Accounting Report: Fair Value, Impairment, and Medibank Analysis

VerifiedAdded on 2023/04/21

|11

|2457

|399

Report

AI Summary

This report addresses key accounting concepts including fair value measurement, impairment testing, and relevant accounting standards such as AASB 13/IFRS 13, AASB 116/IAS 16, and AASB 136/IAS 39. The report begins with a discussion on whether Simba Ltd should adopt the fair value revaluation model for fixed assets, considering the challenges of determining fair value for certain assets and its potential impact on the company's financial statements. The second part of the report clarifies the relevance of impairment testing and its relationship with the revaluation model, clarifying the differences between them. Finally, the report analyzes Medibank's 2018 annual report to assess its compliance with the aforementioned accounting standards. This analysis includes a review of the company's valuation techniques, disclosures regarding impairment of assets, and the application of fair value accounting to various assets, including goodwill and other financial assets. The report also examines the company's impairment testing procedures and disclosures in accordance with AASB 136. The provided references support the analysis and findings.

Accounting

Assignment

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

By student name

Professor

University

Date: 31st March 2019.

Page 1

Professor

University

Date: 31st March 2019.

Page 1

Table of Contents

Question 1..................................................................................................................... 3

Question 2..................................................................................................................... 3

Question 3..................................................................................................................... 4

References............................................................................................................... 11

Page 2

Question 1..................................................................................................................... 3

Question 2..................................................................................................................... 3

Question 3..................................................................................................................... 4

References............................................................................................................... 11

Page 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 1

The board of directors of Simba Ltd believe adopting a method of fair value for the valuation of

the assets will help the company in making the financial statements look better, and that would

eliminate the need for depreciation for the company. Most of these assets are not possible to be

obtained easily and the overall valuation of the same is also very difficult. So, the board of

director has given this proposal.

Fair value measurement is a method that uses the current market prices of the assets to value

them. There are different approaches based on which fair value can be calculated which includes

market approach, income approach or cost approach. But this does not eliminate the need for

calculation of depreciation, it leads to the revaluation model, where the assets carried on the

books is equivalent to asset fair value reduced by the accumulated depreciation and accumulated

impairment losses. So, the best advantage of using such kind of method is that it helps in

maintaining accurate valuation, thus the users can refer to the financial statements of the

company and get a correct value of the company and its assets all over. It also makes sure that

the management of the company is not manipulating with its data and the reported net income of

the company. But it is affected by the market conditions which fluctuates on many ends. Thus, it

can be said that the board of directors should adopt these proposal and value their asset as per

fair value accounting.

Question 2

The main characters of impairment testing are to make sure that the assets are carried by the

company at a price that is not more than the recoverable amount of the asset. This helps in

ensuring that overvaluation of the assets is not done and so the financial statements shows a true

position of the company and its overall financial position. In case of the revaluation model the

carrying amount of the assets increases decreases in sync with the fluctuations in the fair value of

the asset. Even though both are fairly connected there is a difference in them and that is very

apparent from its accounting. In case a company ignores the recoverable value of the asset then

there are chances that the assets fair value might exceed its recoverable value, and this will

Page 3

The board of directors of Simba Ltd believe adopting a method of fair value for the valuation of

the assets will help the company in making the financial statements look better, and that would

eliminate the need for depreciation for the company. Most of these assets are not possible to be

obtained easily and the overall valuation of the same is also very difficult. So, the board of

director has given this proposal.

Fair value measurement is a method that uses the current market prices of the assets to value

them. There are different approaches based on which fair value can be calculated which includes

market approach, income approach or cost approach. But this does not eliminate the need for

calculation of depreciation, it leads to the revaluation model, where the assets carried on the

books is equivalent to asset fair value reduced by the accumulated depreciation and accumulated

impairment losses. So, the best advantage of using such kind of method is that it helps in

maintaining accurate valuation, thus the users can refer to the financial statements of the

company and get a correct value of the company and its assets all over. It also makes sure that

the management of the company is not manipulating with its data and the reported net income of

the company. But it is affected by the market conditions which fluctuates on many ends. Thus, it

can be said that the board of directors should adopt these proposal and value their asset as per

fair value accounting.

Question 2

The main characters of impairment testing are to make sure that the assets are carried by the

company at a price that is not more than the recoverable amount of the asset. This helps in

ensuring that overvaluation of the assets is not done and so the financial statements shows a true

position of the company and its overall financial position. In case of the revaluation model the

carrying amount of the assets increases decreases in sync with the fluctuations in the fair value of

the asset. Even though both are fairly connected there is a difference in them and that is very

apparent from its accounting. In case a company ignores the recoverable value of the asset then

there are chances that the assets fair value might exceed its recoverable value, and this will

Page 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

happen in situations where the recoverable value of the asset is equal to the fair value reduced by

the cost of disposal of the asset. If the asset is revalued to the fair value its carrying amount is

overstated by the disposal cost of the assets. Also, impairment testing is done every year and in

case of revaluation it is done in every 3-5 years. In case impairment losses are ignored it

increases the risk of potential overstatement of the assets. In short impairment is relevant to the

assets that are covered under the model of revaluation and those assets are tested for impairment,

and same applies to land and building also.

Question 3

In the following segment the annual report of the Medibank for 2018 has been downloaded and

analyzed to evaluate whether the annual report of the company is consistent with the

requirements of AASB 13/IFRS 13 Fair value Measurement, AASB 116/IAS 16 Property Plant

and Equipment, and AASB 136/IAS 39 Impairment of Assets.

a) In case of the following case all the assets have been measured under the historical cost

method except financial assets like grant (Johan, 2018). These financial assets consist of

externally managed equity trusts and direct mandates and internally managed fixed

income portfolios. Land and Building have been measured under the fair value method.

The liabilities that are measured at present value of expected future payments. The fair

value of the investments has been calculated using different techniques that includes

making conventions based on the overall market conditions. It also includes valuation

methods like the quoted market prices, and dealer quotation for similar instruments and

many other similar techniques are followed by the company (Yadao, 2018).

b) In the annual report, the management has made disclosures in the notes to account section

with respect to the kind of valuation technique that has been followed and what

measurement basis has been taken in case of most of the assets.

Page 4

the cost of disposal of the asset. If the asset is revalued to the fair value its carrying amount is

overstated by the disposal cost of the assets. Also, impairment testing is done every year and in

case of revaluation it is done in every 3-5 years. In case impairment losses are ignored it

increases the risk of potential overstatement of the assets. In short impairment is relevant to the

assets that are covered under the model of revaluation and those assets are tested for impairment,

and same applies to land and building also.

Question 3

In the following segment the annual report of the Medibank for 2018 has been downloaded and

analyzed to evaluate whether the annual report of the company is consistent with the

requirements of AASB 13/IFRS 13 Fair value Measurement, AASB 116/IAS 16 Property Plant

and Equipment, and AASB 136/IAS 39 Impairment of Assets.

a) In case of the following case all the assets have been measured under the historical cost

method except financial assets like grant (Johan, 2018). These financial assets consist of

externally managed equity trusts and direct mandates and internally managed fixed

income portfolios. Land and Building have been measured under the fair value method.

The liabilities that are measured at present value of expected future payments. The fair

value of the investments has been calculated using different techniques that includes

making conventions based on the overall market conditions. It also includes valuation

methods like the quoted market prices, and dealer quotation for similar instruments and

many other similar techniques are followed by the company (Yadao, 2018).

b) In the annual report, the management has made disclosures in the notes to account section

with respect to the kind of valuation technique that has been followed and what

measurement basis has been taken in case of most of the assets.

Page 4

Like in case of private health insurance scheme it has been stated that premium revenue

has been calculated based on the fair value method and the overall consideration is

recognized based on the straight-line basis between the date of accepting the overall

insurance risk and the date of paying up the overall amount of premium (Wendt, 2018).

In case of investments the fair value has been calculated using a variety of techniques that

includes making assumptions based on the overall market conditions. It also includes

valuation methods like the quoted market prices, or the dealer quotation for similar

instruments and yield curve calculations using the mid-yield. Also, the independent and

the vendor developed models are also followed by the company.

Fair value method of accounting is subjective, and the overall investments has been

categorized into a hierarchy that is dependent on the overall level of subjectivity

involved. The calculation of fair value hierarchy involves three different levels that

includes quoted prices, the next level being inputs other than the quoted prices, and the

last level is inputs for the asset and liability that is not based on the observable market

data (Webster, 2017). The group does not disclose the fair value of other financial assets

like the trade receivables as the overall cost involved is less and these assets are mostly of

short-term nature, the overall carrying amount of these assets are found to be approximate

to their fair value. All these disclosures regarding the type of assets, the type of valuation

method that has been followed and the overall fair value accounting that has been

undertaken is mentioned in the notes to account.

Question 3c)

Impairment of assets happens when the market price of the asset falls below the recorded value

of the asset in the financial statements. There are many assets that are tested in case of the given

company. Necessary disclosures and details regarding the same has been given the annual report

of the company in the notes to accounts sections (Vieira, O’Dwyer, & Schneider, 2017).

Page 5

has been calculated based on the fair value method and the overall consideration is

recognized based on the straight-line basis between the date of accepting the overall

insurance risk and the date of paying up the overall amount of premium (Wendt, 2018).

In case of investments the fair value has been calculated using a variety of techniques that

includes making assumptions based on the overall market conditions. It also includes

valuation methods like the quoted market prices, or the dealer quotation for similar

instruments and yield curve calculations using the mid-yield. Also, the independent and

the vendor developed models are also followed by the company.

Fair value method of accounting is subjective, and the overall investments has been

categorized into a hierarchy that is dependent on the overall level of subjectivity

involved. The calculation of fair value hierarchy involves three different levels that

includes quoted prices, the next level being inputs other than the quoted prices, and the

last level is inputs for the asset and liability that is not based on the observable market

data (Webster, 2017). The group does not disclose the fair value of other financial assets

like the trade receivables as the overall cost involved is less and these assets are mostly of

short-term nature, the overall carrying amount of these assets are found to be approximate

to their fair value. All these disclosures regarding the type of assets, the type of valuation

method that has been followed and the overall fair value accounting that has been

undertaken is mentioned in the notes to account.

Question 3c)

Impairment of assets happens when the market price of the asset falls below the recorded value

of the asset in the financial statements. There are many assets that are tested in case of the given

company. Necessary disclosures and details regarding the same has been given the annual report

of the company in the notes to accounts sections (Vieira, O’Dwyer, & Schneider, 2017).

Page 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

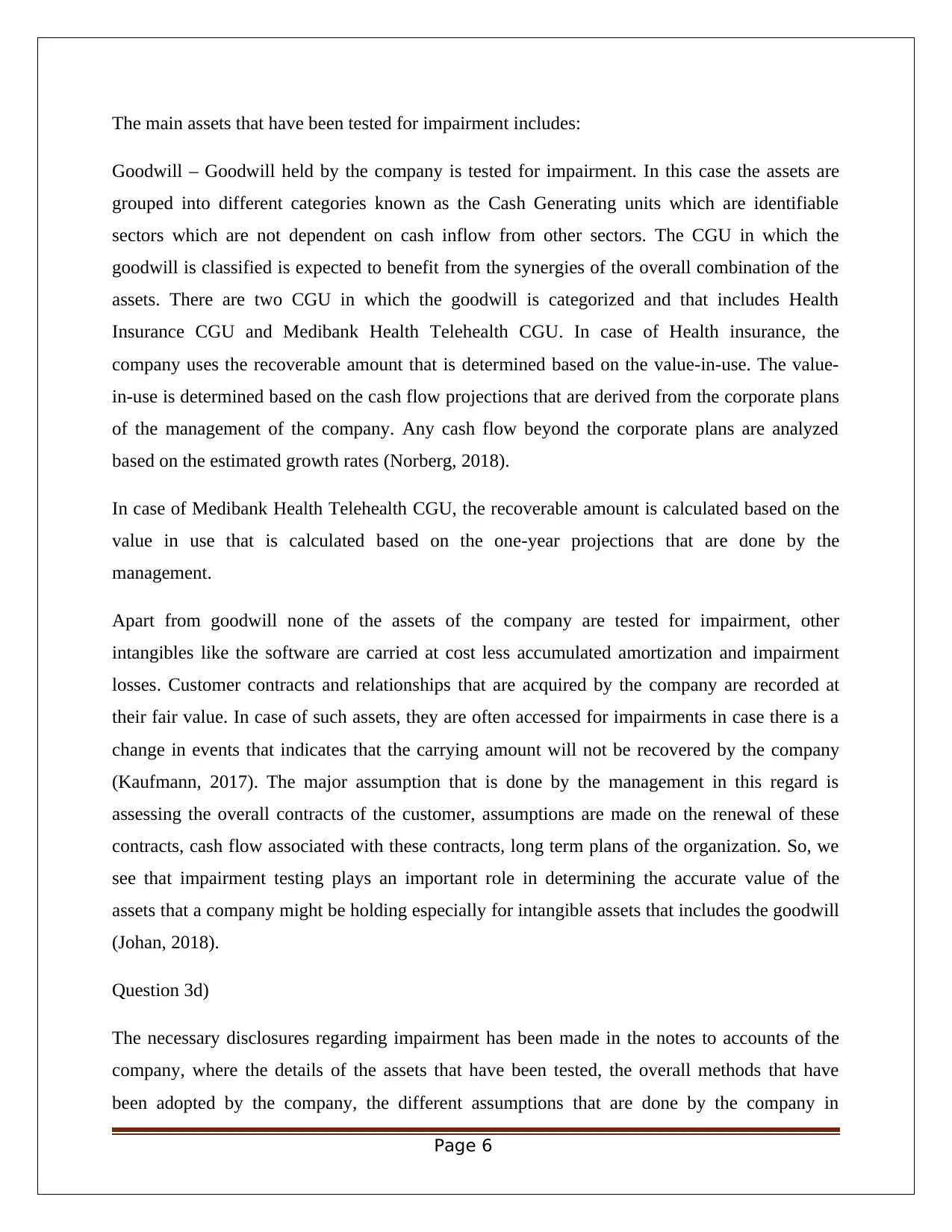

The main assets that have been tested for impairment includes:

Goodwill – Goodwill held by the company is tested for impairment. In this case the assets are

grouped into different categories known as the Cash Generating units which are identifiable

sectors which are not dependent on cash inflow from other sectors. The CGU in which the

goodwill is classified is expected to benefit from the synergies of the overall combination of the

assets. There are two CGU in which the goodwill is categorized and that includes Health

Insurance CGU and Medibank Health Telehealth CGU. In case of Health insurance, the

company uses the recoverable amount that is determined based on the value-in-use. The value-

in-use is determined based on the cash flow projections that are derived from the corporate plans

of the management of the company. Any cash flow beyond the corporate plans are analyzed

based on the estimated growth rates (Norberg, 2018).

In case of Medibank Health Telehealth CGU, the recoverable amount is calculated based on the

value in use that is calculated based on the one-year projections that are done by the

management.

Apart from goodwill none of the assets of the company are tested for impairment, other

intangibles like the software are carried at cost less accumulated amortization and impairment

losses. Customer contracts and relationships that are acquired by the company are recorded at

their fair value. In case of such assets, they are often accessed for impairments in case there is a

change in events that indicates that the carrying amount will not be recovered by the company

(Kaufmann, 2017). The major assumption that is done by the management in this regard is

assessing the overall contracts of the customer, assumptions are made on the renewal of these

contracts, cash flow associated with these contracts, long term plans of the organization. So, we

see that impairment testing plays an important role in determining the accurate value of the

assets that a company might be holding especially for intangible assets that includes the goodwill

(Johan, 2018).

Question 3d)

The necessary disclosures regarding impairment has been made in the notes to accounts of the

company, where the details of the assets that have been tested, the overall methods that have

been adopted by the company, the different assumptions that are done by the company in

Page 6

Goodwill – Goodwill held by the company is tested for impairment. In this case the assets are

grouped into different categories known as the Cash Generating units which are identifiable

sectors which are not dependent on cash inflow from other sectors. The CGU in which the

goodwill is classified is expected to benefit from the synergies of the overall combination of the

assets. There are two CGU in which the goodwill is categorized and that includes Health

Insurance CGU and Medibank Health Telehealth CGU. In case of Health insurance, the

company uses the recoverable amount that is determined based on the value-in-use. The value-

in-use is determined based on the cash flow projections that are derived from the corporate plans

of the management of the company. Any cash flow beyond the corporate plans are analyzed

based on the estimated growth rates (Norberg, 2018).

In case of Medibank Health Telehealth CGU, the recoverable amount is calculated based on the

value in use that is calculated based on the one-year projections that are done by the

management.

Apart from goodwill none of the assets of the company are tested for impairment, other

intangibles like the software are carried at cost less accumulated amortization and impairment

losses. Customer contracts and relationships that are acquired by the company are recorded at

their fair value. In case of such assets, they are often accessed for impairments in case there is a

change in events that indicates that the carrying amount will not be recovered by the company

(Kaufmann, 2017). The major assumption that is done by the management in this regard is

assessing the overall contracts of the customer, assumptions are made on the renewal of these

contracts, cash flow associated with these contracts, long term plans of the organization. So, we

see that impairment testing plays an important role in determining the accurate value of the

assets that a company might be holding especially for intangible assets that includes the goodwill

(Johan, 2018).

Question 3d)

The necessary disclosures regarding impairment has been made in the notes to accounts of the

company, where the details of the assets that have been tested, the overall methods that have

been adopted by the company, the different assumptions that are done by the company in

Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculation of the recoverable amount of depreciation and the necessary accounting standards

that have been followed by the company in this impairment testing. All the necessary disclosures

have been given based on the impairment of assets AASB 136 (Cundill, Smart, & Wilson, 2017).

It highlights the key assumptions of the company in calculation of the carrying charges, the rates

on which the present value are calculated and the events and circumstances under which these

rates changes are also stated in the notes to account of the company (Schwarzbichler, Steiner, &

Turnheim, 2018).

Like we see in the figure stated below, the management of the company has disclosed the overall

trade and other receivable net of the allowance of the impairment losses of the company. Over

the year if we see that the allowance for impairment is and there is very less reduction in the

same. This allowance for impairment loss is stated so that in case there is any change in events or

circumstances then there should be a provision to deal with the same and in no case the carrying

amount of the assets should be more than the recoverable value of the assets (Boghossian, 2017).

Goodwill is the most important asset that is tested for impairment and the company provides

proper disclosures with regards to that in its notes to account. An extract from the same has been

attached below for further understanding –

Page 7

that have been followed by the company in this impairment testing. All the necessary disclosures

have been given based on the impairment of assets AASB 136 (Cundill, Smart, & Wilson, 2017).

It highlights the key assumptions of the company in calculation of the carrying charges, the rates

on which the present value are calculated and the events and circumstances under which these

rates changes are also stated in the notes to account of the company (Schwarzbichler, Steiner, &

Turnheim, 2018).

Like we see in the figure stated below, the management of the company has disclosed the overall

trade and other receivable net of the allowance of the impairment losses of the company. Over

the year if we see that the allowance for impairment is and there is very less reduction in the

same. This allowance for impairment loss is stated so that in case there is any change in events or

circumstances then there should be a provision to deal with the same and in no case the carrying

amount of the assets should be more than the recoverable value of the assets (Boghossian, 2017).

Goodwill is the most important asset that is tested for impairment and the company provides

proper disclosures with regards to that in its notes to account. An extract from the same has been

attached below for further understanding –

Page 7

In case of goodwill the CGU in which the goodwill is classified is expected to benefit from the

overall combination of the assets. There are two CGU in which the goodwill is categorized and

that includes Health Insurance CGU and Medibank Health Telehealth CGU. In case of Health

insurance, the company uses the recoverable amount that is resoluted based on the value-in-use.

The value-in-use is based on the cash flow projections that are derived from the corporate plans

of the management of the company. Any cash flow beyond the corporate plans are analyzed

based on the estimated growth rates (Deegan, 2014).

The key assumptions that are made by the company are also disclosed in the notes to accounts

for the users of the financial statements (Abdullah & Said, 2017). These key assumptions are

related to the growth rates and discount rates, the health insurance CGU, the Medibank Health

Telehealth CGU and the overall impact in case there are changes in any kind of situations and

events are also stated in the notes to account of the company. An extract from the same is

attached below:

The annual report of the company can be found at the below URL :

Page 8

overall combination of the assets. There are two CGU in which the goodwill is categorized and

that includes Health Insurance CGU and Medibank Health Telehealth CGU. In case of Health

insurance, the company uses the recoverable amount that is resoluted based on the value-in-use.

The value-in-use is based on the cash flow projections that are derived from the corporate plans

of the management of the company. Any cash flow beyond the corporate plans are analyzed

based on the estimated growth rates (Deegan, 2014).

The key assumptions that are made by the company are also disclosed in the notes to accounts

for the users of the financial statements (Abdullah & Said, 2017). These key assumptions are

related to the growth rates and discount rates, the health insurance CGU, the Medibank Health

Telehealth CGU and the overall impact in case there are changes in any kind of situations and

events are also stated in the notes to account of the company. An extract from the same is

attached below:

The annual report of the company can be found at the below URL :

Page 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

https://www.medibank.com.au/content/dam/retail/about-assets/pdfs/investor-

centre/annual-reports/Medibank_Annual_Report_2018.pdf

References

Abdullah, W., & Said, R. (2017). Religious, Educational Background and Corporate

Crime Tolerance by Accounting Professionals. State-of-the-Art Theories and

Empirical Evidence, 3(1), 129-149.

Boghossian, P. (2017). The Socratic method, defeasibility, and doxastic

responsibility. Educational Philosophy and Theory, 50(3), 244-253.

Cundill, G., Smart, P., & Wilson, H. (2017). Non‐financial Shareholder Activism: A

Process Model for Influencing Corporate Environmental and Social

Performance. International Journal of Management Reviews, 20(2), 606-626.

Deegan, C. (2014). Financial Accounting Theory (first ed.). Australia: McGraw-Hill

Education (Australia) Pty Ltd.

Johan, S. (2018). The Relationship Between Economic Value Added, Market Value

Added And Return On Cost Of Capital In Measuring Corporate Performance.

Jurnal Manajemen Bisnis dan Kewirausahaan, 3(1), 121-134.

Kaufmann, W. (2017). The Problem of Regulatory Unreasonableness (First ed.). New

York: Routledge.

Norberg, P. (2018). Bankers Bashing Back: Amoral CSR Justifications. Journal of

Business Ethics, 147(2), 401-418.

Schwarzbichler, M., Steiner, C., & Turnheim, D. (2018). Impairment of Assets (Fixed

Assets and Goodwill) (first ed.). New York: Springer Publication.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance

Management Systems. SAGE Journals, 30(1), 23-48.

Webster, T. (2017). Successful Ethical Decision-Making Practices from the

Professional Accountants' Perspective. ProQuest Dissertations Publishing,

3(1), 142-156.

Wendt, K. (2018). Positive Impact Investing: A Sustainable Bridge between Strategy,

Innovation, Change and Learning (first ed.). Switzerland: Springer.

Yadao, J. (2018). Forensic accountants and big data.

Page 9

centre/annual-reports/Medibank_Annual_Report_2018.pdf

References

Abdullah, W., & Said, R. (2017). Religious, Educational Background and Corporate

Crime Tolerance by Accounting Professionals. State-of-the-Art Theories and

Empirical Evidence, 3(1), 129-149.

Boghossian, P. (2017). The Socratic method, defeasibility, and doxastic

responsibility. Educational Philosophy and Theory, 50(3), 244-253.

Cundill, G., Smart, P., & Wilson, H. (2017). Non‐financial Shareholder Activism: A

Process Model for Influencing Corporate Environmental and Social

Performance. International Journal of Management Reviews, 20(2), 606-626.

Deegan, C. (2014). Financial Accounting Theory (first ed.). Australia: McGraw-Hill

Education (Australia) Pty Ltd.

Johan, S. (2018). The Relationship Between Economic Value Added, Market Value

Added And Return On Cost Of Capital In Measuring Corporate Performance.

Jurnal Manajemen Bisnis dan Kewirausahaan, 3(1), 121-134.

Kaufmann, W. (2017). The Problem of Regulatory Unreasonableness (First ed.). New

York: Routledge.

Norberg, P. (2018). Bankers Bashing Back: Amoral CSR Justifications. Journal of

Business Ethics, 147(2), 401-418.

Schwarzbichler, M., Steiner, C., & Turnheim, D. (2018). Impairment of Assets (Fixed

Assets and Goodwill) (first ed.). New York: Springer Publication.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance

Management Systems. SAGE Journals, 30(1), 23-48.

Webster, T. (2017). Successful Ethical Decision-Making Practices from the

Professional Accountants' Perspective. ProQuest Dissertations Publishing,

3(1), 142-156.

Wendt, K. (2018). Positive Impact Investing: A Sustainable Bridge between Strategy,

Innovation, Change and Learning (first ed.). Switzerland: Springer.

Yadao, J. (2018). Forensic accountants and big data.

Page 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.