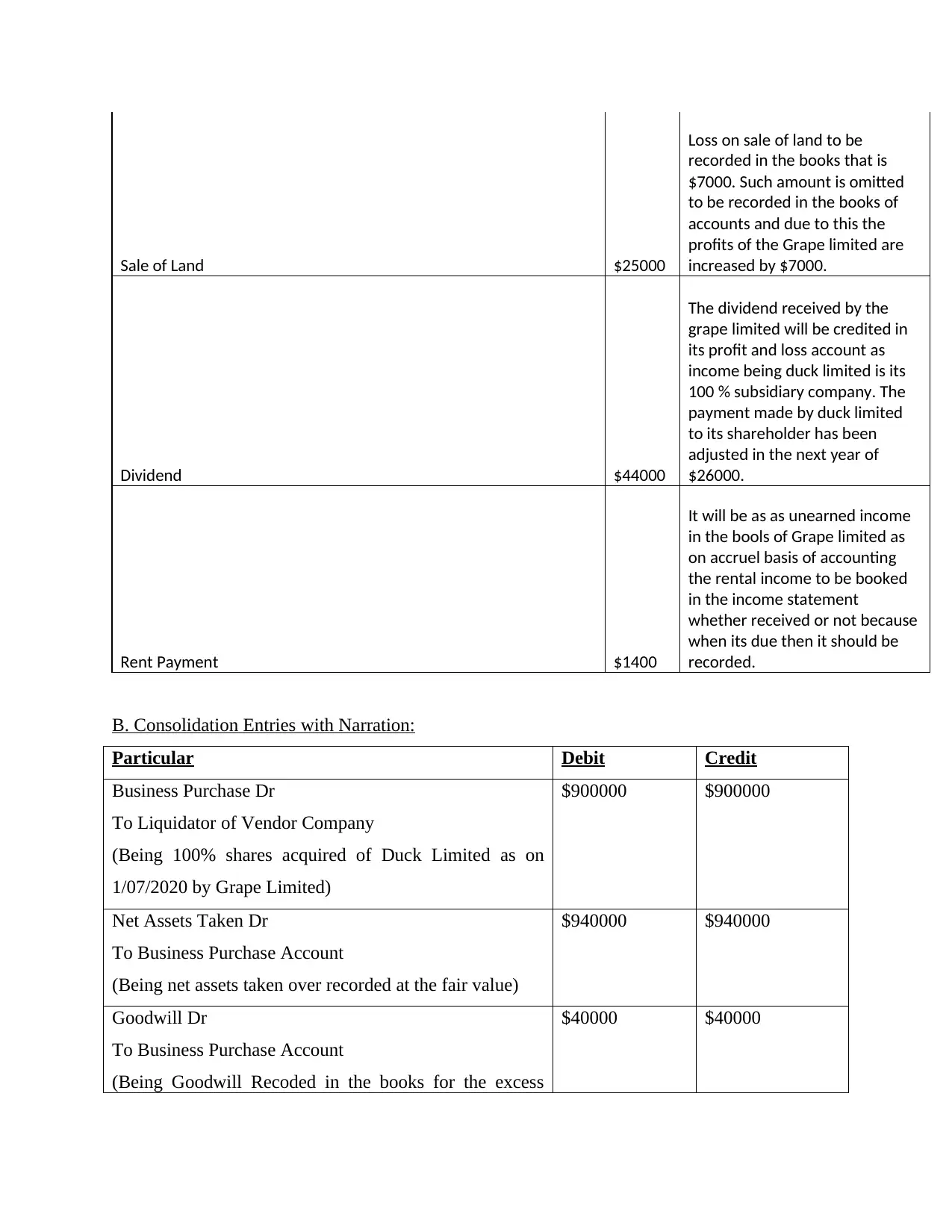

This report provides an evaluation of Grape and Duch Limited, focusing on correcting accounting errors and preparing consolidated financial statements. It addresses unrealized profits, incorrect inventory charges, omitted land sale losses, and dividend adjustments. The report includes consolidation entries, a consolidation worksheet, and consolidated financial accounts, demonstrating the importance of accurate accounting for assessing company performance and ensuring financial stability. It also highlights the adjustments needed for a clear representation of work-related activities and improved financial reporting, emphasizing how proper accounting practices contribute to business growth and expansion. Desklib offers a wealth of similar solved assignments for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.