Comprehensive Accounting and Finance Analysis: University Assignment

VerifiedAdded on 2023/01/18

|15

|3369

|27

Homework Assignment

AI Summary

This finance assignment delves into various aspects of accounting and finance. It begins with a calculation of the amount needed for a future sum, considering monthly compounding interest rates. The assignment then evaluates a project's financial viability using net present value and analyzes cash flows. It proceeds to assess the value of financial assets, including superannuation funds and share portfolios, and calculates monthly pension amounts. Furthermore, the assignment explores real interest rates, negative gearing, and their implications. It also covers investment risk, dividend imputation, and the calculation of monthly and annual returns for BHP Ltd, considering both Australian and international shareholders. The solution provides detailed calculations and explanations of the financial concepts involved.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................6

Question 3..................................................................................................................................7

References................................................................................................................................14

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................6

Question 3..................................................................................................................................7

References................................................................................................................................14

2ACCOUNTING AND FINANCE

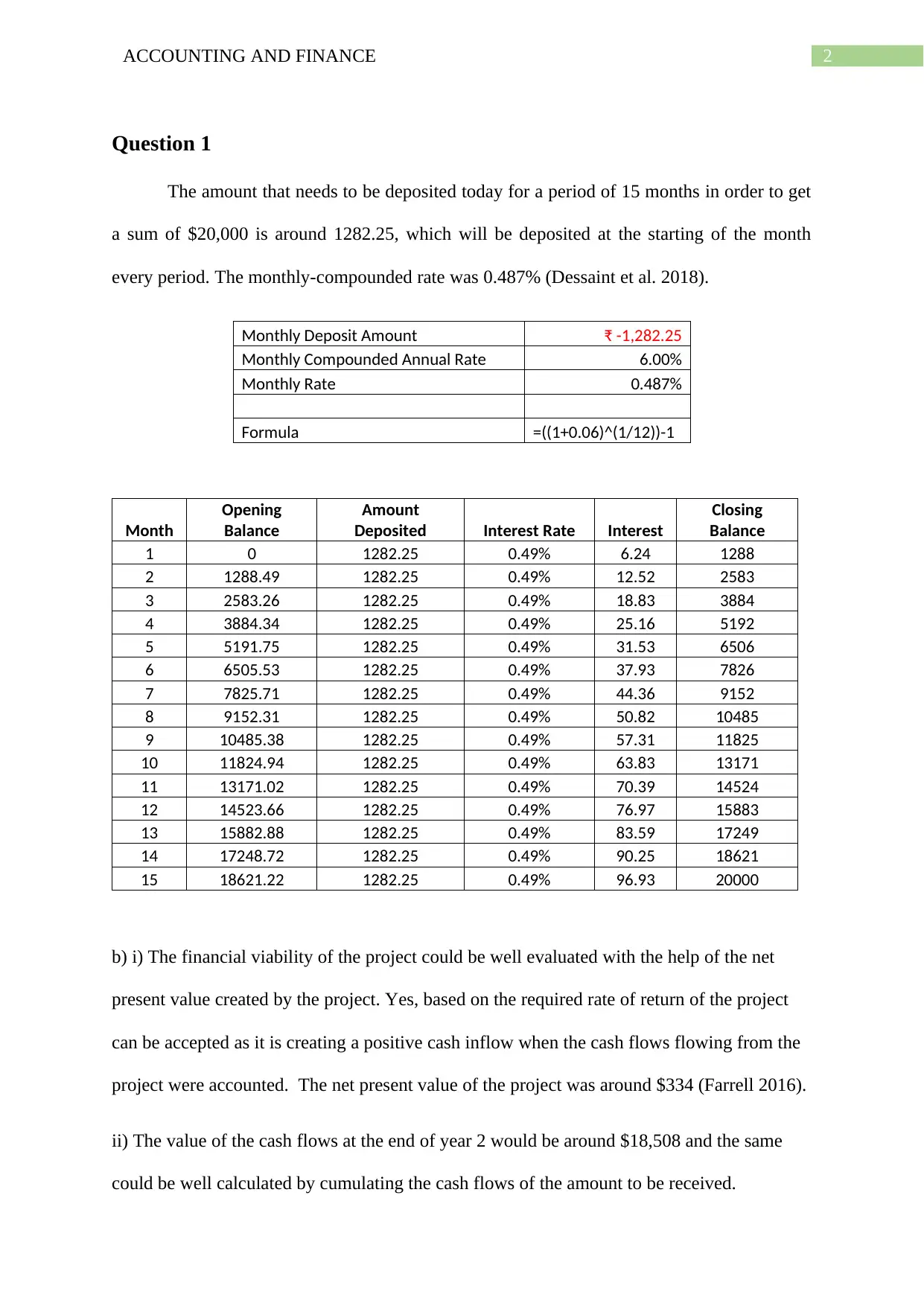

Question 1

The amount that needs to be deposited today for a period of 15 months in order to get

a sum of $20,000 is around 1282.25, which will be deposited at the starting of the month

every period. The monthly-compounded rate was 0.487% (Dessaint et al. 2018).

Monthly Deposit Amount ₹ -1,282.25

Monthly Compounded Annual Rate 6.00%

Monthly Rate 0.487%

Formula =((1+0.06)^(1/12))-1

Month

Opening

Balance

Amount

Deposited Interest Rate Interest

Closing

Balance

1 0 1282.25 0.49% 6.24 1288

2 1288.49 1282.25 0.49% 12.52 2583

3 2583.26 1282.25 0.49% 18.83 3884

4 3884.34 1282.25 0.49% 25.16 5192

5 5191.75 1282.25 0.49% 31.53 6506

6 6505.53 1282.25 0.49% 37.93 7826

7 7825.71 1282.25 0.49% 44.36 9152

8 9152.31 1282.25 0.49% 50.82 10485

9 10485.38 1282.25 0.49% 57.31 11825

10 11824.94 1282.25 0.49% 63.83 13171

11 13171.02 1282.25 0.49% 70.39 14524

12 14523.66 1282.25 0.49% 76.97 15883

13 15882.88 1282.25 0.49% 83.59 17249

14 17248.72 1282.25 0.49% 90.25 18621

15 18621.22 1282.25 0.49% 96.93 20000

b) i) The financial viability of the project could be well evaluated with the help of the net

present value created by the project. Yes, based on the required rate of return of the project

can be accepted as it is creating a positive cash inflow when the cash flows flowing from the

project were accounted. The net present value of the project was around $334 (Farrell 2016).

ii) The value of the cash flows at the end of year 2 would be around $18,508 and the same

could be well calculated by cumulating the cash flows of the amount to be received.

Question 1

The amount that needs to be deposited today for a period of 15 months in order to get

a sum of $20,000 is around 1282.25, which will be deposited at the starting of the month

every period. The monthly-compounded rate was 0.487% (Dessaint et al. 2018).

Monthly Deposit Amount ₹ -1,282.25

Monthly Compounded Annual Rate 6.00%

Monthly Rate 0.487%

Formula =((1+0.06)^(1/12))-1

Month

Opening

Balance

Amount

Deposited Interest Rate Interest

Closing

Balance

1 0 1282.25 0.49% 6.24 1288

2 1288.49 1282.25 0.49% 12.52 2583

3 2583.26 1282.25 0.49% 18.83 3884

4 3884.34 1282.25 0.49% 25.16 5192

5 5191.75 1282.25 0.49% 31.53 6506

6 6505.53 1282.25 0.49% 37.93 7826

7 7825.71 1282.25 0.49% 44.36 9152

8 9152.31 1282.25 0.49% 50.82 10485

9 10485.38 1282.25 0.49% 57.31 11825

10 11824.94 1282.25 0.49% 63.83 13171

11 13171.02 1282.25 0.49% 70.39 14524

12 14523.66 1282.25 0.49% 76.97 15883

13 15882.88 1282.25 0.49% 83.59 17249

14 17248.72 1282.25 0.49% 90.25 18621

15 18621.22 1282.25 0.49% 96.93 20000

b) i) The financial viability of the project could be well evaluated with the help of the net

present value created by the project. Yes, based on the required rate of return of the project

can be accepted as it is creating a positive cash inflow when the cash flows flowing from the

project were accounted. The net present value of the project was around $334 (Farrell 2016).

ii) The value of the cash flows at the end of year 2 would be around $18,508 and the same

could be well calculated by cumulating the cash flows of the amount to be received.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

End of

year

Cash flow

($,000)

Discount

Factor

Present

Value Cumulative Value

0

-

16,000 1.000

-

16,000

1

-

2,500 0.870

-

2,174

2 - 0.756 -

3

5,00

0 0.658

3,28

8

18,50

8

4

6,80

0 0.572

3,88

8

15,22

0

5

7,00

0 0.497

3,48

0

11,33

2

6

7,00

0 0.432

3,02

6

7,85

2

7

9,50

0 0.376

3,57

1

4,82

6

8

5,50

0 0.327

1,79

8

1,25

4

9

2,00

0 0.284

56

9

-

544

10

-

4,500 0.247

-

1,112

-

1,112

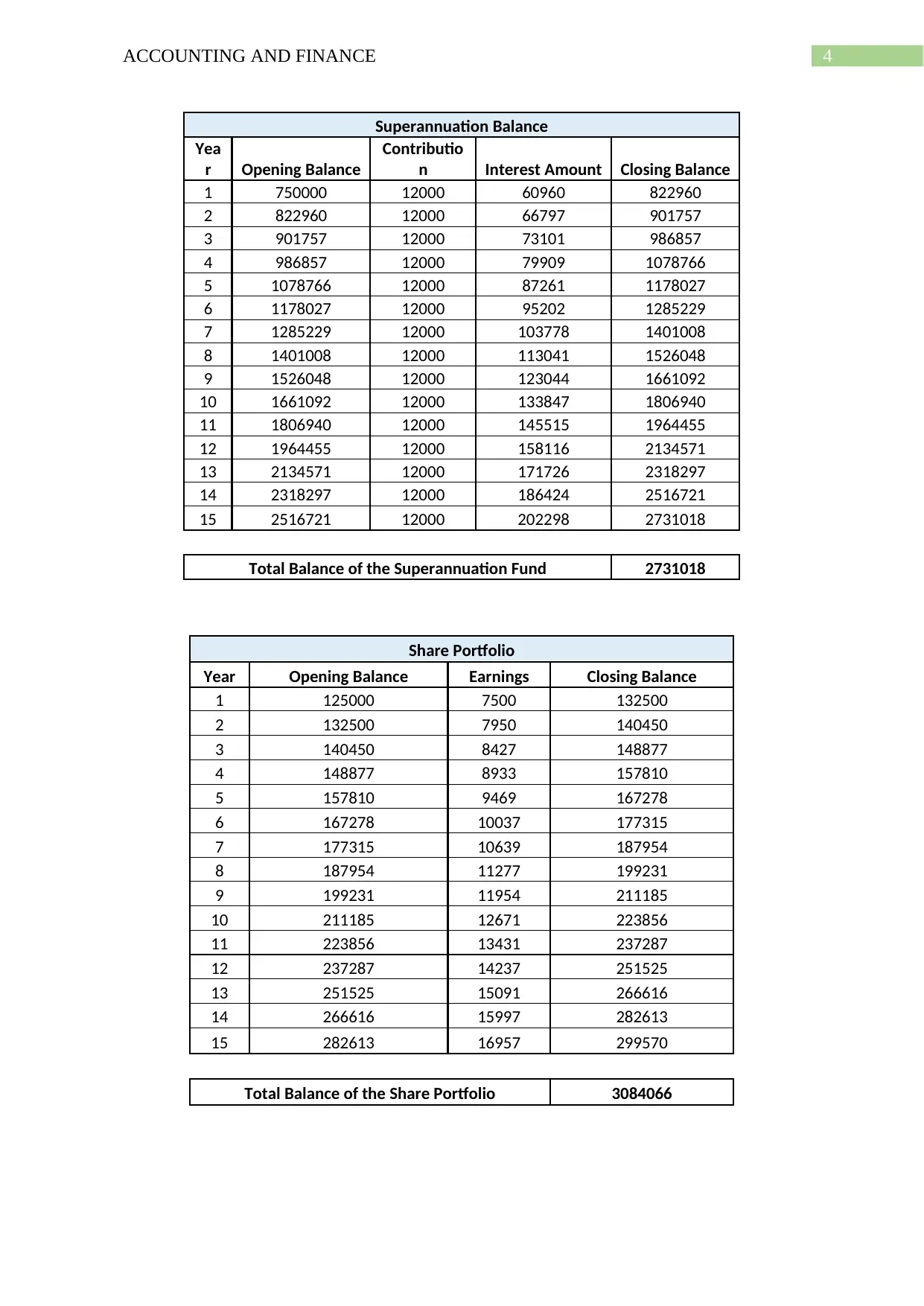

c) i) The value of the Gaye’s Financial Asset will be calculated with the help of the total

value earned by the share portfolio and the superannuation fund would be around $5,815,084.

In the case of superannuation fund, it is expected and assumed that the annual contribution

would be around 12,000 and the opening balance of the fund would be around 750,000 where

the fund would be earning 8% p.a. The value of the superannuation fund would be around

2,731,018. The share portfolio balance was around 125,000 and the portfolio is expected to

earn about 6% per annum continuously. Final closing balance at the end of 60 years for the

share portfolio would be around 3,084,066.

End of

year

Cash flow

($,000)

Discount

Factor

Present

Value Cumulative Value

0

-

16,000 1.000

-

16,000

1

-

2,500 0.870

-

2,174

2 - 0.756 -

3

5,00

0 0.658

3,28

8

18,50

8

4

6,80

0 0.572

3,88

8

15,22

0

5

7,00

0 0.497

3,48

0

11,33

2

6

7,00

0 0.432

3,02

6

7,85

2

7

9,50

0 0.376

3,57

1

4,82

6

8

5,50

0 0.327

1,79

8

1,25

4

9

2,00

0 0.284

56

9

-

544

10

-

4,500 0.247

-

1,112

-

1,112

c) i) The value of the Gaye’s Financial Asset will be calculated with the help of the total

value earned by the share portfolio and the superannuation fund would be around $5,815,084.

In the case of superannuation fund, it is expected and assumed that the annual contribution

would be around 12,000 and the opening balance of the fund would be around 750,000 where

the fund would be earning 8% p.a. The value of the superannuation fund would be around

2,731,018. The share portfolio balance was around 125,000 and the portfolio is expected to

earn about 6% per annum continuously. Final closing balance at the end of 60 years for the

share portfolio would be around 3,084,066.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

Superannuation Balance

Yea

r Opening Balance

Contributio

n Interest Amount Closing Balance

1 750000 12000 60960 822960

2 822960 12000 66797 901757

3 901757 12000 73101 986857

4 986857 12000 79909 1078766

5 1078766 12000 87261 1178027

6 1178027 12000 95202 1285229

7 1285229 12000 103778 1401008

8 1401008 12000 113041 1526048

9 1526048 12000 123044 1661092

10 1661092 12000 133847 1806940

11 1806940 12000 145515 1964455

12 1964455 12000 158116 2134571

13 2134571 12000 171726 2318297

14 2318297 12000 186424 2516721

15 2516721 12000 202298 2731018

Total Balance of the Superannuation Fund 2731018

Share Portfolio

Year Opening Balance Earnings Closing Balance

1 125000 7500 132500

2 132500 7950 140450

3 140450 8427 148877

4 148877 8933 157810

5 157810 9469 167278

6 167278 10037 177315

7 177315 10639 187954

8 187954 11277 199231

9 199231 11954 211185

10 211185 12671 223856

11 223856 13431 237287

12 237287 14237 251525

13 251525 15091 266616

14 266616 15997 282613

15 282613 16957 299570

Total Balance of the Share Portfolio 3084066

Superannuation Balance

Yea

r Opening Balance

Contributio

n Interest Amount Closing Balance

1 750000 12000 60960 822960

2 822960 12000 66797 901757

3 901757 12000 73101 986857

4 986857 12000 79909 1078766

5 1078766 12000 87261 1178027

6 1178027 12000 95202 1285229

7 1285229 12000 103778 1401008

8 1401008 12000 113041 1526048

9 1526048 12000 123044 1661092

10 1661092 12000 133847 1806940

11 1806940 12000 145515 1964455

12 1964455 12000 158116 2134571

13 2134571 12000 171726 2318297

14 2318297 12000 186424 2516721

15 2516721 12000 202298 2731018

Total Balance of the Superannuation Fund 2731018

Share Portfolio

Year Opening Balance Earnings Closing Balance

1 125000 7500 132500

2 132500 7950 140450

3 140450 8427 148877

4 148877 8933 157810

5 157810 9469 167278

6 167278 10037 177315

7 177315 10639 187954

8 187954 11277 199231

9 199231 11954 211185

10 211185 12671 223856

11 223856 13431 237287

12 237287 14237 251525

13 251525 15091 266616

14 266616 15997 282613

15 282613 16957 299570

Total Balance of the Share Portfolio 3084066

5ACCOUNTING AND FINANCE

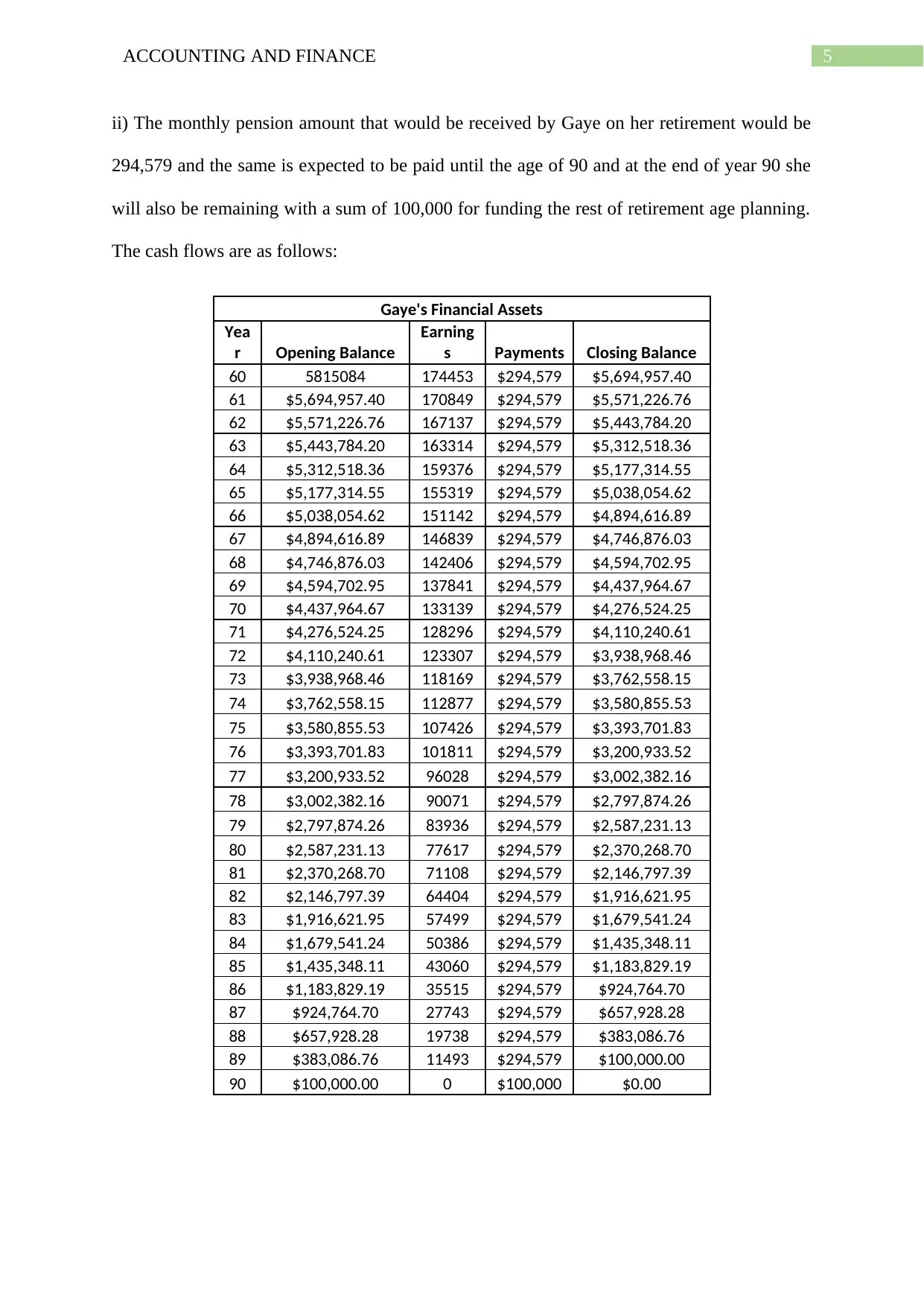

ii) The monthly pension amount that would be received by Gaye on her retirement would be

294,579 and the same is expected to be paid until the age of 90 and at the end of year 90 she

will also be remaining with a sum of 100,000 for funding the rest of retirement age planning.

The cash flows are as follows:

Gaye's Financial Assets

Yea

r Opening Balance

Earning

s Payments Closing Balance

60 5815084 174453 $294,579 $5,694,957.40

61 $5,694,957.40 170849 $294,579 $5,571,226.76

62 $5,571,226.76 167137 $294,579 $5,443,784.20

63 $5,443,784.20 163314 $294,579 $5,312,518.36

64 $5,312,518.36 159376 $294,579 $5,177,314.55

65 $5,177,314.55 155319 $294,579 $5,038,054.62

66 $5,038,054.62 151142 $294,579 $4,894,616.89

67 $4,894,616.89 146839 $294,579 $4,746,876.03

68 $4,746,876.03 142406 $294,579 $4,594,702.95

69 $4,594,702.95 137841 $294,579 $4,437,964.67

70 $4,437,964.67 133139 $294,579 $4,276,524.25

71 $4,276,524.25 128296 $294,579 $4,110,240.61

72 $4,110,240.61 123307 $294,579 $3,938,968.46

73 $3,938,968.46 118169 $294,579 $3,762,558.15

74 $3,762,558.15 112877 $294,579 $3,580,855.53

75 $3,580,855.53 107426 $294,579 $3,393,701.83

76 $3,393,701.83 101811 $294,579 $3,200,933.52

77 $3,200,933.52 96028 $294,579 $3,002,382.16

78 $3,002,382.16 90071 $294,579 $2,797,874.26

79 $2,797,874.26 83936 $294,579 $2,587,231.13

80 $2,587,231.13 77617 $294,579 $2,370,268.70

81 $2,370,268.70 71108 $294,579 $2,146,797.39

82 $2,146,797.39 64404 $294,579 $1,916,621.95

83 $1,916,621.95 57499 $294,579 $1,679,541.24

84 $1,679,541.24 50386 $294,579 $1,435,348.11

85 $1,435,348.11 43060 $294,579 $1,183,829.19

86 $1,183,829.19 35515 $294,579 $924,764.70

87 $924,764.70 27743 $294,579 $657,928.28

88 $657,928.28 19738 $294,579 $383,086.76

89 $383,086.76 11493 $294,579 $100,000.00

90 $100,000.00 0 $100,000 $0.00

ii) The monthly pension amount that would be received by Gaye on her retirement would be

294,579 and the same is expected to be paid until the age of 90 and at the end of year 90 she

will also be remaining with a sum of 100,000 for funding the rest of retirement age planning.

The cash flows are as follows:

Gaye's Financial Assets

Yea

r Opening Balance

Earning

s Payments Closing Balance

60 5815084 174453 $294,579 $5,694,957.40

61 $5,694,957.40 170849 $294,579 $5,571,226.76

62 $5,571,226.76 167137 $294,579 $5,443,784.20

63 $5,443,784.20 163314 $294,579 $5,312,518.36

64 $5,312,518.36 159376 $294,579 $5,177,314.55

65 $5,177,314.55 155319 $294,579 $5,038,054.62

66 $5,038,054.62 151142 $294,579 $4,894,616.89

67 $4,894,616.89 146839 $294,579 $4,746,876.03

68 $4,746,876.03 142406 $294,579 $4,594,702.95

69 $4,594,702.95 137841 $294,579 $4,437,964.67

70 $4,437,964.67 133139 $294,579 $4,276,524.25

71 $4,276,524.25 128296 $294,579 $4,110,240.61

72 $4,110,240.61 123307 $294,579 $3,938,968.46

73 $3,938,968.46 118169 $294,579 $3,762,558.15

74 $3,762,558.15 112877 $294,579 $3,580,855.53

75 $3,580,855.53 107426 $294,579 $3,393,701.83

76 $3,393,701.83 101811 $294,579 $3,200,933.52

77 $3,200,933.52 96028 $294,579 $3,002,382.16

78 $3,002,382.16 90071 $294,579 $2,797,874.26

79 $2,797,874.26 83936 $294,579 $2,587,231.13

80 $2,587,231.13 77617 $294,579 $2,370,268.70

81 $2,370,268.70 71108 $294,579 $2,146,797.39

82 $2,146,797.39 64404 $294,579 $1,916,621.95

83 $1,916,621.95 57499 $294,579 $1,679,541.24

84 $1,679,541.24 50386 $294,579 $1,435,348.11

85 $1,435,348.11 43060 $294,579 $1,183,829.19

86 $1,183,829.19 35515 $294,579 $924,764.70

87 $924,764.70 27743 $294,579 $657,928.28

88 $657,928.28 19738 $294,579 $383,086.76

89 $383,086.76 11493 $294,579 $100,000.00

90 $100,000.00 0 $100,000 $0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

Question 2

i) The real rate of interest is the type of interest rate an investor saver or the lender

expects to receive after considering the inflation factor into account. Real Interest

rate is calculated as Nominal Interest Rate- Inflation Rate or the expected

percentage of inflation rate. The importance of the real interest rate can be well

seen if in a given economy the level of inflation is about 5%, which might be too

high. However, if the prevailing interest rate is to be about 7% then there are

chances that the investors can still protect their money. Thus, the difference can be

well observed with the help of the given scenario. The client would be receiving

the annual real rate of interest from the investment, which is around 0.5% on the

sum of $100,000. If considering the factor for the real rate of interest, if the

interest rate increases then the client would be compensated in the form of higher

return (Hung, 2016).

ii) Negative gearing is the phenomenon where one borrows money and invests it in

income generating assets but the returns form the assets is less than the

repayments and the outgoings on those assets. One of the key advantage of the

negative gearing is that the losses are adjusted against all the other incomes that

reduces the total taxable income and hence the tax payable is reduced. The

wealthy Australians are using this concept in order to reduce their tax burdens and

thus they are getting an opportunity to inflate the house prices (Blunden, 2016).

The people having a stable income purchase houses by taking loan and they let it

to the other people. The rents that are charged might not meet the mortgage

amount of the loan. This would help them subsidise their taxable amount.

Negative gearing has become a deliberate investment strategy at present. The

wealthy people are intentionally running a house property at an operating loss.

Question 2

i) The real rate of interest is the type of interest rate an investor saver or the lender

expects to receive after considering the inflation factor into account. Real Interest

rate is calculated as Nominal Interest Rate- Inflation Rate or the expected

percentage of inflation rate. The importance of the real interest rate can be well

seen if in a given economy the level of inflation is about 5%, which might be too

high. However, if the prevailing interest rate is to be about 7% then there are

chances that the investors can still protect their money. Thus, the difference can be

well observed with the help of the given scenario. The client would be receiving

the annual real rate of interest from the investment, which is around 0.5% on the

sum of $100,000. If considering the factor for the real rate of interest, if the

interest rate increases then the client would be compensated in the form of higher

return (Hung, 2016).

ii) Negative gearing is the phenomenon where one borrows money and invests it in

income generating assets but the returns form the assets is less than the

repayments and the outgoings on those assets. One of the key advantage of the

negative gearing is that the losses are adjusted against all the other incomes that

reduces the total taxable income and hence the tax payable is reduced. The

wealthy Australians are using this concept in order to reduce their tax burdens and

thus they are getting an opportunity to inflate the house prices (Blunden, 2016).

The people having a stable income purchase houses by taking loan and they let it

to the other people. The rents that are charged might not meet the mortgage

amount of the loan. This would help them subsidise their taxable amount.

Negative gearing has become a deliberate investment strategy at present. The

wealthy people are intentionally running a house property at an operating loss.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

They are therefore being able to build an asset portfolio with the minimum efforts

and it would become cash positive in the long run. The practice of the negative

gearing has inflated the house prices in Australia every year. The investors used to

take loans from the bank by telling lies, generally termed as the liar loans (Cho, Li

& Uren 2017). This has reduced the faith of the customers on the Australian banks

as well. The risks involved in this concept have awakened the economy and there

has been changes in the Labour’s Policy, which is reducing the prices of the house

at present and making it affordable for the commoners of the country.

Question 3

i) Risk is a part of investment with which an investor gets an exposure of investing

and gathering return from a specified assets class. Risk and return are the key

integral part of an investment. Risk in terms of investment or the investment risk

shows the probability or the likelihood reflecting a percentage of loss relative to

the return earned by the investor (Muda & Hasibuan, 2018). No risk is not a bad

thing in-fact some risk is good when viewed from the context of portfolio

management. However, risk is solely determined by the characteristics of the asset

class in which the investor is invested. Every Financial instruments have some or

other kind of risk, investor wants compensation in the form of higher return for

higher risk taken. However, it is crucial to note that the risk and return of an

individual may vary depending on the financial goals and investment plans. It is

required the return to risk ratio should be optimally higher where the investor can

earn a high amount of investment profit from the same (García, 2017).

ii) Dividend Imputation or Franking Credit is a type of tax credit allowing the

Companies operating in the Australia to pass on the tax credit to the shareholders

of the company. Franking Credits or the Dividend imputation removes the effect

They are therefore being able to build an asset portfolio with the minimum efforts

and it would become cash positive in the long run. The practice of the negative

gearing has inflated the house prices in Australia every year. The investors used to

take loans from the bank by telling lies, generally termed as the liar loans (Cho, Li

& Uren 2017). This has reduced the faith of the customers on the Australian banks

as well. The risks involved in this concept have awakened the economy and there

has been changes in the Labour’s Policy, which is reducing the prices of the house

at present and making it affordable for the commoners of the country.

Question 3

i) Risk is a part of investment with which an investor gets an exposure of investing

and gathering return from a specified assets class. Risk and return are the key

integral part of an investment. Risk in terms of investment or the investment risk

shows the probability or the likelihood reflecting a percentage of loss relative to

the return earned by the investor (Muda & Hasibuan, 2018). No risk is not a bad

thing in-fact some risk is good when viewed from the context of portfolio

management. However, risk is solely determined by the characteristics of the asset

class in which the investor is invested. Every Financial instruments have some or

other kind of risk, investor wants compensation in the form of higher return for

higher risk taken. However, it is crucial to note that the risk and return of an

individual may vary depending on the financial goals and investment plans. It is

required the return to risk ratio should be optimally higher where the investor can

earn a high amount of investment profit from the same (García, 2017).

ii) Dividend Imputation or Franking Credit is a type of tax credit allowing the

Companies operating in the Australia to pass on the tax credit to the shareholders

of the company. Franking Credits or the Dividend imputation removes the effect

8ACCOUNTING AND FINANCE

of double taxation where taxation would not be charged at both the shareholder’s

and the investor’s level. The Australian Franking Credit would only be applicable

to the Australian Resident where they will be getting avoidance of double taxation

from the benefit of franking credits. The nonresident of Australia at the base case

would be applicable for a 30% of withholding tax on un-franked dividend.

However, if the resident resides in a tax treaty country than the effective tax rate

could come down to around 15% and may come to 0% depending on the profile of

the investors (Shrivastav, 2017). In the case of foreign investor, there would be

some restriction in getting or usage of the franking credit but on the other hand,

the domestic shareholders can easily use the franking credit for reducing the

effective tax rate of the company. Franking credit can be categorically divided

into three steps based on the release and identification of the same:

Immediate franking credits: Credits that will be received when the

company will pay the dividend.

Stockpiled franking credits: Planned Structured credits, which would be

given in special cases like share buyback and special dividends paid by the

company.

Future franking credits: The credit would be paid in future via the future

tax payments paid.

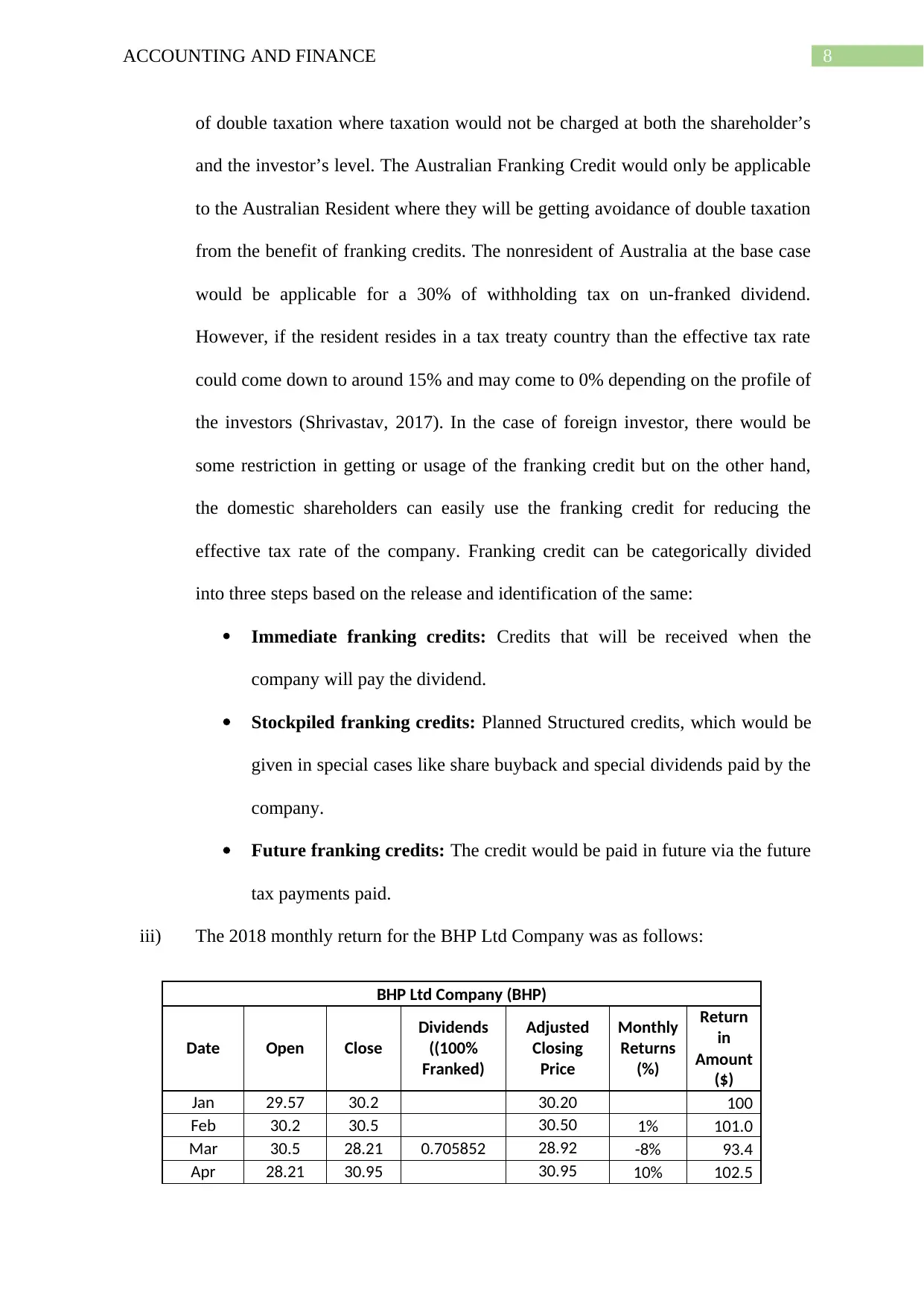

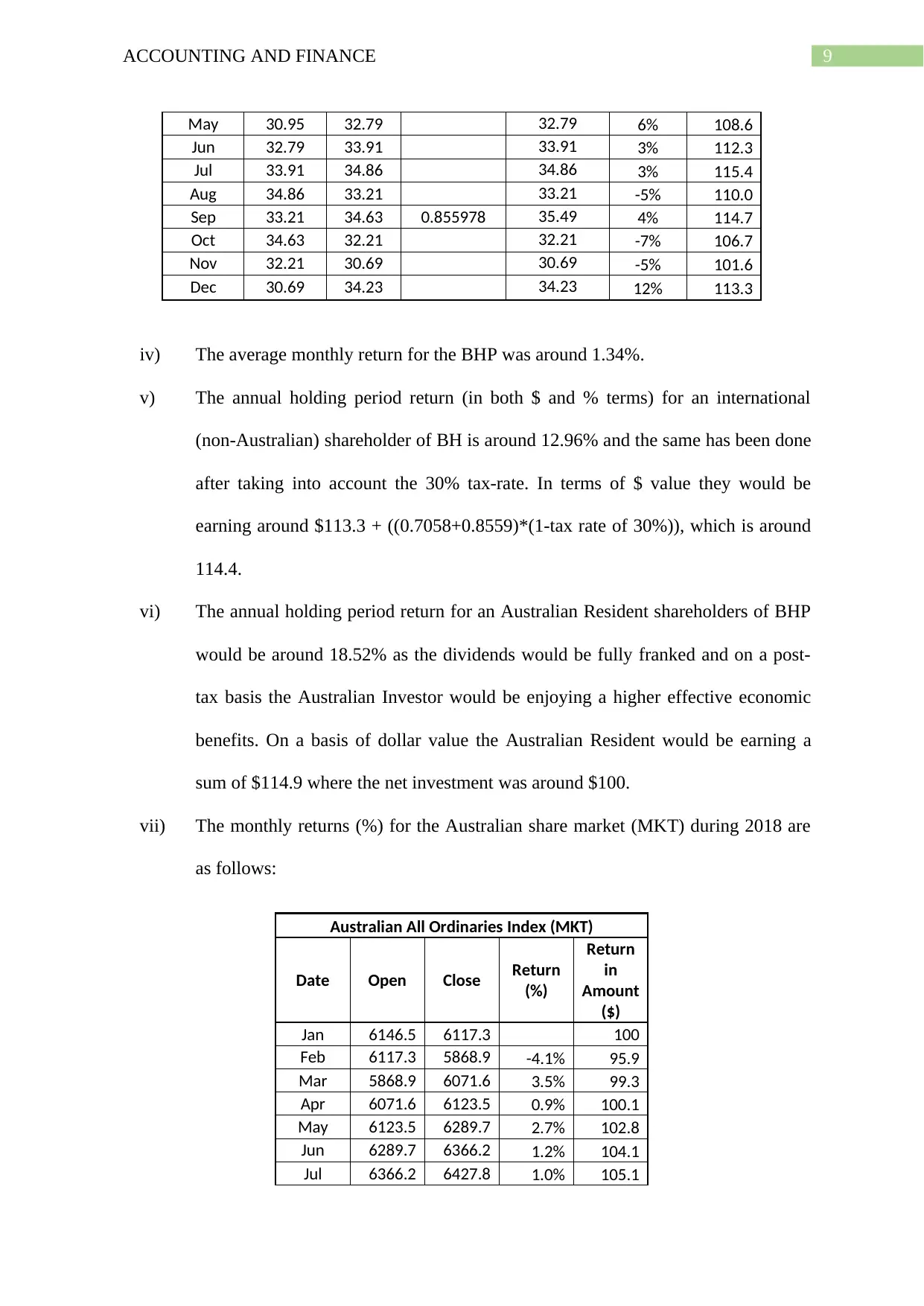

iii) The 2018 monthly return for the BHP Ltd Company was as follows:

BHP Ltd Company (BHP)

Date Open Close

Dividends

((100%

Franked)

Adjusted

Closing

Price

Monthly

Returns

(%)

Return

in

Amount

($)

Jan 29.57 30.2 30.20 100

Feb 30.2 30.5 30.50 1% 101.0

Mar 30.5 28.21 0.705852 28.92 -8% 93.4

Apr 28.21 30.95 30.95 10% 102.5

of double taxation where taxation would not be charged at both the shareholder’s

and the investor’s level. The Australian Franking Credit would only be applicable

to the Australian Resident where they will be getting avoidance of double taxation

from the benefit of franking credits. The nonresident of Australia at the base case

would be applicable for a 30% of withholding tax on un-franked dividend.

However, if the resident resides in a tax treaty country than the effective tax rate

could come down to around 15% and may come to 0% depending on the profile of

the investors (Shrivastav, 2017). In the case of foreign investor, there would be

some restriction in getting or usage of the franking credit but on the other hand,

the domestic shareholders can easily use the franking credit for reducing the

effective tax rate of the company. Franking credit can be categorically divided

into three steps based on the release and identification of the same:

Immediate franking credits: Credits that will be received when the

company will pay the dividend.

Stockpiled franking credits: Planned Structured credits, which would be

given in special cases like share buyback and special dividends paid by the

company.

Future franking credits: The credit would be paid in future via the future

tax payments paid.

iii) The 2018 monthly return for the BHP Ltd Company was as follows:

BHP Ltd Company (BHP)

Date Open Close

Dividends

((100%

Franked)

Adjusted

Closing

Price

Monthly

Returns

(%)

Return

in

Amount

($)

Jan 29.57 30.2 30.20 100

Feb 30.2 30.5 30.50 1% 101.0

Mar 30.5 28.21 0.705852 28.92 -8% 93.4

Apr 28.21 30.95 30.95 10% 102.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

May 30.95 32.79 32.79 6% 108.6

Jun 32.79 33.91 33.91 3% 112.3

Jul 33.91 34.86 34.86 3% 115.4

Aug 34.86 33.21 33.21 -5% 110.0

Sep 33.21 34.63 0.855978 35.49 4% 114.7

Oct 34.63 32.21 32.21 -7% 106.7

Nov 32.21 30.69 30.69 -5% 101.6

Dec 30.69 34.23 34.23 12% 113.3

iv) The average monthly return for the BHP was around 1.34%.

v) The annual holding period return (in both $ and % terms) for an international

(non-Australian) shareholder of BH is around 12.96% and the same has been done

after taking into account the 30% tax-rate. In terms of $ value they would be

earning around $113.3 + ((0.7058+0.8559)*(1-tax rate of 30%)), which is around

114.4.

vi) The annual holding period return for an Australian Resident shareholders of BHP

would be around 18.52% as the dividends would be fully franked and on a post-

tax basis the Australian Investor would be enjoying a higher effective economic

benefits. On a basis of dollar value the Australian Resident would be earning a

sum of $114.9 where the net investment was around $100.

vii) The monthly returns (%) for the Australian share market (MKT) during 2018 are

as follows:

Australian All Ordinaries Index (MKT)

Date Open Close Return

(%)

Return

in

Amount

($)

Jan 6146.5 6117.3 100

Feb 6117.3 5868.9 -4.1% 95.9

Mar 5868.9 6071.6 3.5% 99.3

Apr 6071.6 6123.5 0.9% 100.1

May 6123.5 6289.7 2.7% 102.8

Jun 6289.7 6366.2 1.2% 104.1

Jul 6366.2 6427.8 1.0% 105.1

May 30.95 32.79 32.79 6% 108.6

Jun 32.79 33.91 33.91 3% 112.3

Jul 33.91 34.86 34.86 3% 115.4

Aug 34.86 33.21 33.21 -5% 110.0

Sep 33.21 34.63 0.855978 35.49 4% 114.7

Oct 34.63 32.21 32.21 -7% 106.7

Nov 32.21 30.69 30.69 -5% 101.6

Dec 30.69 34.23 34.23 12% 113.3

iv) The average monthly return for the BHP was around 1.34%.

v) The annual holding period return (in both $ and % terms) for an international

(non-Australian) shareholder of BH is around 12.96% and the same has been done

after taking into account the 30% tax-rate. In terms of $ value they would be

earning around $113.3 + ((0.7058+0.8559)*(1-tax rate of 30%)), which is around

114.4.

vi) The annual holding period return for an Australian Resident shareholders of BHP

would be around 18.52% as the dividends would be fully franked and on a post-

tax basis the Australian Investor would be enjoying a higher effective economic

benefits. On a basis of dollar value the Australian Resident would be earning a

sum of $114.9 where the net investment was around $100.

vii) The monthly returns (%) for the Australian share market (MKT) during 2018 are

as follows:

Australian All Ordinaries Index (MKT)

Date Open Close Return

(%)

Return

in

Amount

($)

Jan 6146.5 6117.3 100

Feb 6117.3 5868.9 -4.1% 95.9

Mar 5868.9 6071.6 3.5% 99.3

Apr 6071.6 6123.5 0.9% 100.1

May 6123.5 6289.7 2.7% 102.8

Jun 6289.7 6366.2 1.2% 104.1

Jul 6366.2 6427.8 1.0% 105.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

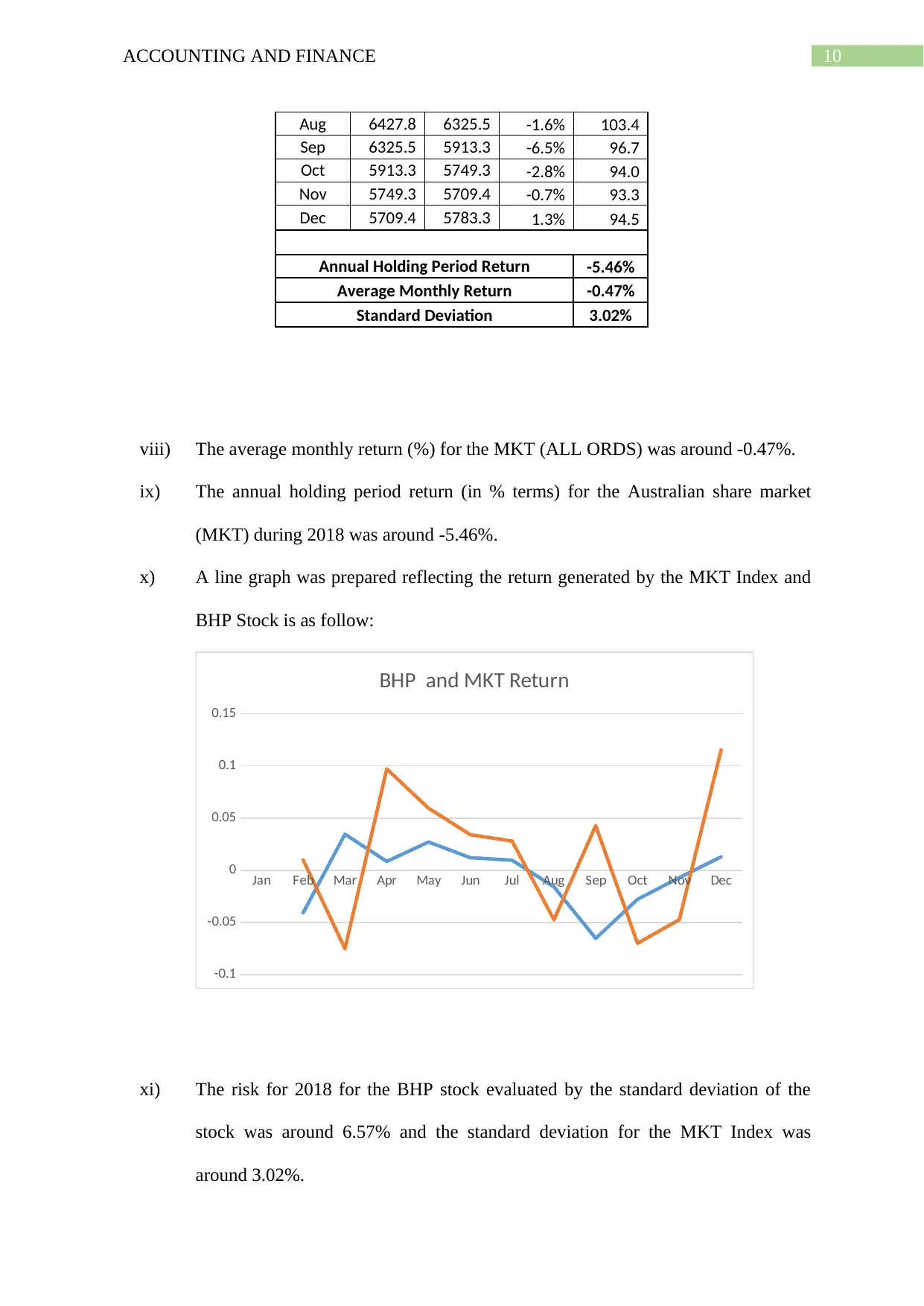

Aug 6427.8 6325.5 -1.6% 103.4

Sep 6325.5 5913.3 -6.5% 96.7

Oct 5913.3 5749.3 -2.8% 94.0

Nov 5749.3 5709.4 -0.7% 93.3

Dec 5709.4 5783.3 1.3% 94.5

Annual Holding Period Return -5.46%

Average Monthly Return -0.47%

Standard Deviation 3.02%

viii) The average monthly return (%) for the MKT (ALL ORDS) was around -0.47%.

ix) The annual holding period return (in % terms) for the Australian share market

(MKT) during 2018 was around -5.46%.

x) A line graph was prepared reflecting the return generated by the MKT Index and

BHP Stock is as follow:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-0.1

-0.05

0

0.05

0.1

0.15

BHP and MKT Return

xi) The risk for 2018 for the BHP stock evaluated by the standard deviation of the

stock was around 6.57% and the standard deviation for the MKT Index was

around 3.02%.

Aug 6427.8 6325.5 -1.6% 103.4

Sep 6325.5 5913.3 -6.5% 96.7

Oct 5913.3 5749.3 -2.8% 94.0

Nov 5749.3 5709.4 -0.7% 93.3

Dec 5709.4 5783.3 1.3% 94.5

Annual Holding Period Return -5.46%

Average Monthly Return -0.47%

Standard Deviation 3.02%

viii) The average monthly return (%) for the MKT (ALL ORDS) was around -0.47%.

ix) The annual holding period return (in % terms) for the Australian share market

(MKT) during 2018 was around -5.46%.

x) A line graph was prepared reflecting the return generated by the MKT Index and

BHP Stock is as follow:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-0.1

-0.05

0

0.05

0.1

0.15

BHP and MKT Return

xi) The risk for 2018 for the BHP stock evaluated by the standard deviation of the

stock was around 6.57% and the standard deviation for the MKT Index was

around 3.02%.

11ACCOUNTING AND FINANCE

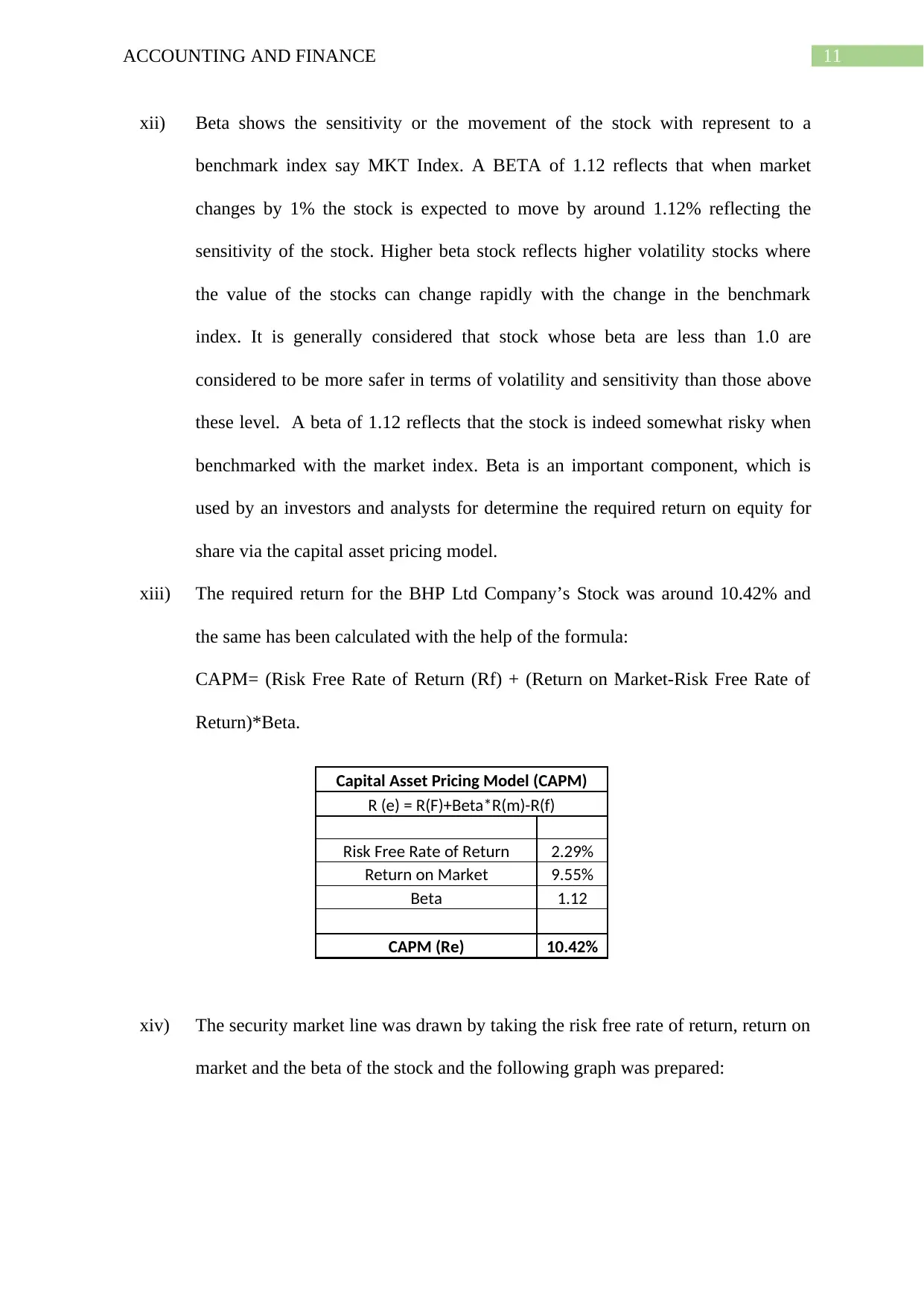

xii) Beta shows the sensitivity or the movement of the stock with represent to a

benchmark index say MKT Index. A BETA of 1.12 reflects that when market

changes by 1% the stock is expected to move by around 1.12% reflecting the

sensitivity of the stock. Higher beta stock reflects higher volatility stocks where

the value of the stocks can change rapidly with the change in the benchmark

index. It is generally considered that stock whose beta are less than 1.0 are

considered to be more safer in terms of volatility and sensitivity than those above

these level. A beta of 1.12 reflects that the stock is indeed somewhat risky when

benchmarked with the market index. Beta is an important component, which is

used by an investors and analysts for determine the required return on equity for

share via the capital asset pricing model.

xiii) The required return for the BHP Ltd Company’s Stock was around 10.42% and

the same has been calculated with the help of the formula:

CAPM= (Risk Free Rate of Return (Rf) + (Return on Market-Risk Free Rate of

Return)*Beta.

Capital Asset Pricing Model (CAPM)

R (e) = R(F)+Beta*R(m)-R(f)

Risk Free Rate of Return 2.29%

Return on Market 9.55%

Beta 1.12

CAPM (Re) 10.42%

xiv) The security market line was drawn by taking the risk free rate of return, return on

market and the beta of the stock and the following graph was prepared:

xii) Beta shows the sensitivity or the movement of the stock with represent to a

benchmark index say MKT Index. A BETA of 1.12 reflects that when market

changes by 1% the stock is expected to move by around 1.12% reflecting the

sensitivity of the stock. Higher beta stock reflects higher volatility stocks where

the value of the stocks can change rapidly with the change in the benchmark

index. It is generally considered that stock whose beta are less than 1.0 are

considered to be more safer in terms of volatility and sensitivity than those above

these level. A beta of 1.12 reflects that the stock is indeed somewhat risky when

benchmarked with the market index. Beta is an important component, which is

used by an investors and analysts for determine the required return on equity for

share via the capital asset pricing model.

xiii) The required return for the BHP Ltd Company’s Stock was around 10.42% and

the same has been calculated with the help of the formula:

CAPM= (Risk Free Rate of Return (Rf) + (Return on Market-Risk Free Rate of

Return)*Beta.

Capital Asset Pricing Model (CAPM)

R (e) = R(F)+Beta*R(m)-R(f)

Risk Free Rate of Return 2.29%

Return on Market 9.55%

Beta 1.12

CAPM (Re) 10.42%

xiv) The security market line was drawn by taking the risk free rate of return, return on

market and the beta of the stock and the following graph was prepared:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.