University Accounting Report: Chipps Ltd Expenditure Cycle Review

VerifiedAdded on 2023/03/23

|5

|742

|90

Report

AI Summary

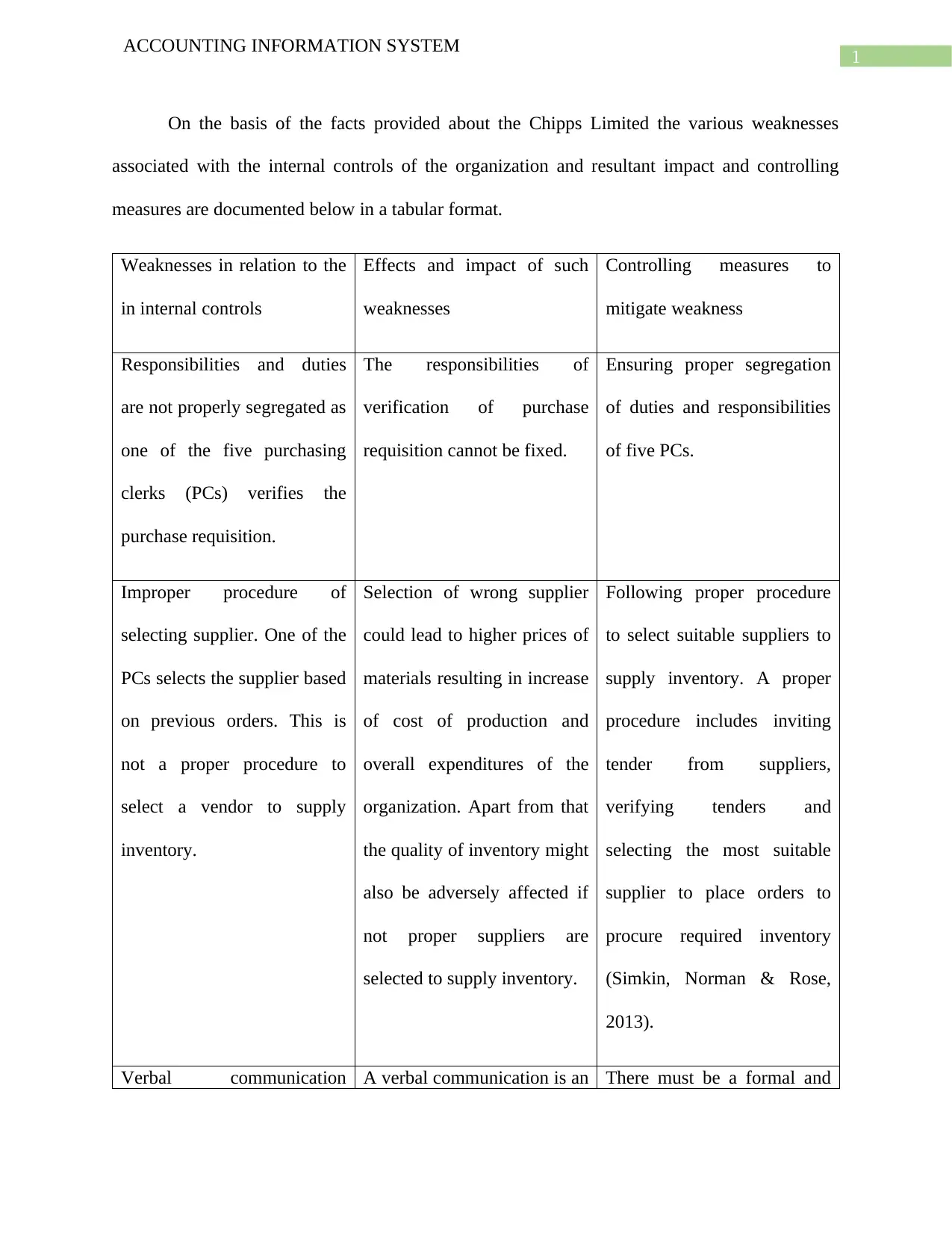

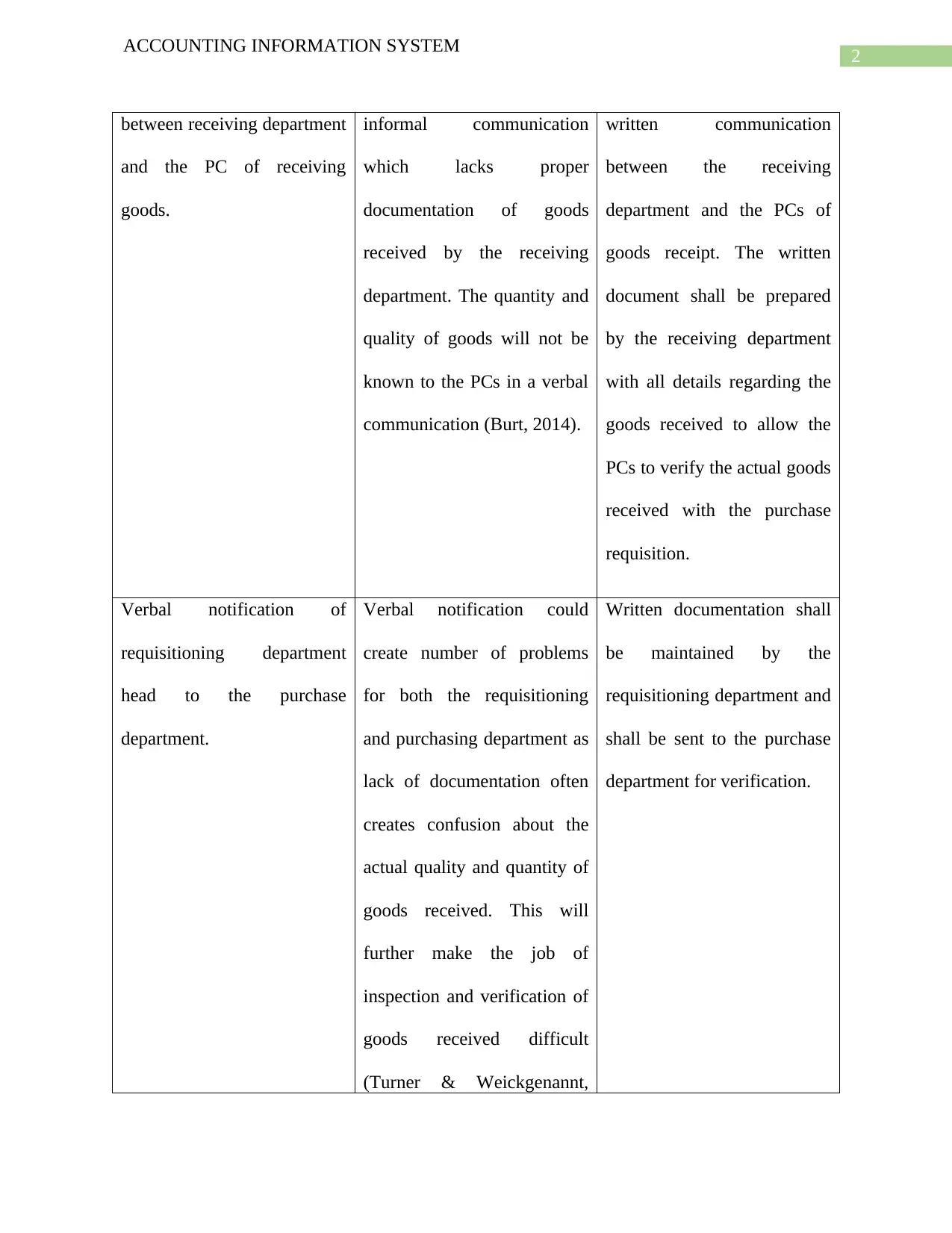

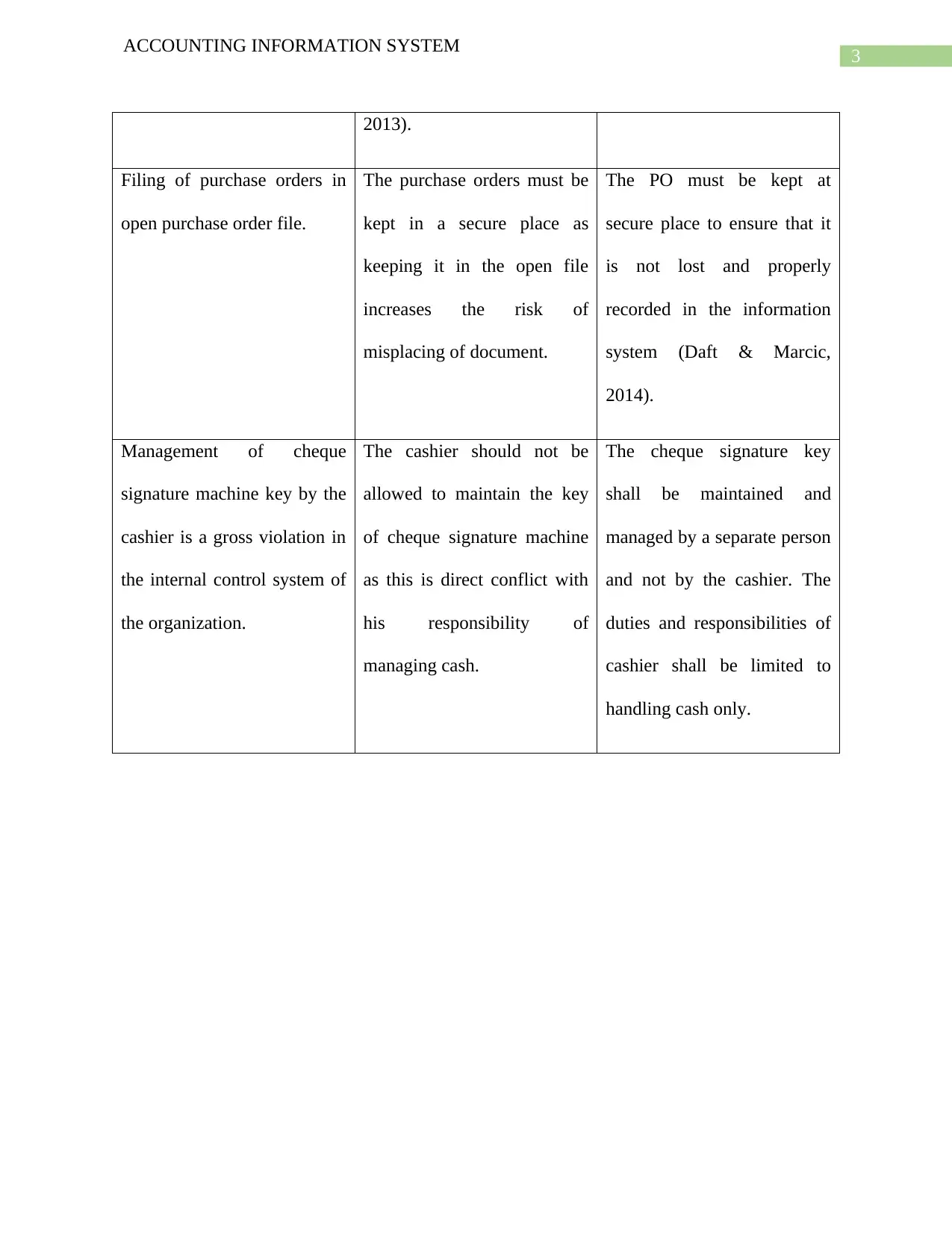

This report analyzes the expenditure cycle of Chipps Limited, a medium-sized Australian enterprise manufacturing computer parts. The report, prepared for the CEO, Mrs. Sophia Martin, identifies weaknesses in the company's internal controls related to inventory purchasing and management. These weaknesses include improper segregation of duties, flawed supplier selection processes, reliance on verbal communication, and inadequate document filing procedures, as well as poor management of cheque signature keys. The report details the potential impacts of each weakness, such as increased costs, inventory quality issues, and confusion in communication. Furthermore, it provides practical, short-term internal controls to mitigate these weaknesses. These controls include proper segregation of duties, implementing a formal supplier selection procedure, transitioning to written communication, securing purchase orders, and securing the cheque signature key. The analysis is presented in a tabular format, providing a clear overview of the issues and recommended solutions. The report is based on the information provided about Chipps' inventory purchasing and management, and it references relevant accounting literature to support the analysis.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.